At a 10-year Treasury yield of roughly 4.48%, the average American homebuyer in mid-2026 is paying approximately $2,542 per month in principal and interest on a $400,000 mortgage. A number reported on a bond market screen is determining whether families can afford a home.

Many buyers instinctively watch Federal Reserve announcements when tracking mortgage rates, but the Fed does not set the number that appears on a lender’s rate sheet. A separate, less-watched figure does. Understanding which number to track, and why, gives buyers a meaningful edge in timing decisions.

What follows explains exactly how the 10-year Treasury yield connects to the mortgage rate a lender quotes, what mid-2026 rates mean in concrete dollar terms, and how the current shape of the yield curve frames what buyers can realistically expect next.

The two numbers behind every mortgage rate quote

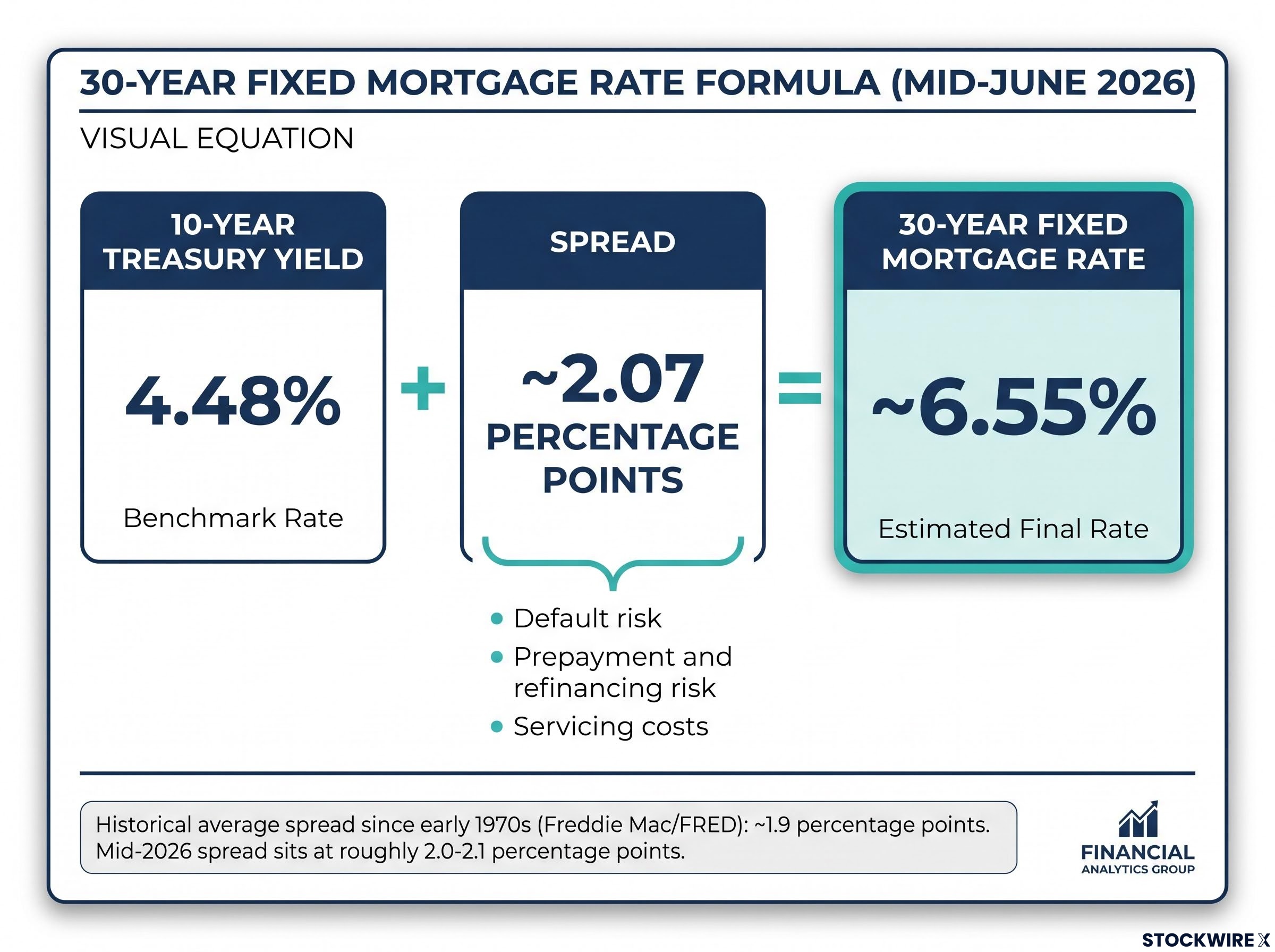

Every 30-year fixed mortgage rate has two parts. The first is a baseline: the yield on the 10-year U.S. Treasury note. The second is a spread, typically 1.8-2.2 percentage points, that lenders add on top. Together, they produce the rate on a borrower’s quote sheet.

The core formula: 30-year fixed mortgage rate ≈ 10-year Treasury yield + roughly 1.8-2.2 percentage points.

Historical data from Freddie Mac and FRED show the average spread has been approximately 1.9 percentage points since the early 1970s, though it has recently widened to around 2.2 percentage points. In mid-June 2026, the formula is visible in real time: a 4.48% ten-year yield plus roughly 2.07 percentage points of spread produces a national average 30-year fixed rate of approximately 6.55%.

FRED historical mortgage-Treasury spread data, which tracks the relationship between the 30-year fixed mortgage average and the 10-year Treasury yield back to the early 1960s, shows the current spread of approximately 2.0-2.1 percentage points sits close to the long-run historical average, reflecting a market environment without acute stress premiums.

