Why Governance and Communication Drive Post-IPO Value

3 hrs ago

A company can report genuinely strong results in its first quarters as a public entity and still watch its stock fall 15% or more. That paradox sits at the centre of post-IPO investing, and it points to something most investors miss entirely: the forces that determine whether a newly listed stock rewards or punishes its shareholders are largely set in motion before the first trade ever executes. The window spanning six to eighteen months after listing is where those pre-listing decisions collide with reality. Most investors arrive at that moment without the tools to tell whether they are looking at a genuine business problem or a structural deal problem they inherited from pricing day. What follows gives you a framework for reading deal construction quality before committing capital, so you can separate a business worth owning from a deal structure worth avoiding, regardless of what the underlying company actually does.

An IPO is not a starting line. It is a decision point that hard-codes the expectations against which every subsequent quarter will be judged. Once a company moves from private to public ownership, the market stops evaluating potential and begins measuring actual delivery against the specific commitments made during the listing process. Every projection shared during the roadshow, every peer comparison drawn, every total addressable market figure cited becomes a benchmark the market will hold management to, quarter by quarter.

That makes the roadshow something more than a marketing exercise. It functions as an implicit contract. The expectations baseline is set once, at pricing, and it cannot easily be reset without significant reputational cost. Its construction is, by that logic, the single most consequential pre-listing decision a company makes.

“Post-IPO price action is driven by deviations from that baseline rather than by absolute business performance.”

For the first 12 to 18 months of public life, pre-listing choices matter more for returns than almost any tactical decision management can make afterward. The deal’s architecture is already working for or against shareholders before trading opens.

The IPO underperformance data stretching from 1980 to 2024 reinforces the mechanism described here: newly listed companies have lagged comparably sized established peers by an average of 3.3% per year over their first five years, a drag that compounds structurally rather than correcting once the initial hype fades.

In a standard IPO, management and their advisers are both pulling in the same direction: towards the highest achievable price and a completed transaction. Long-term shareholders, by contrast, are best served by moderate pricing, conservative guidance, and realistic narratives.

No principal party in the standard IPO process is directly penalised for a forecast that proves too aggressive after listing. That structural gap means the bias toward optimism is not an exception. It is the expected output of the system. For investors, this means every element of IPO communication should be treated as biased upward by design.

When a company lists at revenue and EBITDA multiples well above those of comparable public peers, the premium is rarely backed by anything more than aggressive growth assumptions that demand highly consistent execution over several years. That is not simply an optimistic starting point. Mathematically, it leaves almost no room for the ordinary operational variability any business encounters.

The outcomes that follow are binary. If execution matches the aggressive assumptions, the stock can hold or extend its premium. But when even a small shortfall materialises, it tends to produce a disproportionate price correction, because the market is not only processing the immediate news. Investors are also revising their broader confidence in management’s ability to forecast accurately, and questioning whether the entire multi-year growth thesis was soundly constructed from the start.

| Pricing scenario | Multiple vs. peers | Execution tolerance | Likely outcome if small miss | Likely outcome if execution matches guidance |

|---|---|---|---|---|

| Richly priced deal | Substantial premium | Near zero | Sharp downward re-rating; confidence loss compounds the price impact | Premium holds or extends |

| Conservatively priced deal | In line or modest discount | Meaningful buffer | Limited downside; market absorbs normal variance | Positive re-rating as execution builds credibility |

Three signals suggest a premium lacks structural justification:

Hype-driven listings compound the valuation premium problem because sentiment prices in best-case outcomes before a single public share trades, effectively removing the margin of error that conservative pricing would otherwise preserve for incoming shareholders.

Ritter’s long-run IPO performance data from the University of Florida documents a persistent pattern of post-listing underperformance relative to comparable public firms across multiple decades and market cycles, which is broadly consistent with the structural optimism embedded in deal pricing rather than any systematic deterioration in the underlying businesses themselves.

For you as an investor, a company priced at a large premium to peers is not just expensive at listing. It is structurally fragile for the first 12 to 18 months, because a single quarter of normal business variance can produce an outsized, and potentially lasting, impairment to the stock. The premium multiple is the mechanism through which the deal transfers execution risk entirely onto the buyer.

