Why Governance and Communication Drive Post-IPO Value

11 hrs ago

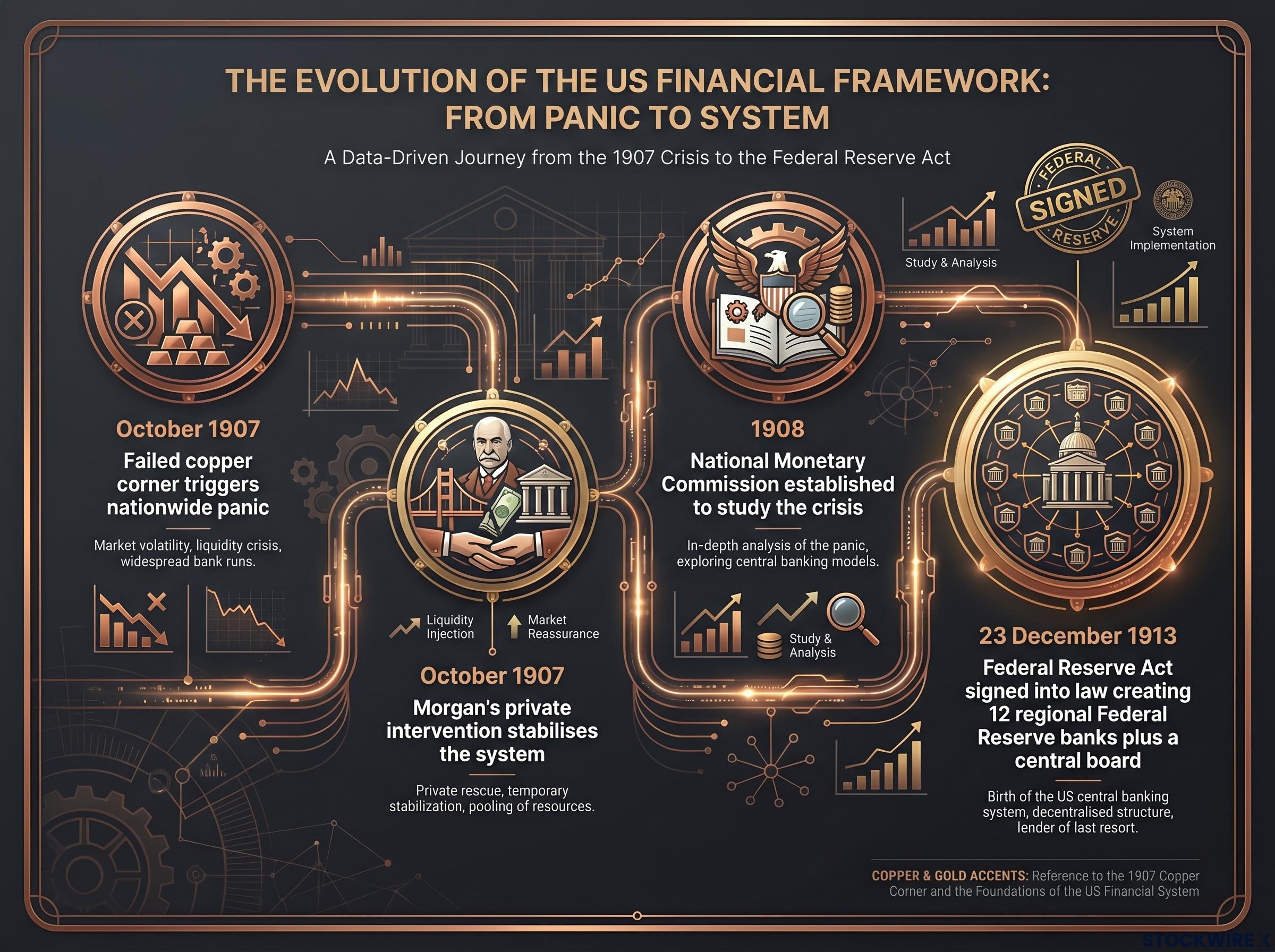

In October 1907, two speculators tried to corner the copper market. They failed. Within days, one of America’s largest trust companies was under siege, loan interest rates had surged beyond 100% annually, and the only thing standing between the United States and financial collapse was one private citizen with a locked door and a list of names.

The Panic of 1907 predates deposit insurance, the Federal Reserve, and securities regulation. It offers a rare, unobstructed view of what a modern-style financial crisis looks like when no institutional backstop exists. Every mechanism that amplified the panic, from opaque institutions and confidence-sensitive funding to information asymmetry and regulatory gaps, still operates in contemporary markets. What follows traces the full causal chain from a failed copper corner to the creation of the Federal Reserve, then extracts specific portfolio lessons that remain applicable today.

The copper corner itself was almost mundane. Two wealthy speculators used large loans from a major trust company to attempt a squeeze on United Copper shares. When the scheme collapsed, the immediate losses were painful but contained. The trade should not have been capable of threatening the financial system.

