Only 5% of SpaceX shares are trading today. The other 95% sit behind a lockup schedule that most IPO coverage has not bothered to decode, and the structure bears almost no resemblance to the standard template investors have come to expect from large-cap listings.

While mainstream reporting has focused on the $135 IPO price and Elon Musk’s public profile, the supply mechanics that will govern SPCX through December 2026 are hiding in plain sight inside the SEC prospectus. The schedule is not a single cliff. It is a series of roughly a dozen distinct unlock events, one of which is tied to a performance trigger that could fire within weeks of today’s opening bell.

What follows is a precise calendar of every unlock date, a breakdown of the performance trigger that could accelerate insider supply, and a structural map of how index rebalancing interacts with each expanding float event. This is the supply architecture retail investors need before the first unlock arrives in August.

How SpaceX built a non-standard lockup with multiple release stages instead of one expiration date

Most large IPOs use a single lockup expiration. Rivian and Uber both employed the conventional model: one 180-day cliff, one expiration date, one wave of potential selling. Investors mark the calendar, watch the date, and move on.

SpaceX built something structurally different. The prospectus contains a multi-stage release framework incorporating:

- A performance trigger tied to early price appreciation

- A Q2 earnings cliff releasing 20% of eligible insider shares

- Five time-based tranches, each releasing 7%

- A Q3 earnings cliff releasing 28%, the largest single event

- A 180-day endpoint releasing the remaining 17%

Musk and certain significant investors sit outside this schedule entirely, subject to a separate 366-day lockup.

The strategic logic is distribution. Spreading supply across roughly 12 distinct dates reduces the headline impact of any single event and avoids the concentrated panic that a one-day cliff can trigger. Whether it prevents sustained selling pressure is a separate question, one the next six months will answer.

