Every generation of investors discovers the same pattern: an exciting new theme ignites, prices surge, the financial media declares a new era, and then the stocks quietly collapse while the underlying technology limps on. The technology was often real. The investment was still disastrous.

Thematic investing, building part of a portfolio around a broad economic or technological trend, has a genuinely mixed track record. The internet, cloud computing, and mobile technology rewarded patient believers handsomely. But 3D printing, cannabis, and buy-now-pay-later each attracted serious capital, credible narratives, and real investor losses. Understanding what separates the two categories is not a minor refinement to investment thinking. It is a foundational skill.

This guide uses the historical record of both failed and durable themes to build a practical five-question framework that any investor can apply to the next wave of hype, whether that is artificial intelligence, space commercialisation, longevity biotech, or whatever comes after.

Why thematic investing is so seductive, and so dangerous

Thematic investing means constructing portfolio exposure around a broad economic, technological, or social trend rather than individual company fundamentals. Instead of asking “Is this specific company undervalued?”, the thematic investor asks a different question: “Is this trend going to be important, and which companies will benefit?”

The appeal is genuine. Several features make this approach feel intuitively right:

- Big trends do create big winners. The internet, e-commerce, and cloud computing all rewarded investors who recognised them early and stayed the course.

- Themes are easy to relate to. Smartphones are everywhere, streaming has replaced cable television, and instalment payment options appear at every online checkout.

- Early movers in legitimate themes can be richly rewarded over long time horizons.

- The reasoning feels like useful, real-world observation rather than abstract financial modelling.

Where the trap closes

The core problem is that a real trend and a profitable investment theme are not the same thing. Seeing BNPL options at checkout and treating that observation as investment-grade insight conflates visibility with valuation.

Easy relatability is not a valuation framework. A trend can be genuinely reshaping consumer behaviour while every listed company riding it is overpriced, under-moated, or structurally unprofitable. Confusing the two is where most thematic investors go wrong, and the rest of this guide explains how to avoid that mistake.

When big ASX news breaks, our subscribers know first

The graveyard: what 3D printing, cannabis, and BNPL have in common

Three distinct themes attracted serious investor capital in the past decade. Each had a compelling narrative, real underlying activity, and a painful outcome.

3D printing offered a seductive pitch: machines that could manufacture physical objects layer by layer from digital files, potentially democratising production. Stocks like 3D Systems and Stratasys soared as investors priced in explosive, sustained manufacturing disruption. The technology proved genuine and useful in aerospace, medical devices, and rapid prototyping, but the mass-market revolution never arrived. Consumer printers gathered dust. The addressable market was far narrower than implied, and traditional manufacturing remained cheaper and more efficient for most applications.

Cannabis legalisation rode a powerful emotional narrative. Prohibition was ending, an enormous illegal market was entering the legal economy, and early movers would scale like consumer-packaged-goods giants. What followed was slower, messier, and more expensive than any model assumed. Illegal operators undercut legal prices. Banking access in the United States remained constrained by federal law. Regulatory progress was fragmented and unpredictable. Companies burned through cash and repeatedly diluted shareholders. Many stocks fell 80-95% from peak levels, with some going bankrupt, despite continued growth in cannabis consumption.

Buy-now-pay-later became a defining fintech theme of the early 2020s. Afterpay was acquired for tens of billions at peak enthusiasm. Klarna’s private valuation reached tens of billions. Affirm’s IPO valuation implied extraordinary long-term growth. When interest rates rose sharply, funding costs surged for companies that relied on short-term borrowing to front purchases. Regulators began treating BNPL as consumer credit. Traditional banks and card networks introduced their own instalment products, eroding whatever differentiation existed.

| Theme | Core Pitch | What Went Wrong | Key Lesson |

|---|---|---|---|

| 3D Printing | Democratise manufacturing; desktop factories for everyone | Mass-market use case never materialised; addressable market far narrower than priced | Real technology does not guarantee a large, investable market |

| Cannabis | Legalisation unlocks a massive new consumer industry | Regulatory timelines missed; illegal competition persisted; commodity economics, not platform margins | A growing industry can still destroy capital if competitive and regulatory assumptions are wrong |

| BNPL | Young consumers reject credit cards; fintech super-apps emerge | Business model depended on near-zero rates; banks easily copied the product | Macro-dependent models are fragile; incumbents can replicate low-moat innovations |

“In each case, investors confused a real phenomenon with a durable, well-priced investment opportunity.”