The spread exists because fixed-rate mortgages are bundled into mortgage-backed securities (MBS), which are bonds backed by pools of home loans, and sold to investors. Those investors compare MBS yields against Treasuries, the benchmark for risk-free returns. The additional spread compensates them for the risks that mortgages carry and Treasuries do not: the chance a borrower defaults, the risk of early repayment, and the cost of servicing the loan.

The inverse relationship at the heart of bond price and yield mechanics explains why a 10-year Treasury selling off in the secondary market, meaning its price is falling, simultaneously produces a higher yield number on the rate screen that lenders use to price mortgages.

Why the Federal Reserve is the wrong number to watch

The federal funds rate, the rate the Fed directly controls, is an overnight lending rate between banks. It influences long-term yields only indirectly, through market expectations about future inflation, economic growth, and the Fed’s own future decisions.

Fannie Mae research has found that movements in the 10-year Treasury have a larger, more direct impact on mortgage rates than changes in the fed funds rate itself. This is observable on any trading day: mortgage rates frequently move when the Fed has not met or acted, because bond investors are independently repricing the 10-year yield based on new economic data.

The number to watch is on the bond screen, not the Fed podium.

Beyond their direct effect on mortgage pricing, Treasury yields as a policy lever have taken on a broader role in 2026, with multiple institutional analysts concluding that bond market stress, not equity selloffs, now exerts more immediate pressure on White House economic decision-making than stock index movements do.

