One ETF is a start. A portfolio is a strategy. Most Australian investors reach a point where a single diversified fund no longer matches their ambitions, but adding more holdings without a framework risks turning a portfolio into a collection of overlapping bets. The core satellite portfolio approach solves that problem. With more than 400 ETFs now available on the ASX and 20% of Australian investors holding ETFs (up from 15% in 2020, according to the ASX Australian Investor Study 2023), the options for portfolio construction have never been broader. More choice without structure, however, leads to overcrowded, emotionally reactive portfolios. This guide explains how the core-satellite framework works, how to size each component for the Australian context, what types of investments belong where, and how to avoid the most common mistakes that quietly undermine the approach.

What the core-satellite framework actually means

The framework divides a portfolio into two structurally distinct components, each with a different objective and a different management style. The core is a stable, broadly diversified foundation designed for long-term compounding. The satellites are a smaller set of higher-conviction or thematic positions that complement the core without replacing it.

Gemma Mitchell of Rask has described this approach as separating “probability from possibility.” The core captures the broad market’s long-term probability of growth. The satellites express a specific view about where additional opportunity may exist.

Even a single ETF constitutes a portfolio. A framework is not about adding complexity for its own sake; it is about imposing discipline on how holdings relate to each other and to the investor’s goals.

ETF portfolio structure decisions, particularly the proportional split between growth and defensive assets, have a larger effect on long-term outcomes than the specific funds chosen within each category, which is why the core-satellite framework prioritises getting the allocation right before optimising for individual holdings.

The core: your stable return engine

The core is broadly diversified, low-cost, and largely hands-off. It functions similarly to how superannuation funds operate: select it based on risk profile, automate contributions where possible, and leave it to compound across market cycles. Its purpose is reliable long-term returns, not outperformance in any single theme or sector.

The satellite: deliberate, thesis-driven exposure

Satellites are niche, thematic, or higher-conviction positions layered around the core. They might target a specific sector, a geographic tilt, or an individual company. Investors may already hold indirect exposure to certain themes through their core ETFs; satellites allow a deliberate additional allocation to those areas.

A satellite component is entirely optional. Experienced, long-term investors may maintain only a core portfolio throughout their investing life, and that is a perfectly valid approach.

- Core characteristics: Broad diversification, low fees, long time horizon, minimal trading, set-and-review approach

- Satellite characteristics: Narrower focus, thesis-driven, defined time horizon, actively monitored, opportunity-responsive

