Every time markets seize up before a Federal Open Market Committee (FOMC) meeting, a quiet assumption takes hold: that a small committee in Washington can steer a $30 trillion economy with surgical precision. Investors reposition portfolios, pundits speculate on basis points, and entire trading floors hold their breath at 2:15 p.m. on a Wednesday. But has that assumption ever been stress-tested against the evidence? The Federal Reserve holds genuine, consequential power over short-term interest rates and crisis liquidity. That is not in dispute. The leap from “the Fed influences financial conditions” to “the Fed controls the economy,” however, is not supported by the historical record, by research on how rate changes actually reach the real economy, or by the Fed’s own forecasting accuracy. Milton Friedman made this argument decades ago. Ken Fisher has extended it across a full career of practitioner critique. By the end, you will understand exactly what the Fed can and cannot do, why the gap between those two things matters for how you think about your portfolio, and why crediting or blaming any Fed chair for broad economic outcomes is largely a compelling story rather than a precise causal claim.

What the Fed actually controls (and it is less than you think)

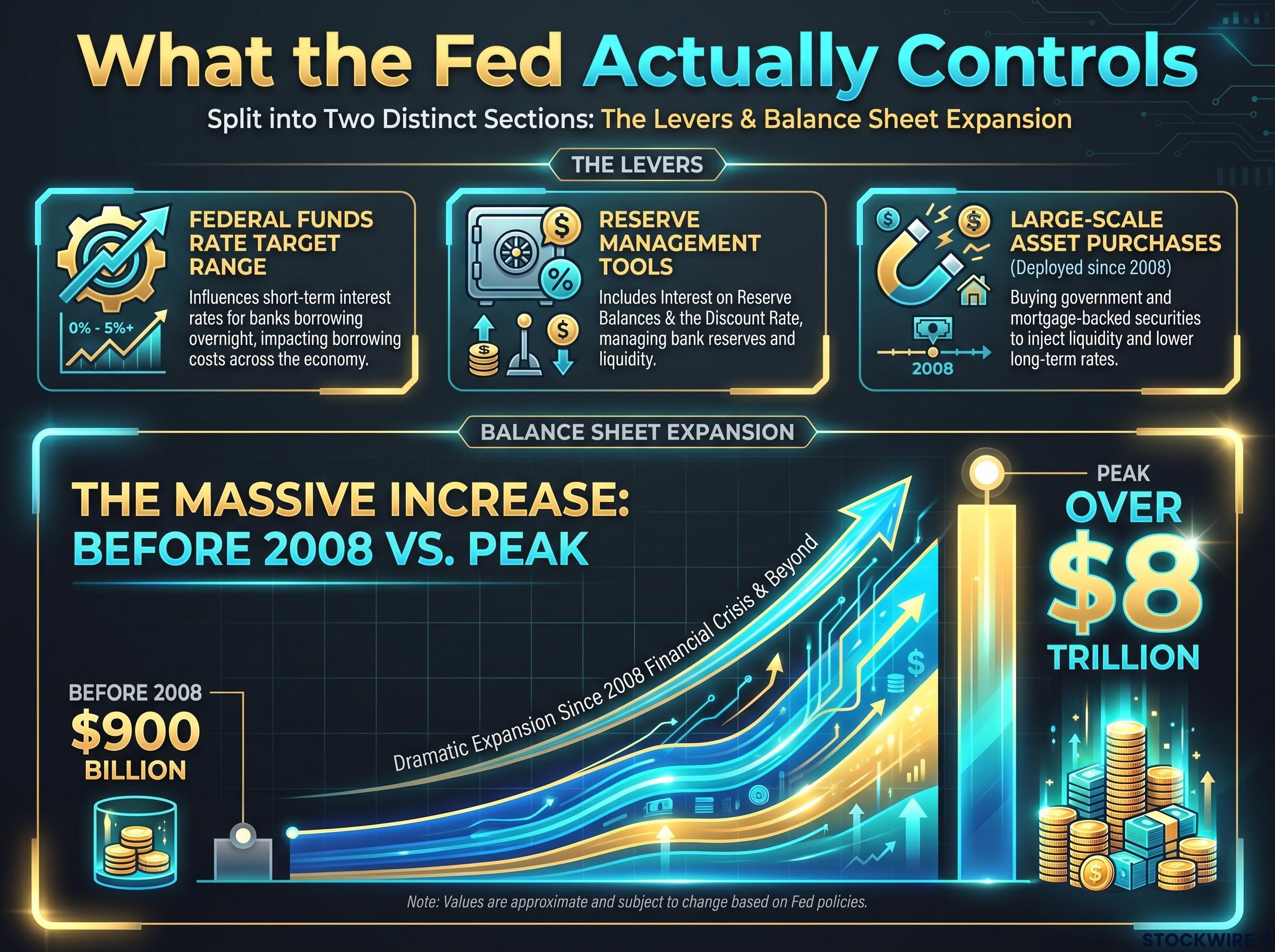

The Fed’s genuine powers deserve their due. Three levers sit directly under FOMC control:

- The federal funds rate target range: the overnight rate at which banks lend reserves to each other, set by the FOMC at each meeting.

