What Really Happens to Your Money When an ETF Closes

1 hr ago

Three ASX ETFs hit 52-week highs on the same trading day, and the instinct for most investors is to step back. Vanguard MSCI Index International Shares ETF (VGS), iShares S&P 500 ETF (IVV), and Global X Semiconductor ETF (SEMI) all reached their highest prices in a year simultaneously. That shared milestone raises an obvious question: is it too late to buy? The answer depends far less on where these funds traded last year than on what they hold, what risks they carry, and whether they fit a long-term portfolio. What follows is a breakdown of each ETF’s structural case, the risks at current levels, and a practical framework for thinking about allocation when prices are running hot.

A 52-week high is a backward-looking price comparison. It confirms that a fund’s unit price is higher than at any point in the previous 12 months, and nothing more.

For broad equity index ETFs designed to be held for a decade or longer, setting new highs is the expected outcome of compounding earnings and dividends. It is a sign the engine is working, not a warning light.

“A 52-week high says nothing about whether the underlying earnings and cash flows have grown in line with price.”

The questions that actually matter at any price are different:

Those three filters, not the 52-week marker, determine whether an entry point is defensible.

The ASX is structurally concentrated in financials and resources. For Australian investors whose jobs, property, and superannuation are already tied to the domestic economy, that concentration compounds into a meaningful portfolio gap: limited exposure to global technology, pharmaceuticals, consumer platforms, and industrial conglomerates.

The ASX structural diversification gap is more pronounced than many investors realise: financials and materials together account for over 52% of the ASX 200 by weight, while information technology represents just 3.3%, leaving domestically concentrated investors with almost no organic exposure to the technology and consumer platform sectors that have driven global equity returns over the past decade.

VGS fills that gap in a single trade. The fund tracks the MSCI World ex-Australia Index, holding hundreds of large and mid-cap companies across developed markets. Sectors span technology, healthcare, financials, industrials, consumer goods, and communication services, across multiple countries. Its management fee sits at 0.18% per annum.

None of that changes because the unit price reached an annual high. The mandate, the diversification, and the structural rationale remain intact.

Three risks apply regardless of conviction:

IVV tracks the S&P 500, covering approximately 500 of the largest US-listed companies. Many of those businesses earn substantial revenue globally, across cloud computing, AI, smartphones, digital advertising, healthcare, payments, retail, logistics, and financial services. That global revenue base makes IVV more than a pure US consumer bet.

The S&P 500 has delivered strong long-term real returns over many decades, though past performance does not guarantee future results. For investors with a 10-plus year horizon, buying at elevated prices has historically been more defensible than it feels in the moment.

The concentration trade-off is where IVV diverges from VGS. Mega-cap technology and platform companies now dominate S&P 500 index weightings. A de-rating of that group would hit IVV disproportionately harder than a broader index like VGS.

Mega-cap concentration in passive indices has reached a level that fundamentally changes the risk profile of a cap-weighted S&P 500 fund: five companies, Nvidia, Apple, Microsoft, Amazon, and Alphabet, now control approximately 23% of the broad US market index, a proportion that exceeded the historical 1930s concentration peak as of mid-April 2026.

| Feature | VGS | IVV |

|---|---|---|

| Index tracked | MSCI World ex-Australia | S&P 500 |

| Approx. holdings | Hundreds (multi-country) | ~500 (US-listed) |

| Management fee | 0.18% p.a. | Low-cost (varies by provider) |

| Primary concentration risk | Developed-market valuation stretch | Mega-cap US tech dominance |

These are not interchangeable funds. IVV serves as a US equity core; VGS serves as a broader global diversifier. The decision is whether to use one, both, or layer them deliberately.