What the winners had that the fads did not

The internet, cloud computing, and mobile technology are often treated as obvious-in-hindsight successes. They were not obvious at the time. But they shared identifiable structural properties that distinguished them from the themes that failed.

The dot-com bust proved that even a genuine revolution can destroy capital at the wrong price. Many internet companies of the late 1990s were terrible businesses or absurdly valued. Yet the infrastructure and platform winners, Amazon being the most frequently cited example, generated extraordinary long-term returns. The addressable market was effectively everything that could be digitised, and surviving businesses built mission-critical infrastructure with durable competitive advantages.

The structural pattern

Cloud computing succeeded because it solved a huge, concrete, persistent problem. Enterprises were spending heavily on on-premise IT that was capital-intensive, inflexible, and difficult to scale. The cloud offered elastic capacity, predictable costs, and access to advanced tools. The addressable market was enormous: global enterprise IT spending. The time horizon was measured in decades. And leading platforms such as AWS, Azure, and Salesforce developed switching costs and ecosystems that made migration away from them costly and risky.

Mobile technology functioned as a platform multiplier. Once billions of people carried connected computers, the addressable market for any digital service became the global population. Entire categories, payments, streaming, ride-sharing, social media, did not exist at meaningful scale before smartphones enabled them.

Across these durable themes, the same structural properties appear repeatedly:

- They solved large, obvious, persistent problems that existing solutions addressed poorly.

- Their addressable markets were vast and often expanded over time as new use cases emerged.

- They became embedded infrastructure or platforms that other businesses built upon.

- Leading companies developed durable competitive advantages, including switching costs, network effects, and ecosystem lock-in.

- Their structural time horizons stretched across decades, not business cycles.