- Reserve management tools: interest on reserve balances and the discount rate, which together keep the funds rate within its target range.

- Large-scale asset purchases: deployed since 2008, these involve buying government securities and mortgage-backed bonds to push down longer-term rates and inject liquidity into the financial system.

Within these tools, the Fed’s grip is strong. It can move short-term risk-free rates with precision, and its lender-of-last-resort function gives it decisive power during funding panics. In 2008-09 and again in March 2020, emergency liquidity facilities stopped panic spirals in their tracks. That function is an emergency brake, though, not a steering wheel. It activates at moments of acute stress and then steps back.

For readers wanting to understand why the lender-of-last-resort function exists in the first place, our dedicated guide to the Panic of 1907 traces how a contained copper trade failure cascaded into systemic collapse precisely because no institution held the authority to backstop confidence-sensitive funding, the structural gap that drove Congress to create the Federal Reserve by December 1913.

The distinction that matters is between the overnight interbank rate the Fed sets and the rates you actually encounter: mortgage rates, business loan rates, consumer credit. The Fed does not set any of those directly.

The St. Louis Fed’s monetary policy implementation overview details how interest on reserve balances, the overnight reverse repurchase agreement facility, and open market operations work together to keep the federal funds rate within its FOMC-set target range, confirming that the Fed’s direct grip ends at the overnight interbank market rather than extending to the borrowing costs consumers and businesses actually face.

Expectations management and its limits

The Fed’s most modern tool is forward guidance: public statements and projections (the “dot plot”) about where rates are heading. These shape how markets price the future path of policy, which in turn influences financial conditions today.

This channel is real. But it runs entirely through belief. If markets stop trusting the Fed’s commitments, forward guidance loses its power. That makes it inherently more fragile than rate-setting itself. The Fed’s balance sheet expanded from roughly $900 billion before 2008 to over $8 trillion at its peak, a measure of how extensively it has deployed non-traditional tools to compensate for the limits of rate policy alone. If you have been treating FOMC decisions as a master dial for the whole economy, you have been conflating one important input with the entire system.