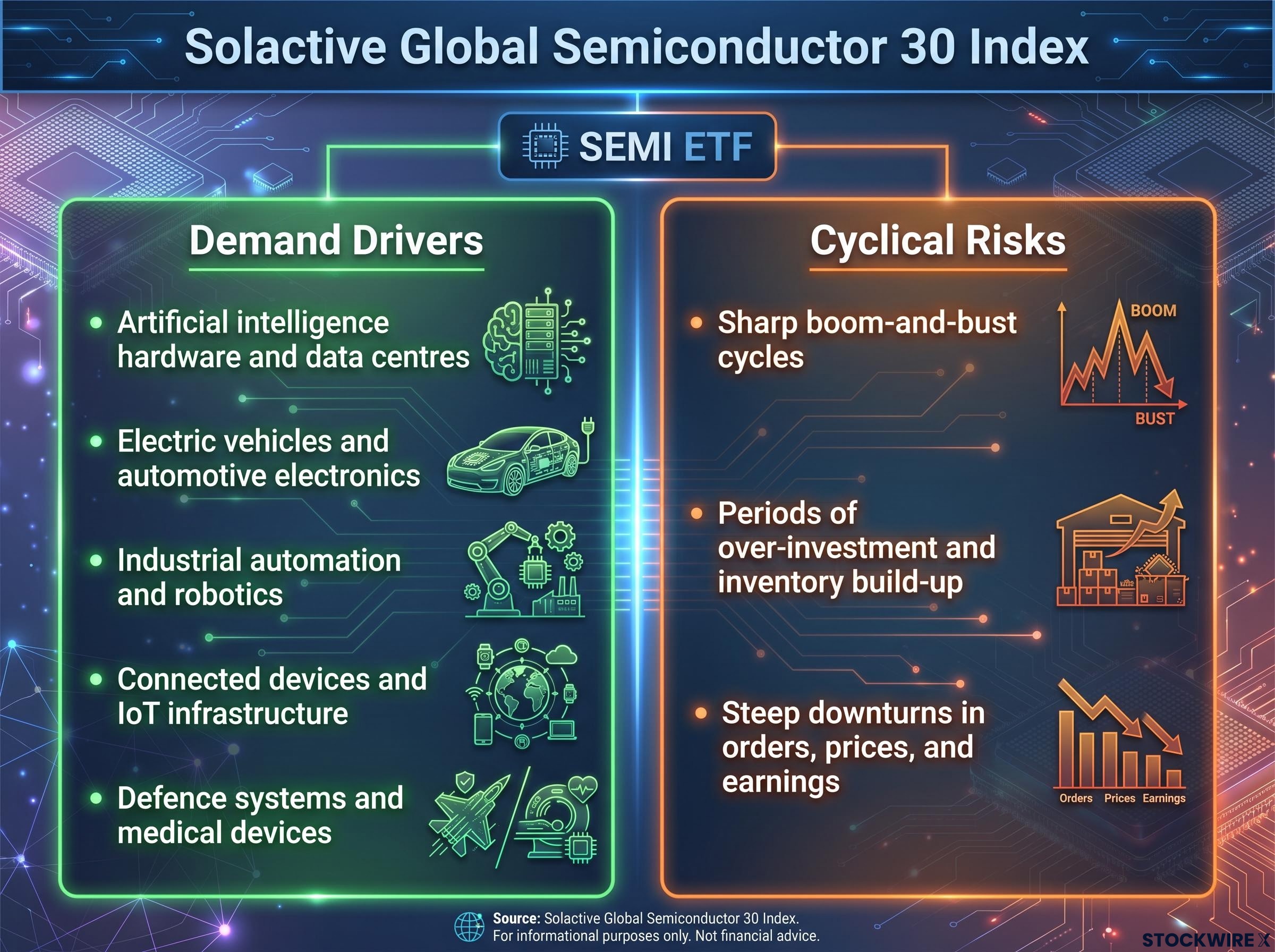

The secular growth story behind semiconductors is straightforward: chips sit at the centre of nearly every structural technology trend shaping the next decade. Demand drivers include:

SEMI tracks the Solactive Global Semiconductor 30 Index, holding chip designers, foundries, and equipment makers. A basket approach reduces single-company risk while maintaining concentrated sector exposure.

The cyclicality risk is where the story shifts. Semiconductor demand, inventory levels, and capital expenditure are historically prone to sharp boom-and-bust cycles. Periods of over-investment and inventory build-up are routinely followed by steep downturns in orders, prices, and earnings.