When big ASX news breaks, our subscribers know first

What the Treasury-mortgage connection actually means in dollars

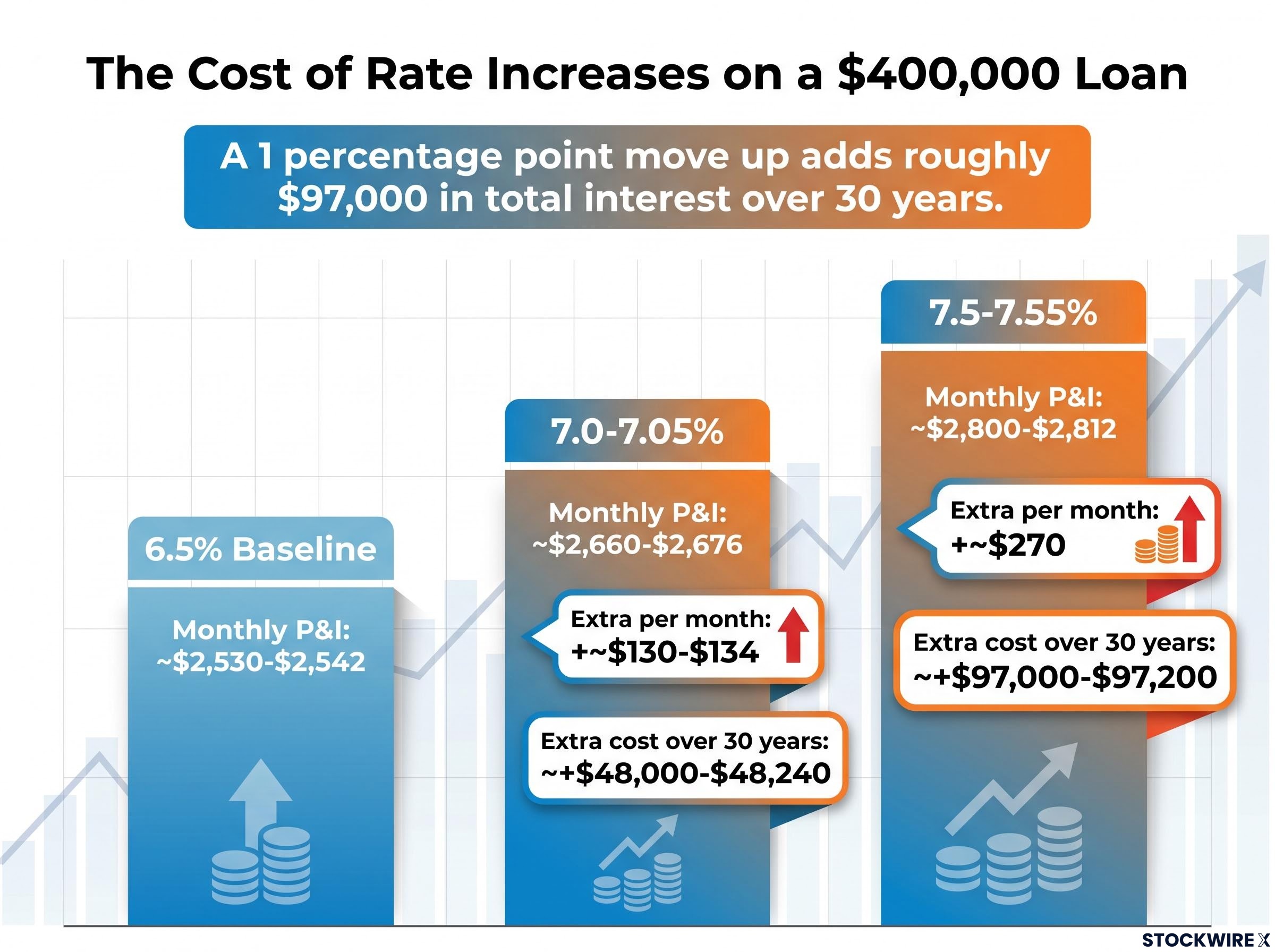

At 6.55% on a $400,000 loan, the monthly principal and interest payment comes to approximately $2,542. Over 30 years, that borrower pays roughly $915,000 in total, of which approximately $510,000 is interest alone. The majority of what a homebuyer pays over three decades is not the house; it is the cost of borrowing.

That proportion is what makes rate sensitivity so consequential. A 0.5 percentage point increase in the mortgage rate, the kind of move that can occur in a matter of weeks when the 10-year yield shifts, adds roughly $130-$134 per month. Over the full loan term, that translates to approximately $48,000 in additional interest.

A full 1.0 percentage point increase doubles the impact.

| Mortgage Rate | Approx. Monthly P&I | Extra per Month vs 6.5% | Extra Cost Over 30 Years |

|---|---|---|---|

| 6.5% (baseline) | ~$2,530-$2,542 | Baseline | Baseline |

| 7.0-7.05% | ~$2,660-$2,676 | +~$130-$134 | ~+$48,000-$48,240 |

| 7.5-7.55% | ~$2,800-$2,812 | +~$270 | ~+$97,000-$97,200 |

All figures are principal and interest only. Property taxes, homeowner’s insurance, HOA dues, and mortgage insurance are additional.