When big ASX news breaks, our subscribers know first

The transmission problem: why rate changes do not steer the economy like a dial

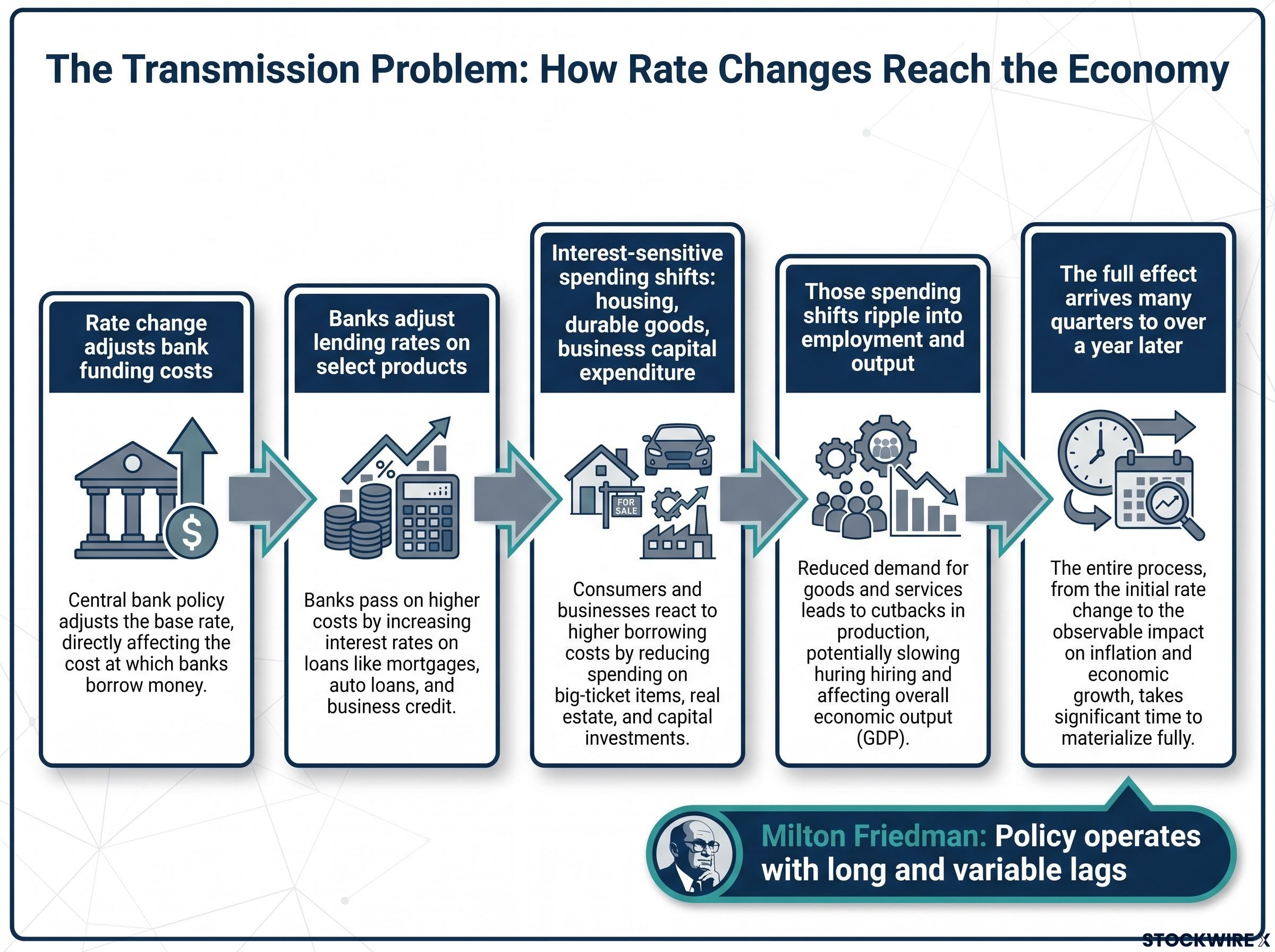

When the FOMC changes its rate target, the effect on the real economy travels through a long, uncertain chain:

- The rate change adjusts bank funding costs.

- Banks adjust lending rates on select products.

- Interest-sensitive spending shifts: housing, durable goods, business capital expenditure.

- Those spending shifts ripple into employment and output.

- The full effect arrives many quarters to over a year later.

Each link in that chain introduces its own uncertainty. A rate hike hits a homebuyer on a variable-rate mortgage immediately. It may barely touch a large corporation that locked in fixed-rate bonds at low rates in 2020-21. The transmission is uneven across sectors, across borrowers, and across time.

Milton Friedman described monetary policy as operating with “long and variable lags,” meaning that by the time a rate change fully affects the economy, the conditions that prompted it may have already shifted.

Research on the transmission mechanism confirms the problem. Studies indicate that monetary policy’s impact on real output has declined over time, even while its effects on inflation and asset prices remain significant. Financial deepening and globalisation have made the connection between short-term rates and real economic activity weaker and more complex than textbook models suggest.

The 2021-22 inflation episode is the live case study. The Fed’s delayed tightening, followed by the most rapid rate hiking cycle in decades, has produced active debate over how much of the subsequent disinflation reflects Fed policy versus fading supply shocks and fiscal changes. The lag and heterogeneity problems mean that by the time you can observe whether a policy move was the right size, it is already too late to correct it in real time. That is precisely why Friedman was sceptical of discretionary fine-tuning. And if the Fed itself cannot reliably predict the size or timing of its own policy effects, the informational edge from Fed-watching is far thinner than financial media coverage implies.

What central banks cannot do: the nominal-real distinction

This is the intellectual backbone of the critique, and it is worth understanding clearly. In his landmark 1968 address, “The Role of Monetary Policy,” Friedman drew a line between two categories of economic outcomes.

Friedman’s 1968 address on monetary policy, published in the American Economic Review, is where the nominal-real distinction and the natural rate of unemployment were formally introduced to macroeconomics, establishing the theoretical foundation that central banks can anchor the price level over time but cannot permanently lift employment or output above their structurally determined levels.

Nominal variables are expressed in dollar terms: the price level, the inflation rate, the amount of money circulating in the economy. Real variables are expressed in terms of actual output and wellbeing: how many goods an economy produces, how many people are employed, how fast living standards rise.