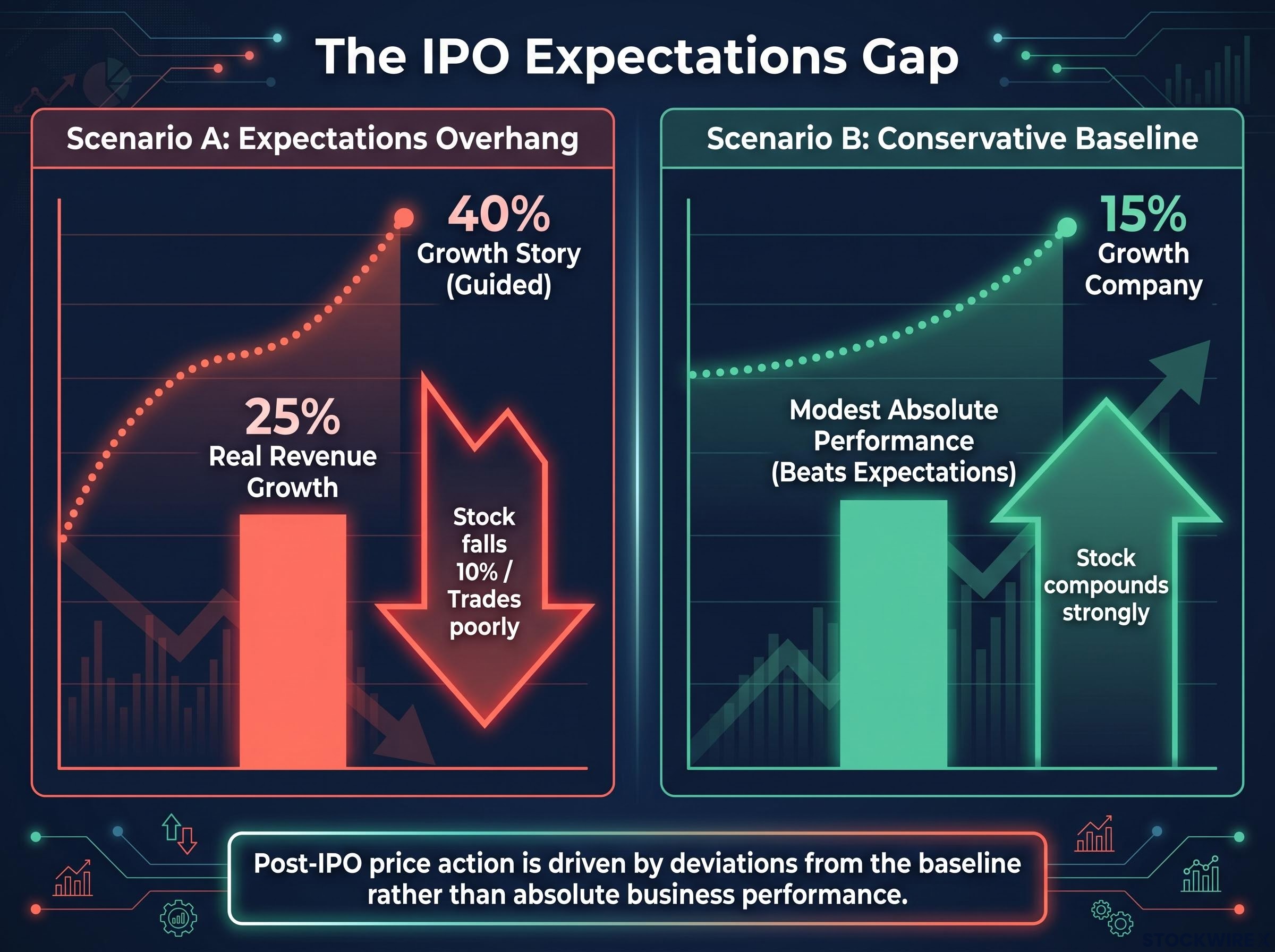

Here is the paradox named at the start of this piece, unpacked. A company grows revenue by 25% year on year. By most measures, that is a strong result. But the stock falls 10% on the day. What happened?

The answer is that markets do not move on whether results are objectively good. They move on whether results beat or miss the expectations that were already priced in. These are two entirely separate measures, and it is performance relative to the embedded expectations, not the raw numbers themselves, that dictates post-IPO price action over the short to medium term.

Two scenarios make this concrete:

The second company is the weaker business on paper. It is the better stock. That distinction is the analytical lens separating informed IPO investors from those chasing story quality.

“Companies that perform well in secondary trading are not necessarily those with the strongest absolute results, but those whose outcomes align with what was communicated during the listing process.”

For any investor evaluating a new listing, the question that matters most is not “is this a good business?” It is: “is the expectations baseline set at a level this business can consistently beat, or does it require a best-case scenario in every quarter just to stay flat?”

In their first year as a public company, newly listed businesses must manage three challenges at once: getting to grips with more demanding reporting obligations, navigating a new and potentially impatient set of shareholders, and maintaining operational performance while under a level of external scrutiny they have not previously faced. Each is manageable in isolation. Together, they compound.

This is precisely why a stretched expectations baseline is particularly dangerous. The company is dealing with maximum institutional complexity at the exact moment it needs maximum execution reliability. Conservative initial framing is not timidity. It is risk management.