When big ASX news breaks, our subscribers know first

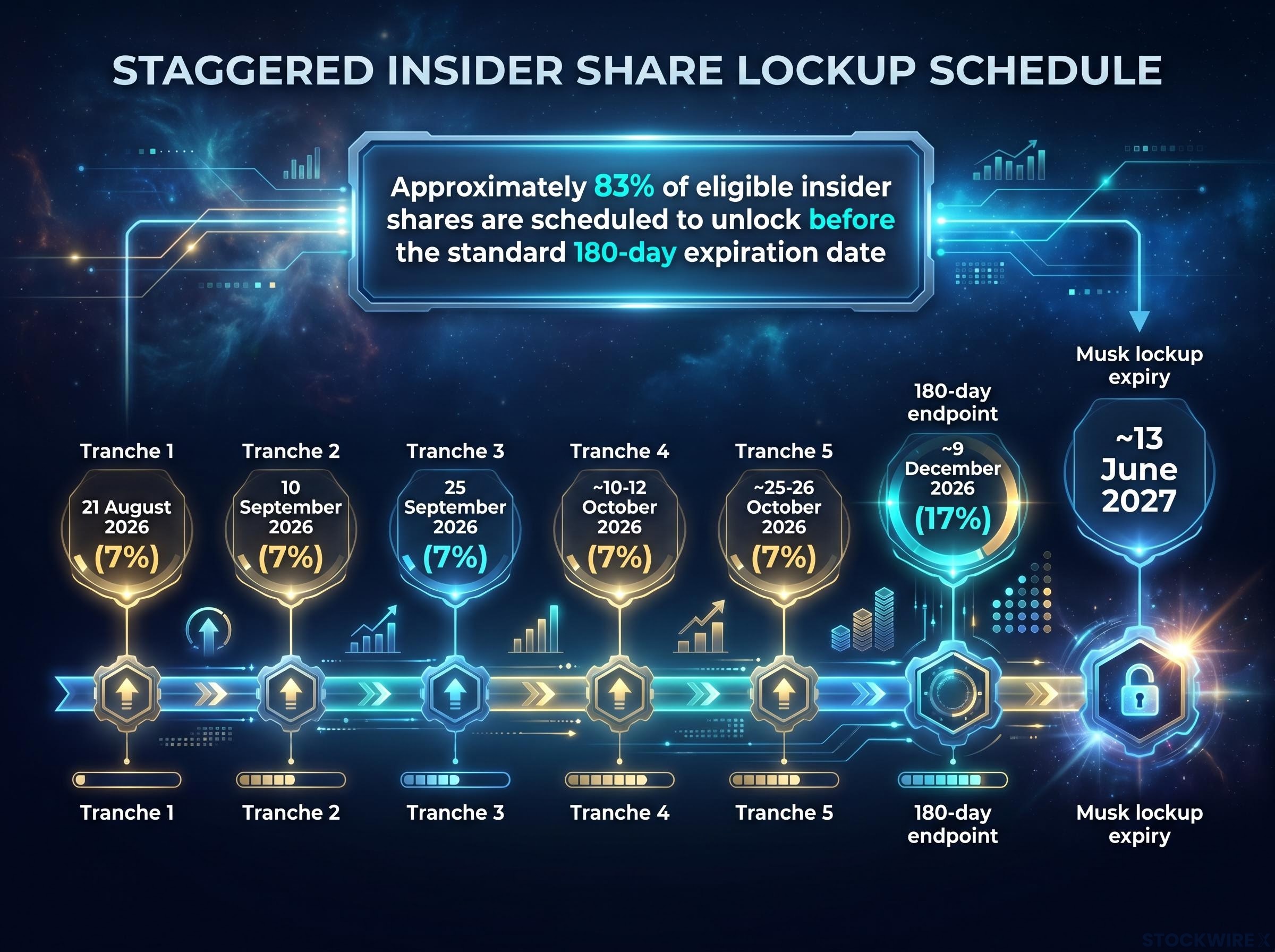

The full unlock calendar: every date, every percentage, mapped from today

The table below consolidates every unlock event from the SEC prospectus into a single reference, ordered chronologically from today’s listing through Musk’s June 2027 expiry.

Two caveats before reading it. The five time-based tranche dates are weekend-adjusted approximations based on a 12 June 2026 IPO. The two earnings-cliff dates cannot be precisely fixed until SpaceX confirms its Q2 and Q3 reporting schedule.

Reading the table correctly

All percentages apply to eligible insider shares, a category that explicitly excludes Musk and certain MNPI-restricted holders. These figures do not map directly to total company share count. Investors should monitor SpaceX’s earnings announcements to pin the Q2 and Q3 cliff dates as they approach.

