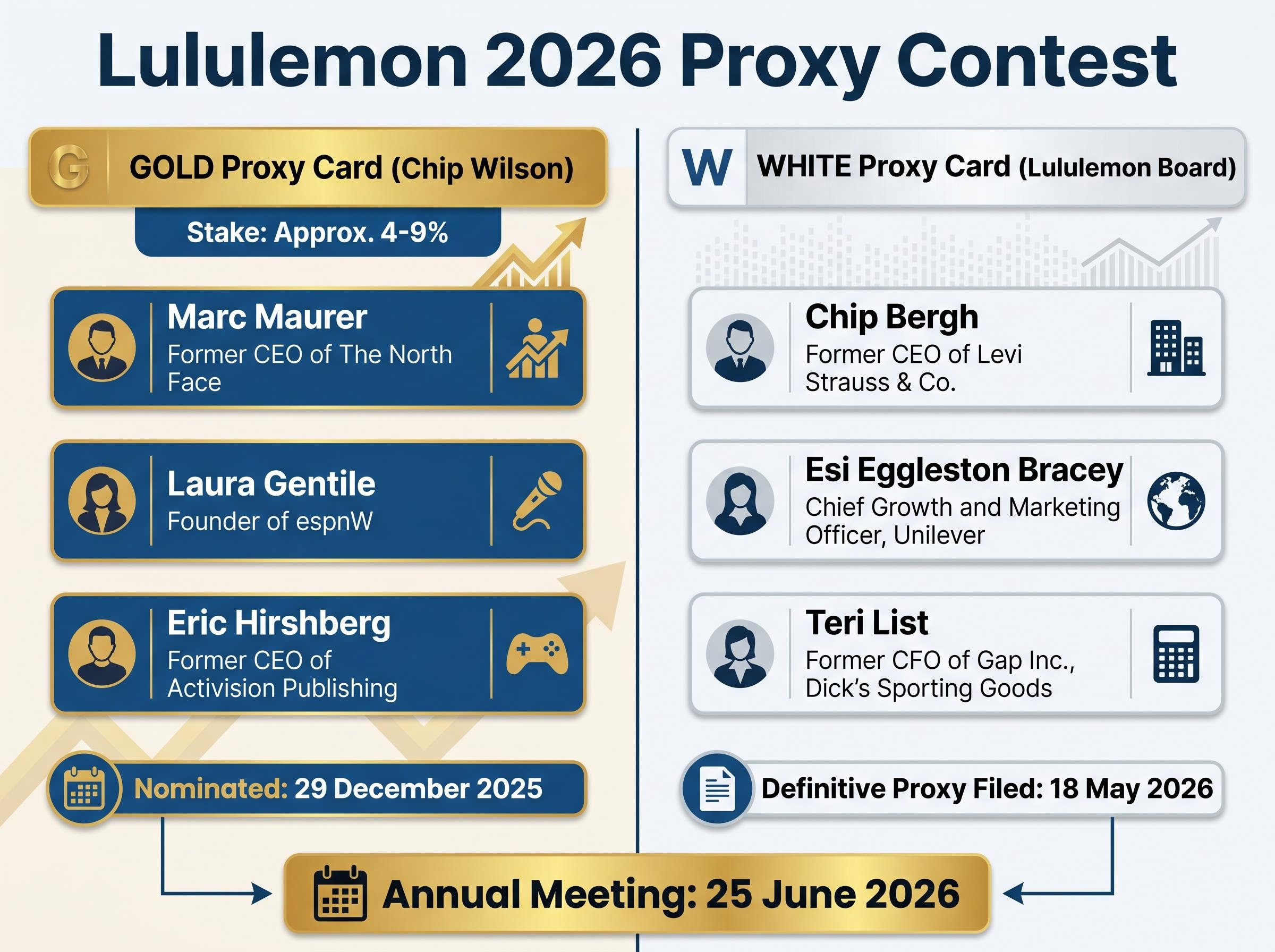

A founder who built a multi-billion-dollar athletic brand is waging a formal proxy battle against a board whose members hold equity stakes near the minimum required by the company’s own guidelines, while collecting roughly $250,000 per year in director fees. Chip Wilson, Lululemon’s largest individual shareholder, filed a GOLD universal proxy card and nominated three director candidates ahead of the June 25, 2026 Annual Meeting. This is not a personality clash. It is a structural governance dispute about whether the people overseeing a public company have enough personal wealth at risk to care about its share price the way ordinary shareholders do. This guide explains what “skin in the game” means in a boardroom context, why it matters for long-term investment outcomes, and provides a practical checklist for evaluating director alignment in any public company.

What “skin in the game” actually means in a boardroom context

The intuition is simple: people who own something protect it differently from people who are paid to watch over it. In corporate governance, that intuition sharpens into a specific, measurable concept. A director has meaningful skin in the game when a significant decline in the company’s share price produces real personal financial pain, not a minor portfolio adjustment.

The distinction matters because many boards satisfy their company’s ownership guidelines without ever crossing the threshold into genuine alignment. A director holding the minimum required equity while collecting approximately $250,000 per year in cash retainer and equity awards has a secured income stream. The fees arrive regardless of whether the share price rises 30% or falls 30%. The ownership guideline is met on paper. The incentive structure, however, remains decoupled from shareholder outcomes.

The governance gap in numbers: Wilson has argued that Lululemon directors receive roughly $250,000 annually in total compensation while holding only minimal equity stakes, per the company’s own proxy beneficial ownership tables.

Consider two director profiles side by side:

- Director A holds a stake worth several multiples of annual compensation, purchased partly with personal capital. A 20% share price decline costs them hundreds of thousands of dollars. Their financial motivation to drive returns is direct and ongoing.

- Director B holds equity at or near the minimum guideline threshold, accumulated entirely through granted compensation. A 20% share price decline costs them a fraction of a single year’s fees. Their income is largely indifferent to performance.

