Why Governance and Communication Drive Post-IPO Value

13 hrs ago

Most investors think the hard part is picking a winner. Will Danoff’s record at Fidelity Contrafund suggests the harder part is keeping one.

Danoff has managed Contrafund since 1990, building one of active management’s longest-running and most studied outperformance records. The fund’s edge is not a single insight or a lucky streak. It is a set of interlocking investment principles that reinforce each other over time: a commitment to letting compounders run, a systematic approach to evaluating management quality, and a pipeline strategy for capturing early-stage upside.

These principles were developed at institutional scale, inside a fund managing billions of dollars. But the underlying logic applies to any investor managing a portfolio. What follows breaks down the three principles at the core of Contrafund’s approach and what each one looks like when you apply the same logic to your own holdings.

Contrafund is not a closet index fund. Fidelity describes it as an opportunistic, diversified equity strategy with a large-cap growth bias, built on bottom-up stock picking and a long-term holding horizon. Understanding that distinction matters, because the principles that follow only make sense if you first grasp the deliberate, research-intensive foundation they rest on.

Three defining characteristics set the strategy apart:

The fund’s average portfolio market capitalisation sits marginally below the large-growth category average, even accounting for the substantial scale of assets under management. That tells you the mandate is genuine, not index-hugging. Danoff’s breadth and research volume together create a conviction-driven strategy, and that distinction is what makes the transferable principles worth extracting.

The broader debate around active vs passive investing is essential context here: two decades of SPIVA data show that over 90% of active large-cap fund managers fail to beat the S&P 500 over a 20-year horizon, which is precisely what makes Danoff’s sustained outperformance record at Contrafund a genuinely exceptional data point rather than a typical outcome.

Contrafund’s broad investment mandate has extended well beyond public equities. Prior to their stock market debuts, the fund established stakes in Facebook (now Meta Platforms), Pinterest, and Airbnb, securing exposure at valuations that public-market investors could not access. SpaceX represents a current example of this approach: Contrafund has held a position since 2015, and that stake had grown to roughly 4.7% of total fund assets by April 2026.

The underlying method is what Fidelity describes as a pipeline approach: building numerous smaller starter positions, monitoring them as growth trajectories develop, and sizing up as conviction strengthens. This pipeline extends across both private and public stages, functioning as an internal development system for high-potential holdings.

The honest reality is that you cannot replicate Contrafund’s pre-IPO access. But you can apply the same early-and-patient logic in public markets, where post-IPO volatility frequently creates entry points that look risky in the moment but prove well-priced over a five-to-ten-year hold.

| Contrafund example | Individual investor equivalent | Core principle applied |

|---|---|---|

| Facebook (pre-IPO) | Study newly public companies in their first 1-2 years of trading, when sentiment is often more negative than fundamentals warrant | Early entry when conviction diverges from consensus |

| Airbnb (pre-IPO) | Build small starter positions in early-stage public companies and add as the thesis strengthens | Pipeline approach: small initial sizing, evidence-driven scaling |

| Pinterest (pre-IPO) | Develop differentiated views on secular trends (AI, cloud, payments, healthcare innovation) before they become consensus | Pre-consensus positioning in public markets |

| SpaceX (private, held since 2015) | Use listed vehicles with private-market exposure carefully, where available and within your risk tolerance | Long-duration conviction holding with patience through illiquidity |

Three concrete actions capture the spirit of this principle without requiring institutional access. First, study newly public companies in the first one to two years of trading, when sentiment is often more negative than fundamentals warrant; that gap between perception and reality is where the opportunity sits. Second, build small starter positions in high-potential early-stage public companies rather than waiting for certainty, and let conviction and evidence drive subsequent sizing. Third, develop differentiated views on secular trends before they become consensus. If you had a clear thesis on cloud adoption or digital payments in 2016, the public-market opportunities were already there.