The capex-to-revenue lag in semiconductor demand is the central structural risk for investors entering the sector at elevated prices: Morningstar analyst Dennis Li has identified an 18-24 month gap between hyperscaler infrastructure commitments and the revenue realisation those commitments ultimately generate, a timing mismatch that has historically coincided with inventory build-up cycles and sharp earnings revisions.

Semiconductors underpin AI hardware, EVs, cloud infrastructure, and connected devices, but the sector is notoriously cyclical, and highs can precede sharp inventory-driven downturns.

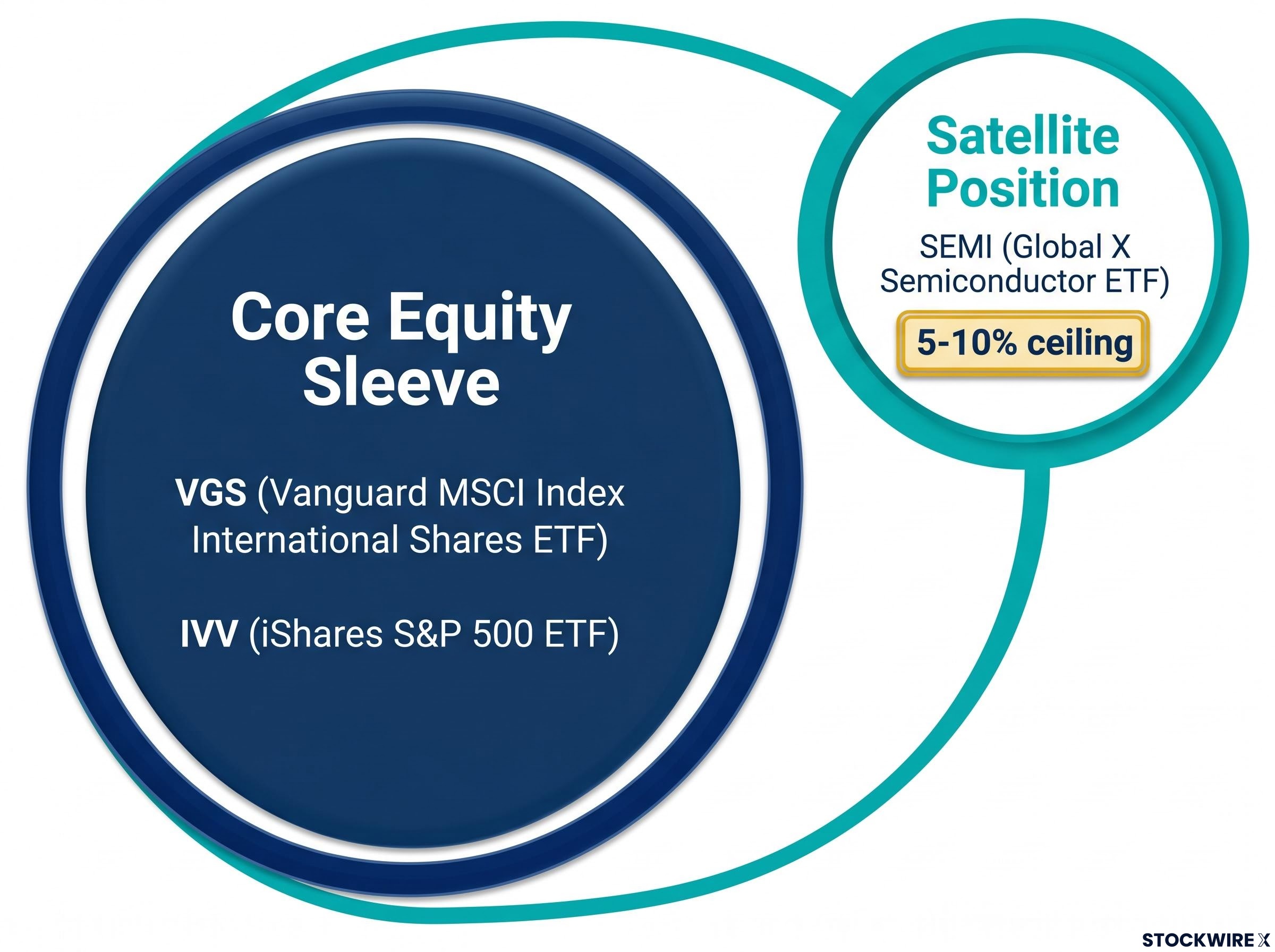

Buying SEMI at a 52-week high amplifies all of this. The fund belongs as a satellite position, not a core holding.