Both directors are technically compliant. Only one is genuinely aligned.

A September 2025 article on the Harvard Law School Forum on Corporate Governance (by Morgan Lewis attorneys) confirmed that institutional investors and proxy advisors now scrutinise director equity ownership as a standard governance metric. For retail investors, learning to read this distinction in a proxy statement transforms it from a compliance document into a signal about how seriously a board treats shareholder capital.

When big ASX news breaks, our subscribers know first

The Lululemon proxy contest as a live case study in governance misalignment

The governance principle has a name and a date. Chip Wilson, whose reported ownership stake in Lululemon has ranged from approximately 4% to nearly 9% across different filings and time periods, nominated three independent director candidates on 29 December 2025: Marc Maurer, Laura Gentile, and Eric Hirshberg. He filed a GOLD universal proxy card and has been campaigning publicly since issuing open letters in May 2025.

Investors wanting to trace the full arc of the dispute from Wilson’s private negotiations through to the public campaign will find our full explainer on how the Lululemon proxy fight escalated, which covers the failed settlement discussions, the staggered board declassification proposal, and the specific timeline of Wilson’s interventions from early 2025 through the June 2026 vote.

Lululemon responded with its own slate. The company filed definitive proxy materials on 18 May 2026, recommending shareholders vote for Chip Bergh, Esi Eggleston Bracey, and Teri List on the WHITE proxy card. The Annual Meeting is scheduled for 25 June 2026.

| Proxy Contestant | Nominee Slate | Basis of Standing | Core Argument |

|---|---|---|---|

| Chip Wilson (GOLD card) | Marc Maurer, Laura Gentile, Eric Hirshberg | Largest individual shareholder (approx. 4-9%) | Directors lack meaningful equity exposure; governance misalignment |

| Lululemon Board (WHITE card) | Chip Bergh, Esi Eggleston Bracey, Teri List | Incumbent board recommendation | Current board composition serves shareholder interests |

Wilson’s core objection is structural, not personal. Directors holding minimal equity while collecting fixed annual fees are insulated from the consequences of poor strategic decisions. His financial exposure, worth hundreds of millions of dollars, is qualitatively different from theirs.