When big ASX news breaks, our subscribers know first

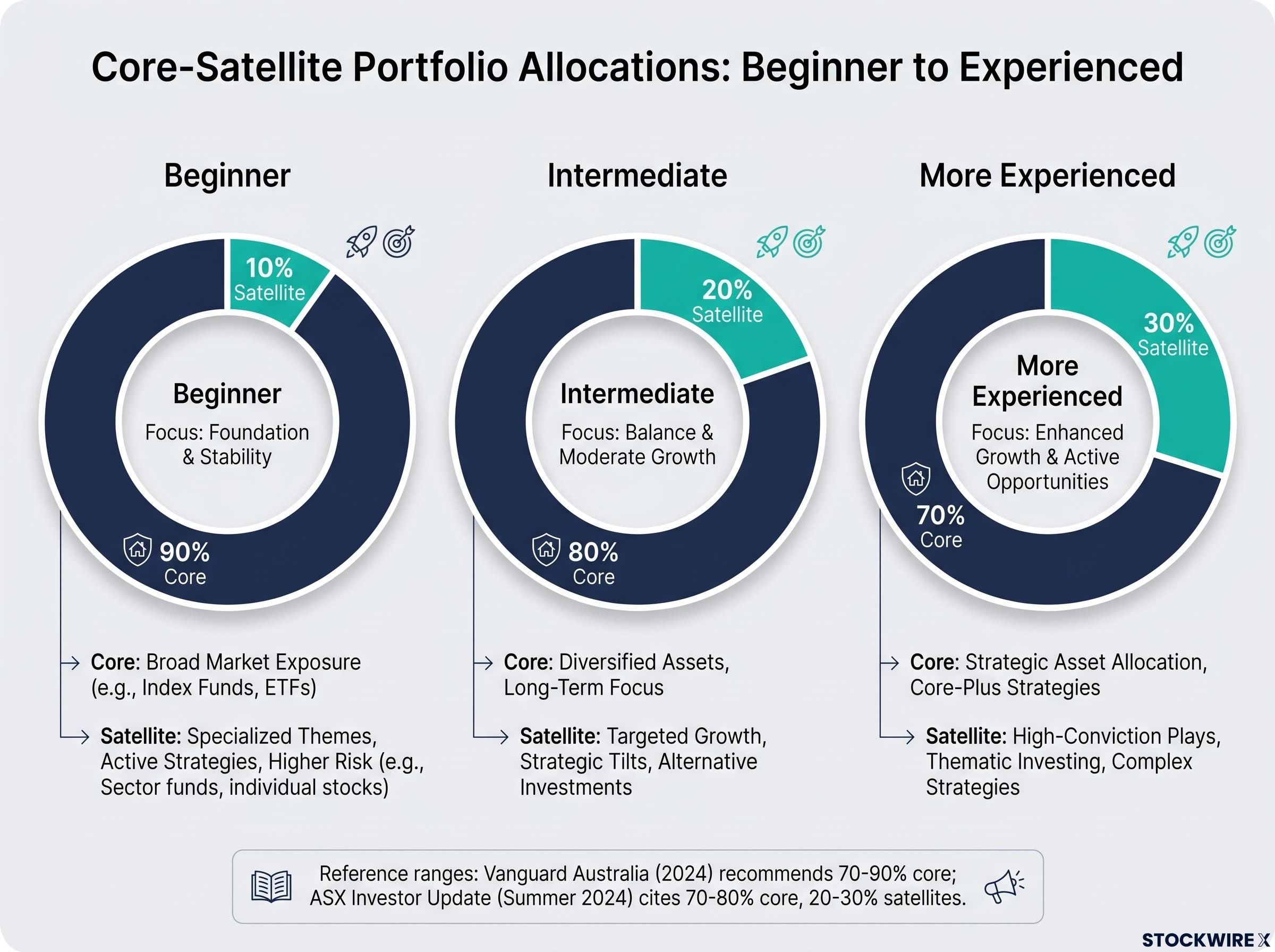

How to split your portfolio: choosing the right core-to-satellite ratio

The guidance from Australian sources is consistent: keep the core dominant. The appropriate range sits between 70-90% in the core and 10-30% in satellites, depending on investor experience, risk tolerance, and the nature of the satellite positions.

Vanguard Australia’s “Principles for Portfolio Construction” (updated 2024) describes core allocations of 70-90% as consistent with long-term, goal-based investing.

The ASX Investor Update (Summer 2024) cites a typical split of 70-80% core and 20-30% satellites for most retail investors. Stockspot’s Australian ETF Report 2024 reinforces that satellite positions are sensibly kept under 20-30% for many people.

Where an investor sits within that range depends on their circumstances. A community investor example (Alex, not a financial adviser) cited a satellite allocation of approximately 30%, divided roughly equally across small-cap active funds, thematic ETFs, and individual stocks at around 10% each. That example is illustrative, not a recommendation.

| Investor profile | Core allocation | Satellite allocation |

|---|---|---|

| Beginner (building confidence and knowledge) | 90% | 10% |

| Intermediate (comfortable with ETF selection) | 80% | 20% |

| More experienced (clear satellite theses, active monitoring) | 70% | 30% |

A miscalibrated ratio is the most common structural error in core-satellite portfolios. Getting this sizing decision right upfront prevents the satellite tail from wagging the core dog during volatile periods.

Building the core: what belongs in your stable foundation

The core should be low-cost, broadly diversified, and appropriate to the investor’s risk profile. Recent performance or thematic excitement is not the selection criterion. Reliable compounding is.

