Why $108 Oil Is Only Part of the Geopolitical Risk Story

35 mins ago

National Australia Bank delivers a return on equity more than two percentage points above the Big Four average, yet its net interest margin sits below every major peer. That combination is not a contradiction. It is a diagnostic, and reading it correctly requires moving beyond the share price ticker and into the three metrics that reveal how a bank actually generates, retains, and protects shareholder value. With the RBA cash rate at 4.35% as of May 2026 and all four major banks navigating deposit competition and lending margin pressure, investors face a genuinely difficult comparative question: which bank’s financial profile is best positioned for the conditions ahead? This analysis benchmarks NAB against Westpac, ANZ, and CBA across net interest margin (NIM), return on equity (ROE), and Common Equity Tier 1 (CET1) capital ratio, explains what each metric measures, and draws out what NAB’s specific pattern tells investors about its competitive positioning.

Share price movements capture sentiment, liquidity flows, and short-term earnings surprises. They do not reliably capture the structural earning power, capital efficiency, or financial resilience that separate one bank from another over a full cycle. For banks, where lending-derived income represented 81% of NAB’s total revenue in its most recent full financial year, three metrics do that work:

The three-metric framework used here reflects the same logic professional analysts apply when valuing bank shares: NIM establishes how efficiently the lending book converts rate exposure into revenue, ROE translates that revenue into shareholder returns, and CET1 anchors both measures against a solvency baseline that regulators and credit markets watch closely.