Moving from individual fund evaluation to portfolio-level thinking requires a framework. Four steps help structure the decision:

The core-satellite framework for ASX ETF portfolios formalises exactly this kind of division: a broadly diversified, low-cost core (typically 70-90% of the equity sleeve) anchored by funds like VGS or IVV, with a smaller set of deliberate, thesis-driven positions like SEMI layered on top at a controlled weighting that prevents any single sector’s cycle from derailing the broader plan.

Dollar-cost averaging (splitting a total investment into smaller, regular purchases over time) does not guarantee better returns than investing a lump sum. Research has consistently shown lump-sum investing outperforms on average, because markets tend to rise over time.

Vanguard research on lump-sum versus cost averaging found that lump-sum investing outperformed across approximately two-thirds of historical periods studied, because capital deployed earlier has more time exposed to markets that trend upward over the long run.

The value of dollar-cost averaging lies in behavioural discipline. Spreading purchases over months or quarters reduces the psychological sting of buying just before a pullback. It shifts focus from timing to process, which is its real function for investors uncomfortable with buying at elevated levels.

The 52-week high is not the deciding factor for any of these funds. Allocation fit, time horizon, and risk tolerance are.

ASIC’s exchange traded products guidance outlines the regulatory framework governing ASX-listed ETFs, including the Product Disclosure Statement requirements that investors must review before committing capital to any of the funds discussed here.

Past performance does not guarantee future results. The structural themes driving all three funds are long-term in nature, but markets do correct, and entry at any price carries risk.

This article contains general information only. Investors should read each ETF’s Product Disclosure Statement and consider consulting a licensed financial adviser before investing.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

A 52-week high across three popular ETFs is a natural prompt to audit whether current portfolio allocations still match long-term goals. It is not, on its own, a reason to avoid buying.

The lasting framework is straightforward: broad diversified funds belong in the core, thematic sector funds belong at the margin, and time horizon determines how much valuation risk is tolerable. For investors who can hold through cycles, the structural themes driving VGS, IVV, and SEMI (global earnings growth, US corporate profitability, and semiconductor demand from AI and electrification) are multi-decade in nature.

That is the relevant frame for evaluating today’s prices. Review the allocation, size positions deliberately, and let the process, not the price on any single day, drive the decision.

A 52-week high simply means a fund's unit price is higher than at any point in the previous 12 months. For long-term ETF investors, it is a backward-looking price comparison that says nothing about whether underlying earnings and valuations justify the current price.

VGS tracks the MSCI World ex-Australia Index, providing broad multi-country, multi-sector exposure at a 0.18% management fee, while IVV tracks the S&P 500 and concentrates on approximately 500 large US-listed companies, with higher exposure to mega-cap technology stocks.

SEMI is best treated as a satellite position rather than a core holding, with a position-size cap of around 5-10% of the equity portfolio, given the semiconductor sector's well-documented boom-and-bust cycles and the current capex-to-revenue timing mismatch in AI infrastructure spending.

Research, including Vanguard studies, shows lump-sum investing outperforms in approximately two-thirds of historical periods because capital deployed earlier has more time exposed to rising markets. Dollar-cost averaging is primarily a behavioural discipline tool that reduces the psychological risk of buying just before a pullback.

The core-satellite framework places broadly diversified, low-cost funds like VGS or IVV in the core sleeve (typically 70-90% of the equity allocation), with smaller, thesis-driven thematic positions like SEMI layered on top at a controlled weighting to prevent any single sector cycle from derailing the broader portfolio.