On 15 May 2026, two companies caused a national stock index to fall more than 6% in a single session. Not two sectors. Not a macro shock. Two stocks.

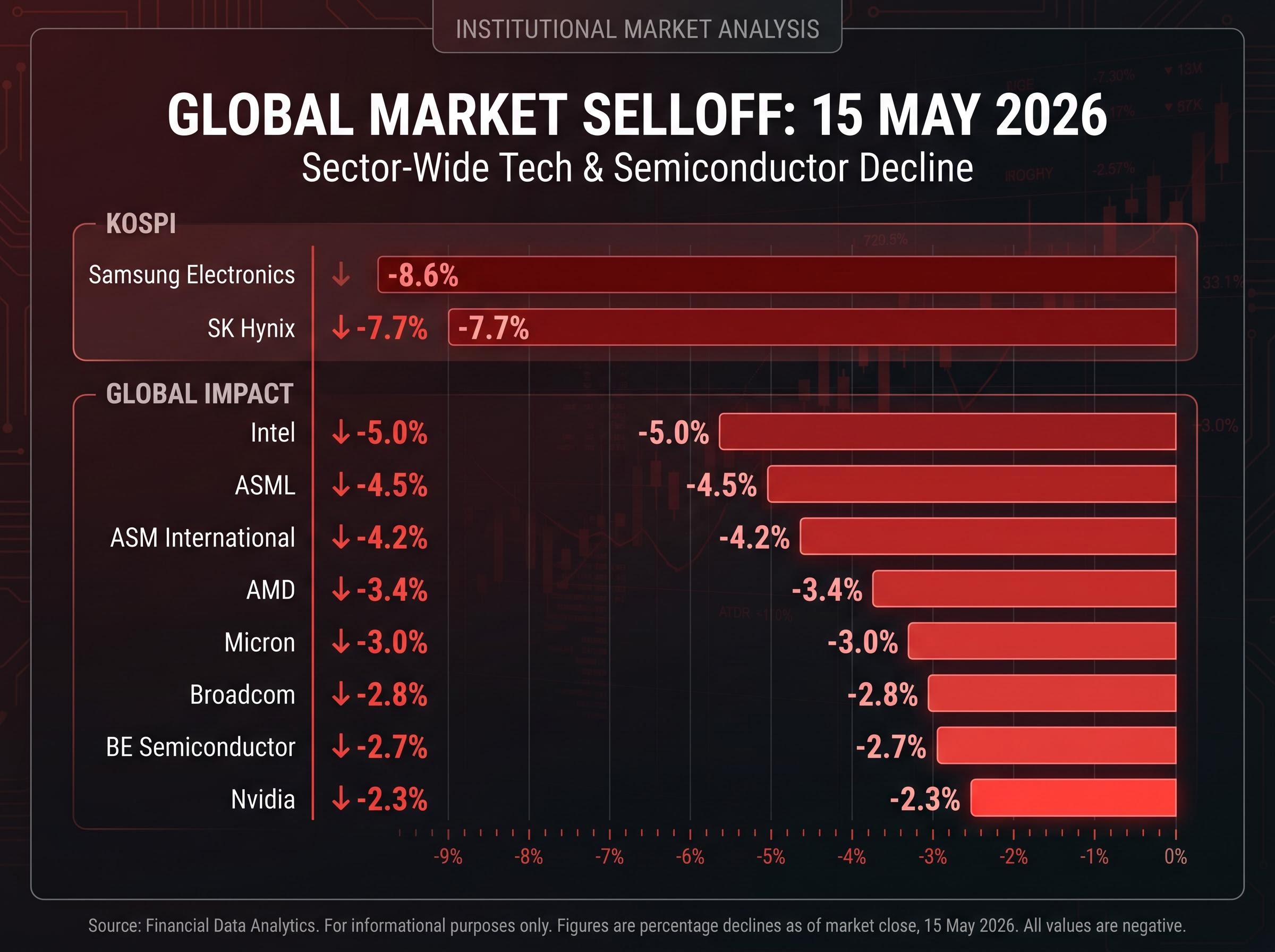

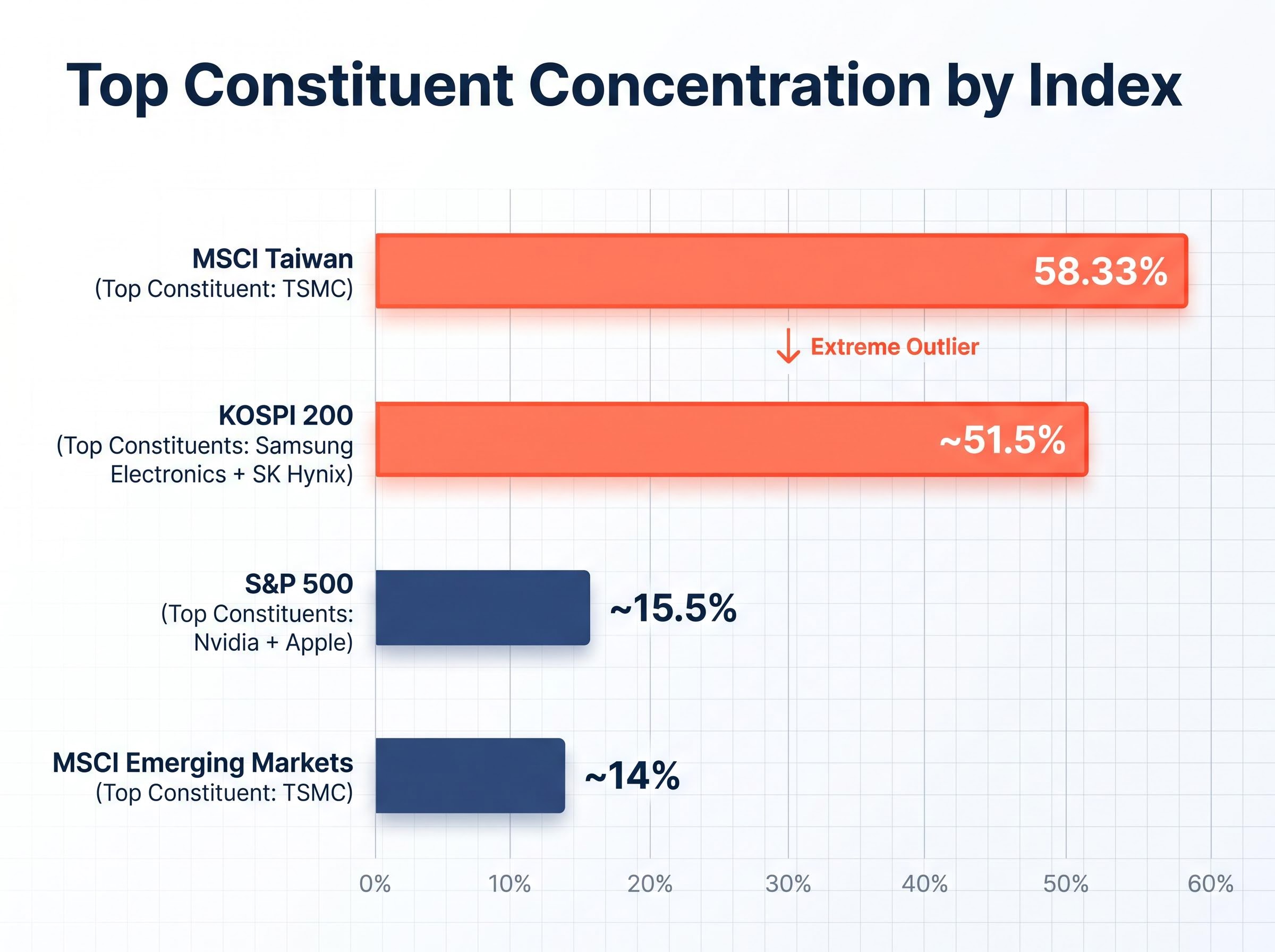

The KOSPI’s collapse that day was triggered by Samsung Electronics shedding 8.6% and SK Hynix falling 7.7%, after Samsung’s labour union confirmed an 18-day strike beginning 21 May. In isolation, a labour dispute at one company should not move a country’s entire equity benchmark by a percentage point, let alone six. That it did reveals something structural: Samsung and SK Hynix together carry a combined weight of approximately 42.2% in the KOSPI, according to Manulife Investment Management, with Korean financial sources citing figures as high as 51.5-52% in the KOSPI 200 specifically. That is not normal index construction. It is index concentration risk made visible in real time.