It became capable because nobody could see inside the institutions that mattered. The Knickerbocker Trust Company, New York’s third-largest trust at the time, was directly implicated in the failed scheme. Depositors had no reliable way to determine how deeply Knickerbocker or its peers were exposed to the losses. They acted rationally on worst-case assumptions: they ran.

The sequence of transmission followed a pattern that has repeated in every major crisis since:

Fear arrived across the country by telegraph and telephone within hours. Credible balance-sheet data did not arrive at all. That information gap, where panic travels faster than facts, is the actual mechanism of contagion.

Confidence-sensitive pricing, where asset values depend on the continued willingness of participants to treat risk as contained, is the common thread between Knickerbocker depositors in 1907 and equity markets that absorb geopolitical supply shocks as routine dips; in both cases, the mechanism that eventually forces repricing is not the arrival of new negative information but the exhaustion of the assumption that someone will intervene before conditions become severe.

At the peak of the crisis, loan interest rates surged beyond 100% annually as national banks hoarded reserves and called loans. Any business attempting to borrow during those days faced borrowing costs that would annihilate a full year’s profit in weeks.

Trust companies were not banks, but they behaved like them. They took deposits, extended credit, and engaged in maturity transformation, borrowing short and lending long. What they did not do was submit to the same rules.

| Attribute | Trust Companies | National Banks |

|---|---|---|

| Reserve requirements | Lower or absent | Mandated by federal charter |

| Regulatory oversight | Minimal; state-level and inconsistent | Federal examination regime |

| Depositor rates | Higher (attracting deposits through yield) | Lower, constrained by reserve costs |

| Public disclosure | Very little; balance sheets largely opaque | Regular public reporting required |

The combination was attractive right up until it was lethal. Trust companies offered higher returns precisely because they carried fewer regulatory costs. Depositors enjoyed the yield without understanding that the missing regulation was the source of the extra return, not managerial brilliance.

Trust companies were not a one-off. They fit a recurring sequence in which financial innovation precedes the regulatory understanding of its risks. The innovation itself is rarely the direct cause of the crisis; the danger arises when institutions, investors, and businesses depend on an untested structure without accounting for stress scenarios.

The pattern spans centuries. The South Sea Bubble of 1720 followed the rapid expansion of joint-stock company speculation. The 1907 panic followed the unchecked growth of trust companies. The 1920s saw leveraged speculation on margin grow faster than supervisory capacity. And 2008 saw shadow banking structures, performing bank-like functions with less oversight, amplify a housing downturn into a global financial crisis.

Between 1875 and 1905, US stock market composition diversified dramatically, adding real estate, utilities, energy, and consumer staples alongside earlier transportation and finance sectors. By 1905, the market broadly resembled the modern economy, with the exception of technology and computing infrastructure. Innovation was real. The risk was invisible until stress revealed it.

With no central bank, no deposit insurance, and no formal mechanism for coordinating a response, the system’s only backstop was J.P. Morgan himself.

The sequence unfolded under extraordinary pressure:

The intervention worked. Morgan’s personal authority, network, and willingness to act prevented a complete financial meltdown. He was, for a few critical days, performing the function that a central bank would later be designed to fill: supplying emergency liquidity and stopping contagion from destroying solvent institutions.

A system that requires a single individual to perform a heroic rescue under extreme time pressure is fragile by design. Robust systems depend on pre-defined rules, institutions, and buffers, not the assumption that the right person will be in the right room at the right moment.

That fragility was the lesson Congress took from 1907. Systemic stability could not depend on private bankers voluntarily organising rescues. The question was what to build instead.

Congress moved first by establishing the National Monetary Commission in 1908, tasking it with studying what had gone wrong in 1907 and how European central banks operated. The Commission’s findings confirmed the structural diagnosis: an advanced industrial economy was relying on ad hoc, private coordination for systemic stability.

The Federal Reserve Act legislative history published by the Federal Reserve itself confirms that the National Monetary Commission’s study of European central bank models was the direct intellectual bridge between the 1907 panic and the December 1913 legislation, underscoring how thoroughly one crisis reshaped American monetary architecture.

What followed was not a swift legislative response. It was six years of political negotiation shaped by two competing fears.

One faction feared concentrating all monetary power in a single New York institution, effectively formalising the dominance of Wall Street banks. The opposing faction recognised that the pre-1907 status quo, in which the nation’s financial stability depended on one man’s willingness to answer the phone, was untenable.

The resulting compromise created 12 regional Federal Reserve banks plus a central board, a structure designed specifically to distribute power while still providing a functioning lender of last resort. The regional architecture was a direct political response to the fear of New York dominance.

The Fed’s core function was to supply emergency liquidity to prevent contagion from destroying solvent institutions, institutionalising what Morgan had improvised by hand. What the Federal Reserve was never designed to do: guarantee risk asset prices, prevent credit or equity losses, or protect entities operating fully outside the banking system’s safety net. That distinction remains relevant whenever investors assume the Fed will act with unlimited speed and scope in a future crisis.