| Event | Approx. Date | % of Eligible Insider Shares | Notes |

|---|---|---|---|

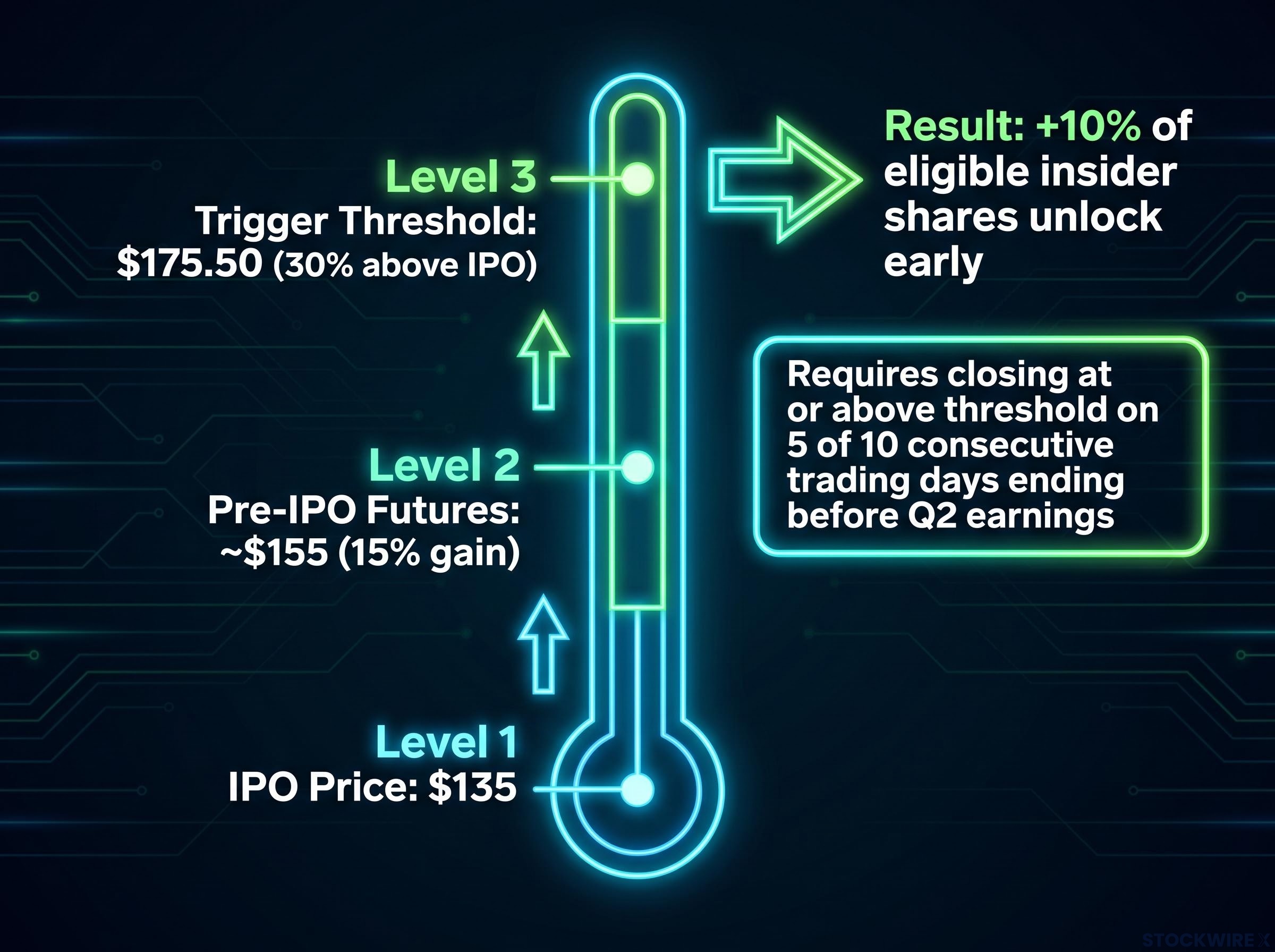

| Performance trigger (if activated) | Before Q2 earnings | +10% | Requires ≥30% above IPO price on 5 of 10 trading days |

| Q2 earnings cliff | 2 trading days after Q2 release | 20% | Timing uncertain; may precede or follow Tranche 1 |

| Tranche 1 (Day 70) | 21 August 2026 | 7% | Time-based, unconditional |

| Tranche 2 (Day 90) | 10 September 2026 | 7% | Time-based, unconditional |

| Tranche 3 (Day 105) | 25 September 2026 | 7% | Time-based, unconditional |

| Tranche 4 (Day 120) | ~10-12 October 2026 | 7% | Weekend-adjusted |

| Tranche 5 (Day 135) | ~25-26 October 2026 | 7% | Weekend-adjusted |

| Q3 earnings cliff | 2 trading days after Q3 release | 28% | Largest single unlock; can cluster with Tranches 4-5 |

| 180-day endpoint | ~9 December 2026 | 17% (remainder) | Cleanup event; bulk already unlocked |

| Musk lockup expiry | ~13 June 2027 | Musk’s shares only | Entirely separate from above schedule |

Approximately 83% of eligible insider shares are scheduled to unlock before the standard 180-day expiration date.

