Valuing ASX Bank Stocks: What the Ratios Don’t Tell You

58 mins ago

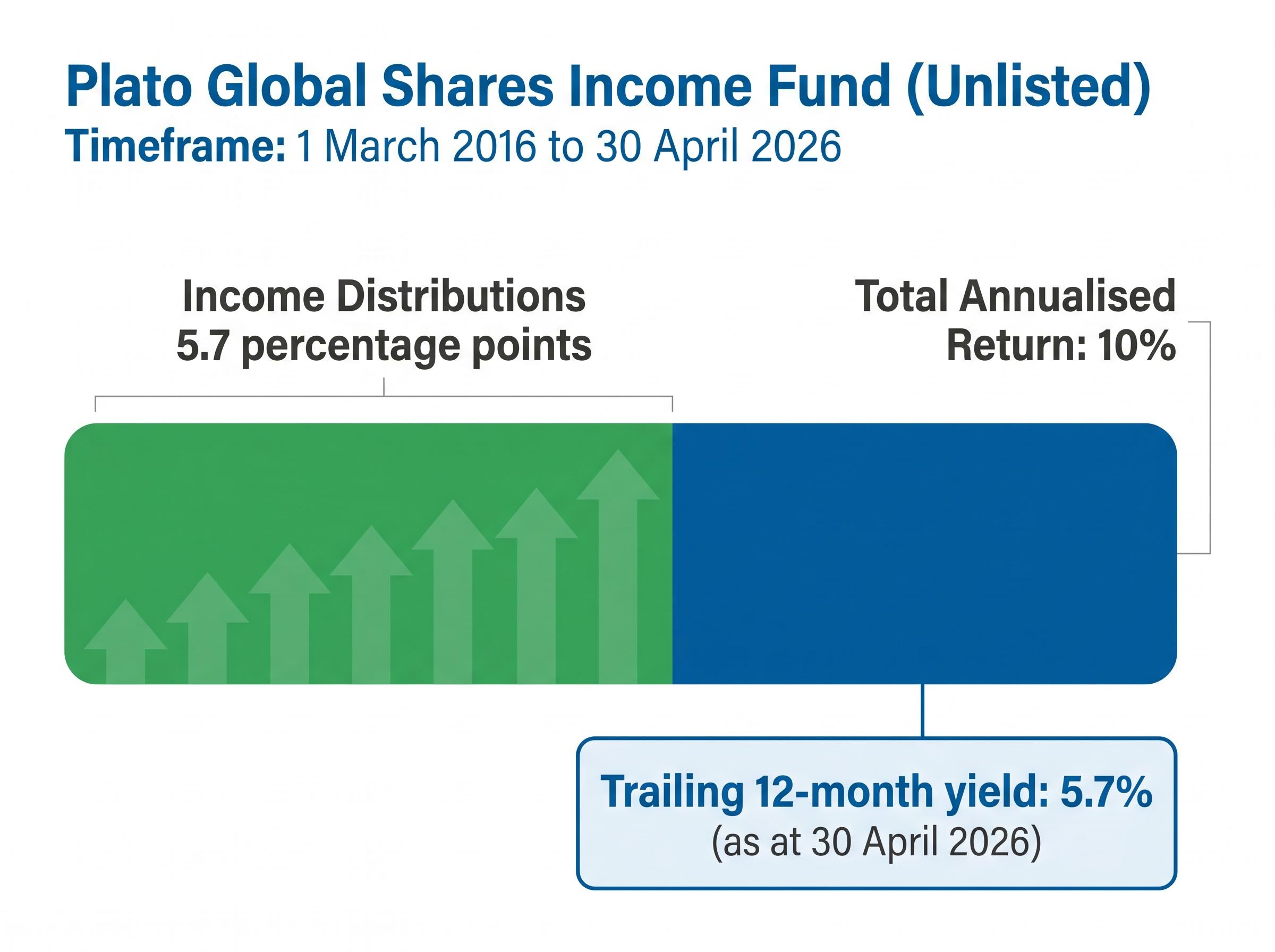

The unlisted strategy behind Plato Investment Management’s newest product has returned 10% per annum since March 2016, with 5.7 percentage points of that figure derived from income distributions alone. As of 19 May 2026, that same approach is available directly on the ASX. PGI2, the Plato Global Shares Income Fund Active ETF, gives Australian income investors access to an actively managed global dividend strategy through a single exchange-traded vehicle, a category that has been notably thin on the local market. With domestic dividend options concentrated heavily in banks and miners, and passive high-yield screens carrying well-documented concentration risks, the arrival of a global income-focused active ETF warrants close examination. What follows is an analysis of what PGI2 actually does, what its performance history suggests, how it compares to Plato’s existing PL8 vehicle, and what distinguishes active dividend selection from a passive yield screen.