Central bank independence, the principle that monetary policy decisions should track economic data rather than political preferences, was the specific institutional guarantee the Federal Reserve Act was designed to provide; the 1907 crisis made plain that ad hoc private coordination could not substitute for a rules-based lender of last resort, yet the rules themselves only hold if the institution administering them retains the credibility to act without political interference.

The 1907 template does not stay in 1907. It migrates. Each post-crisis regulatory response closes certain gaps while leaving adjacent ones open:

The pattern suggests that future crises are most likely to emerge in areas just beyond the reach of existing backstops, precisely where the most recent round of reforms did not reach.

The structural characteristics of 1907’s trust companies provide a diagnostic checklist for identifying where today’s vulnerabilities may sit:

Private credit markets exhibit several of the structural characteristics that made 1907’s trust companies a transmission mechanism for contagion: rapid growth outpacing regulatory frameworks, opacity in bank-to-non-bank linkages, and funding structures that have not been tested through a severe credit cycle; the global market has grown to approximately US$2.3 trillion, with regulators including the FSB, IMF, and BIS each independently flagging compounding structural concerns.

The central diagnostic question for modern investors: “Where are today’s trust companies, and how much indirect exposure do I have to them?”

One principle from 1907 applies with particular force to yield. Trust companies attracted depositors by offering higher returns than nationally chartered banks. The extra yield was not a reward for cleverness; it was compensation for risks that depositors could not see. When an instrument described as “safe” or “cash-like” offers meaningfully higher returns than insured deposits or Treasury bills, the gap represents hidden liquidity or credit risk, not financial innovation.

Each of these rules corresponds to a specific failure mode visible in 1907. They carry structural force because the mechanisms behind them have not changed.

| Rule | 1907 Mechanism | Modern Application |

|---|---|---|

| High yield signals hidden risk | Trust companies paid more by holding fewer reserves | Scrutinise any “cash-like” product yielding well above insured deposits |

| Size for illiquidity | Knickerbocker depositors discovered opacity only during the run | Position-size opaque funds assuming no exit in a crisis |

| Hold genuinely liquid reserves | Reserves separated survivors from casualties | Maintain a buffer in simple, transparent instruments |

| Avoid forced selling | Solvent institutions failed because they could not survive the liquidity squeeze | Structure obligations so risky assets need not be sold in a downturn |

| Map shared fragilities | Trusts appeared diversified but shared confidence-sensitive funding | Test whether “diversified” holdings depend on the same funding structure |

The overarching principle is the one Morgan demonstrated under pressure: economic solvency, meaning assets likely worth more than liabilities over time, is a different question from liquidity survival, meaning the ability to ride out forced selling without becoming a distressed seller. In 1907, loan interest rates above 100% annually showed how completely short-term funding can vanish once fear takes hold. Portfolios that survive are those built to endure the freeze, not those constructed on the assumption that someone will intervene before conditions become severe enough to matter.

For investors wanting to stress-test the liquidity survival principle against a live modern crisis, our full explainer on safe haven asset failure during the 2026 Iran War supply shock examines why gold, government bonds, and the Japanese yen simultaneously broke down, which asset categories institutional investors moved into as replacements, and how a supply-shock crisis breaks the diversification mechanics that demand-shock crises rely on.

The Panic of 1907 is not primarily a story about copper, Morgan, or even the Federal Reserve. It is a story about what happens when financial innovation consistently outpaces the institutional frameworks designed to contain its failure modes. Opacity plus confidence-sensitive funding plus an information gap plus no lender of last resort equals systemic fragility. At least three of those four conditions are present somewhere in every modern financial system.

The investor’s obligation is practical, not academic: use history as a live risk-mapping tool, ask the diagnostic question about today’s trust companies regularly, and build portfolios that do not require heroic rescues to survive. The copper corner of 1907 reshaped American finance permanently. Its lessons have not expired.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The Panic of 1907 was triggered by a failed attempt to corner the copper market, which exposed speculative losses at the Knickerbocker Trust Company and sparked depositor runs across New York's trust sector, freezing credit markets and pushing short-term loan rates above 100% annually.

J.P. Morgan convened the leaders of major banks at his private library, triaged failing institutions to separate illiquid but solvent firms from genuinely insolvent ones, and organised coordinated emergency liquidity from his peers, effectively performing the function a central bank would later be designed to fill.

Congress established the National Monetary Commission in 1908 to study the crisis and European central bank models, and after six years of political negotiation the Federal Reserve Act was signed into law on 23 December 1913, creating a formal lender of last resort so systemic stability would never again depend on a single private citizen.

The 1907 panic enforces five enduring rules: treat unusually high yields on supposedly safe instruments as a signal of hidden risk, size opaque positions for illiquidity, hold genuinely liquid reserves, avoid structures that force asset sales during downturns, and regularly map whether diversified holdings share the same fragile funding structure.

The article identifies private credit markets, which have grown to approximately US$2.3 trillion globally, as exhibiting the same structural characteristics that made 1907 trust companies dangerous: rapid growth outpacing regulation, opacity in bank-to-non-bank linkages, and short-term confidence-sensitive funding that has never been tested through a severe credit cycle.