SpaceX IPO Lockup: 83% of Insider Shares Unlock Before 180 Days

41 mins ago

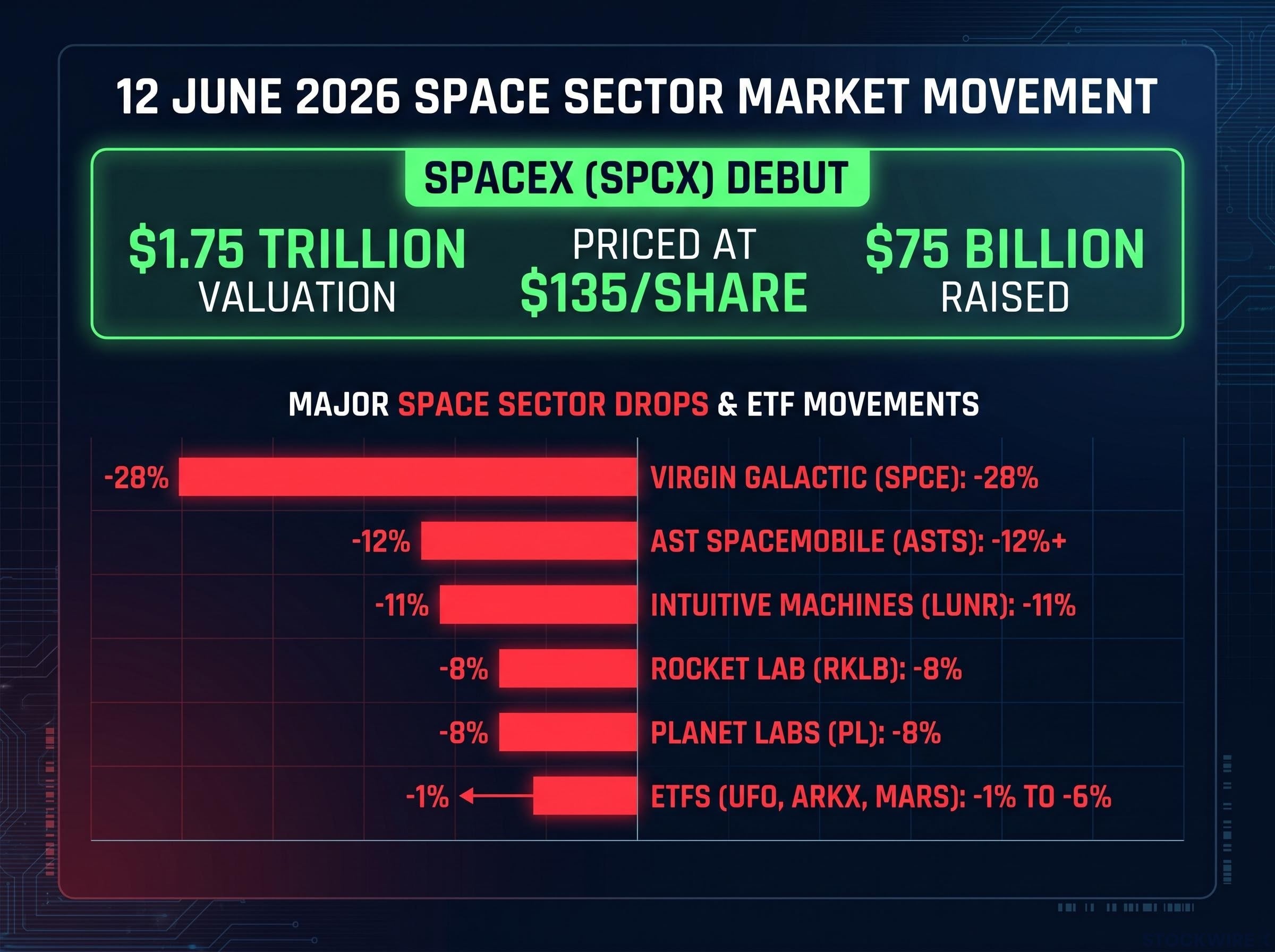

SpaceX debuted on Nasdaq at a valuation of approximately $1.75 trillion on 12 June 2026, the largest initial public offering in history. In the same session, the stocks that investors had been using as proxies for space sector exposure fell between 8% and 28%. The event that was supposed to validate space sector stocks as an investable theme instead triggered a sector-wide repricing. What follows is an examination of the three forces behind the selloff, an assessment of which types of space companies face the greatest re-rating risk, and a four-dimension framework for evaluating positions held or under consideration today.

