Micron Technology’s shares surged more than 37% in a single trading week. The Nasdaq is at record highs. And in three days, Donald Trump and Xi Jinping will sit across a table in Beijing with semiconductor supply chains as one of the primary items on the agenda. The May 14 summit represents the most concentrated near-term risk event for a sector that has already run far and fast. What follows is a structured scenario analysis for the chip rally: the forces that built it, the geopolitical mechanics that could disrupt it, the valuation signals flashing caution, and a concrete framework for evaluating exposure before Thursday’s session opens.

The rally that got semiconductor stocks here

The numbers speak first. AMD has gained 66% year-to-date as of May 9, 2026. Micron closed at approximately $646.63 on May 7. Nvidia sat at roughly $215.20 on May 8. Broadcom held near $430 on May 9. The SMH ETF has returned somewhere in the 40-57% range year-to-date, depending on the data source, and the SOX index touched approximately 11,408 on May 8.

The rally, though, is not one story. It is two distinct engines running concurrently, and understanding which one powers which name matters for what happens after Thursday.

| Ticker | Approx. Price (May 7-9) | YTD Context |

|---|---|---|

| NVDA | ~$215.20 (May 8) | AI GPU demand leader; summit risk premium noted |

| MU | ~$646.63 (May 7) | HBM shortage dynamics; 37%+ single-week gain |

| AMD | ~$430.60 (May 6) | 66% YTD; earnings-driven market share gains |

| TSM | ~$411.68 (May 8) | AI fab orders; material summit exposure flagged |

| AVGO | ~$430 (May 9) | Custom AI chip deals; less China-exposed than peers |

AI capex as the GPU demand engine

Hyperscaler capital expenditure commitments for 2026 now sit in the range of $600-690 billion across major cloud providers, with Microsoft alone committing $80 billion in FY2025 AI infrastructure and signalling a continued ramp. That spending flows directly into GPU orders from Nvidia and AMD, and it has been the primary justification for elevated multiples across the sector. Forward price-to-earnings ratios on both names embed 30-40% growth expectations, which means any revision to hyperscaler capex guidance would compress valuations quickly.

The hyperscaler capex cycle driving GPU demand is projected to consume roughly 90% of major cloud providers’ operating cash flow by 2027, a commitment level that transforms infrastructure spending from a discretionary line item into a structural obligation and provides the floor under semiconductor revenue estimates regardless of near-term diplomatic outcomes.

HBM memory shortages as a separate but concurrent driver

Micron’s rally operates on a different axis. High-bandwidth memory (HBM), the specialised memory required for AI training chips, is supply-constrained in a way that gives memory producers pricing power independent of the export restriction debate. Analysts have characterised MU as well-positioned for any diplomatic thaw, but its recent gains are fundamentally about scarcity, not geopolitics.

That distinction matters. GPU-exposed names like Nvidia and TSMC carry direct China revenue sensitivity. Memory names like Micron are more insulated from whatever happens in Beijing on Thursday.

When big ASX news breaks, our subscribers know first

What the Trump-Xi summit actually means for chip supply chains

Three specific policy levers sit on the table, and each one maps to different names in the semiconductor complex.

The first is Entity List status for advanced AI chips. Companies placed on the Entity List cannot receive US-origin technology, which for Nvidia and TSMC means losing access to significant Chinese data centre customers. The second is HBM memory export controls, where partial easing could widen Micron’s addressable market. The third is China’s rare earth and gallium/germanium export restrictions, introduced in December 2024 and subsequently suspended until November 2026, making any summit discussion about the terms of that suspension rather than a new restriction.

The leverage is asymmetric. China controls approximately 95% of global rare earth supply, giving it substantial bargaining power over materials the entire semiconductor supply chain depends on. The US controls advanced chip licensing, which caps Chinese access to leading-edge AI hardware. Neither side can concede without receiving something in return, which is why a binary “deal or no deal” framing misreads the dynamics.