Four categories of core building blocks are consistently cited across Australian guidance:

- Broad Australian equity ETFs for domestic market exposure

- Broad international equity ETFs for global diversification

- Diversified multi-asset ETFs (the “one-ticket core”) for investors who want a single holding to serve as the entire core

- Defensive fixed income or cash ETFs for risk management within the core

For beginners, the one-ticket core option is a practical starting point. A diversified multi-asset ETF such as VDHG or VDBA already blends Australian equities, international equities, and bonds into a single holding. Satellites can be introduced later once the investor is comfortable with the framework.

| Core category | Role in portfolio | ASX ETF examples | Characteristic |

|---|---|---|---|

| Broad Australian equity | Domestic market exposure and franked dividends | VAS, IOZ, STW | Low-cost, market-cap-weighted, highly liquid |

| Broad international equity | Global diversification across developed markets | VGS, IWLD | Exposure to thousands of companies across multiple regions |

| Diversified multi-asset | All-in-one core for simplicity | VDHG, VDBA | Pre-built blend of equities and bonds; auto-rebalanced |

| Defensive fixed income | Stability and income within the core | VAF, IAF | Lower volatility, acts as ballast during equity drawdowns |

These examples illustrate the principle of simplicity, diversification, and low cost. They do not constitute personal financial advice.

Building the satellite: how to add conviction without creating chaos

Every satellite position should be an answer to a specific question: what thesis does this express, why does the core not already capture it, and over what time horizon does the thesis need to play out? Without those answers, a satellite is a reaction to a headline, not a deliberate portfolio decision.

Satellite ETF selection within a single thematic category can produce radically different outcomes: across cybersecurity, robotics, and gaming in 2026, the return spread between the best and worst performer exceeded 35 percentage points, illustrating why thesis clarity and individual fund due diligence matter even when the broad thematic direction appears straightforward.

The main categories of satellite instruments available to Australian investors include:

- Thematic ETFs: AI and technology, clean energy, global infrastructure, defence and cybersecurity, factor tilts (value, quality, high dividend)

- Individual shares: Direct equity positions in companies the investor has researched independently

- Startup or private business stakes: Higher-risk, illiquid positions for experienced investors

According to the BetaShares Australian ETF Review 2024 (published January 2025), AI and technology-related ETFs were among the fastest-growing thematic segments by funds under management in 2024. Morningstar Australia’s 2024 ETF Landscape reports highlight global infrastructure ETFs as a popular satellite income theme, with potential inflation-linked cash flows from utilities, toll roads, and pipelines. Livewire Markets coverage in late 2024 noted rising interest in defence and cybersecurity ETFs as satellites linked to geopolitical risk.

The ASX Investor Update (Summer 2024) warns that niche sector or thematic ETFs should not be mistaken for broad diversification.

That warning matters. Stockspot’s 2024 report notes that multiple overlapping tech and thematic ETFs can create unintended concentration in a few global mega-cap stocks. Morningstar Australia’s 2024 analysis adds that many popular global thematics are heavily U.S.-centric and tech-heavy, leading to over-concentration in U.S. tech when layered on top of a global index core.

Sizing individual satellite positions

Each individual satellite should remain small relative to the total satellite allocation. If satellites represent 20% of the portfolio, no single satellite position should dominate that 20%. Alex’s community example of roughly 10% each across three categories (small-caps, thematics, and individual stocks) illustrates one way to distribute the satellite allocation, though this is illustrative only.

Limiting the total number of satellite positions is also advisable. Numerous small holdings create administrative burden, including tax reporting obligations at each financial year end.