A five-question framework for evaluating any thematic investment

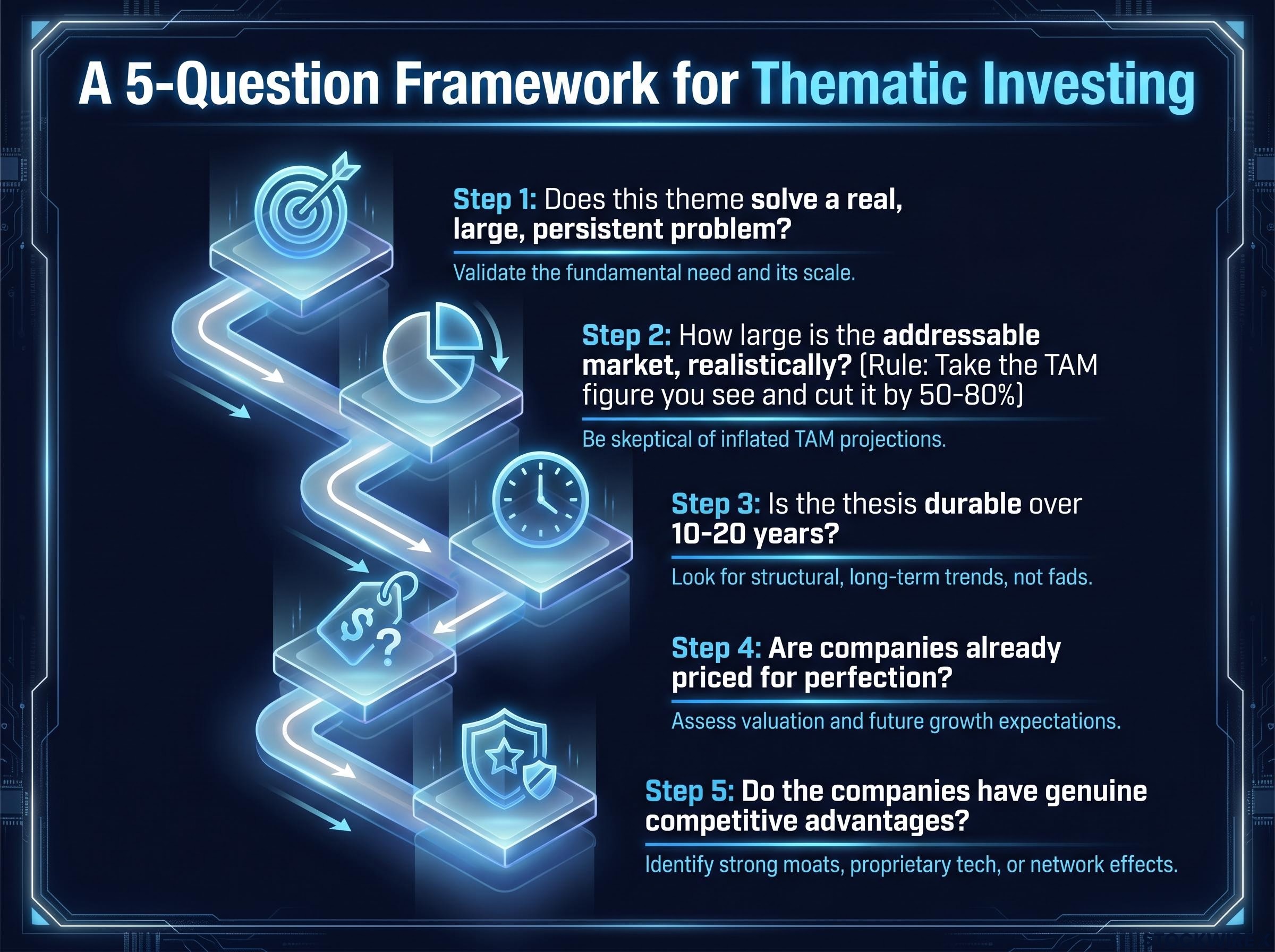

The historical record of successes and failures distils into five questions that stress-test any emerging theme before capital is committed. A theme can pass some questions and fail others. The framework produces a calibrated view of risk rather than a binary yes or no.

1. Does this theme solve a real, large, persistent problem?

Identify the specific problem, who has it, and why existing solutions fail. Cloud computing passed this test because enterprises were overspending on rigid, on-premise IT. Cannabis largely failed it because the thesis rested on regulatory change rather than a technological solution to an unmet need. If articulating the problem requires speculative or political assumptions, treat that as a red flag.

2. How large is the addressable market, realistically?

Every pitch deck features a massive total addressable market (TAM), the total revenue opportunity available if a product or service captured its entire potential customer base. Fads inflate TAM by double-counting categories, assuming rapid global adoption, and treating adjacent markets as guaranteed.

“Take the TAM figure you see and cut it by 50-80%. Does the investment still make sense on those conservative assumptions?”

If the thesis only works at full TAM, it is probably relying on optimistic assumptions rather than robust analysis.

Durability, valuation, and competitive advantage

3. Is the thesis durable over 10-20 years?

Identify the two or three conditions that must hold true for the theme to succeed over decades. If those conditions include “rates stay low,” “regulators remain hands-off,” or “consumer enthusiasm never fades,” proceed with caution. BNPL’s early narrative depended heavily on near-zero interest rates and minimal regulatory scrutiny, conditions that were never guaranteed. Durable themes reflect structural changes that become more entrenched as infrastructure, habits, and ecosystems build around them.

4. Are companies already priced for perfection?

Model roughly what needs to happen for today’s price to be reasonable: revenue growth over five to ten years, sustainable margins, and a reasonable valuation multiple at maturity. If flawless execution, category dominance, and unusually high margins are all required just to justify current valuations, that is a warning sign. Being right about the theme and wrong about the investment, by overpaying, is one of the most common outcomes in thematic investing.