Friedman’s core argument was that monetary policy can determine nominal variables over the long run, particularly the price level and inflation, but cannot permanently push real variables above their structural level. Attempts to do so produce inflation rather than lasting prosperity.

The dual-mandate conflict became structurally irresolvable in 2026, with PCE inflation at 3.5% against a 2% target while unemployment simultaneously rose to 4.3%, a configuration that exposes the core problem Friedman identified: a single set of rate tools cannot simultaneously push a nominal variable toward target and prevent a real variable from deteriorating, because those two objectives can require opposite policy directions.

The concept that enforces this boundary is the natural rate of unemployment, sometimes called NAIRU (the non-accelerating inflation rate of unemployment). This is the unemployment rate consistent with stable inflation, determined by structural factors like labour market flexibility, demographics, and skills matching. If the Fed tries to hold unemployment below this rate through easy policy, the result is not permanent employment gains but rising inflation, as the 1970s painfully demonstrated.

Real growth, over the long run, depends on productivity, technology, demographics, and institutional quality. Monetary policy touches these only at the margin.

Three episodes that test the theory

| Episode | Fed Action | Nominal Outcome | Real Outcome | Lesson |

|---|---|---|---|---|

| Great Depression (1929-33) | Misjudged monetary contraction; allowed money supply to collapse | Severe deflation | Ordinary recession became a depression | Central bank mistakes can destabilise as powerfully as successes can stabilise |

| 1970s Stagflation | Overly accommodative policy; attempted to hold unemployment below natural rate | Inflation expectations drifted higher, forcing painful Volcker tightening | Stagnant growth alongside rising prices | Pushing real variables beyond structural limits produces inflation, not prosperity |

| Great Moderation (1985-2007) | Improved frameworks; credible inflation targeting adopted | Stable, low inflation for two decades | Reduced output volatility (though not solely due to the Fed) | The Fed’s genuine power over inflation can be used well or badly |

The Fed is the custodian of the price level, not the custodian of prosperity. Understanding that distinction helps you calibrate which macro outcomes to track the Fed on (inflation credibility) versus which ones to track elsewhere (growth, innovation, labour supply). The institution you should care about most for real long-run returns is not the FOMC but the forces shaping productivity and population growth, and those respond to fiscal policy, technology, and demographics far more than to rate decisions.

Why discretionary rate-setting tends to produce systematic error

Friedman, early in Fisher’s career, offered an image of central bank policymakers as akin to children at an amusement park bumper-car ride: compelled by their own nature toward constant intervention, forever reacting to circumstances that had already moved on, and generating overcorrections in each direction as a result.

Fisher has long regarded that image as an apt summary of central bank tendencies toward overactivity and has carried the argument into his own practitioner writing. In Fisher’s assessment, the officials responsible for setting rates operate from a fundamentally flawed model of how monetary systems work, which leads them to pursue outcomes that lie beyond the reach of their actual tools, and to get the direction or timing of moves wrong more often than they get them right.

Fisher goes further, contending that algorithmic rate-setting could plausibly do the job with greater consistency and fewer errors than a committee of human policymakers, a view that sits naturally within the longstanding rules-based tradition now being applied to emerging technology. This is not as radical as it sounds. The debate between rules and discretion has structured monetary economics for decades.

The rules-versus-discretion debate moved from theoretical to operational in May 2026, when Kevin Warsh was confirmed as Fed Chair under documented presidential pressure, creating an environment where market participants must assess whether rate decisions reflect economic data or political accommodation, the exact credibility problem the Nixon-Burns episode of the early 1970s demonstrated can persist for years before its costs become visible in inflation expectations.

The case for rule-based or algorithmic policy:

- Avoids groupthink and anchoring to recent data that plagues committee decisions

- Removes political pressure from rate-setting

- Applies consistent, transparent frameworks (Taylor rules, nominal GDP targeting) that empirical evidence suggests improve outcomes relative to ad-hoc discretion

The case against:

- Purely mechanical rules can fail badly in unprecedented environments

- Models are only as good as the data and structure they encode

- Institutional credibility still depends on human-led communication and expectations management

The 2021-22 “transitory” episode is the most recent illustration of the bumper-car dynamic: delayed recognition of inflation followed by the fastest tightening cycle in decades, then a recalibration. It fits the Friedmanesque pattern of lag-misjudging discretionary policy almost precisely.

