Most investors judge a newly listed company by its first-day performance. The stock pops, the roadshow narrative feels validated, and the position seems to be working. But first-day price action is close to meaningless as a predictor of whether a stock holds its value over the following two to three years. The evidence points elsewhere entirely. Two operational disciplines, corporate governance and investor communication, determine whether a company’s post-IPO valuation compresses or drifts. Governance shapes whether minority shareholders can trust the company is being run in their interests. Communication shapes whether expectations stay aligned with what the business actually delivers. Together, they set the discount rate the market applies to the company’s future cash flows, and that discount rate is the primary lever on sustained valuation. What follows is a framework for separating structurally sound listings from those likely to drift: what to look at, what questions to ask, and how to tell whether a recently listed company is worth holding beyond the IPO window.

Why the post-IPO window is where value is made or lost

The roadshow builds the story. Management presents the thesis, the growth trajectory, the addressable market. Investors price that narrative into the IPO. Then the company lists, and every subsequent quarter becomes a test of whether the story holds.

IPO long-run underperformance is not a recent anomaly: data spanning 1980 to 2024 shows newly listed companies lagging comparably sized established peers by an average of 3.3% per year over their first five years, a drag that compounds into a gap of more than $2,100 on every $10,000 invested before governance and communication quality even enter the picture.

This is what makes the first eight to twelve quarters of public life so consequential. During that window, the market is actively collecting signals and updating its beliefs about whether the IPO thesis will be delivered. The signals investors are weighing include:

- Guidance accuracy: does management hit, beat, or miss the targets it sets?

- Board response to setbacks: does the company adapt visibly, or does the narrative go quiet?

- Ownership structure changes: are insiders selling at the earliest opportunity?

- Management accessibility: does the executive team engage with investors consistently, or only when results are strong?

The stakes in this window are disproportionate. An early miss in the first or second quarter of public life lands with far greater market force than the same shortfall would two or three years into the company’s listed life, because it revises what investors believe about management’s ability to forecast and lead, not merely about near-term cash flows.

Earnings surprises and guidance revisions trigger outsized price moves in the post-IPO period because they update beliefs about management credibility and risk, not just cash flows.

Empirical research evaluating IPO long-run performance over three-to-five-year horizons finds that a meaningful subset of IPOs outperform due to strong oversight and disciplined execution. But it also finds that even fundamentally sound businesses can face protracted confidence restoration if early expectations were misaligned. If you hold or are evaluating a recently listed position, the first year of public life is a credibility audit, not just a financial reporting cycle. The cost of early communication errors is higher than it looks.