For investors who want to operationalise the pre-consensus positioning principle in their own research process, our comprehensive walkthrough of evaluating thematic investments before consensus forms applies a five-question framework to emerging secular trends including AI, cloud infrastructure, and healthcare innovation, covering how to distinguish a durable structural shift from a fashionable fad before the market prices in unrealistic growth.

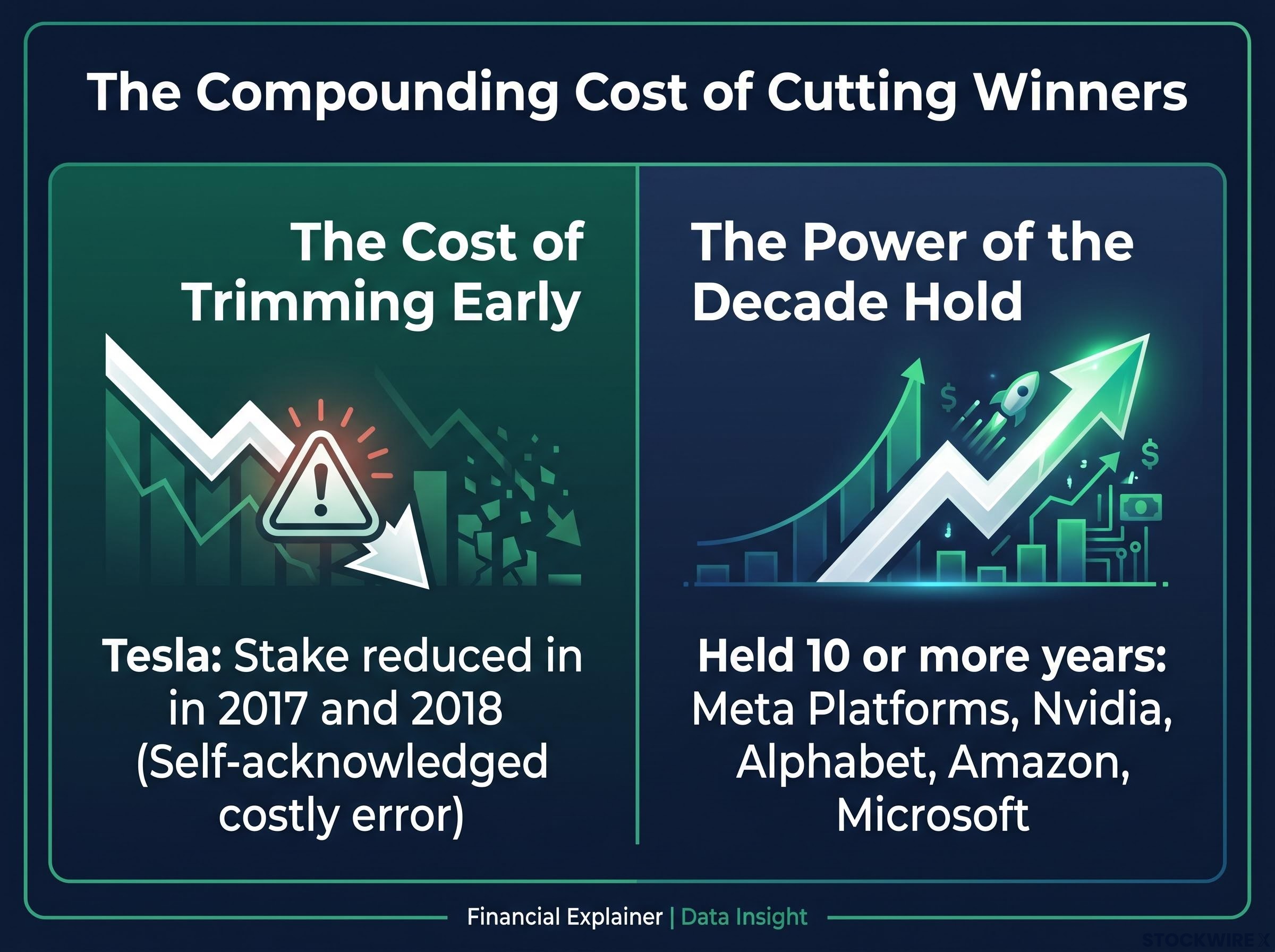

You know the feeling. A stock you own has doubled, maybe tripled, and every instinct tells you to lock in the gain. The position feels uncomfortably large. The chart looks stretched. Your thumb hovers over the sell button.