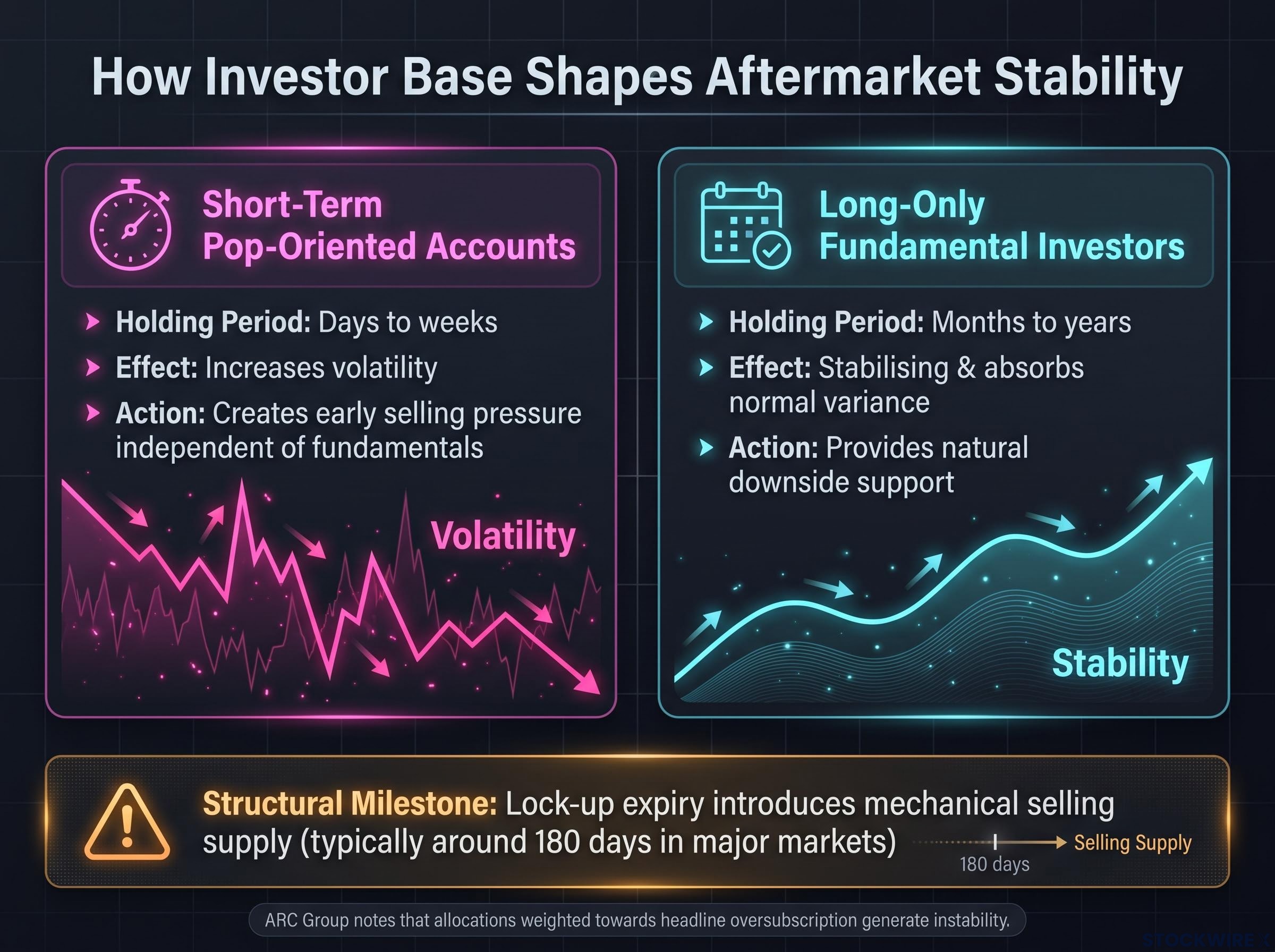

The quality of a company’s business is one variable governing post-IPO price behaviour. The composition of who actually owns the stock is another, and it operates independently of fundamentals.

Two investor base archetypes produce mechanically different aftermarket outcomes. Flip-oriented accounts enter IPOs to harvest an early gain and rotate out quickly, generating selling pressure in the initial weeks and months that has nothing to do with how the business is actually performing. Long-only fundamental investors, by contrast, accumulate their positions gradually and tend to step in as buyers when sentiment turns or results disappoint slightly, providing a stabilising floor under the stock.

| Investor type | Typical holding period | Effect on aftermarket volatility | Support during weak periods |

|---|---|---|---|

| Short-term pop-oriented accounts | Days to weeks | Increases volatility; creates early selling pressure independent of fundamentals | Minimal; exits at first sign of weakness |

| Long-only fundamental investors | Months to years | Stabilising; absorbs normal variance | Provides natural downside support; adds on weakness |

Deals constructed to maximise oversubscription optics rather than curate high-conviction holders introduce structural volatility that will surface the moment the first headwind arrives. ARC Group has noted that when allocations are weighted towards achieving headline oversubscription figures rather than securing genuinely committed shareholders, the resulting ownership base tends to generate instability that is very difficult to correct once the company is listed.