When big ASX news breaks, our subscribers know first

What institutional investors actually examine in board composition

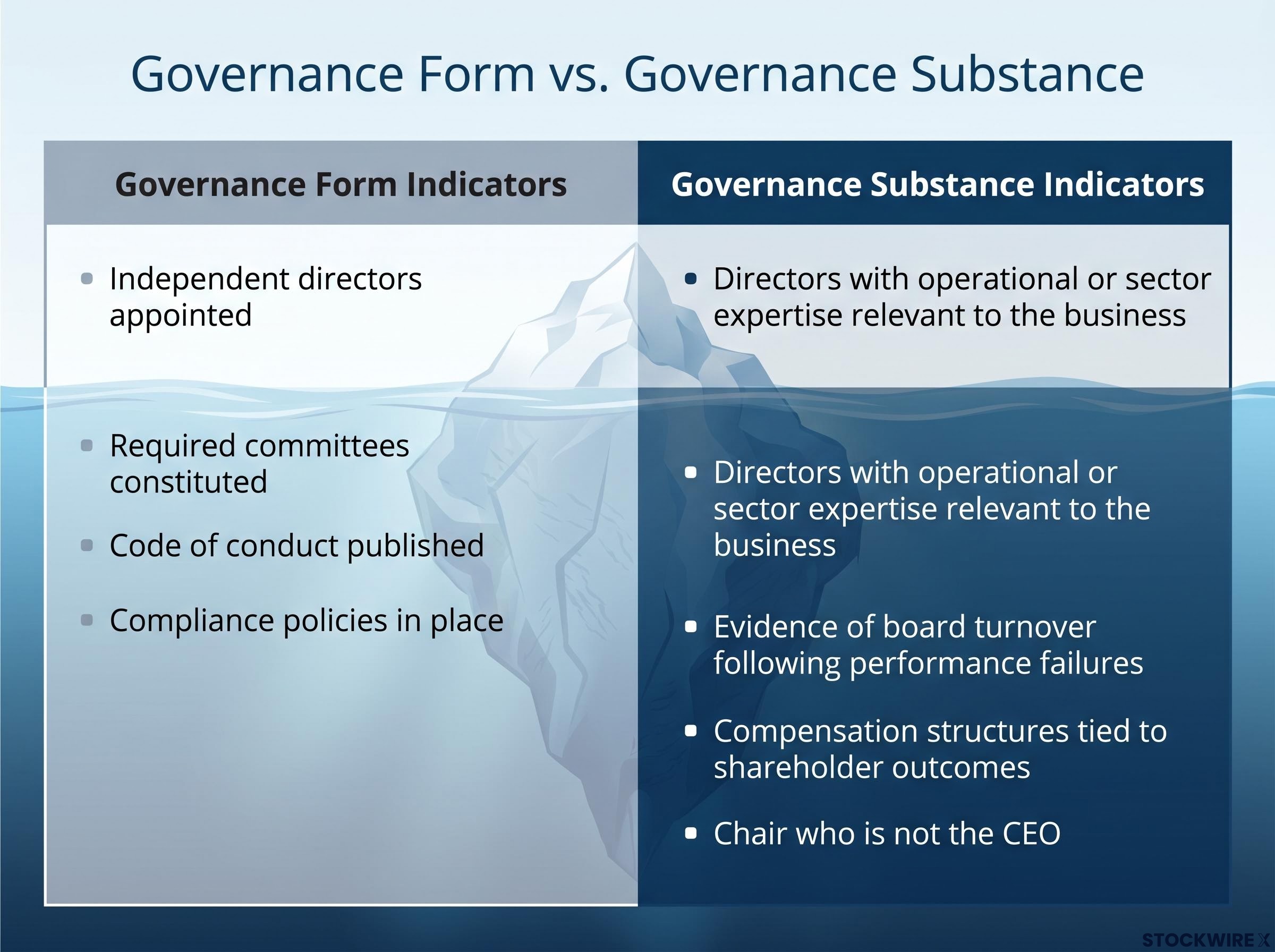

Most governance disclosures read like compliance documents. Independent directors are listed. Committee memberships are ticked off. Audit, remuneration, nomination: all present. But sophisticated institutional investors look past credentials to function, and the distinction matters more than most retail investors realise.

The difference is between governance form and governance substance. Form means the required structures are in place: independent directors appointed, committees constituted, policies written. Substance means those directors operate with genuine independence, have relevant expertise, receive adequate information, and are willing to challenge management when the situation demands it. Directors who hold strong credentials on paper but sit passively around the boardroom table give minority shareholders very little meaningful protection in practice.

Board equity alignment goes further than checking whether directors hold stock: the distinction between equity granted as compensation and equity purchased with personal capital is one of the signals institutional investors and proxy advisors now treat as a standard governance screen, and it is visible in the beneficial ownership and director compensation tables of any public company’s proxy statement.

Research broadly supports the view that firms with stronger pre-IPO governance, including more independent boards, separation of CEO and chair, and stronger shareholder rights, tend to achieve higher IPO valuations and better long-run operating performance. The market prices governance substance, not just governance form.

Here is what to look for when reading a board composition disclosure:

- Governance form indicators: independent directors appointed, required committees constituted, code of conduct published, compliance policies in place

- Governance substance indicators: directors with operational or sector expertise relevant to the business, evidence of board turnover following performance failures, compensation structures tied to shareholder outcomes, chair who is not the CEO

Executive compensation arrangements that reward management irrespective of share price performance signal a potential misalignment between leadership and shareholders, whether or not that is the intention. Investors assessing alignment risk treat these arrangements accordingly.

The index inclusion problem

There is a structural dimension to governance quality that many individual investors overlook. Large institutional and index investors increasingly integrate governance screens into index inclusion and stewardship decisions. Passive index strategies now represent a large share of equity ownership. That means governance compatibility with institutional policy is directly relevant to trading liquidity and valuation premium.

Governance arrangements that conflict with index providers’ stewardship policies can lead to reduced demand or explicit exclusion, with compounding effects on liquidity. For you as an investor, the practical read is that governance structures designed without regard for institutional policy compatibility introduce a structural headwind to valuation durability that is entirely distinct from operating performance.

The structures that attract measurable valuation discounts

Certain governance arrangements carry specific, empirically documented pricing penalties. Understanding the conditions under which they apply, rather than treating them as blanket red flags, gives you a more precise basis for evaluating a recently listed company.