Lululemon’s classified board structure, which staggers director elections so that only a subset of seats comes up for a vote in any given year, complicates Wilson’s path to seating three nominees at a single meeting and is one of the structural features institutional proxy advisors have scrutinised alongside the ownership alignment concerns at the centre of his campaign.

What Wilson is actually proposing beyond the director swap

Wilson’s 6 May 2026 open letter went beyond nominating replacement directors. He proposed establishing a brand product committee at Lululemon, modelled on a structure he implemented at Amer Sports, whose portfolio includes Arc’teryx, Salomon, and Wilson (the sports equipment brand). The proposal connects governance reform to operational oversight: Wilson is arguing not just for different directors, but for a different way the board engages with brand and product strategy at the highest level.

Why founder vision and board alignment have an uneven track record historically

The stakes of this type of governance decision are not theoretical. One of the most studied corporate governance episodes in history began with a board removing its founder.

- 1985: Apple’s board removed Steve Jobs, motivated by internal conflicts over management direction.

- 1985-1997: Apple cycled through multiple CEOs. Product focus eroded. Brand identity weakened. The company’s competitive position deteriorated over roughly a decade.

- 1997: Jobs returned as interim CEO and began restructuring the company’s product strategy.

- 1998-2007: The iMac (1998), iPod (2001), and iPhone (2007) followed, each redefining its respective market.

Apple subsequently became the most valuable consumer company in history. The founder’s product vision, once dismissed by a board that had lost confidence in it, proved to be the company’s most valuable strategic asset.

A board that marginalises its founder’s product vision may be eliminating a competitive advantage that cannot be hired back.

The analogy has limits. Not every founder is right, not every board is wrong, and the Lululemon situation is unresolved. Wilson’s more proximate track record is at Amer Sports, where he held an approximately 16-20% stake following the company’s early 2024 IPO and sold approximately $160 million worth of shares in August 2025. He credits the brand product committee structure he established there with revitalising the portfolio’s brand identities.

The Apple precedent does not guarantee a parallel outcome at Lululemon. What it does is illustrate the scale of value that can be created or destroyed when a board makes decisions about founder involvement, a consideration that is financially material, not sentimental.

Warren Buffett’s framework for reading board incentives as an investor signal

The governance tension visible at Lululemon maps onto a durable investment evaluation framework. Warren Buffett has long argued that boards should be composed of directors who think and act like owners, not like professional directors whose primary relationship with the company is their annual fee.

The specific signal Buffett’s philosophy highlights is the distinction between two types of director equity exposure:

- Granted equity: Shares or share equivalents received as part of the director compensation package. These represent value the company gave the director, not a personal financial commitment.

- Purchased equity: Shares bought by the director on the open market with personal capital. These represent a deliberate decision to put personal wealth at risk alongside ordinary shareholders.

Both appear in the same beneficial ownership table. They do not carry the same alignment signal. A director whose entire equity position consists of granted shares has made no independent financial bet on the company’s future. A director who has additionally purchased shares with personal capital has.

Research from the Harvard Law School Forum on Corporate Governance (September 2025, Morgan Lewis) confirmed that institutional investors and proxy advisors view meaningful non-employee director equity ownership as a positive alignment signal. ISS and Glass Lewis both assess director ownership as part of governance evaluation, though neither prescribes a universal minimum.

The Berkshire succession offers a real-time test of whether an owner-operator governance culture can survive the departure of the owner-operator who built it, with Greg Abel inheriting nearly $400 billion in reserves and a capital allocation mandate that carries no formal requirement to deploy capital the way Buffett would have.

The difference between mandatory minimum holdings and genuine ownership culture

Many large companies structure director ownership requirements as a multiple of the annual cash retainer. The requirement sets a floor, not a target. A director who holds exactly the minimum and no more is structurally different from one who holds several multiples of that minimum, partly through open-market purchases.