SpaceX priced at $135 per share under the ticker SPCX, raising approximately $75 billion and beginning trading on 12 June 2026. The scale of the debut was matched by the scale of the damage across smaller names.

The SpaceX IPO pricing mechanics that shaped the debut include a decision to bypass the traditional institutional roadshow entirely, meaning no institutional order book existed to signal demand before shares began trading and the first genuine price discovery occurred live on the exchange.

SpaceX priced at $135 per share under the ticker SPCX, raising approximately $75 billion and beginning trading on 12 June 2026; LA Times reporting on the debut session confirmed shares rose approximately 18% above the IPO price in early trading, with the company’s valuation reaching $1.77 trillion.

| Ticker | Company | June 12 Move (approx.) | Category |

|---|---|---|---|

| SPCE | Virgin Galactic | -28% | Individual stock |

| ASTS | AST SpaceMobile | -12%+ | Individual stock |

| LUNR | Intuitive Machines | -11% | Individual stock |

| RKLB | Rocket Lab | -8% | Individual stock |

| PL | Planet Labs | -8% | Individual stock |

| UFO | Procure Space ETF | -1% to -6% | ETF |

| ARKX | Ark Space & Defence Innovation ETF | -1% to -6% | ETF |

| MARS | Roundhill Space and Technology ETF | -1% to -6% | ETF |

These figures are based on intraday reporting and may be subject to revision against final closing data.

The breadth matters. This was not company-specific news driving isolated declines. The ETF-level losses of 1%-6% across UFO, ARKX, and MARS confirm a systemic repricing of space sector valuations, not a rotation within the sector.

Chris Beauchamp, Chief Market Analyst at UK-based broker IG Group, noted that investor concern centred on hype failing to match real-world expectations, a dynamic that the SpaceX debut crystallised rather than created.

Space sector stocks had gained between 34% and 89% year-to-date through the last close before 12 June 2026. That context changes how the selloff reads. The declines were not erasing fundamental progress; they were reversing a prolonged speculative premium that had been building for months in anticipation of exactly this event.

Virgin Galactic offers the starkest illustration. On 11 June, SPCE surged more than 20%, a move partly attributed to investor confusion between its ticker and SpaceX’s new SPCX symbol. That gain reversed entirely the following day, with SPCE falling approximately 28%. In a market with thin liquidity and sentiment-driven flows, small order imbalances produced outsized price swings in both directions.

Only a relatively small portion of SpaceX shares initially floated, but the existence of a tradeable ticker was sufficient to trigger the rotation that followed.

The selloff was not a single dynamic. Three forces operated simultaneously, and all three are likely to persist beyond the listing day:

These three forces are additive, not alternative explanations. Each amplified the others on 12 June, and each has a duration that extends well beyond a single trading session.