The Asian semiconductor supply chain is where China’s leverage is most concentrated: SK Hynix holds an estimated 52-70% of Nvidia’s HBM orders, ASML holds a global monopoly on EUV lithography equipment used by every advanced AI chip manufacturer, and TSMC and Samsung together represent approximately 35% of global semiconductor market capitalisation, a concentration that amplifies the stakes of any summit outcome beyond what US-listed names alone reflect.

- Entity List easing for AI chips: Most directly affects Nvidia and TSMC, which have the largest suppressed China revenue pools

- HBM export control adjustments: Primary beneficiary is Micron, though the impact is secondary to its existing supply-constraint tailwind

- Rare earth and gallium/germanium suspension terms: Broad supply chain relevance; affects all semiconductor manufacturers reliant on Chinese-sourced materials

- Broadcom: Analysts consistently characterise AVGO as less China-exposed given its hyperscaler-focused custom chip model

Bloomberg Intelligence (May 9) estimated approximately a 70% probability of partial de-escalation, noting that partial easing could unlock $20 billion or more in TSMC and Nvidia China revenue.

The Semiconductor Industry Association (SIA) expressed optimism about the dialogue while cautioning against expectations of rapid supply chain fixes.

Why semiconductor valuations are sensitive to diplomatic language

For readers tracking chip stocks without a background in export policy, the connection between a diplomatic meeting and a hardware company’s share price runs through a specific three-step mechanism:

- US export licensing controls set a ceiling on which chips can be sold to which countries. The Bureau of Industry and Security determines the classification of each product and the destinations it can reach.

- Entity List placement removes specific companies or organisations from the approved buyer pool entirely. For TSMC, despite being a Taiwanese company, this applies because it manufactures using US-origin equipment, placing it under US export jurisdiction.

- Revenue impact follows directly. When a licensing restriction tightens, the addressable market for affected companies shrinks by the value of the blocked customers. When it eases, that revenue becomes available again.

This is why diplomatic language matters at the margin. A Needham analyst estimated that meaningful export easing could lift semiconductor names by 10-15%. On the bearish side, Deutsche Bank modelled SMH target levels in the $220 range if curbs harden. Broadcom sits further from this volatility given its hyperscaler-focused revenue mix, which is less dependent on direct China sales.