PGI2 is an actively managed global equity income ETF that commenced trading on the ASX on 19 May 2026, with units opening at approximately $10.75. The fund’s stated objective is to generate income exceeding that of its benchmark, the MSCI World ex Australia Net Returns Unhedged Index, through active selection of global dividend-paying equities.

Fund objective: To surpass the income generated by the MSCI World ex Australia benchmark through active dividend selection across global markets.

The expected portfolio spans US technology, financials, consumer staples, and healthcare names alongside European and Asian holdings, though specific positions had not been publicly disclosed at listing. Key details at a glance:

That 0.85% fee is the first number income investors should weigh against the income premium the strategy aims to deliver over cheaper passive alternatives.

The distinction between active and passive dividend investing is not a branding exercise. It reflects a structural difference in how portfolios are built, and the consequences of that difference compound over time.

A yield trap occurs when a stock’s headline yield is high not because its dividends are strong, but because its share price has fallen sharply or its payout ratio has become unsustainable. Passive high-yield index ETFs apply mechanical screens, selecting stocks based on yield metrics alone. This process is structurally exposed to yield traps because it cannot distinguish between a genuinely high-yielding business and one whose dividend is about to be cut.

For Australian investors, the problem carries added context. Australia’s domestic dividend market is heavily weighted toward financials and resources sectors. Moving into global equities for diversification, only to land in a passive screen that concentrates in distressed yield names offshore, defeats the purpose.

Australian dividend ETFs such as VHY carry significant financials and resources weight by design, reflecting the composition of the domestic market, which is precisely the concentration problem that a global income allocation via PGI2 is intended to offset.

Active management adds discretionary portfolio construction: the ability to assess dividend sustainability, sector balance, and the quality of earnings backing each payout. The trade-off is higher fees and dependence on the consistency of the investment team.

Passive dividend screen risks extend beyond concentration in financials and utilities; during the February-March 2026 correction, high-dividend indexes provided only marginal downside cushion and then failed to participate fully in the subsequent recovery, a pattern that strengthens the case for active quality screening over mechanical yield selection.

| Dimension | Active global dividend ETF | Passive global dividend ETF |

|---|---|---|

| Selection method | Discretionary, based on earnings quality and dividend sustainability | Mechanical screen based on yield metrics |

| Concentration risk | Managed through portfolio construction | Can cluster in high-yield sectors |

| Fee level | Higher (e.g. 0.85% p.a.) | Lower (typically 0.25-0.50% p.a.) |

| Yield trap protection | Active screening for unsustainable payouts | No built-in protection |

PGI2 itself has no post-listing performance data. It commenced trading one day ago. The closest available proxy is the unlisted Plato Global Shares Income Fund, which shares the same strategy and has operated since 1 March 2016.

The numbers tell a specific story about where the return comes from. Presented in descending time horizon:

Since-inception performance: 10% per annum, with 5.7 percentage points from income distributions.

The income-versus-growth split is where the analytical weight sits. More than half of the strategy’s long-run return has come from dividends rather than capital appreciation. That makes the trailing 5.7% income yield the central proposition, not the 19.2% three-year figure, which reflects a favourable market period that may not persist.

The distinction between dividend yield and total return matters here because the unlisted fund’s since-inception figure of 10% per annum embeds both the 5.7 percentage point income component and residual capital growth, and conflating the two can lead investors to overweight the income figure in isolation.

All figures are drawn from the unlisted managed fund. They represent the strategy’s historical capability, not a guarantee that PGI2 will replicate them at the ETF level.

