On 9 June 2026, the last trading day for MSII passed without fanfare. The REX MicroStrategy Growth & Income ETF held roughly $3 to $4 million in assets, a figure that never came close to the scale required for a fund to justify its own existence. Its closure was not the product of fraud, regulatory action, or a catastrophic loss. It was arithmetic.

Rex Shares announced the shutdown of MSII and several companion single-stock and covered-call ETFs in late May 2026, joining a steady stream of small fund closures that marks every calendar year in the US ETF industry. For investors encountering a fund liquidation for the first time, the experience can feel unsettling. It should not be.

What follows explains exactly what happens to investor capital when an ETF shuts down, why funds like MSII reach this point, how the tax implications work for US investors, and what income-focused shareholders might weigh as they redeploy proceeds.

Why small ETFs eventually run out of runway

ETF issuers earn revenue through expense ratios charged on assets under management. When AUM is too small, that revenue cannot cover the fixed costs of keeping a registered fund alive.

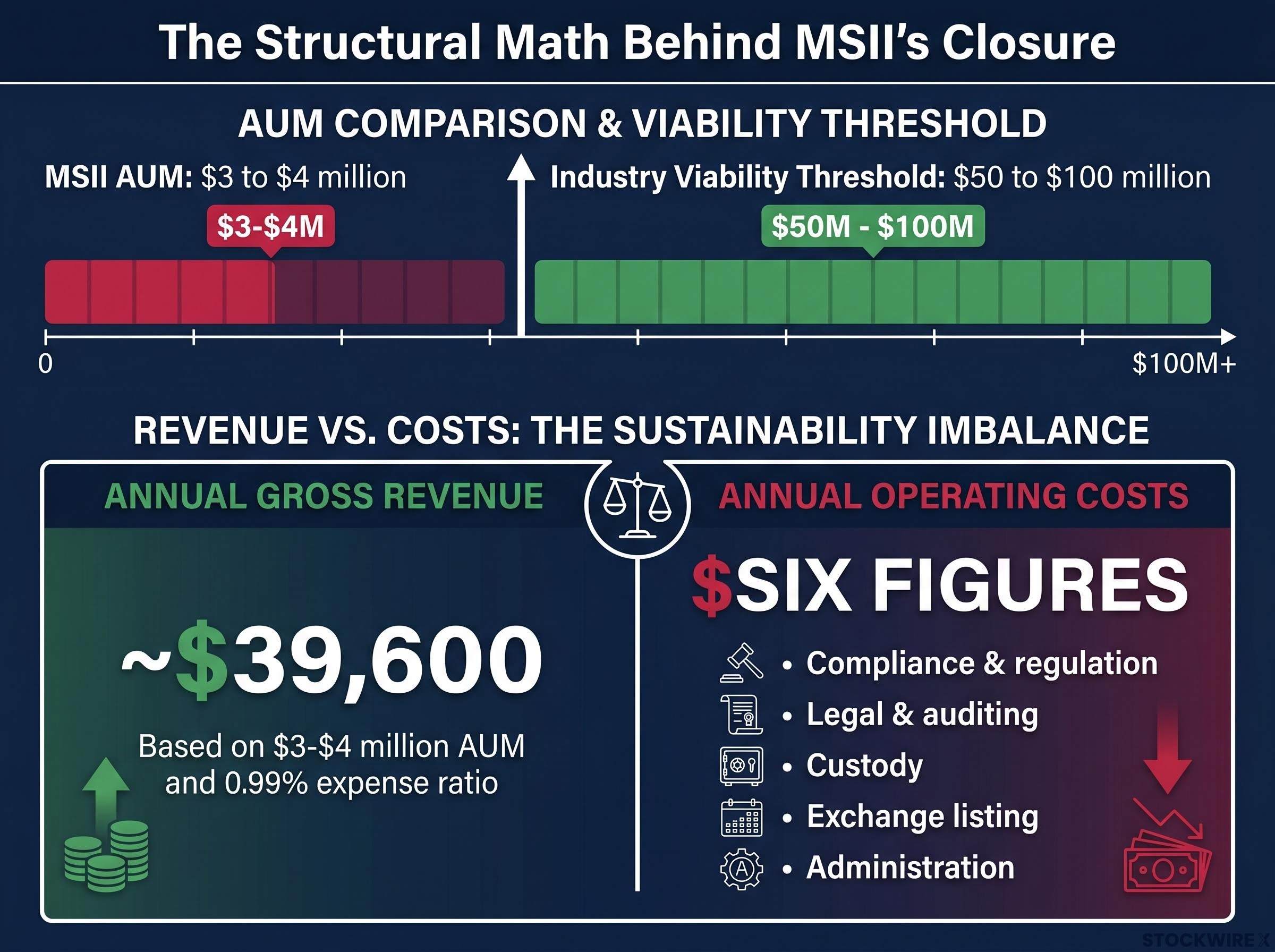

MSII’s numbers make the mismatch visible. At roughly $3 to $4 million in AUM and a 0.99% expense ratio, the fund generated approximately $39,600 per year in gross revenue. Running a US-registered ETF, however, carries fixed annual costs that routinely exceed six figures. Those costs include:

- Compliance and regulation (SEC filings, board governance, ongoing reporting)

- Legal and auditing (independent counsel, annual audit, prospectus updates)

- Custody (safekeeping and settlement of fund assets)

- Exchange listing (fees to the listing exchange)

- Administration (NAV calculation, shareholder servicing, transfer agency)

Approximately $39,600 in annual revenue against six-figure annual operating costs is not a close call. It is a structural loss from day one.

Most industry participants cite a rough viability threshold of $50 to $100 million in AUM for a typical ETF to sustain itself, with complex or actively managed single-stock strategies often requiring even greater scale. 2025 saw record active ETF closures, and the overwhelming majority of funds shuttered held AUM below $25 million.

MSII did not fail. It simply never gathered enough capital for its economics to work.

When big ASX news breaks, our subscribers know first

The step-by-step mechanics of what actually happens to your money

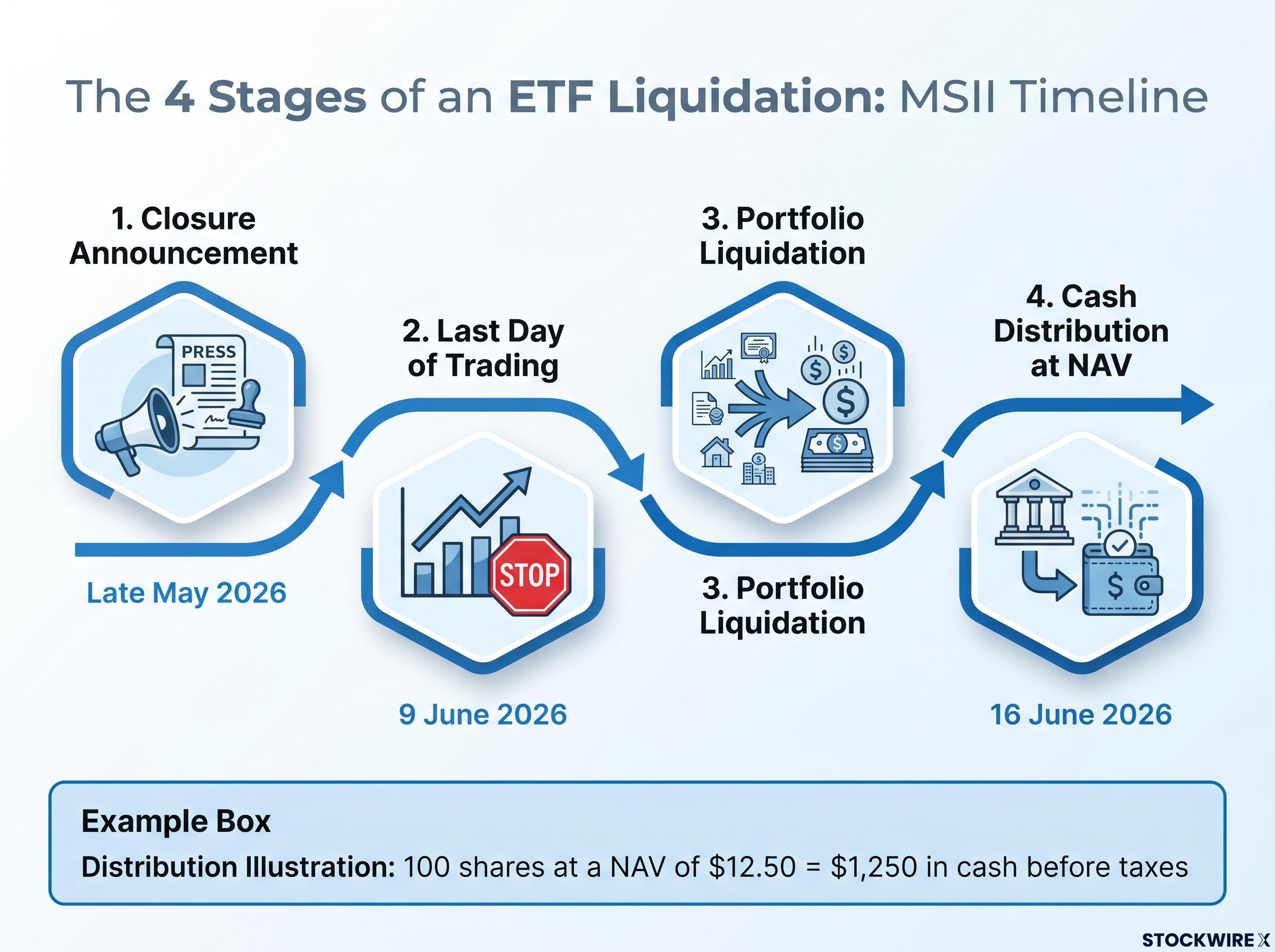

An ETF is a separate legal entity that owns the underlying assets. When that entity winds down, remaining shareholders receive a cash distribution based on the fund’s net asset value per share, not a distressed sale price. The process follows four distinct stages.