That figure reframes 9 December 2026 from “the lockup expiry” to a cleanup event. The supply story plays out months earlier.

The performance trigger: how a strong early rally could pull 10% of supply forward

The trigger is not hypothetical. The clock started ticking at this morning’s opening bell.

The mechanics are precise: if SPCX closes at or above 30% above the $135 IPO price on at least 5 of 10 consecutive trading days ending immediately before the Q2 earnings release, an additional 10% of eligible insider shares unlock early. That threshold sits at approximately $175.50.

Pre-IPO futures markets were already pricing SPCX at roughly $155, implying an anticipated 15% gain above the IPO price before a single share traded publicly. The gap between that anticipated opening level and the trigger threshold is approximately 13%, meaning the trigger is not a distant target but a plausible outcome of sustained early momentum.

If the trigger fires, two things happen simultaneously:

- 10% of additional eligible insider shares unlock on top of the 20% Q2 earnings cliff, creating a combined 30% early unlock window

- The elevated price levels that activated the trigger simultaneously signal to already-eligible insiders that it is an attractive moment to sell

A strong enough first-week rally could be sufficient to activate the performance trigger, pulling forward the largest combined unlock of the early schedule.

A retail investor buying into a first-week rally needs to understand they may be simultaneously creating the conditions that accelerate insider supply.

Valuation overstretch risk compounds the supply mechanics: at a 250x EBITDA multiple, the $1.75 trillion pricing already embeds decades of forward growth, meaning that any insider selling into post-trigger price levels arrives at a moment when market cap may be furthest from fundamental anchor points.

What lockup schedules actually do to share prices: the structural mechanics explained

A lockup expiration does not force anyone to sell. It removes the contractual barrier that prevented them from doing so. The distinction matters because the actual price impact at any unlock date depends entirely on how many eligible insiders choose to exercise their new ability.

The pressures pushing toward selling are real and well-documented. Insiders who have held pre-IPO shares for years face rational incentives to convert paper gains to cash once the first window opens. Those pressures break down into three broad categories:

- Venture capital funds with LP-driven return obligations, where fund structures require realised distributions, not unrealised appreciation

- Senior employees carrying high concentration risk, whose net worth is disproportionately tied to a single holding

- Early investors with multi-year paper gains and, in some cases, client return obligations creating additional pressure to monetise

The tool for distinguishing between an unlock that triggers aggressive selling and one that passes quietly is Form 4 filings, the SEC-mandated disclosure that captures actual insider transactions. Until Form 4s appear, every unlock event is a window of elevated supply risk, not a confirmed supply increase.

The SEC Form 4 filing requirements mandate that insiders report transactions within two business days, making Form 4 disclosures the most timely public signal of whether eligible insiders are converting unlocked shares into actual sales at each window.

What history shows about staggered lockup performance

Staggered lockup structures do not guarantee price support. Facebook’s IPO is the most cited precedent: shares fell significantly by the end of the lockup period despite a staged release structure. The staging distributed the selling across multiple dates, but it did not prevent cumulative pressure from exceeding demand over the full lockup window.

Post-IPO underperformance across the broader IPO universe follows a documented pattern: newly listed companies have trailed comparably sized established peers by an average of 3.3% annually over their first five years, a drag that operates independently of any single lockup structure.

The lesson is straightforward. The schedule defines eligibility, not outcome. Actual selling intensity, visible only through Form 4 filings, determines whether each event creates measurable price pressure.

Float expansion and institutional demand: how passive buying responds to each new unlock

Each unlock event is not purely a supply story. It is a supply-versus-demand tension, and the demand side has a structural component that most lockup analysis ignores.