This explainer unpacks what index concentration risk actually means, how index weighting mechanics create it, why passive investors and ETF holders are exposed in ways they may not fully appreciate, and what the KOSPI selloff reveals about the broader problem of concentrated emerging market indices.

How two stocks came to control nearly half of South Korea’s benchmark

South Korea’s stock market gained approximately 75% year-to-date as of 6 May 2026, according to MarketWatch and Morningstar. The driver was not broad-based economic expansion. It was semiconductors, and specifically the AI-fuelled memory supercycle that pushed Samsung Electronics to a $1 trillion market capitalisation and lifted SK Hynix alongside it.

As both companies grew, their float-adjusted market capitalisations swelled relative to every other KOSPI constituent. No index committee decided to concentrate the benchmark in two names. The concentration accumulated organically, one trading session at a time, as semiconductor stocks outperformed every other sector during the AI investment cycle.

By mid-May, the scale of that accumulation was striking:

- Samsung Electronics weighting: the single largest KOSPI constituent by a wide margin

- SK Hynix weighting: the second-largest, driven by its position as a leading high-bandwidth memory supplier

- Combined weight: approximately 42.2% (Manulife Investment Management) to 51.5-52% (Korean financial press, KOSPI 200, 13-14 May 2026)

- KOSPI decline on 15 May: more than 6%, from a record high above 8,000

- Samsung Electronics: -8.6% on the day; SK Hynix: -7.7%

Manulife Investment Management cited a combined Samsung and SK Hynix weighting of approximately 42.2% in the KOSPI, a figure repeated across financial media coverage on 15 May 2026 as the concentration dynamic driving the selloff became clear.

The difference between the 42.2% and 51.5-52% figures reflects scope and timing. The Manulife figure likely represents an earlier or differently calculated baseline. Korean financial sources, including Asia Economy’s 14 May 2026 analysis, placed the KOSPI 200 concentration at the higher end of the range. Both figures describe the same underlying problem at different scales: two companies controlling between four-tenths and half of a national equity benchmark.

Any investor holding a South Korea ETF was, in practice, holding a leveraged semiconductor position.

When big ASX news breaks, our subscribers know first

What index concentration risk actually means and why it matters

Index concentration risk is the condition where a small number of constituents account for a disproportionate share of an index’s total weight. When that condition exists, events affecting those few stocks behave like systemic market events, even when the underlying catalyst is company-specific.

The distinction matters because most investors treat index ownership as diversified ownership. A fund tracking an index with 200 or 800 constituents sounds diversified. If two of those constituents represent half the index’s total weight, however, the fund’s performance is dominated by what happens to those two names. The label says “market.” The exposure says “concentrated bet.”

ETF ownership mechanics explain why the diversification label on a fund does not guarantee diversification in practice: the fund holds what the index holds, in the proportions the index dictates, meaning a two-stock concentration problem in the underlying index becomes a two-stock concentration problem in every ETF that tracks it.

The KOSPI on 15 May demonstrated this in real time. If Samsung and SK Hynix together account for approximately 50% of the index, an 8% decline in both stocks produces a roughly 4-percentage-point drag on the index before any other constituent moves. The actual KOSPI decline exceeded 6%, reflecting additional negative momentum across other holdings as selling pressure spread.

The self-reinforcing mechanics of market-cap weighting

Market-cap weighting creates concentration through a self-reinforcing loop:

- A stock’s price rises, increasing its market capitalisation and its proportional weight in the index

- Passive funds tracking the index must buy more shares of that stock to match its increased weight, adding further buying pressure

- The additional buying pressure supports the stock’s price, which increases its weight further, restarting the cycle

This dynamic works symmetrically on the downside. Falling prices reduce a stock’s index weight, forcing passive funds to sell proportionally, which can amplify the decline. On 15 May, with foreign investors holding 38% of the KOSPI largely through index-tracking products, this downside amplification was visible in the speed and scale of the selloff.

When a labour strike becomes a market-wide event: the transmission mechanism unpacked

The catalyst was specific and contained: Samsung Electronics’ labour union confirmed an 18-day strike planned to begin 21 May 2026, after negotiations broke down. As of 15 May, no settlement had been reached and the union planned to proceed unless a new offer was made.