A 1 percentage point move up in the mortgage rate on a $400,000 loan adds roughly $97,000 in total interest over 30 years.

How the 10-year yield is tracked (and why the spread sometimes widens)

The spread between the 10-year Treasury and the mortgage rate is not a fixed fee. It compensates investors for three distinct risks:

- Default risk: The possibility that a borrower loses income and cannot make payments, resulting in a loss for the MBS investor.

- Prepayment and refinancing risk: The chance that borrowers repay their loans early, typically by refinancing when rates drop, returning capital to the investor at precisely the moment when reinvestment yields are lower.

- Servicing costs: The administrative expenses of collecting payments, managing escrow accounts, and handling delinquencies on behalf of investors.

Of these three, prepayment risk is the most volatile. It fluctuates with interest rate expectations and is the primary reason spreads widen and compress over time.

Richmond Fed research on mortgage spreads confirms that changes in expected mortgage duration, driven by yield curve shape and refinancing expectations, are the dominant force behind spread widening and compression, explaining why MBS investors demand higher yield premiums precisely when economic uncertainty is highest.

Historically, the spread has averaged approximately 1.9 percentage points. In mid-2026, it sits at roughly 2.0-2.1 percentage points, close to normal levels.

When the spread widens and mortgage rates lag Treasury moves

During periods of economic stress or yield curve inversion (when short-term Treasury yields rise above long-term yields), prepayment assumptions shift sharply. Investors expect shorter mortgage durations because borrowers in a falling-rate environment are likely to refinance sooner. That uncertainty forces MBS investors to demand a higher yield premium, pushing the spread wider.

Richmond Fed research confirms this pattern: yield curve inversions tend to spike the spread between 30-year mortgage rates and the 10-year Treasury. The result is a situation many buyers find frustrating. Bond yields may be falling, yet mortgage rates barely budge or even stay elevated.

A normalising, upward-sloping yield curve, such as the one present in mid-2026, tends to keep spreads closer to their historical average. That benefits buyers relative to a stressed environment, because more of any decline in the 10-year yield actually flows through to the mortgage quote.

Where mid-2026 mortgage rates sit in historical perspective

In January 2021, the 30-year fixed mortgage rate touched approximately 2.65%, the lowest on record. On a $400,000 loan, that produced a monthly payment of roughly $1,611. By October 2023, the same rate had climbed to approximately 7.79%, pushing the monthly payment to roughly $2,878.

The gap between those two eras: approximately $1,267 more per month at the 2023 peak versus the 2021 low, amounting to an estimated $455,349 in additional cost over the full 30-year term.

| Time Period | 30-Year Fixed Rate | Monthly P&I on $400,000 | Context |

|---|---|---|---|

| January 2021 | ~2.65% | ~$1,611 | All-time low, pandemic-era monetary policy |

| October 2023 | ~7.79% | ~$2,878 | Highest in decades, aggressive Fed tightening cycle |

| Mid-June 2026 | ~6.55% | ~$2,542 | Below 2023 peak, closer to long-run norms |

Mid-2026’s rate sits meaningfully below that 2023 peak, yet far above the 2021 lows. Across several decades, 30-year fixed mortgages have more often lived in the 6-8% range than below it.

The 30-year Treasury briefly tested Treasury yield levels last seen before 2008 during the May 2026 spike, a move that pushed MBS spreads temporarily wider and illustrated precisely how rapidly the 10-year-to-mortgage-rate formula can shift when bond markets are repricing duration risk under fiscal and inflation pressure.

Sub-3% rates were the outlier. Mid-6% rates are closer to the historical norm.

The 2020-2021 experience, shaped by extraordinary pandemic-era monetary policy and near-zero short-term rates, was not a baseline. It was an anomaly driven by conditions that would require severe economic deterioration to replicate. Buyers whose frame of reference starts in 2020 are comparing today’s rates against the most unusual period in modern mortgage history.