Danoff has been explicit about this: premature selling is one of the most costly errors an investor can make. His core premise is that stock prices follow businesses, not the other way around. A business growing earnings at a high-teens or 20% rate can double and then redouble over a decade, creating multiple turns on original capital if the competitive advantage endures. Cutting that trajectory short after the first double permanently lowers your long-run return.

Tesla is the case study Danoff himself has cited most directly. Contrafund reduced its stake during 2017 and 2018, and he has since acknowledged that decision as one of the clearest lessons from his career. The lesson is not really about Tesla specifically. It is about the asymmetric cost of letting psychological discomfort with gains override a thesis that had not actually changed.

The asymmetric cost Danoff describes is well-documented across named investor postmortems: anchoring to absolute market-cap size, treating a large gain as automatic evidence of overvaluation, and letting structural selling pressure override a thesis that remains intact are the specific errors that define when to sell winning stocks badly, and each one has a documented mechanism you can learn to recognise in your own decision-making.

Selling a structurally advantaged compounder too early, not holding it too long, is often the bigger risk. A small number of exceptional winners drive the bulk of long-run returns. Truncating them after the first double can permanently lower overall portfolio performance.

The evidence from Contrafund’s portfolio is compelling in aggregate. Meta Platforms, Nvidia, Alphabet, Amazon, and Microsoft have each been held for ten or more years, and the compounding effect of staying invested through their respective growth periods has been a meaningful driver of the fund’s long-run record.

The alternative to reflexive profit-taking is a sell discipline anchored in business fundamentals, not price levels. Three triggers warrant genuine consideration of selling: the company’s competitive position has eroded, management quality has deteriorated, or the long-term growth economics have clearly worsened.

What should not trigger a sell decision is equally important. The stock being “up a lot” is not a thesis change. The position feeling uncomfortable because it has grown large is not a thesis change. Price appreciation alone tells you nothing about whether the business case you underwrote still holds. Regularly revisit your original thesis: if the company is executing as well or better than you expected, consider whether the urge to trim is driven by fundamentals or simply by discomfort with gains.