A labour dispute at a single company, even one as large as Samsung, should not move an entire national benchmark by 6% in a single session. The transmission mechanism that turned a company-level catalyst into an index-level shock was structural, not fundamental.

Samsung’s weight in the KOSPI meant that its 8.6% decline on 15 May mechanically dragged the index. SK Hynix, exposed to the same semiconductor supply chain concerns, fell 7.7%. Together, their combined decline accounted for the majority of the index-level move before broader selling pressure compounded the damage.

Foreign investors held 38% of the KOSPI as of 13 May 2026, with exposure channelled largely through index-tracking ETFs and passive products. That ownership structure meant a domestic Korean labour dispute triggered programmatic selling across international portfolios.

As the KOSPI fell, ETF redemptions forced additional selling of all index constituents, amplifying the decline beyond what Samsung and SK Hynix alone would have produced. The contagion then moved internationally. On 15 May, global semiconductor stocks fell in sympathy as markets repriced supply chain disruption risk:

ETF redemption mechanics explain why index-level declines tend to accelerate beyond what the initial catalyst warrants: as the index falls, redemptions force fund managers to sell all constituents proportionally, pushing prices lower across holdings that have no direct connection to the original shock and creating a feedback loop between passive flows and market prices.

| Company | Exchange / Market | Decline (%) |

|---|---|---|

| Samsung Electronics | KOSPI (South Korea) | -8.6% |

| SK Hynix | KOSPI (South Korea) | -7.7% |

| Intel | NASDAQ (US) | -5.0% |

| ASML | Euronext (Netherlands) | -4.5% |

| ASM International | Euronext (Netherlands) | -4.2% |

| AMD | NASDAQ (US) | -3.4% |

| Micron | NASDAQ (US) | -3.0% |

| Broadcom | NASDAQ (US) | -2.8% |

| BE Semiconductor | Euronext (Netherlands) | -2.7% |

| Nvidia | NASDAQ (US) | -2.3% |

U.S.-Iran tensions over the Strait of Hormuz added a layer of geopolitical unease on the same day, compounding the risk-off sentiment. The coincidence of a supply chain shock and a geopolitical shock in the same session amplified selling beyond what concentration alone would have produced.

The transmission chain, from Samsung union announcement to KOSPI collapse to global semiconductor repricing, was mechanical and, given the index’s construction, inevitable. Global investors who had never examined a KOSPI constituent list were selling semiconductors that same morning.

South Korea is not alone: index concentration across global markets

The KOSPI’s two-stock concentration problem is not an isolated anomaly. It sits on a spectrum, and some of the world’s most widely held indices occupy positions on that spectrum that may surprise investors who assume passive exposure is inherently diversified.

TSMC held a 58.33% weighting in the MSCI Taiwan Index as of 14 May 2026. A single company’s share of that index exceeds the entire combined Samsung and SK Hynix figure in the KOSPI. The second-largest constituent in the MSCI Taiwan Index is estimated at approximately 2-3%, meaning TSMC’s dominance is not merely large; it is without meaningful counterbalance.

At the other end of the spectrum, the S&P 500’s top two constituents, Nvidia at 8.59% and Apple at 6.87% (as of 30 April 2026), combine for approximately 15.5%. That is still meaningful concentration, but it is structurally different from an index where two names account for half the total weight.

US mega-cap concentration has followed the same self-reinforcing trajectory, with five companies now controlling roughly 30% of total US equity market capitalisation, a level that exceeds the dot-com peak and that passive S&P 500 holders carry by default through their index allocation.

Japan’s Nikkei 225 presents a distinct case. Its price-weighted methodology (rather than market-cap weighted) creates different concentration dynamics. Fast Retailing is estimated at 10-12% and Tokyo Electron at 6-8%, though precise current figures require index provider confirmation.

Saudi Aramco’s dominance of the Tadawul index represents an analogous historical case of single-stock concentration in an emerging market context, where one company’s weight can reshape the entire index’s risk profile.

| Index | Market | Top Constituent(s) | Combined Top Weight (%) |

|---|---|---|---|

| KOSPI 200 | South Korea | Samsung Electronics + SK Hynix | ~51.5% |

| MSCI Taiwan | Taiwan | TSMC | 58.33% |

| S&P 500 | United States | Nvidia + Apple | ~15.5% |

| MSCI Emerging Markets | Global | TSMC | ~14% |

How single-stock concentration stacks inside broad EM funds

The MSCI Emerging Markets Index aggregates these individual country exposures into a single instrument. TSMC, with a market capitalisation of approximately $1.66 trillion, represents roughly 14% of the index’s approximately $11.68 trillion total value, making it the largest single constituent.