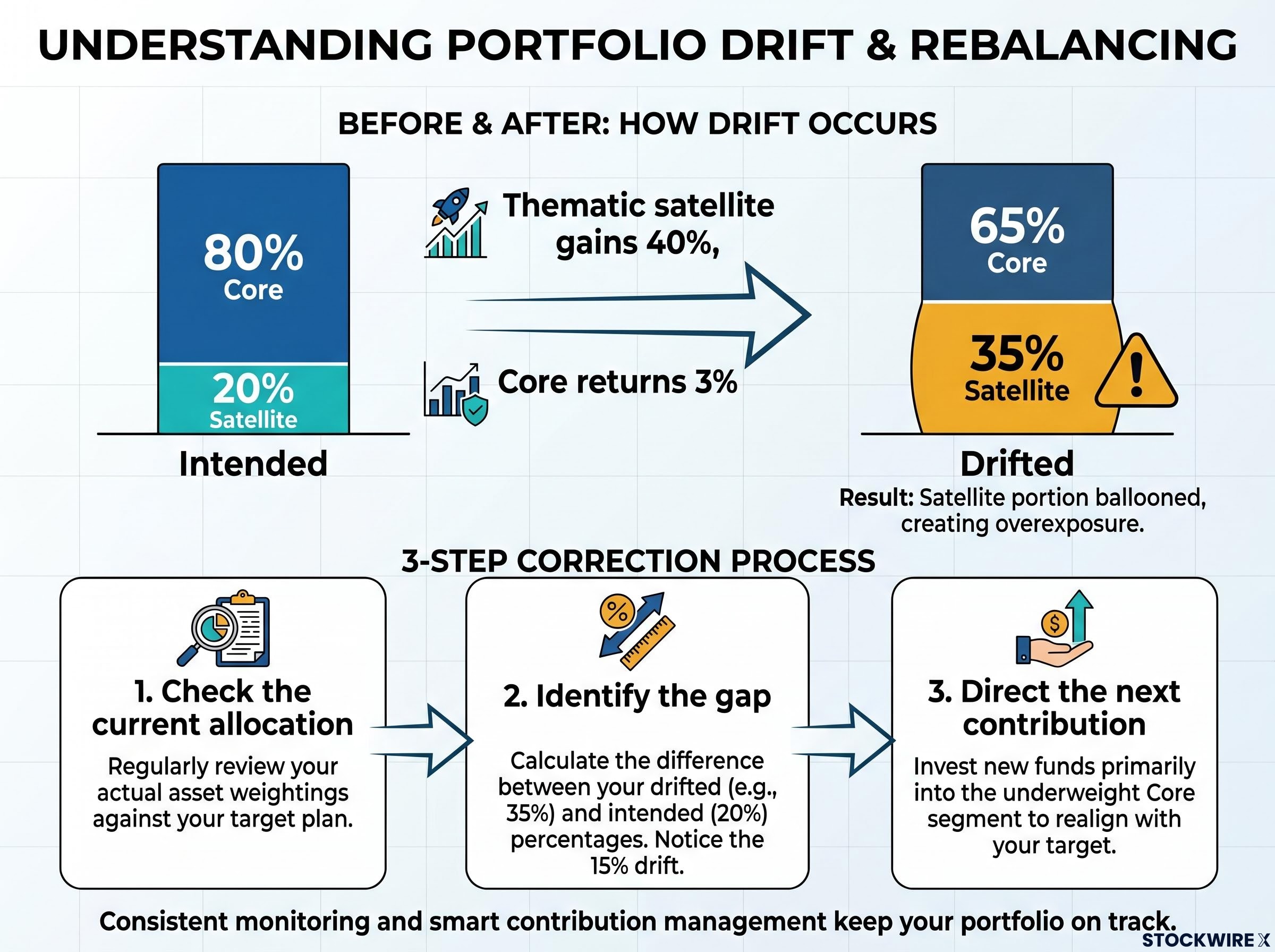

What to do when your portfolio drifts off plan

A portfolio does not stay at its intended allocation on its own. When a thematic satellite gains 40% in a quarter while the core returns 3%, the satellite’s share of the total portfolio grows without the investor making a single trade. That quiet drift changes the portfolio’s actual risk profile.

This is how investors who started with a 20% satellite allocation wake up holding 35% in satellites after a strong run. The intended structure has changed, and so has the downside exposure.

Rebalance by adding, not selling, wherever possible.

The preferred approach for Australian investors is to direct future contributions toward whichever component is underweight, rather than selling appreciated holdings. Selling triggers capital gains tax (CGT) events, and Australia’s 12-month CGT discount structure means the timing of any sale matters. Frequent rebalancing through selling is particularly costly.