Retail investors cannot see book-building dynamics directly. But they can observe meaningful signals from the outside: early trading volatility relative to actual business news, the pace and scale of post-open price deterioration, and the relationship between volume spikes and price action.

If a newly listed stock experiences sharp volatility in the first weeks without any material news catalyst, the more productive question is not “what is wrong with the business?” It is “what does the shareholder base look like, and is this selling structural rather than fundamental?”

The lock-up expiry period (typically around 180 days in major markets) is a structurally significant event worth monitoring. Lock-up expiry introduces mechanical selling supply regardless of business performance, and for retail investors considering entry, the post-lock-up period may offer both more information and more stable pricing than day-one participation.

The analytical layers established above convert into a six-point evaluation sequence you can run before allocating capital to any new listing. Each dimension is framed as a question worth answering before you commit.

The FCA primary market guidance on lock-up disclosure sets out the specific prospectus obligations companies face when structuring these agreements, including requirements to disclose the duration, scope, and any release conditions that could accelerate supply into the market before the nominal expiry date.

“Treat the first quarterly report as an audit of the roadshow.”

A clean beat or in-line result validates initial guidance discipline. A miss is evidence of structural optimism baked into the deal, and it warrants a full re-rating of your risk assumptions. Running this framework before allocation reveals whether an IPO is structurally set up to reward you over the first 12 to 18 months, or whether the deal has been constructed to serve the sellers at listing rather than the buyers who will live with the stock afterward.

The core argument of this analysis reduces to a single distinction: the quality of a business and the quality of an IPO as an investment vehicle are related but separate assessments. Conflating them is the most common, and most costly, mistake investors make when participating in new listings.

Pre-listing decisions about valuation, investor base composition, and narrative construction create structural conditions that either support or undermine aftermarket performance, largely independently of the business’s intrinsic quality. Investors who focus exclusively on business fundamentals and ignore deal structure are exposing themselves to risks that are not business risks at all. They are deal construction risks, baked in before the stock ever traded.

Post-IPO return profiles are not uniformly negative for public shareholders: cases like Planet Labs, which delivered a tenfold share price increase entirely in public markets after listing, demonstrate that when deal structure is managed conservatively and insider selling pressure is reduced through staggered lockups, the framework described here can work in the buyer’s favour rather than against them.

| Structural factor | Risk if poorly managed | Benefit if well managed |

|---|---|---|

| Valuation vs. peers | Low tolerance for operational variance; binary re-rating risk | Headroom to absorb normal execution volatility |

| Investor base composition | Early selling pressure; reduced support during weak periods | Price stability; patient capital during first-year challenges |

| Equity narrative | Persistent expectations gap; recurring disappointment cycle | Credibility buffer; positive surprise potential |

| Lock-up structure | Mechanical supply overhang at predictable intervals | Predictable shareholder base evolution |

| Market regime at pricing | Normalisation risk as euphoric multiples compress | Realistic starting valuation with less compression risk |

| First earnings print | Structural optimism confirmed; risk re-rating triggered | Guidance credibility established; valuation supported |

Both institutional and retail investors can apply this framework, though through different access points:

The investor who separates business quality from deal quality is the one positioned to participate in new listings selectively and profitably, rather than inheriting the embedded risks of a roadshow narrative designed to serve the sellers.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding IPO outcomes and market behaviour are subject to change based on market conditions and various risk factors.

—

The main factors are valuation relative to peers, the conservatism of the expectations baseline set during the roadshow, investor base composition, lock-up structure, and the market regime at pricing. These structural variables shape aftermarket performance largely independently of the underlying business quality.

Markets move on whether results beat or miss the expectations embedded at pricing, not on whether results are objectively strong. A company that guided for 40% growth and delivers 25% real growth will see its stock fall even though 25% growth is a solid result, because every quarter disappoints relative to the baseline set at listing.

The lock-up expiry, typically around 180 days in major markets, is the point at which early shareholders such as founders and pre-IPO investors are permitted to sell their shares. It introduces mechanical selling supply regardless of business performance, which can pressure the stock even when underlying results are sound.

Retail investors can evaluate publicly observable signals: revenue and EBITDA multiples relative to sector peers, the specificity or vagueness of total addressable market claims, disclosed lock-up expiry dates, and whether the first quarterly earnings report confirms or contradicts the roadshow narrative.

The expectations baseline set at pricing typically governs stock behaviour for the first 12 to 18 months of public life, a window in which pre-listing deal construction decisions matter more for returns than almost any operational decision management can make afterward.