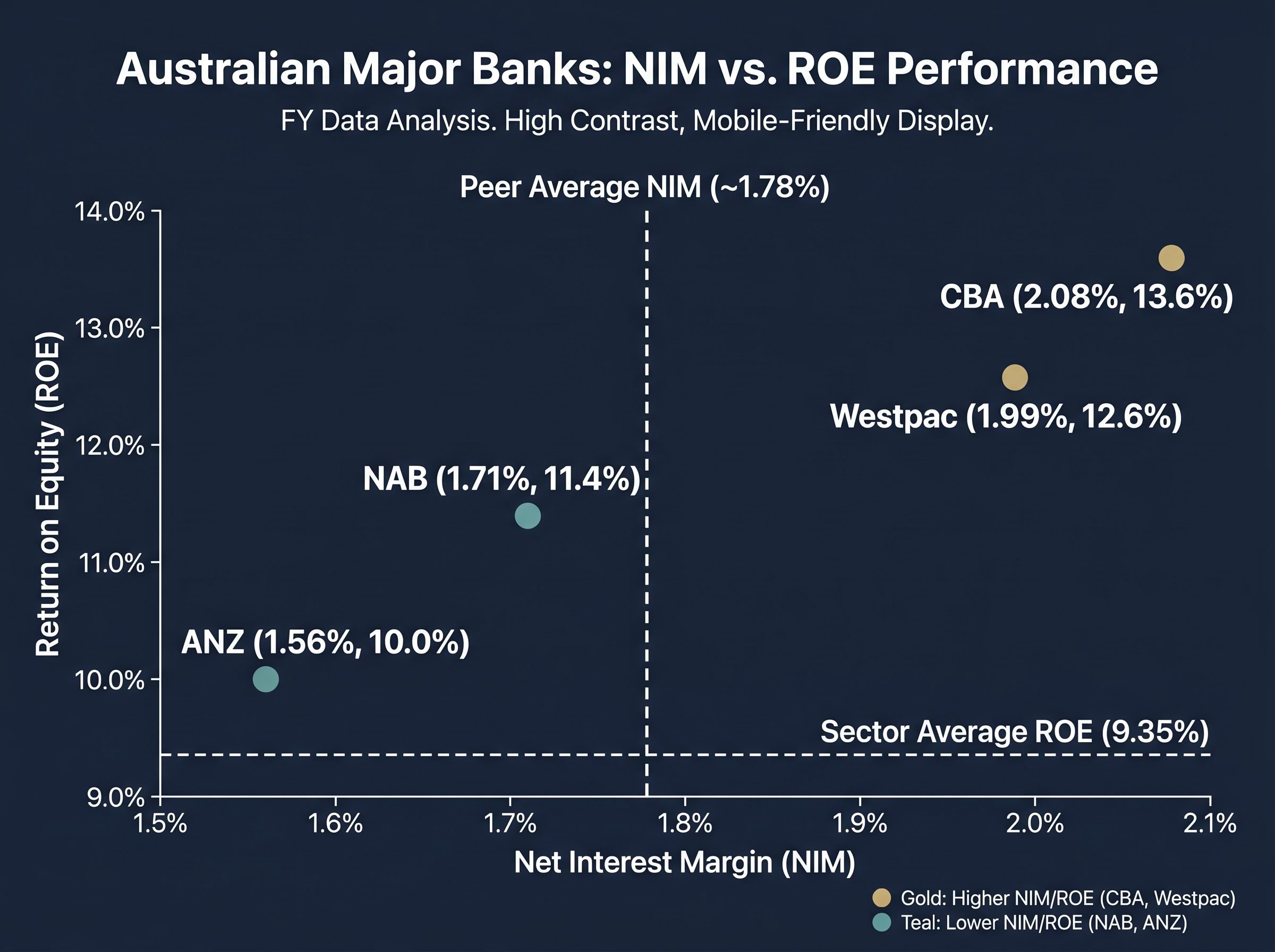

The Big Four peer NIM range of 1.56% to 2.08% immediately signals that meaningful dispersion exists across institutions that, from a share price chart, can appear interchangeable. Each of the following sections uses one metric as a distinct diagnostic lens, before the combined picture is read in full.

NIM measures the spread between what a bank pays depositors and wholesale lenders versus what it collects from borrowers, expressed as a percentage of interest-earning assets. It is the single most direct measure of a bank’s ability to generate revenue from its core function: lending.

81% of NAB’s total revenue in its most recent full financial year was derived from lending-related income, anchoring NIM as the metric with the most direct line to earnings.

NAB’s NIM of 1.71% sits 7 basis points below the peer group average of approximately 1.78%. The full peer spread reveals the structural differences: ANZ reported 1.56%, Westpac came in at 1.99%, and CBA led the group at 2.08%. CBA’s position at the top reflects its dominant retail deposit franchise, which provides a lower-cost funding base than competitors with heavier wholesale or business-banking weightings.

KPMG’s Big Four half-year results analysis for 2026 reported that the sector average NIM held at 178 basis points across the majors, with the combined CET1 ratio rising to 12.1%, providing independent benchmarking that corroborates the peer dispersion visible across NAB, CBA, Westpac, and ANZ.

NAB’s below-average NIM is not a failure of execution. It is the price of a specific competitive position. NAB’s loan book is more heavily weighted toward SME and commercial lending than CBA’s or Westpac’s retail-dominated portfolios. Business lending involves different margin dynamics: competitive pricing pressure from all four majors and regional lenders has compressed spreads in the segment, placing a structural ceiling on NIM that is a feature of NAB’s strategy, not a deficiency.

The RBA’s 2026 rate hike cycle (increases in February, March, and May 2026, bringing the cash rate to 4.35%) is applying asymmetric pressure across the sector. On the asset side, lending rates reprice upward, which supports margins. On the liability side, deposit competition intensifies as term deposit rates rise, eroding the funding cost advantage. The net NIM effect depends on the speed of asset repricing versus liability cost increases, and on each bank’s specific deposit and loan mix. NAB’s deposit composition, with its business-banking skew, makes it particularly sensitive to this dynamic.

ROE measures profit generated per dollar of shareholder equity, and it is the metric institutional investors use most consistently to compare capital efficiency across banks of different sizes. A higher ROE means the bank is extracting more value from the capital shareholders have contributed.

NAB’s ROE of 11.4% sits well above the sector average of 9.35%. In practical terms, each $100 of shareholder equity generates $11.40 in annual profit. Given that NAB’s NIM trails the peer average, this outperformance is worth pausing on. A bank with below-average margins delivering above-average returns on equity is doing something different with its cost base, its loan book composition, or its capital management, or some combination of all three.

| Bank | NIM | ROE |

|---|---|---|

| NAB | 1.71% | 11.4% |

| ANZ | 1.56% | 10.0% |

| Westpac | 1.99% | 12.6% |

| CBA | 2.08% | 13.6% |

The table makes the divergence visible. CBA leads on both metrics; ANZ trails on both. NAB and Westpac occupy different quadrants: Westpac pairs a higher NIM with a higher ROE, while NAB achieves above-average ROE despite a below-average NIM. That gap points to cost discipline and business lending volumes doing the heavy lifting on returns.

The analytical tension for investors is straightforward. Strong ROE is a positive signal. But if it is being sustained under margin pressure via cost management rather than revenue growth, its durability becomes a question worth tracking across future reporting periods.

NAB’s H1 2026 result complicates a straightforward reading of the ROE figure: the $949 million after-tax software capitalisation charge reduced reported cash earnings materially, meaning the 11.4% ROE visible in the scorecard reflects an adjusted earnings base rather than the statutory headline, and the $300 million forward-looking geopolitical provision adds a further layer of interpretation to any period-on-period comparison.