Two failure modes are common:

- Check the current allocation against the intended core-to-satellite ratio

- Identify the gap between where the portfolio sits and where it should be

- Direct the next contribution (salary, dividend reinvestment, or lump sum) toward the underweight component

The opposite error is equally damaging: rebalancing too frequently in response to short-term volatility, incurring unnecessary CGT and trading costs. The core guidance from 2024 adviser commentary is to remain aware of shifting exposure and take action only when the actual allocation moves outside the investor’s comfort zone.

For investors wanting to model exactly how to execute this in practice, our dedicated guide to tax-efficient rebalancing in Australia walks through the contribution-first method, rebalancing inside super and SMSF structures at the concessional 15% rate, and how to use a 5% drift threshold to avoid both under-rebalancing and unnecessary CGT events.

The next major ASX story will hit our subscribers first

The six mistakes that quietly undermine a core-satellite portfolio

Each of these pitfalls is well-documented across Australian sources. Most investors do not make them deliberately; they accumulate through small, seemingly reasonable decisions.

- Oversized satellites. It starts with one extra thematic ETF, then another. Stockspot’s 2024 report notes portfolios with 10-20+ ETFs and overlapping exposures are common among DIY investors. The corrective principle: set a maximum satellite percentage before buying, and enforce it.

- Performance-chasing and recency bias. ASIC’s Report 778 (December 2023) found that a subset of ETF investors choose funds based on recent strong performance, particularly in technology and clean energy, rather than long-term strategy. The corrective principle: if the primary reason for buying is that the ETF has recently risen, it is not a thesis.

The thematic ETF behaviour gap, the difference between a fund’s reported time-weighted return and the money-weighted return actually experienced by investors who bought near peak inflows, is the mechanism behind the performance-chasing mistake, and it has cost the average thematic investor more than headline fund returns suggest.

ASIC’s Report 778 documented patterns of retail investors selecting exchange-traded products based on recent strong performance rather than long-term strategy, a behavioural tendency that the core-satellite framework directly addresses by requiring a stated thesis before any satellite position is added.

- Misunderstanding ETF concentration. Morningstar Australia’s 2024 commentary notes that some thematic ETFs hold concentrated baskets of 20-50 stocks highly correlated with each other. Investors assume all ETFs are broadly diversified. The corrective principle: check the holdings list and the number of positions before treating any ETF as a diversifier.

- Complexity creep. Too many ETFs defeats the purpose of a simple framework. Stockspot’s 2024 report highlights that portfolios with overlapping global equity, sector, and thematic funds make it difficult to track true asset allocation. The corrective principle: if the portfolio cannot be summarised in a few sentences, it has too many holdings.

- Misaligned risk. Adviser commentary in 2024 describes two patterns: investors who build a conservative core but add geared or crypto-linked satellites, making the overall portfolio far riskier than intended; and investors who hold an aggressive growth core plus high-beta satellites, making drawdowns emotionally intolerable. The corrective principle: assess the total portfolio’s risk, not the core’s and satellites’ risks separately.

- Ignoring geographic and sector overlap. Morningstar Australia’s 2024 analysis shows that many global thematics are heavily U.S.-centric. Adding several on top of a global index ETF can over-concentrate in U.S. tech mega-caps. The corrective principle: before adding a satellite, check whether the core already provides 50% or more of the same underlying exposure.

The framework is the plan, and the plan is the point

The core-satellite framework’s primary value is not the specific ETFs chosen. It is the discipline of having a structure that investors can reference during market volatility, instead of making reactive decisions based on short-term price movements.

The key principles to carry forward:

- Keep the core dominant at 70-90% of the portfolio

- Select core holdings for broad diversification and low cost, not recent performance

- Treat each satellite as a deliberate answer to a specific investment thesis

- Size satellites small enough that any single position’s failure does not destabilise the portfolio

- Manage drift through directing future contributions, not through frequent selling

- Resist complexity creep; fewer holdings with clear roles outperform a crowded portfolio

A practical next step: identify what is already held, determine whether it constitutes a core, and decide whether any satellite exposure is warranted and clearly justified. The framework works not because it is complex, but because it replaces impulse with intention.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.