Dual-class share structures are the most visible example. A dual-class structure gives certain shareholders (typically founders) disproportionate voting power relative to their economic ownership. Evidence indicates that dual-class IPOs often price at a discount or experience a valuation penalty over time compared with single-class peers. The penalty is sharpest when there are no sunset clauses (provisions that convert the structure to one-share-one-vote after a set period), no performance safeguards, and no credible founder track record to offset perceived entrenchment risk. That said, some dual-class structures are justified by innovation context or long-horizon R&D requirements, making the conditional assessment necessary rather than a blanket rule.

ECGI research on dual-class firm valuations confirms that the pricing penalty for these structures is most pronounced in the absence of sunset provisions and verifiable founder performance records, supporting the conditional rather than blanket assessment investors should apply when evaluating newly listed companies with complex share structures.

Related-party transactions, where a listed company transacts with entities controlled by its founders or major shareholders, attract similar scrutiny. Empirical work in emerging markets and family-controlled firms shows that higher related-party dealing is associated with lower valuation multiples and weaker long-term stock performance. The market assumes some probability of value leakage from minority shareholders.

In Asian and emerging market listings, governance weaknesses tend to attract particularly close scrutiny from investors, with pricing consequences that can run to several valuation multiples.

| Structure Type | Discount Trigger Conditions | Mitigating Factors | Investor Question to Ask |

|---|---|---|---|

| Dual-class shares | No sunset clause, no performance safeguards, weak founder track record | Clear sunset provisions, strong innovation or R&D rationale, demonstrated founder value creation | Is the voting premium justified by a specific business need, and does it have a defined expiry? |

| Related-party transactions | High transaction volume, opaque pricing, board members with conflicts of interest | Independent audit committee oversight, arm’s-length pricing verification, full disclosure | Are related-party transactions reviewed independently, and is pricing disclosed at a level that allows verification? |

For you, the question when assessing a newly listed company with these structures is not whether they exist but whether the specific safeguards, track record, and business context are strong enough to justify accepting the structural risk at the current valuation.

How credibility is won and lost through investor communication

Investor communication is not a cosmetic function. It is a core valuation mechanism, and the asymmetry in how it works is the most important thing to understand. Credibility is built incrementally, one quarter at a time, through a track record of setting achievable targets and meeting or modestly beating them. It is destroyed in a single quarter by an unexplained miss.

Companies that follow the “meet and beat” model, setting conservative, achievable post-IPO targets and then delivering consistently, build the kind of credibility that stabilises the shareholder base and supports higher multiples over time. When management permits the gap between market expectations and operational delivery to widen, recovering investor confidence becomes a lengthy and difficult exercise, even if the core business has not fundamentally deteriorated.

Management credibility signals compound across reporting cycles: credible teams typically flag capital raise intentions well in advance, miss ranges infrequently, and maintain consistent narrative framing even when results are below plan, while teams with weak transparency records tend to narrow guidance ranges before misses and reduce investor engagement in the periods that matter most.

IPO communication guidance stresses that overly optimistic roadshow narratives may produce a larger first-day pop but increase the risk of post-IPO underperformance when early quarters do not match the implied trajectory. The credibility gap between roadshow promises and operational delivery is where lasting valuation damage occurs.