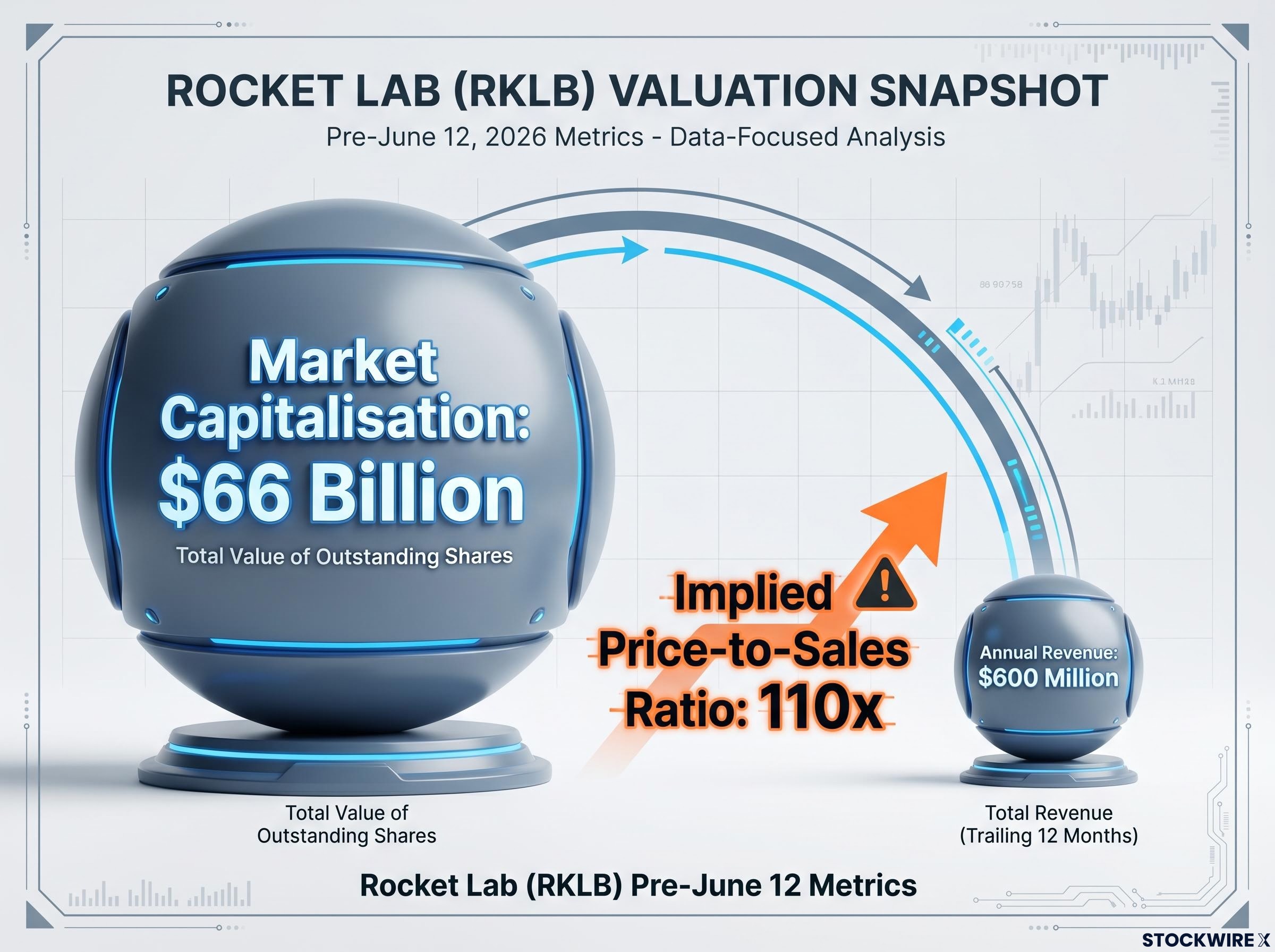

Rocket Lab closed the session before 12 June 2026 with a market capitalisation of approximately $66 billion. Its annual revenue in the prior fiscal year was approximately $600 million.

The implied price-to-sales ratio is approximately 110x. (This figure is derived from the market cap and revenue data cited above and has not been independently verified against final revenue reporting; pre-publication confirmation against audited figures is recommended.)

That number, by itself, tells the story. A $66 billion valuation for a $600 million revenue business requires investors to believe in sustained high revenue growth for many years, eventual strong margins in a capital-intensive industry, and minimal competitive disruption from SpaceX’s own expanding services, including Starship and Starlink.

Before 12 June, investors could sustain that belief in relative isolation. No directly comparable public benchmark existed. The sector’s valuations floated in a vacuum.

The benchmarking logic is straightforward: if SpaceX, with superior scale, launch cadence, Starlink’s recurring revenue base, and deep government relationships, trades at a given price-to-sales multiple, it becomes structurally difficult to justify a smaller peer with fewer competitive advantages trading at a higher one.

SpaceX’s $1.75 trillion valuation is now the live reference point. Every peer multiple in the sector is measured against it in real time. Rocket Lab is used here as a case study, but the same arithmetic applies to any space company whose market capitalisation implies multiples that exceed SpaceX’s own.

SpaceX’s revenue segments span four distinct business lines at different maturity stages — launch services, Starlink broadband, Direct-to-Cell wholesale infrastructure, and AI compute — and applying a sum-of-the-parts methodology to each segment produces a materially different valuation picture than treating the $1.75 trillion figure as a single-business multiple.

At 50x to 100x-plus price-to-sales multiples, investors are not buying today’s business. They are buying an aggressive 5-10 year growth scenario with minimal margin for error. Any deceleration in growth, any missed milestone, or any macro-driven compression in speculative appetite can produce outsized drawdowns from elevated entry points.

The long-duration growth assumptions embedded in space sector multiples were documented in analyst assessments before the IPO priced, with a 250x EBITDA multiple flagging approximately 30% overvaluation risk even before the live benchmark existed to test those assumptions against.

The sector’s pricing had embedded these aggressive long-duration assumptions precisely because SpaceX’s private status made direct exposure unavailable. Smaller companies absorbed capital that would otherwise have sought the market leader. That proxy premium is now being unwound.