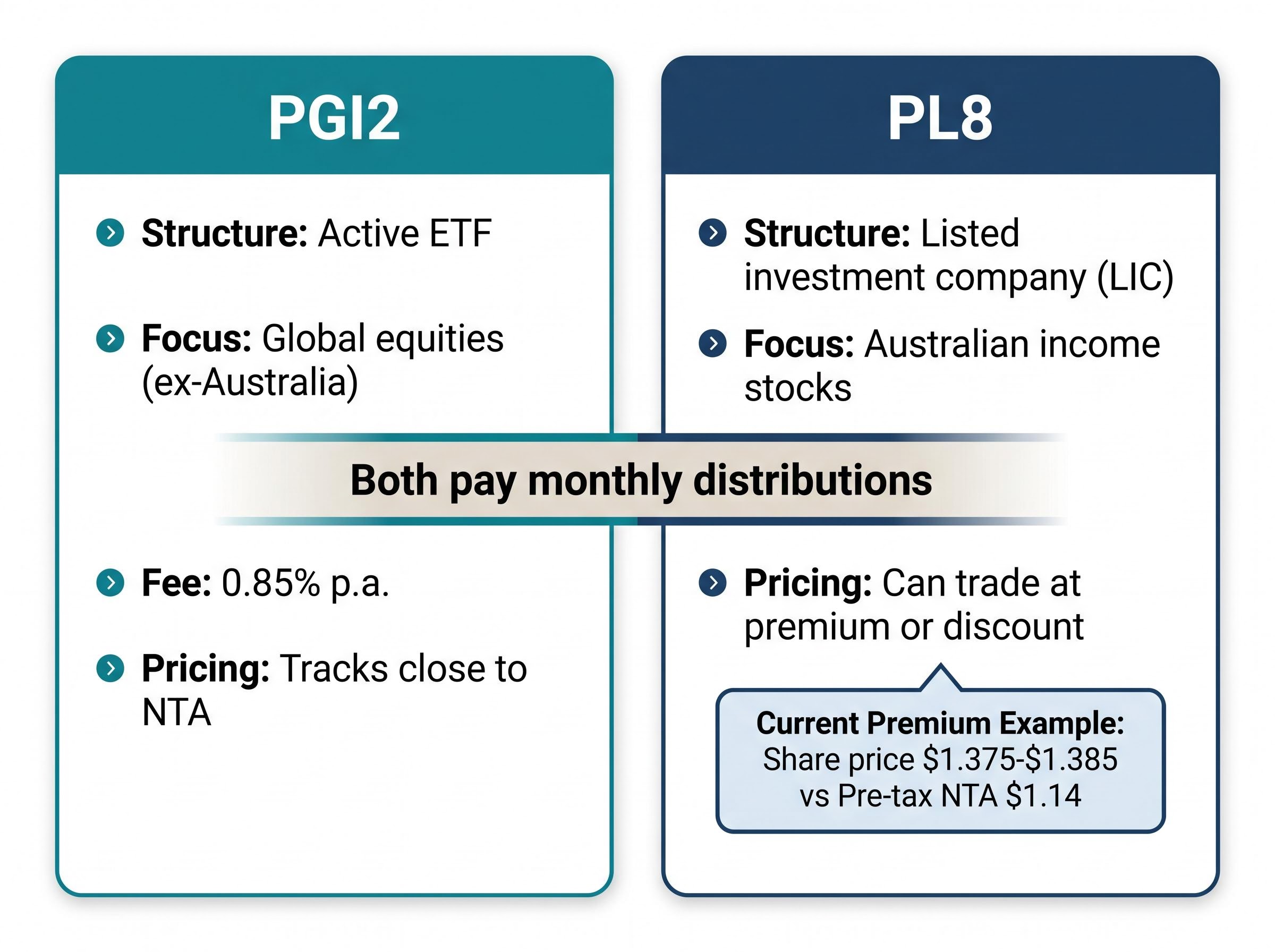

Income investors already holding PL8, the Plato Income Maximiser, may wonder whether PGI2 adds genuine diversification or simply doubles their Plato exposure. The answer turns on structure and geography.

PGI2 is an active ETF, meaning the fund itself holds the underlying global securities directly. Its market price tracks net asset value (NTA) closely through the creation and redemption mechanism that ETFs use. PL8 is a listed investment company (LIC), meaning investors buy shares in a company whose portfolio value can trade at a premium or discount to NTA.