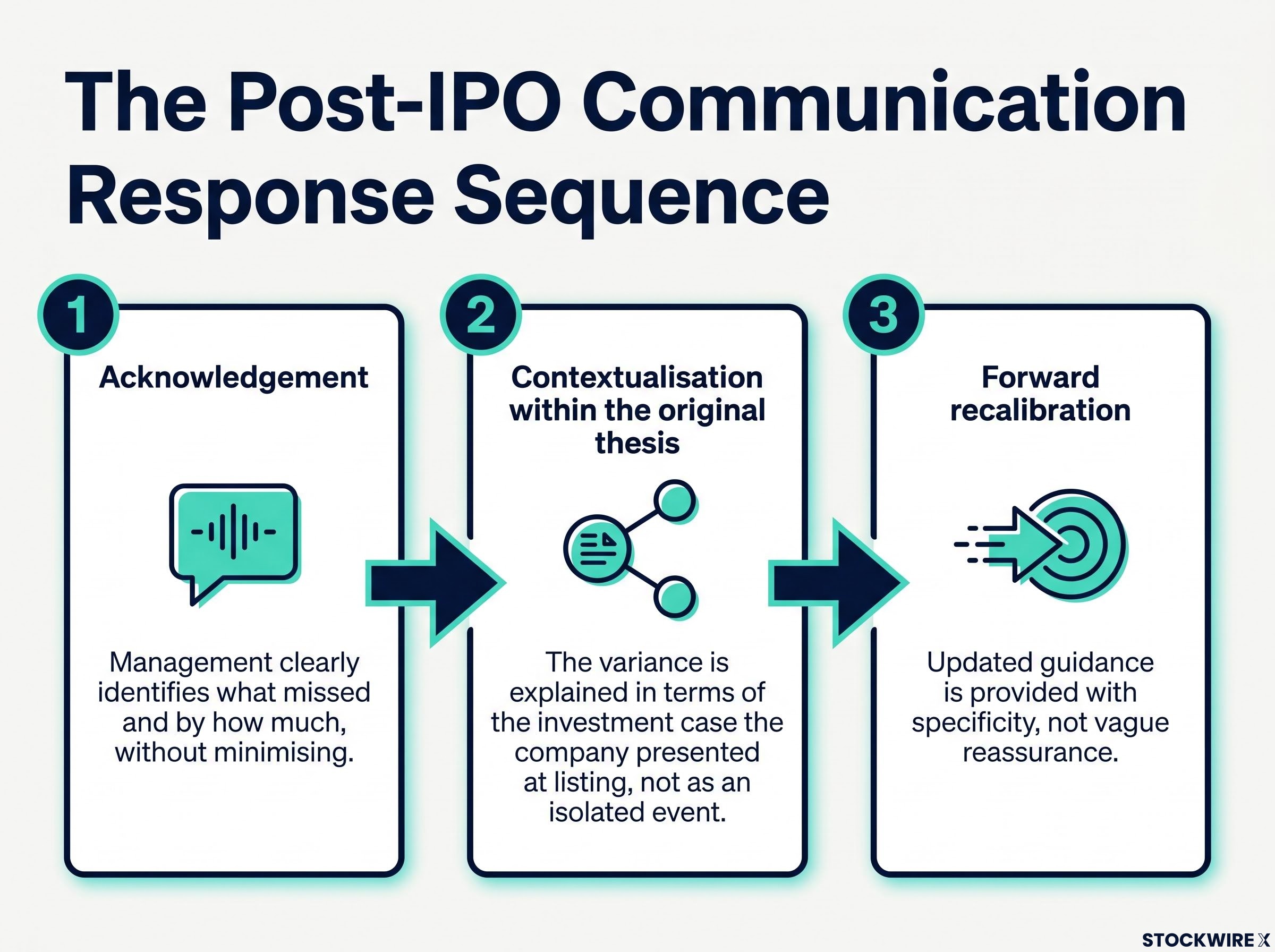

What matters most is what happens when things go wrong. Delaying or soft-pedalling bad news is consistently associated with sharper drawdowns and more persistent valuation damage than the underlying miss alone. The response pattern you should look for after a guidance miss follows a specific sequence:

- Acknowledgement: Management clearly identifies what missed and by how much, without minimising.

- Contextualisation within the original thesis: The variance is explained in terms of the investment case the company presented at listing, not as an isolated event.

- Forward recalibration: Updated guidance is provided with specificity, not vague reassurance.

Accessibility and transparency during adverse periods are more important to long-run credibility than performance during strong ones.

If you hold a recently listed stock through a guidance miss, the key diagnostic question is whether management explained the variance clearly and within the original thesis, or whether they went quiet. The response pattern tells you more about long-run holding risk than the miss itself. Communication cannot eliminate execution risk, but it gives you a clearer view of where the business is heading, what choices management is making, and the logic underpinning those decisions.

Why governance and communication only work when they reinforce each other

Each discipline is necessary. Neither is sufficient on its own. The failure modes that emerge when one is present without the other make this clear.

Strong governance with weak communication means the board may be functioning well, the oversight may be genuine, and the incentive structures may be aligned, but if none of this is visible through earnings calls, investor days, and transparent capital allocation disclosures, the market cannot fully price the governance quality. The result is a company that is better-run than its valuation implies, but where the discount persists because investors lack the informational basis to lower their required return.

Strong communication with weak governance means management may be articulate, accessible, and transparent in messaging, but without a credible board and clean audit structure, every statement is treated with elevated scepticism. Investors have no structural assurance that the numbers and narratives are reliable. The informational discount remains elevated regardless of messaging quality.

- Failure mode one: Strong governance, weak communication. Governance quality is partially hidden from the market and therefore only partially priced. The company trades below its structural quality.

- Failure mode two: Strong communication, weak governance. Messaging is treated with elevated scepticism. The informational discount persists despite high-quality IR.

Research on IPOs in different interest-rate environments reinforces this interaction. When risk-free rates are low, governance quality and credible forward guidance matter even more, because a larger share of valuation is driven by far-out cash flows whose discount rate is highly sensitive to perceived governance and information risk. Reputable venture capital or private equity sponsors with active monitoring roles can partially substitute for weaker formal governance structures in the transition period immediately following listing.