Proxy beneficial ownership tables disclose the actual number of shares or share equivalents held by each director. The data is there. The question is whether investors look at it.

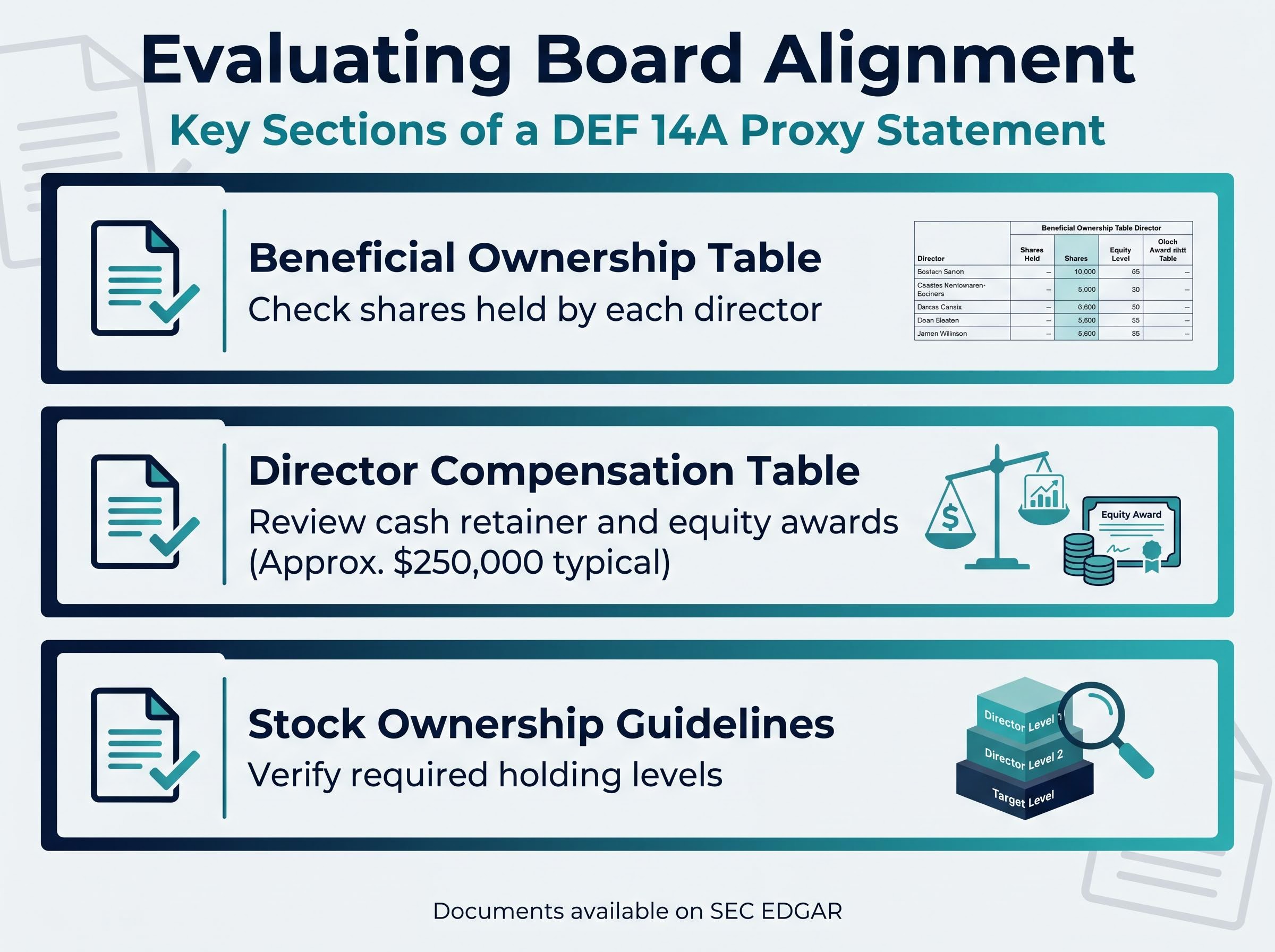

A practical checklist for evaluating board alignment in any public company

Three sections of a proxy statement contain the information needed to evaluate director alignment. All are publicly available on SEC EDGAR and on company investor relations pages at no cost.