The NASDAQ 100 recently adopted a fast-entry rule allowing qualifying large IPOs to join the index after only 15 trading days, a dramatic compression from the prior multi-month waiting period. Russell indexes can add SpaceX even faster, within the first 5 trading days. Both inclusions force passive funds tracking these indexes to purchase SPCX shares, concentrating institutional buying into the first weeks of trading.

The interaction deepens at each subsequent unlock. The mechanism follows a sequential logic:

- An unlock event increases the free float

- The higher float raises the float-adjusted market capitalisation

- The increased market capitalisation lifts SPCX’s index weight

- Passive funds must purchase additional shares at the next rebalancing to match the higher weight

A float multiplier rule amplifies this effect for low-float securities. Under current methodology, SpaceX’s initial 5% float is treated as approximately 15% for index weighting purposes, substantially increasing the stock’s initial weight relative to its actual available supply.

Passive assets tracking the NASDAQ 100 are estimated at over $600 billion, though this figure has not been independently verified and should be treated as directional context.

The structural point holds regardless of the precise dollar figure: each lockup step simultaneously releases insider supply and, by expanding float, can generate incremental passive demand. The net price impact at any given date depends on the balance between those two forces.

Why Musk’s year-long lockup tells a different story from the schedule facing other insiders

Musk’s 366-day lockup, with a first eligible sell date of approximately 13 June 2027, is likely to be framed publicly as a confidence signal. It is worth understanding what it does and does not restrain.

Musk controls approximately 85.1% of voting power. His financial interests are not dependent on near-term liquidity in the way that a VC fund managing client capital or an employee with 90% of their net worth in a single holding must consider. His extended lockup is structurally comfortable for his position: majority control, diversified wealth, no concentration risk. It is not a signal about the stock’s near-term supply dynamics.

The supply schedule documented here sits alongside a separate layer of structural complexity: the dual-class share structure that concentrates voting control with founders and insiders regardless of how much economic ownership public shareholders accumulate over time.

The insiders with the most pressing financial reasons to sell, venture funds facing LP return obligations, senior employees diversifying concentration risk, early investors converting multi-year paper gains, all participate in the staggered schedule that begins on 21 August 2026 and concludes on 9 December 2026. By the time Musk’s lockup expires next June, those insiders will have had access to nearly a full year of unlock windows during which they could sell into retail demand.

Three dates that will define the supply picture through December

- Q2 earnings date: Determines whether the performance trigger fires (stock at or above $175.50 on 5 of 10 days before release) and whether the combined early unlock is 20% or 30%

- Q3 earnings date: Triggers the 28% cliff, the largest single unlock, which can cluster with Tranches 4 and 5 in October, creating the most concentrated potential supply window of the entire schedule

- 9 December 2026: The 180-day endpoint releasing the final 17% remainder; by this point, cumulative Form 4 activity will reveal how much eligible selling has already occurred

Tracking the unlock windows: the supply signals that will matter most over the next six months

This is not a single-event lockup story. It is a rolling series of supply windows spanning roughly six months, requiring active calendar monitoring rather than a single expiry alert set for December.

Two takeaways stand above the rest. First, the Q2 earnings date and the $175.50 trigger threshold represent the first definitive branching point in the supply schedule, the moment that determines whether the early unlock is 20% or 30% of eligible insider shares. Second, the Q3 earnings cliff and its potential October clustering with Tranches 4 and 5 represent the most consequential supply concentration of the entire period.

The lockup defines eligibility, not obligation. The actual price impact at each event will reflect the balance between insider selling and passive index demand, neither of which can be forecast in advance. Form 4 filings will be the only hard evidence of realised transactions as each window opens.

For investors wanting to situate the SPCX unlock calendar within a broader framework for approaching marquee IPO listings, our deep-dive into lockup expiry timing strategies examines historical evidence on waiting for first earnings reports and the build-up of independent institutional coverage before establishing a position, rather than buying at the moment of peak public excitement.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements regarding future supply events and price dynamics are speculative and subject to change based on market developments and company performance.