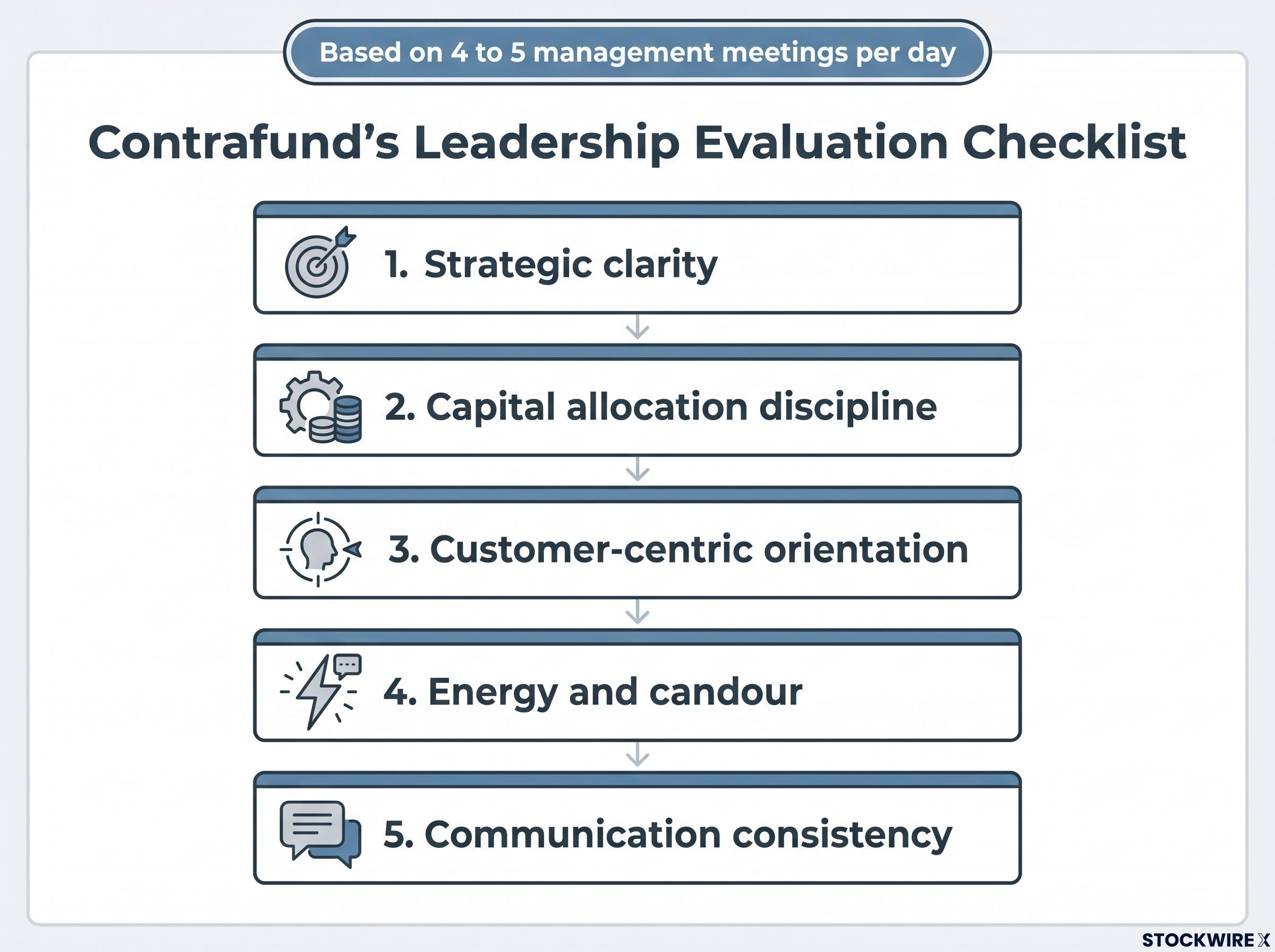

Four to five management meetings per day sounds like relationship-building. In practice, it is something more systematic than that: a mechanism for building a longitudinal, comparative view of leadership quality that compounds as an informational edge over years.

Danoff maintains records from prior meetings and tests each subsequent interaction against what management said before, building a running assessment of whether leaders actually deliver on the priorities they articulate. That longitudinal view is unavailable to investors who engage only episodically, reading one annual report or listening to a single earnings call. When you have met with the same CEO eight times over four years, you can distinguish between leaders who execute and leaders who narrate.

The specific qualities Danoff evaluates form a consistent checklist:

Conducting such a high volume of meetings gives Danoff a running, cross-sector view of where trends are forming before they become widely recognised, a structural informational advantage that no single company interaction can provide.

The most transferable part of this process for you is the longitudinal tracking itself. You have access to earnings calls, investor day presentations, proxy statements, and prior management statements. The key is treating these not as passive consumption but as an active hypothesis-testing discipline. Read what the CEO said a year ago, then check whether they did it. That single habit transforms how you evaluate management quality.

Danoff’s preference for founder-led businesses is not sentimental. Both Morningstar and Fidelity flag it as a defining pattern in how Contrafund’s portfolio is constructed. The logic is structural, rooted in incentives, time horizon, and the willingness to make unconventional decisions that professional managers often cannot.