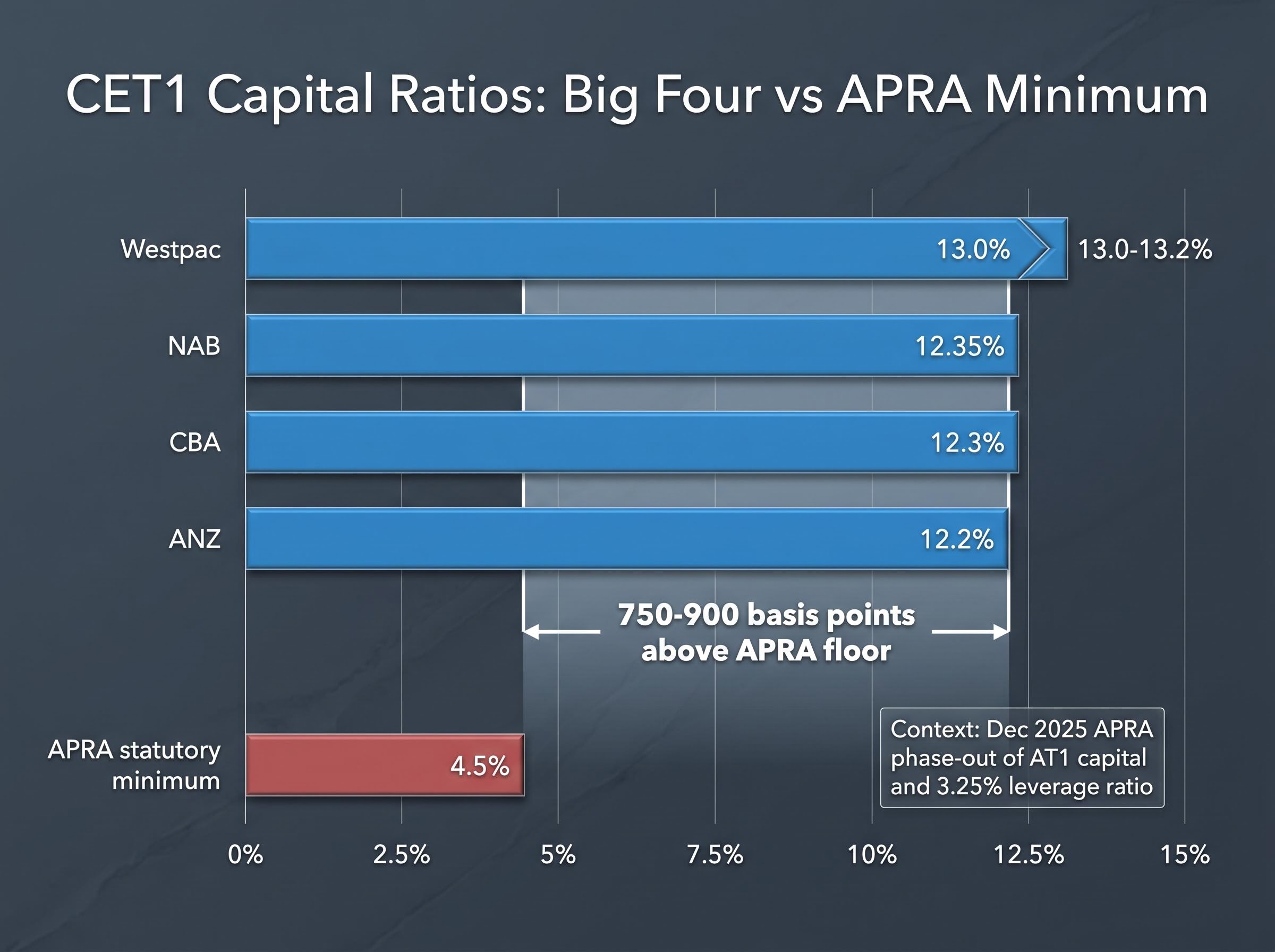

Common Equity Tier 1 (CET1) capital ratio measures the proportion of a bank’s risk-weighted assets funded by the highest-quality capital, primarily ordinary shares and retained earnings. It functions as a financial buffer: the higher the ratio, the more loss a bank can absorb before its solvency comes into question.

NAB’s CET1 of 12.35% places it in a comfortable position within the peer group:

All four majors operate 750-900 basis points above APRA’s floor, reflecting regulatory expectations and the banks’ own capital management frameworks. The surplus above regulatory requirements is not idle capital. It represents capacity for buybacks, special dividends, or lending growth, making it directly relevant to shareholder return expectations.

In December 2025, APRA finalised its decision to phase out Additional Tier 1 (AT1) capital instruments and reduced the leverage ratio requirement to 3.25% on a CET1 basis. This regulatory shift is gradually increasing the importance of pure CET1 as the relevant measure of bank capitalisation across the industry.