The ETF legal structure matters here: each fund is a registered investment company that holds assets separately from the issuer, which is precisely why a business decision to wind down a fund does not mean investor capital is at risk from issuer insolvency.

The SEC investor guidance on ETF closures confirms that shareholders are entitled to receive their pro-rata share of the fund’s net assets, and that issuers must provide advance notice through prospectus supplements and other official communications before a liquidation date is reached.

- Closure announcement: The issuer announces a planned liquidation date and last day of trading, typically weeks in advance. Notifications arrive via press release, fund website, brokerage notices, and prospectus supplements. Trading continues normally during this window, though volume often declines as the date approaches.

- Last day of trading: On this date, the ETF is delisted from the exchange. After delisting, shares can no longer be bought or sold on the secondary market.

- Portfolio liquidation: The fund’s portfolio manager sells the remaining holdings and converts them to cash. This process typically takes a few days, depending on the liquidity and complexity of the positions.

- Cash distribution at NAV: Remaining shareholders as of the liquidation record date receive a cash payout based on NAV per share. Proceeds are credited directly to the brokerage account, similar to stock sale proceeds.

As an illustration: an investor holding 100 shares at a NAV of $12.50 would receive $1,250 in cash before taxes.

MSII’s specific closure timeline

For MSII, the key dates are straightforward. The closure was announced in late May 2026. The last day of trading was 9 June 2026 at close of business. Final liquidation is set for after close of business on 16 June 2026.

Investors should monitor the official Rex Shares press release, brokerage corporate actions notices, and the fund’s prospectus supplement for any issuer-specific nuances around the final distribution.

What ETF closure means on your tax return

For investors who have never held a fund through liquidation, the tax treatment can arrive as a surprise. In a taxable brokerage account, an ETF liquidation is treated as a sale for US tax purposes. The consequences depend on the relationship between the liquidation NAV and the investor’s cost basis.

Three scenarios apply:

- NAV exceeds cost basis: The investor realises a capital gain. The holding period determines whether it is taxed as short-term or long-term.

- NAV falls below cost basis: The investor realises a capital loss, which may offset other gains or reduce taxable income up to annual limits.

- Final capital gains distribution: Separately from the liquidation cash, the fund may issue a final capital gains distribution arising from gains realised as the portfolio was wound down. Leveraged and derivatives-heavy funds like MSII are particularly likely to generate this additional distribution.

The taxable event occurs in the year of liquidation, which for MSII means the 2026 tax year.

In tax-advantaged accounts (IRAs, 401(k)s, and similar vehicles), the closure itself typically does not create an immediate tax bill. Those accounts are tax-deferred or tax-free depending on account type, so the liquidation proceeds simply become uninvested cash within the account.

Before deciding whether to sell early or hold to liquidation, investors in taxable accounts may benefit from reviewing the potential tax impact of each option with a qualified professional.

Sell before June 9 or hold to liquidation? How to decide

MSII shareholders faced a binary choice before the 9 June 2026 trading halt: sell on the secondary market or hold through liquidation and receive NAV in cash. Both options carry legitimate trade-offs.

| Decision Factor | Sell Before Last Trading Day | Hold to Liquidation |

|---|---|---|

| Timing control | Full control over execution price and timing | No control; proceeds arrive on the liquidation schedule |

| Tax year management | Flexibility to realise gains or losses in a chosen tax year | Taxable event locked to the liquidation year (2026) |

| Spread and liquidity risk | Risk of wide bid/ask spreads on a thinly traded closing fund | Payout based on NAV, avoiding intraday spread costs |

| Simplicity | Requires active order placement and price monitoring | Automatic exit; no action required after the trading halt |

The risk with the clearest right answer sits on the sell-early side. MSII had only 540,000 shares outstanding, indicating a narrow secondary market. Selling into a poorly priced market order on a thinly traded closing ETF can cost real money relative to waiting for the NAV distribution. Panic-selling at a discount to NAV is the most common and most avoidable mistake investors make during an ETF closure.

For shareholders who missed the 9 June deadline, the decision has already been made. Liquidation proceeds based on NAV are expected after close of business on 16 June 2026.