AST SpaceMobile (ASTS), which fell over 12% on 12 June, illustrates the competitive dimension. Its satellite broadband ambitions place it in direct competition with Starlink, a business that already generates significant recurring revenue for SpaceX. The question facing ASTS holders is not whether satellite broadband is a large market; it is whether ASTS can capture enough of that market to justify its valuation when SpaceX is already operating at scale.

Three categories of investors face the greatest exposure to further re-rating:

The question every space sector position must now answer is specific: what can this business do that SpaceX cannot, will not, or should not do?

Companies with government mission-specific contracts, proprietary Earth observation data products, or non-launch service niches are better positioned to pass this test. Pure-play launch competitors, or those offering services where SpaceX is already building at scale, carry the highest re-rating risk.

Investors applying the competitive differentiation test to individual names will find our detailed coverage of space stocks with differentiated competitive positions, which profiles Rocket Lab, Intuitive Machines, and AST SpaceMobile with their specific contract wins, revenue figures, and government relationships that form the basis of any durable differentiation argument.

The analysis above converts into a four-dimension evaluation framework that can be applied to any space sector position:

Even a correct long-term thesis can be derailed by forced selling if the position is oversized relative to total capital. Position sizing matters more than entry-price precision in a sector capable of producing 20%-28% single-session moves.

Direct SpaceX exposure via SPCX is now available and represents a structurally different risk profile than the smaller names: higher certainty of revenue base, Starlink cashflow, and launch cadence. It also carries its own embedded growth assumptions at a $1.75 trillion starting valuation.

The near-term profit-taking component of the 12 June selloff is largely mechanical and may be substantially complete within days. The structural re-rating component is not.

The three forces identified earlier, capital rotation, valuation benchmarking, and sentiment normalisation, each have durations that extend beyond a single session. The proxy premium that inflated smaller space stocks over recent months reflected borrowed enthusiasm from a future event. That event has now occurred. The premium has no forward catalyst to sustain it.

What remains is a visible gap between current valuations and current fundamentals, a gap that was easier to overlook when no live benchmark existed. SpaceX’s public valuation is now a permanent fixture of the sector’s analytical landscape.

Three conditions could justify re-rating smaller space stocks back toward prior multiples: meaningful acceleration in contract wins that demonstrates demand independent of SpaceX, a credible path to profitability within a defined timeframe, or demonstrated competitive differentiation that SpaceX’s own expansion has not eroded.

Investors holding these positions should set concrete revenue or contract milestone triggers as review points. Price recovery alone is not thesis validation; it may simply reflect another speculative cycle layering on top of the same unresolved fundamentals.

The 12 June 2026 selloff was predictable, structurally driven, and likely to persist until fundamentals close the gap with valuations. The space sector’s pricing model changed permanently when SPCX began trading, introducing real-time benchmarking that smaller companies cannot avoid.

The actionable step is direct: apply the four-dimension framework, time horizon, competitive position, funding risk, and position sizing, to every space sector holding before the next trading session. The space sector’s long-term growth story remains intact, but the valuation chapter has changed. The investors who navigate this shift successfully will be those who price that change into their positioning rather than waiting for the market to do it for them.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.

—

Three forces drove the selloff: investors sold smaller space stocks to buy SpaceX directly (mechanical rotation), SpaceX's live valuation became a real-time benchmark that made peer multiples harder to justify, and the speculative forward premium built up in anticipation of the IPO was removed once the event occurred.

The proxy premium refers to the extra valuation that smaller, publicly traded space companies absorbed because investors had no direct way to buy SpaceX while it was private; once SpaceX began trading under SPCX, that premium began unwinding as capital rotated to the direct ticker.

Virgin Galactic (SPCE) fell approximately 28%, AST SpaceMobile (ASTS) fell over 12%, Intuitive Machines (LUNR) fell around 11%, and Rocket Lab (RKLB) and Planet Labs (PL) each fell approximately 8%, while space ETFs including UFO, ARKX, and MARS declined 1%-6%.

The article recommends a four-dimension framework: assess whether your holding period is long enough to allow the business to grow into its valuation, confirm the company has a clear competitive advantage over SpaceX, check that revenue visibility or a path to profitability exists, and ensure your position is sized so a 20%-plus single-session decline does not force a liquidation decision.

Three conditions could support a recovery in smaller space stock valuations: meaningful acceleration in contract wins that demonstrates demand independent of SpaceX, a credible path to profitability within a defined timeframe, and demonstrated competitive differentiation that SpaceX's own expansion has not eroded.