APRA’s finalised AT1 phase-out framework confirms that the removal of Additional Tier 1 instruments is being accompanied by a reduction in the minimum leverage ratio requirement from 3.5% to 3.25% on a CET1 basis, a calibration designed to avoid unintended tightening of the overall capital regime during the transition.

In a rising-rate environment where credit risk may increase, a well-capitalised bank retains more options. NAB’s CET1 above the peer average (excluding Westpac) is a quiet but meaningful component of its investment case.

Three metrics, read together: below-average NIM (1.71% versus 1.78% peer average), above-average ROE (11.4% versus 9.35% sector average), and above-average CET1 (12.35%). The combination describes a capital-efficient business-banking specialist that trades profitability breadth for depth in a specific lending segment.

| Bank | NIM | ROE | CET1 | Positioning |

|---|---|---|---|---|

| NAB | 1.71% | 11.4% | 12.35% | Business-banking specialist; efficiency-led returns |

| ANZ | 1.56% | 10.0% | 12.2% | Institutional and international mix; lowest NIM and ROE |

| Westpac | 1.99% | 12.6% | 13.0-13.2% | Retail-weighted; highest CET1 buffer |

| CBA | 2.08% | 13.6% | 12.3% | Retail deposit franchise leader; highest NIM and ROE |

The valuation context adds a layer. A dividend discount model averaging across growth and risk rate scenarios produces an estimated fair value range of approximately $35.74-$36.16 per share on a trailing dividend basis, or $51.66 when incorporating the fully franked gross dividend. Against a share price of approximately $36.85 as of mid-May 2026, the trailing estimate suggests limited margin of safety, while the franking-adjusted figure highlights the significant value embedded in NAB’s dividend franking for eligible Australian taxpayers. NAB’s most recent full-year dividend was $1.69 per share, with a forecast of $1.71 per share.

Market commentary broadly frames NAB as a relative value name within the Big Four, trading at a discount to CBA on forward multiples. A re-rating is typically framed as contingent on:

Analyst consensus across the sector sits in sharp contrast to the share price momentum that has characterised 2026 to date, with all 14 analysts covering CBA holding a sell rating and NAB trading against a broadly bearish tilt despite its relative valuation discount to CBA on forward multiples.

The three-metric framework applied throughout this analysis functions as a reusable diagnostic for any bank comparison:

At the current 4.35% cash rate, NIM compression is a sector-wide condition, making ROE and CET1 relatively more important as near-term differentiators. A single reporting period, however, captures only a snapshot. Investors benefit from tracking how each metric moves across multiple results cycles, as trend direction often matters more than any individual year’s figure.

NAB’s full results materials are available at the NAB investor centre, and APRA’s prudential capital standards are published at APRA banking capital.

For investors wanting to extend the three-metric framework into a fuller balance sheet assessment, our comprehensive walkthrough of ASX bank balance sheet metrics covers NPL ratios, deposit funding composition, and price-to-book multiples across CBA, ANZ, NAB, Westpac, and Macquarie, with worked comparisons showing how loan quality and funding mix interact to produce materially different earnings cyclicality profiles.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Net interest margin (NIM) is the spread between what a bank pays for funding and what it charges borrowers, expressed as a percentage of interest-earning assets. For NAB shareholders it matters because lending-related income represented 81% of NAB's total revenue in its most recent full financial year, making NIM the most direct measure of the bank's core earning power.

NAB's ROE of 11.4% sits above the sector average of 9.35%, placing it ahead of ANZ (10.0%) but below Westpac (12.6%) and CBA (13.6%). Notably, NAB achieves this above-average ROE despite carrying the second-lowest NIM in the peer group, pointing to cost discipline and business lending volumes as the key drivers.

The Common Equity Tier 1 (CET1) ratio measures the proportion of a bank's risk-weighted assets funded by the highest-quality capital, primarily ordinary shares and retained earnings. NAB's CET1 of 12.35% sits above ANZ (12.2%) and CBA (12.3%), and well above APRA's 4.5% statutory minimum, though below Westpac's 13.0-13.2% range.

NAB's NIM of 1.71% is structurally lower because its loan book is more heavily weighted toward SME and commercial lending, a segment where competitive pricing from all four majors and regional lenders compresses spreads. This is a feature of NAB's business-banking strategy rather than a sign of poor execution.

The RBA's February, March, and May 2026 rate increases to 4.35% are applying asymmetric pressure across the sector: higher rates support lending income on the asset side but intensify deposit competition on the liability side. NAB's business-banking deposit mix makes it particularly sensitive to funding cost increases relative to peers with larger retail deposit franchises.