Why single-stock ETFs are structurally prone to closure

MSII’s shutdown is not an isolated event. It reflects a pattern that runs through the single-stock ETF space.

These products are niche by design. They attract a specialised subset of investors, and when multiple issuers launch competing strategies on the same underlying stock, assets fragment. No single fund may reach the AUM needed for viability. Rex Shares is simultaneously closing funds tied to Palantir (PLTI), Eli Lilly (LLII), Coinbase (COII), and Robinhood, alongside MSII. It is retaining its Tesla and Nvidia focused products, which have gathered enough assets to remain economically viable.

That triage decision follows AUM, not asset quality.

- Funds closing: MSII, LLII, COII, PLTI, and Rex’s all-in-one universal covered call ETF

- Funds retained: Tesla and Nvidia single-stock covered-call products

Leveraged, inverse, and highly specialised ETFs are structurally more likely to close than large broad-index funds. Many shut down within their first few years if they never gain traction.

MSTY versus MSII: why one survived and the other did not

The MicroStrategy income ETF space offers a clean comparison. MSTY (YieldMax MSTR Option Income Strategy ETF) holds approximately $1.29 billion in AUM and remains open. MSII held $3 to $4 million and is closing. Strategy type alone did not determine the outcome; scale did.

Performance context reinforces the gap. In a flat to declining MSTR price environment, MSTY’s covered-call strategy (without traditional leverage) generated positive returns through option premium income. MSII’s hybrid leveraged covered-call structure added drag through the same period, making it less appealing to income-focused allocators. The result was a self-reinforcing cycle: weaker performance led to lower inflows, which kept AUM below viability, which made closure inevitable.

Investors who use niche or single-stock ETFs should recognise that viability risk is part of the product risk. Understanding it before buying is as important as understanding the underlying strategy itself.

What US income investors might consider after the MSII liquidation

Investors receiving MSII liquidation proceeds on or around 16 June 2026 face an immediate reinvestment decision. The following categories provide educational context, not personalised investment advice. Current prospectuses, holdings, and distribution histories should be reviewed before acting.

| Alternative Category | Primary Appeal | Primary Trade-off |

|---|---|---|

| MSTR-focused covered-call ETFs (e.g., MSTY) | Option income tied to MSTR without traditional leverage; approx. $1.29B AUM | Single-stock concentration risk; capped upside above call strike |

| Other single-stock income funds (e.g., Rex Tesla/Nvidia products) | High distribution potential from volatility of individual names | Significant idiosyncratic risk; generally suited only as small satellite positions |

| Broad-index covered-call ETFs (e.g., XYLD, QYLD) | Diversified exposure with income from writing calls on S&P 500 or Nasdaq-100 | Lower yield than single-stock strategies; still trades upside for premium |

| Actively managed option-income ETFs | Dynamic call-writing across diversified equity portfolios; flexible risk management | Higher fees; manager skill dependency; less transparent positioning |

| Short-term cash instruments (T-bills, money market funds) | Capital preservation while reassessing income goals and risk tolerance | Lower yield; does not maintain equity market exposure |

Parking liquidation proceeds in cash or short-term Treasuries while reassessing income goals is a rational and underrated response to an involuntary closure. There is no obligation to redeploy immediately.

Income portfolio construction choices made after an involuntary liquidation often reflect habit rather than deliberate strategy; investors who previously held a single-stock covered-call fund for yield may find that a blended approach combining dividend-growth equity and diversified option-income vehicles produces a more durable income stream at comparable yield levels.

Each alternative carries its own risk profile. The decision should reflect the investor’s income needs, risk tolerance, and whether single-stock exposure still fits within the broader portfolio.

ETF closure is a business event, not a crisis: what to take away

ETF closures are a normal, recurring feature of the fund industry. Dozens of US ETFs shut down every year, driven by AUM economics rather than fund failure or investor harm. Shareholders receive the underlying asset value in cash, provided they hold through the record date.

Two actions matter most for any investor in a closing fund. First, monitor official communications carefully: issuer press releases, broker corporate actions notices, and the fund’s prospectus supplement. Second, make a deliberate choice between selling early and holding to NAV distribution rather than reacting emotionally to the closure announcement.

For investors who use niche or single-stock strategies, the broader lesson is straightforward. Viability risk is part of the product risk. A fund that never gathers sufficient AUM will eventually close, regardless of how compelling its underlying strategy appears. Evaluating that risk before committing capital is as important as evaluating the strategy itself.

For investors wanting a systematic process for evaluating ETF viability before buying, our dedicated guide to ETF due diligence covers how to assess AUM thresholds, total cost of ownership beyond the headline expense ratio, and the structural red flags that often precede a fund closure.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.