The pre-listing constraint

The architecture for both governance and communication must be designed before listing, because post-listing disciplines cannot correct structural mispricing set by aggressive IPO positioning. An overstretched equity story, a low-quality investor base attracted by hype rather than fundamentals, or aggressive pricing can set expectations that even strong governance and investor relations cannot subsequently correct. A low-quality investor base creates ongoing instability in the shareholder register that governance and communication cannot resolve.

Evaluating governance and communication separately, as if they were independent checklists, will miss the compounding risk that occurs when one is absent. A structurally sound board with opaque communication is still a valuation discount candidate.

A practical framework for evaluating post-IPO resilience

The preceding sections give you the conceptual foundation. This section converts it into a structured process you can apply to any recently listed position.

The evaluation runs on two axes: governance and communication. Assess each, then read them together.

- Governance axis first: Evaluate board substance, ownership structure, compensation alignment, and the absence of structural discount triggers (dual-class without safeguards, high related-party dealing).

- Communication axis second: Evaluate guidance track record across available quarters, management accessibility during adverse periods, and consistency of narrative between roadshow promises and subsequent reporting.

- Combined resilience read: Assess whether both axes reinforce each other. If governance is strong but communication is weak, expect the valuation to lag structural quality. If communication is polished but governance is thin, expect scepticism to persist.

The eight-to-twelve-quarter window post-listing is the practical signal-collection horizon. Early quarters carry more information weight per quarter than later ones, because credibility is being established, not just tested.

| Evaluation Axis | Key Questions to Ask | Red Flag Signals |

|---|---|---|

| Governance | Does the board have sector-relevant expertise? Is the chair independent from the CEO? Are compensation structures tied to shareholder outcomes? Are there sunset clauses on any dual-class arrangements? | Passive board with no visible response to setbacks; compensation decoupled from share price; high related-party transaction volume with no independent oversight |

| Communication | Has management met or beaten guidance in available quarters? Did management explain clearly when results diverged from plan? Is the executive team accessible to investors during difficult periods? | Guidance ranges narrowing before a miss; management going quiet after disappointments; narrative shifts that contradict the original IPO thesis without explanation |

Macro and sector conditions act as amplifiers. Governance and communication deficiencies tolerated in a bull market can produce severe derating in risk-off conditions. Research confirms that a meaningful subset of IPOs outperform long-run benchmarks due to strong oversight and disciplined execution, but neither governance nor communication eliminates execution risk or macro exposure. Your assessment framework should explicitly distinguish between valuation pressure from company-specific failures and pressure from external conditions.

What sustained post-IPO performance actually looks like from the outside

The framework is useful in the abstract, but what does it look like in practice? The observable patterns are surprisingly consistent.

Signs of a durable post-IPO trajectory:

- Consistent guidance delivery, or modest positive surprises, across multiple quarters

- Management that explains variance clearly and within the original thesis when results disappoint

- A board that visibly responds to challenges, whether through strategic adjustments, leadership changes, or capital allocation shifts

- A stable and growing institutional shareholder base

- Compensation arrangements that remain tied to share price and operating performance

Warning signals worth monitoring:

- Narrowing guidance ranges followed by misses

- Management going quiet or reducing investor engagement after disappointing quarters

- Compensation arrangements decoupling from share price performance

- A shareholder register showing institutional exits or rapid turnover

- Related-party transaction volumes increasing without clear business rationale

The market’s discount rate is not fixed. Governance and communication quality, consistently expressed over the first several years, determine whether it compresses or widens from the IPO level.

Empirical research finds that governance and communication explain a meaningful share of cross-sectional differences in long-run post-IPO performance, over and above fundamentals like size, sector, and leverage. Taken together, the two disciplines shape the speed and completeness with which investor trust can be reconstructed after a period of disappointing results.

Investors wanting to challenge the conventional assumption that venture insiders capture all the meaningful upside before listing will find our deep-dive into post-IPO return profiles for public shareholders, which examines evidence from Cerebras Systems, Planet Labs, and Altimeter Capital portfolio data to map where gains have actually accrued across the private-to-public transition in recent cycles.

The synthesis for you as an investor is this: post-IPO resilience is not primarily a question of whether the business model will succeed. It is a question of whether the company has built the governance and communication infrastructure to carry investors through the inevitable periods when things do not go to plan. That infrastructure is observable, assessable, and, most importantly, it is something you can evaluate before the next difficult quarter arrives.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

—