Three summit scenarios and what each means for your portfolio

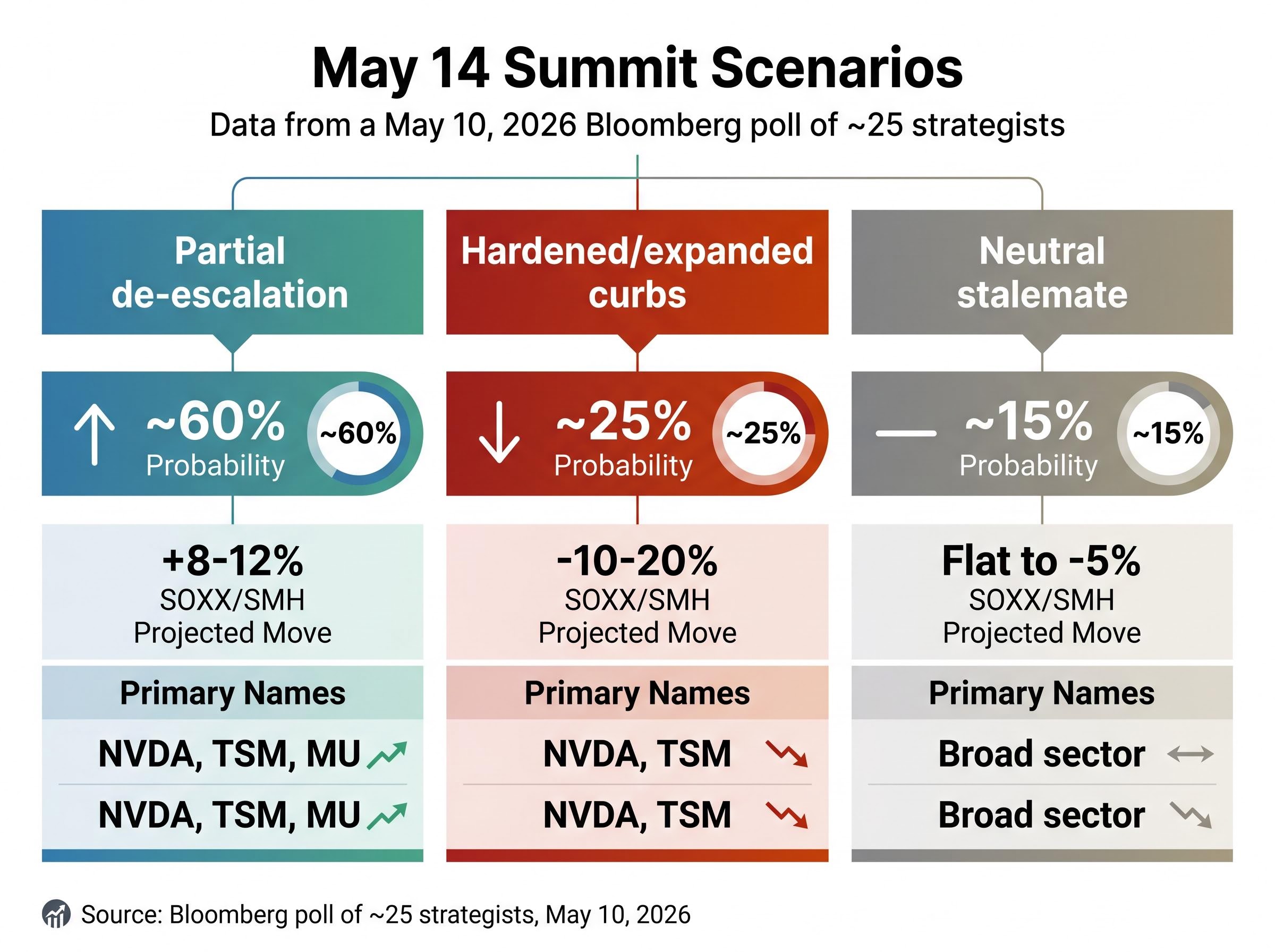

A Bloomberg poll of approximately 25 strategists, published May 10, 2026, provides the probability-weighted framework.

| Scenario | Probability | SOXX/SMH Projected Move | Primary Impacted Names |

|---|---|---|---|

| Partial de-escalation | ~60% | +8-12% | NVDA, TSM, MU |

| Hardened/expanded curbs | ~25% | -10-20% | NVDA, TSM (highest exposure) |

| Neutral stalemate | ~15% | Flat to -5% | Broad sector (muted reaction) |

The most likely outcome, partial de-escalation, carries the smallest absolute percentage move. The less likely but not improbable hardening scenario carries substantially larger downside.

The asymmetry is the real insight: +8-12% upside in the best case versus -10-20% downside in the worst case. That gap has portfolio construction implications for anyone sizing positions ahead of Thursday.

JPMorgan has framed the stalemate scenario as “geopolitics already priced in,” suggesting limited movement. Citron Research, on May 10, characterised the SOX as overbought and flagged short positions in memory and AI chip names on momentum fade. SOXX traded at approximately $520 and SMH at approximately $560 as of May 10 (both figures carry data reliability caveats).

The valuation fragility that makes timing matter

The rally’s speed has left technical and fundamental fingerprints that bear examination, not as a prediction of collapse, but as evidence that the margin for error is thin.

- RSI readings above 80 on multiple semiconductor names as of early May 2026, a level historically associated with mean-reversion risk

- SOX at or near approximately 11,408 (May 8 close), with analysts citing a 15th consecutive all-time high

- Forward P/E multiples on Nvidia and AMD embedding 30-40% growth expectations

- Capex front-loading concern: the bear case, articulated in Barron’s on May 10, holds that hyperscaler spending is real but potentially compressed into the near term, with risk of multiple derating if cloud provider ROI disappoints

A name-by-name valuation framework separates the signal from the noise here: Micron trades at roughly 8x forward earnings despite record revenue, while Intel sits near 101x, a spread that makes sector-wide bubble calls as misleading as sector-wide buy signals.