5. Do the companies have genuine competitive advantages?

Ask what prevents a well-funded competitor from taking share. Cloud platforms benefit from high switching costs: once enterprise workloads are deeply embedded in AWS or Azure, migration is costly and risky. Internet and mobile platforms benefit from network effects and ecosystems. By contrast, cannabis producers operate in commodity-like markets with low differentiation. BNPL’s product was easy for incumbent banks and card networks to replicate. If the answer to the competitive advantage question is essentially “nothing,” the business is probably weak even within a strong theme.

Applying the framework to AI, and to whatever comes next

No current theme illustrates the tension between genuine potential and investment risk more clearly than artificial intelligence.

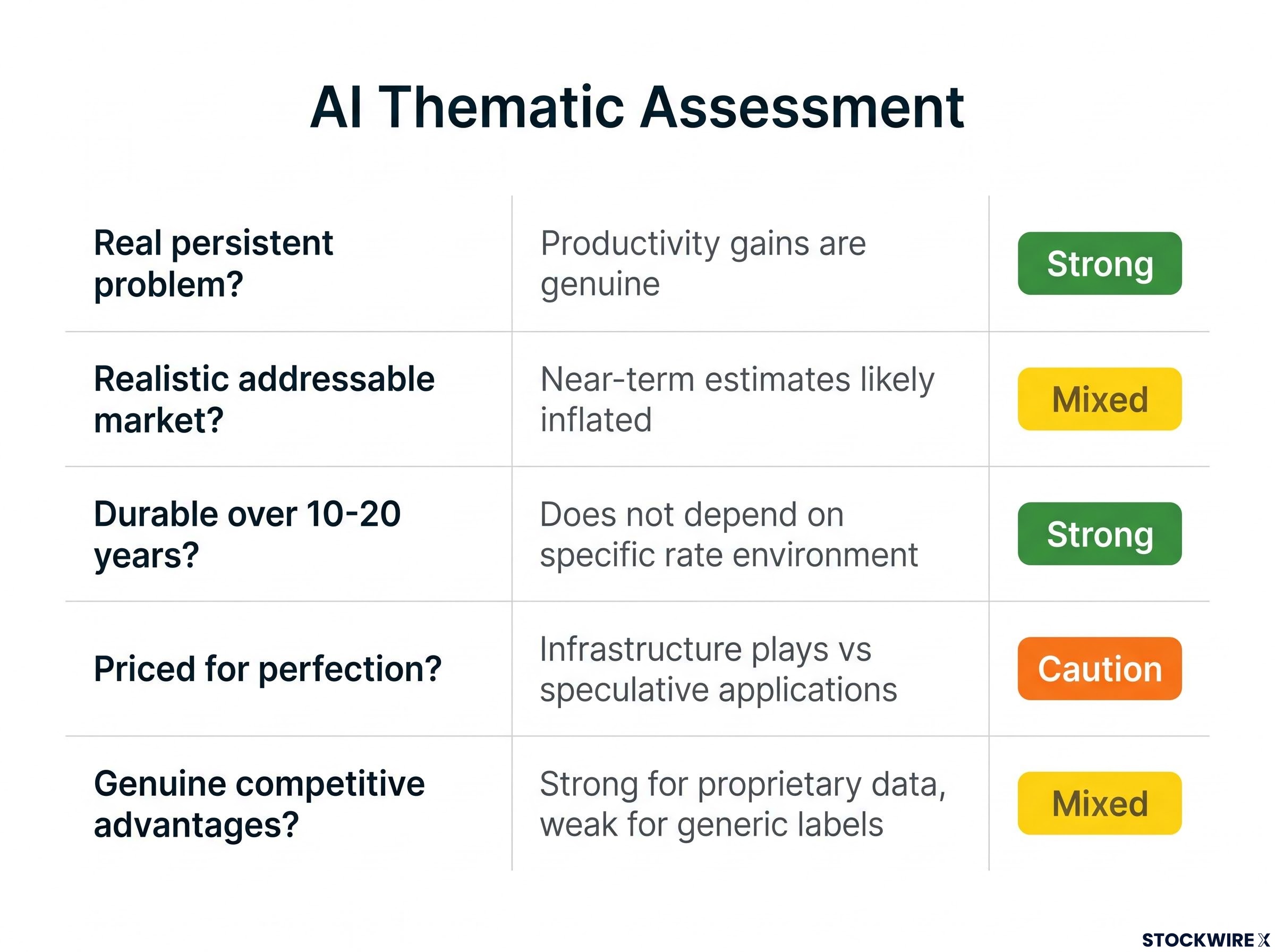

Running AI through the five-question framework produces a nuanced verdict rather than a simple endorsement or dismissal. AI clearly solves real, economically meaningful problems in software development, content creation, customer service, and analytics. Near-term TAM figures are likely inflated, but even conservative estimates leave a very large opportunity. The durability of AI does not depend on a specific interest rate environment or political stance, unlike BNPL. It looks structurally more like cloud computing than cannabis.

| Question | AI Assessment | Verdict |

|---|---|---|

| Real, large, persistent problem? | Productivity gains across knowledge work, software, and analytics are genuine and economically measurable | Strong |

| Realistic addressable market? | Potentially massive, but near-term estimates likely inflated; conservative figures still large | Mixed |

| Durable over 10-20 years? | Does not depend on specific rate environment or regulatory stance; structural capability improvement | Strong |

| Priced for perfection? | Infrastructure plays (semiconductors, data centres) can be valued traditionally; many “AI application” companies look speculative | Caution |

| Genuine competitive advantages? | Strong for firms with proprietary data, workflow integration, or differentiated models; weak for those adding AI labels to undifferentiated products | Mixed |

The distinction between AI infrastructure plays and AI application companies matters. Semiconductor and data-centre businesses can be evaluated with more traditional valuation tools. Companies that are simply wrapping a generic model in an application, without proprietary data or meaningful integration into customer workflows, look far more speculative.