What the yield curve’s current shape signals for buyers

The yield curve is a chart that plots Treasury yields from the shortest maturities (such as 3-month bills) out to the longest (30-year bonds). Its shape tells investors what the bond market collectively expects about economic growth, inflation, and future interest rates.

In a healthy economy, the curve slopes upward: longer-term yields sit above shorter-term yields, reflecting the additional compensation investors require for locking up capital over longer time horizons. When the curve inverts, with short-term yields rising above long-term yields, bond markets are signalling expectations of weaker growth and future Fed rate cuts.

As of mid-June 2026, the yield curve is in a normal, upward-sloping configuration:

| Maturity | Approximate Yield |

|---|---|

| 3-month | ~3.71% |

| 2-year | ~4.09% |

| 10-year | ~4.48% |

| 30-year | ~5.0% |

Research from the Federal Reserve Bank of San Francisco found that all 10 U.S. recessions since 1955 were preceded by a yield curve inversion, a perfect record across roughly 70 years. The current curve is not inverted.

What a normal yield curve means for rate expectations

A normal, upward-sloping curve means bond markets are not pricing in imminent aggressive Fed rate cuts. Without a severe deterioration in economic conditions, a rapid return to 4-5% mortgage rates is unlikely in the near term.

The current spread of approximately 2.0-2.1 percentage points above the 10-year also suggests no acute stress premium is embedded in mortgage rates. The implication for buyers: rates may drift modestly in either direction, but a sharp collapse, the kind that would bring mid-6% mortgages back toward pandemic-era levels, would require an economic downturn the curve is not currently signalling.

A practical decision framework for mid-2026 buyers and refinancers

All of the mechanics above distil into a set of concrete questions a buyer can work through before making a timing decision.

- What does the 10-year yield imply the mortgage rate will be today? Take the current 10-year Treasury yield and add approximately 2 percentage points. That gives a working estimate of the prevailing 30-year fixed rate, often before lenders update their rate sheets.

- How much would a 0.5 or 1.0 point drop actually save per month? On a $400,000 loan, a 1.0 percentage point reduction saves approximately $270 per month. A 0.5 point drop saves roughly $130-$134.

- How many months of savings does it take to recover refinancing costs if buying now and refinancing later? Refinances typically cost 2-3% of the loan amount in closing costs. On a $400,000 loan, that equals $8,000-$12,000 upfront. At $270 per month in savings from a full percentage point reduction, the break-even point is approximately 30-44 months.

Any savings from a lower future rate must also be weighed against potential home price appreciation during the waiting period. Prices do not pause while buyers wait for yields to move.

The broader housing market conditions in early 2026, including a 17.6% January decline in new single-family home sales and 9.7 months of supply, provide the demand-side context behind why affordability at mid-6% rates is compressing buyer activity even as the economy as a whole has remained relatively insulated from the housing slowdown.

Waiting for a return to 3-4% mortgage rates would require the kind of severe economic downturn the current yield curve is not signalling.

Mid-2026’s mid-6% rates are within the historically normal range. The arithmetic is available. The question is whether the numbers work for a specific household, not whether a different rate era might return.

The bottom line on Treasury yields and what mid-2026 buyers should do next

The relationship between the Treasury market and a lender’s rate sheet is mechanical, not mysterious. Three points carry the weight of the analysis:

- The formula: The 30-year fixed mortgage rate tracks the 10-year Treasury yield plus approximately 2 percentage points. Watching the 10-year daily gives buyers a head start on rate moves before lender announcements reflect them.

- The historical context: Mid-2026’s mid-6% rates are closer to several decades of normal than to crisis. Sub-3% was the anomaly.

- The yield curve signal: A normal, upward-sloping curve in mid-June 2026 suggests gradual rather than dramatic rate movement ahead, with no imminent recession signal embedded in the bond market.

The dollar impact table in this article provides a starting framework. For figures specific to a particular loan amount, credit profile, and loan structure, a licensed mortgage professional can provide precise calculations.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.