Prominent bearish fund manager commentary projected a 25-30% correction as possible post-summit regardless of outcome. (Note: specific institutional attribution for this view could not be independently verified; it reflects general bearish institutional sentiment rather than a confirmed position from a named firm.)

The counterpoint deserves fair treatment. Wedbush, on May 9, argued that fundamentals override technical signals and that any dip represents a buying opportunity given the durability of AI demand. Both readings are internally consistent; they simply weight the same data differently.

The operative question for investors sitting on significant unrealised gains is not whether the sector is overbought in absolute terms. It is whether a negative summit outcome could function as the trigger for a correction that stretched valuations had been building toward.

Why the structural AI case still sets the floor

The summit is a near-term volatility event, not an existential test of the semiconductor thesis.

Hyperscaler capex in the $600-690 billion range for 2026 represents a multi-year infrastructure cycle spanning data centres, model training, and inference capacity. Microsoft’s $80 billion FY2025 AI infrastructure commitment continues to ramp into 2026. These spending programmes do not reverse on the basis of a single diplomatic meeting.

Even in a negative summit scenario, the domestic US AI infrastructure buildout is insulated from China export dynamics. The data centres being constructed in Virginia, Texas, and Oregon do not require Chinese market access to justify their capital outlays.

- Higher China exposure: Nvidia and TSMC carry the most direct sensitivity to summit outcomes through their suppressed China revenue pools

- Lower China exposure: Broadcom (hyperscaler custom silicon focus) and AMD (domestic GPU demand and earnings-driven 66% YTD gain grounded in market share gains) are relatively less summit-dependent

Investors who can distinguish between these two categories are better positioned to manage near-term risk without abandoning the structural trade.

Three days out: how to think about semiconductor exposure before May 14

The commercial question is not what will happen on Thursday. It is whether readers have a framework for responding to what does happen.

Three questions deserve answers before the summit session opens:

- Which names in the portfolio have material China revenue exposure? Nvidia and TSMC sit at the top of that list; Broadcom and domestically driven AMD exposure sits lower.

- What is the pain tolerance for a -10-20% drawdown if curbs harden? The 25% probability assigned to that scenario is not negligible.

- Is the thesis summit-dependent or structural-demand-dependent? If the investment case rests on AI capex durability, a poor summit outcome changes the near-term trajectory but not the multi-year foundation.

The dominant US-side framing positions the summit as a “catalyst, not the driver.” In a momentum-driven sector, though, catalysts can function as triggers for moves that had been building structurally.

Elevated implied volatility in semiconductor options heading into May 14 signals genuine institutional uncertainty, not consensus. Hedging is more expensive as a result, which itself is informative.

The Bloomberg poll probability distribution, 60% partial de-escalation, 25% hardened curbs, 15% stalemate, provides the base rates. What it does not provide is the specific language that will emerge from the meeting, which is where the real pricing will happen.

Geopolitical risk is a permanent feature of the semiconductor investment landscape

May 14 is the first of four planned US-China presidential summits over a 12-month cycle, a historically unprecedented frequency. The geopolitical overhang on semiconductor stocks is a recurring feature of the investment environment, not a one-time clearing event.

The structural AI demand case, hyperscaler capex extending through 2026 and into 2027 planning cycles, remains the primary long-term valuation support regardless of any single diplomatic outcome. The SIA acknowledged productive dialogue but stressed no rapid resolution for complex supply chain dependencies.

For readers wanting to understand the longer-term structural pressures on TSMC beyond the summit, our dedicated guide to TSMC supply chain diversification covers Apple’s early-stage foundry discussions with Samsung and Intel, the CHIPS Act subsidy dynamics reshaping US-based manufacturing viability, and why any realistic volume shift away from TSMC remains capped below 10% of demand before 2027.

The most likely outcome on Thursday is partial de-escalation with limited specifics, a result that may produce a muted market reaction resolving nothing permanently. Investors positioned for a binary resolution may find the real story is that semiconductors have entered a prolonged period where geopolitics is a standing variable, not a one-off event to trade through.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. These forward-looking statements regarding summit outcomes and projected price movements are speculative and subject to change based on market developments and diplomatic outcomes.