The SEC proxy disclosure requirements mandate that DEF 14A filings present all material facts about matters on which shareholders are asked to vote, including director elections, making the beneficial ownership table and director compensation disclosures a legally required window into board alignment rather than voluntary reporting.

| Section Name | Where to Find It | What to Look For |

|---|---|---|

| Beneficial Ownership Table | DEF 14A proxy statement, typically near the front | Number of shares held by each director; market value at current price |

| Director Compensation Table | DEF 14A, “Director Compensation” section | Total annual compensation breakdown: cash retainer, equity awards, other |

| Stock Ownership Guidelines | DEF 14A or Corporate Governance Guidelines (often cross-referenced) | Required holding level (usually expressed as a multiple of cash retainer) |

With those three sections open, the following steps provide a repeatable evaluation process:

- Locate the beneficial ownership table and note each non-employee director’s share count.

- Calculate the current market value of each director’s holdings using the current share price.

- Compare that value to annual director compensation. Non-employee director total compensation commonly reaches approximately $250,000 per year at large-cap companies.

- Check the stock ownership guidelines disclosure for the company’s required holding threshold.

- Look for evidence of open-market purchases versus holdings composed entirely of granted equity. Some proxy statements disclose transaction history; others require checking Form 4 filings on EDGAR.

- Flag directors at or near the minimum threshold with no evidence of personal purchases. These are the positions where alignment is weakest.

A starting point for scepticism: If a director’s total equity holding is worth less than two to three years of their annual director fees, that is a signal worth investigating further, not a definitive judgement, but a prompt for deeper scrutiny.

The September 2025 Harvard Law School Forum on Corporate Governance article (Morgan Lewis) found that institutional investors now expect robust disclosure around director ownership guidelines and actual holdings. Retail investors can apply the same lens using freely available public filings.

The Lululemon vote is a test case for whether shareholder pressure can fix board culture

The 25 June 2026 Annual Meeting will answer a specific question: are institutional shareholders willing to back a founder-led governance challenge against an established board, or will incumbent directors hold their seats regardless of alignment concerns?

As of 27 May 2026, both proxy cards are in circulation. Wilson’s GOLD card asks shareholders to vote for Maurer, Gentile, and Hirshberg. Lululemon’s WHITE card asks for votes for Bergh, Eggleston Bracey, and List. Lululemon’s definitive proxy materials were filed on 18 May 2026. The contest is active and unresolved.

Two outcomes are possible, and each carries a distinct governance signal:

- Wilson’s nominees are seated. This would indicate that institutional shareholders are willing to act on ownership alignment concerns and that proxy contests grounded in governance structure (rather than pure financial engineering) can succeed. Boards across the market would face increased pressure to demonstrate genuine equity alignment.

- Board nominees are retained. This would suggest that incumbent boards retain significant structural advantages in contested elections, even when a large shareholder raises well-documented alignment concerns. The governance conversation continues, but the mechanism for change proves limited.

What other companies can learn from this moment

The structural problem Wilson has identified at Lululemon is not unique to Lululemon. Many large-cap boards have director equity holdings representing a small fraction of a single year’s director fee income. As proxy advisors and institutional investors increase their scrutiny of ownership guidelines, per the September 2025 Harvard Law School Forum findings, boards across the S&P 500 face growing pressure to demonstrate genuine alignment rather than nominal compliance.

Regardless of how the Lululemon vote resolves, the governance principle it illustrates applies to every public company an investor owns. Boards without genuine skin in the game represent a structural risk. Investors who learn to identify that risk, using the proxy statement tools outlined in this guide, will read governance signals that most retail investors never look for.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

These statements are speculative and subject to change based on market developments and company performance. Past performance does not guarantee future results.