Four advantages make founder-led firms structurally different from companies run by hired operators:

The structural case for this preference is supported by academic research on founder-led company outperformance, including findings from Purdue’s Krannert School of Management and Babson College, which show that founder-controlled firms generate more valuable patents, take more productive risks, and sustain competitive advantages longer than companies run by professional managers without equity stakes.

Founders with large stakes think in terms of long-term enterprise value, not the next few quarters of EPS. That alignment with long-term shareholders is the structural advantage you are looking for when you evaluate management before buying.

Meta Platforms is the clearest illustration in Contrafund’s portfolio. Danoff built the position pre-IPO, when Facebook was still a private company, and has held through the public listing, multiple product pivots, and periods of intense public scrutiny. The founder-led structure, with Mark Zuckerberg retaining meaningful control, supported the kind of long-term reinvestment decisions that a more conventional corporate governance setup might not have tolerated.

For you, the practical screening dimension is straightforward: prioritise companies where founders or founder-linked leaders hold meaningful equity and have demonstrated capital allocation discipline over time. That is not a vague preference. It is a concrete, replicable filter you can apply through proxy statements and ownership data before you buy.

Proxy statements are the primary data source for assessing board alignment, and the distinction between equity granted as compensation and equity purchased with personal capital is the most informative signal: directors who buy shares in the open market are signalling a level of conviction that fee-funded equity awards simply cannot replicate.

The three principles work because they reinforce each other. High-quality, founder-led businesses are worth holding for a decade or more precisely because the leadership structure supports the long-term reinvestment that drives compounding. Letting winners run allows those franchises to drive a disproportionate share of returns as their advantages widen. The pipeline approach, building small positions early and sizing up as conviction grows, injects high-upside optionality that can then be held and compounded if the business proves out.

The common implementation failures these principles are designed to prevent are specific: selling structurally advantaged businesses too early because the gain feels uncomfortable, underweighting management quality as an investment variable, and confusing price appreciation with thesis invalidation.

Adapted for an individual investor, the framework comes down to five commitments:

The sustained performance of Contrafund’s core holdings makes the empirical case clearly. Meta Platforms, Nvidia, Alphabet, Amazon, and Microsoft were commitments measured in decades, not months, held through periods of uncertainty because the quality of management, the durability of competitive positioning, and the economics of compounding all supported continued ownership. The system worked because all three principles operated together.

The most actionable shift for most investors is definitional. Change what triggers a sell decision from “this position is up a lot and feels uncomfortable” to “the business case I underwrote has materially changed.” That single reframing is where the compounding gains, or loses, years.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

Fidelity Contrafund is an opportunistic, diversified equity strategy with a large-cap growth bias, managed by Will Danoff since 1990. It uses bottom-up stock picking, a long-term holding horizon, and invests across market capitalisations including private holdings, giving it a genuinely active mandate rather than an index-hugging one.

Danoff's approach rests on three core principles: letting structurally advantaged compounders run rather than selling after the first double, evaluating management quality through longitudinal tracking of what leaders say versus what they deliver, and building small starter positions early in high-potential companies and sizing up as conviction grows.

Contrafund's broad investment mandate allows it to hold private company stakes before public listings, which is how it established positions in Facebook, Pinterest, and Airbnb at valuations unavailable to public-market investors. SpaceX represents a current example, with Contrafund holding a stake since 2015 that had grown to roughly 4.7% of total fund assets by April 2026.

Founders with large equity stakes think in terms of long-term enterprise value rather than short-term earnings per share, making them more willing to invest heavily in research and product development even at the cost of near-term margins. Academic research supports this preference, with founder-controlled firms shown to generate more valuable patents, take more productive risks, and sustain competitive advantages longer than professionally managed peers.

Danoff's framework anchors sell decisions in business fundamentals rather than price levels: genuine triggers include erosion of competitive position, deterioration in management quality, or a clear worsening of long-term growth economics. A stock being up significantly or a position feeling uncomfortably large are not thesis changes and should not drive selling if the underlying business case remains intact.