The bumper-car critique is not an argument for abolishing the Fed. It is an argument for humility about what any committee of humans can achieve through discretionary rate-setting, and it should make you sceptical of narratives that credit or blame a single chair for broad economic outcomes. If rate-setting decisions are more often wrong than right, building your investment strategy primarily around anticipating those decisions correctly is a game with very thin odds.

Why the Fed-omnipotence story refuses to die

Three reinforcing dynamics keep an exaggerated story alive even when the evidence runs against it:

- Narrative preference for visible agents: The economy is a diffuse, emergent process with no single protagonist, so the Fed Chair becomes the default causal anchor because people need a face and a decision to explain outcomes.

- Media incentive structure: FOMC meetings are scheduled, televised events that supply predictable drama and deadlines, making them irresistible anchors for financial journalism regardless of whether any given decision is genuinely consequential.

- Investor psychology: It is cognitively easier to believe “my portfolio hinges on the Fed” than to grapple with global productivity dynamics, demographic shifts, and technological change, all of which are diffuse, slow-moving, and do not resolve at a specific time on a specific day.

Fisher frames this directly: the widespread cultural focus on the Fed Chair reflects a general public misunderstanding of the limited actual influence central banks have over economic outcomes through rate manipulation. Media cycles gravitate toward scheduled Fed events even in periods when policy rates are on hold and no material change is expected.

The psychology of controllable narratives

Behavioural economics offers a useful lens here. People gravitate toward narratives that imply control and tactical actionability, because uncertainty and diffuse causation are psychologically uncomfortable. Attributing economic outcomes to a single visible institution satisfies the demand for explanatory simplicity. This is entirely rational as a coping mechanism. But it produces systematic over-attribution to the Fed at the expense of structural analysis.

Recognising that the Fed-omnipotence narrative is partly a media and psychology artifact, rather than a reflection of demonstrated causal power, is itself a form of financial literacy. It protects you from reactive, headline-driven portfolio decisions. The hours you currently spend parsing Fed statements could be better spent analysing the structural variables that actually dominate long-run portfolio outcomes.

What the Fed’s actual limits mean for how you invest

Fed-watching is over-weighted in most retail investor mental models. Markets incorporate expected policy paths continuously, not only at FOMC meeting times, so the “surprise” available from any given decision is far smaller than meeting-day volatility implies. Because policy effects are lagged, partially anticipated, and filtered through complex transmission channels, trading primarily on FOMC tea-leaf reading produces noise rather than reliable edge.

There is one important exception. The Fed remains genuinely decisive for your portfolio in crisis conditions. The 2008-09 and March 2020 interventions, with emergency backstops, extraordinary facilities, and rapid balance-sheet expansion, produced large, discrete shifts in risk premia and market functioning. At those moments, the Fed’s lender-of-last-resort function matters enormously.

The practical reorientation is straightforward. Redirect your attention toward three areas that dominate multi-year equity returns far more than any specific rate level:

Valuation dislocations produced by a prolonged rate hold are not evenly distributed across sectors, and the mid-2026 equity market illustrates the point: technology, growth, and small-cap equities were trading at historically rare discounts to fair value while energy had repriced from undervalued to overvalued, a distribution that rewards investors who track structural variables rather than those positioned around a single FOMC outcome.

- Crisis signals: Monitor the Fed for signs of emergency posture (extraordinary facilities, emergency rate moves, balance-sheet signals) rather than routine meeting outcomes.

- Productivity trends: Long-run growth accounting evidence shows that productivity and innovation cycles drive equity returns over horizons of five years and beyond, well outside the Fed’s influence.

- Demographic dynamics: Labour force growth and population trends shape the structural growth rate of the economy, and these respond to immigration policy, fertility patterns, and education, not to the federal funds rate.

If the Fed itself cannot reliably engineer near-term macro outcomes, you should treat your own macro forecasts as highly uncertain. This supports diversified, long-horizon strategies over tactical macro bets.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The Fed matters, but not in the way most investors believe

The Fed is not powerless. It holds genuine long-run authority over the price level and inflation expectations, and its crisis-backstop function has been consequential at moments when financial stability hung in the balance. The argument has always been about the gap between its real influence and the omnipotence attributed to it. Two generations of economists and practitioners, from Friedman through Fisher, have made this critique, and the evidence from the Great Depression through the 2021-22 inflation episode suggests the concern is warranted rather than contrarian posturing. Treat Fed decisions as one input among many rather than the master variable. Weight structural forces, productivity, demographics, innovation, more heavily in your long-run view. And reserve your heightened attention for the moments when the Fed’s emergency brake actually engages, because that is where its power is real, consequential, and worth watching closely.