The same framework applies to themes that do not yet dominate headlines:

- Space commercialisation: real problems (connectivity, Earth observation), but TAM and competitive dynamics remain highly uncertain.

- Longevity biotech: genuine unmet medical need, but regulatory timelines and clinical success rates introduce substantial risk.

- Quantum computing: potentially transformational capability, but commercial applications remain years away for most use cases.

The honest answer for most nascent themes is “interesting but too early to have conviction on the winners.”

The theme was right. The investment was still wrong. How to avoid that trap.

“Identifying a real trend is the beginning of the work, not the end.”

Most investors in 1999 knew the internet was important. Many still lost money because they paid prices that assumed perfection, backed weak companies, and ignored competitive dynamics. Investors in 3D printing, cannabis, and BNPL often correctly identified that the technology or consumer behaviour was real. Their mistake was treating that insight as sufficient to invest rather than as a prompt for deeper analysis.

Six practical rules, drawn directly from the case studies above, can improve outcomes:

- Separate the theme from the stocks. A trend can be obviously real while every visible stock tied to it is overvalued or low quality.

- Be sceptical when regulation is the core driver. Regulatory change is unpredictable in timing and scope. Cannabis is the clearest example of a thesis built on a political schedule that never arrived on time.

- Watch how the story is being sold. When a theme dominates social media, retail podcasts, and ETF marketing, it often signals peak enthusiasm, not early opportunity.

- Use thematic ETFs carefully. They often launch after a theme is already popular, concentrate in the most expensive names, and charge higher fees than broad index funds.

- Size positions to reflect uncertainty. Thematic bets should usually be small slices of a diversified portfolio. History suggests investors misjudge specific themes more often than they expect.

- Continuously revisit the thesis. Unlike a broad index fund, a thematic position requires ongoing monitoring of market size, competition, regulation, and valuation. A thesis that was sound two years ago may no longer hold.

Thematic investing cannot eliminate risk. But asking the right questions, and refusing to confuse enthusiasm with durability, greatly improves the odds of participating in the next real revolution without being swept away by the next fad.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.