ASIC Regulatory Guide RG 282 establishes the framework governing exchange-traded products in Australia, including the creation and redemption mechanism that keeps an active ETF’s market price closely aligned with its net asset value, a structural feature that directly distinguishes PGI2 from a LIC like PL8.

That distinction matters right now. PL8’s share price of approximately $1.375-$1.385 sits at a premium to its pre-tax NTA of approximately $1.14, a structural dynamic that does not apply to an ETF.

| Dimension | PGI2 | PL8 |

|---|---|---|

| Structure | Active ETF | Listed investment company (LIC) |

| Investment universe | Global equities (ex-Australia) | Australian income stocks |

| Distribution frequency | Monthly | Monthly |

| Management fee | 0.85% p.a. | Varies; refer to PDS |

| NTA tracking | Close to NTA (ETF mechanism) | Can trade at premium or discount to NTA |

Both pay monthly distributions, but the geographic separation is clear. PGI2 targets global equities while PL8 focuses on Australian income stocks. For investors seeking both domestic and international income exposure, the two products sit in complementary rather than competing roles.

PGI2 suits a specific investor profile: those seeking monthly global income with geographic diversification away from Australia’s bank-heavy dividend market, who are comfortable paying an active management fee for dividend quality screening.

The unlisted fund’s decade-long track record provides genuine evidence that the strategy can deliver an income yield above 5%. For Australian investors whose global sleeve currently relies on passive yield screens, PGI2 offers a structurally different approach.

For investors who are evaluating PGI2 as part of a broader international allocation rather than as a standalone income solution, our dedicated guide to building a global ASX portfolio compares IVV, IXI, and VGS across costs, returns, and portfolio fit, providing context on where an active income fund sits relative to passive global equity options.

The 0.85% management fee is higher than passive alternatives and must be justified by the income premium the active strategy delivers over time. Active returns can lag during growth-led market cycles when high-yielding stocks underperform faster-growing names.

No post-listing ETF data yet exists. The unlisted fund track record is a proxy, not a guarantee that PGI2 will replicate those figures at the ETF level.

Practical monitoring points for the coming months:

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

PGI2 gives Australian income investors their first actively managed global dividend ETF option on the ASX, backed by a decade-long unlisted track record that shows both the income potential and the strategy’s genuine orientation toward yield over pure capital growth.

The central tension is straightforward. The 0.85% active management fee is the price of dividend quality screening, and the first distribution announcements will be the earliest signal of whether the ETF version delivers on the unlisted fund’s 5.7% income track record. Until those announcements arrive, the investment case rests on strategy design and historical evidence rather than confirmed ETF-level results. Income investors considering PGI2 are directed to the Plato fund page and official PDS for current holdings disclosure and full cost documentation as the fund matures into its listed life.

PGI2 is the Plato Global Shares Income Fund Active ETF, listed on the ASX on 19 May 2026. It actively selects global dividend-paying equities outside Australia with the objective of generating income exceeding the MSCI World ex Australia benchmark, paying monthly distributions at a management fee of 0.85% per annum.

A yield trap occurs when a stock's high headline dividend yield reflects a falling share price or unsustainable payout rather than genuine income strength. Active managers like Plato assess dividend sustainability and earnings quality, whereas passive high-yield screens apply mechanical filters that have no built-in protection against selecting stocks whose dividends are about to be cut.

PGI2 itself has no post-listing performance data, but it shares the same strategy as the unlisted Plato Global Shares Income Fund, which has returned 10% per annum since inception on 1 March 2016, with 5.7 percentage points of that return derived from income distributions and a trailing 12-month yield of 5.7% as at 30 April 2026.

PGI2 is an active ETF targeting global equities outside Australia, meaning its market price stays closely aligned with net asset value through the ETF creation and redemption mechanism. PL8 is a listed investment company focused on Australian income stocks and can trade at a premium or discount to its net asset value, a structural difference that is currently material given PL8 trades at a premium to its pre-tax NTA.

Investors should watch the first monthly distribution announcement to confirm whether the ETF delivers a yield consistent with the unlisted fund's 5.7% income track record, review the full PDS at plato.com.au for buy-sell spread and indirect cost disclosures, and track quarterly performance against the MSCI World ex Australia benchmark.