Investors who bought EM exposure for geographic diversification also bought meaningful TSMC concentration. Even investors who specifically avoided South Korea ETFs may carry KOSPI-correlated semiconductor exposure through their EM allocation, because the same AI-driven semiconductor theme that concentrated the KOSPI also elevated TSMC’s weight in the broader EM index.

What passive investors and ETF holders actually need to check

The KOSPI selloff demonstrated what can happen when passive investors hold concentrated index exposure without visibility into the construction beneath the fund label. The diagnostic steps below apply to any index ETF, not only South Korea funds.

- Check the top-10 holdings: If the top 10 constituents account for more than 40-50% of total fund weight, the ETF carries meaningful concentration risk regardless of how many total holdings it lists

- Review sector allocation: Information technology comprising more than 35-40% of any single-country or EM fund is the clearest surface signal of embedded single-name concentration

- Identify index methodology: Market-cap-weighted indices concentrate naturally during sector rallies; equal-weighted or factor-based alternatives distribute exposure differently

- Look for single-stock caps: Some index providers impose maximum single-stock weights (often 10% or 15%); funds tracking uncapped indices are more exposed to concentration drift

- Assess foreign ownership dynamics: High foreign ownership through passive products (such as the KOSPI’s 38%) amplifies forced-selling risk during drawdowns

The iShares MSCI South Korea ETF (EWY) is the primary vehicle through which international investors hold KOSPI exposure. Its holdings mirror the KOSPI’s semiconductor concentration, meaning investors who purchased it for “South Korea equity exposure” were, in practice, making a concentrated semiconductor bet.

A fund labelled “diversified” may hold 50% of its weight in two stocks if the underlying index does. The diversification label describes the number of holdings. It does not describe the distribution of weight across them.

The KOSPI’s 75% year-to-date gain as of 6 May 2026 illustrates how quickly sector-led performance can concentrate an index. Investors who checked their ETF’s top holdings a year ago may find the concentration profile has shifted materially since.

The KOSPI moment as a permanent benchmark for index risk

The 15 May 2026 KOSPI selloff will likely be cited alongside TSMC’s dominance of the MSCI Taiwan Index and Saudi Aramco’s weight in the Tadawul as a canonical example of how index construction shapes, rather than merely reflects, market risk. The index was at a record high above 8,000 before the session. Hours later, it had shed more than 6%, triggered not by a macroeconomic event but by a labour dispute at one company whose index weight gave it market-moving power.

The Samsung strike is scheduled to begin 21 May 2026, and as of today, its outcome remains unresolved. Investors with KOSPI or broader semiconductor exposure should monitor developments closely, as the full market impact of the labour action has not yet been priced.

The broader lesson extends beyond the AI semiconductor cycle. Whenever one theme captures a disproportionate share of index weight, that index becomes a sector bet wearing a market-wide label. It happened with semiconductors in the KOSPI. It has happened with TSMC in Taiwan. The structural conditions for it to happen again exist in other indices today.

Market breadth divergence has become one of the clearest early-warning signals for this kind of concentration-driven fragility: when a headline index makes new highs while fewer than 60% of its constituents trade above their 200-day moving average, the advance is being carried by a narrowing leadership group whose eventual repricing pulls the entire index lower.

- KOSPI 200: Samsung Electronics and SK Hynix at approximately 51.5% combined weight

- MSCI Taiwan: TSMC at 58.33%, the most extreme single-stock concentration among major indices

- MSCI Emerging Markets: TSMC at approximately 14%, embedding single-stock tech concentration inside a geographically “diversified” instrument

- Tadawul: Saudi Aramco as a historical precedent for single-stock dominance in an emerging market index

Index concentration risk is not theoretical. It crystallised on 15 May 2026, and the same structural conditions exist in indices that many passive investors already hold.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements regarding potential market impacts are speculative and subject to change based on market developments and company performance.