Are Rate Hikes Actually Bad for Stocks? What the Data Shows

1 hr ago

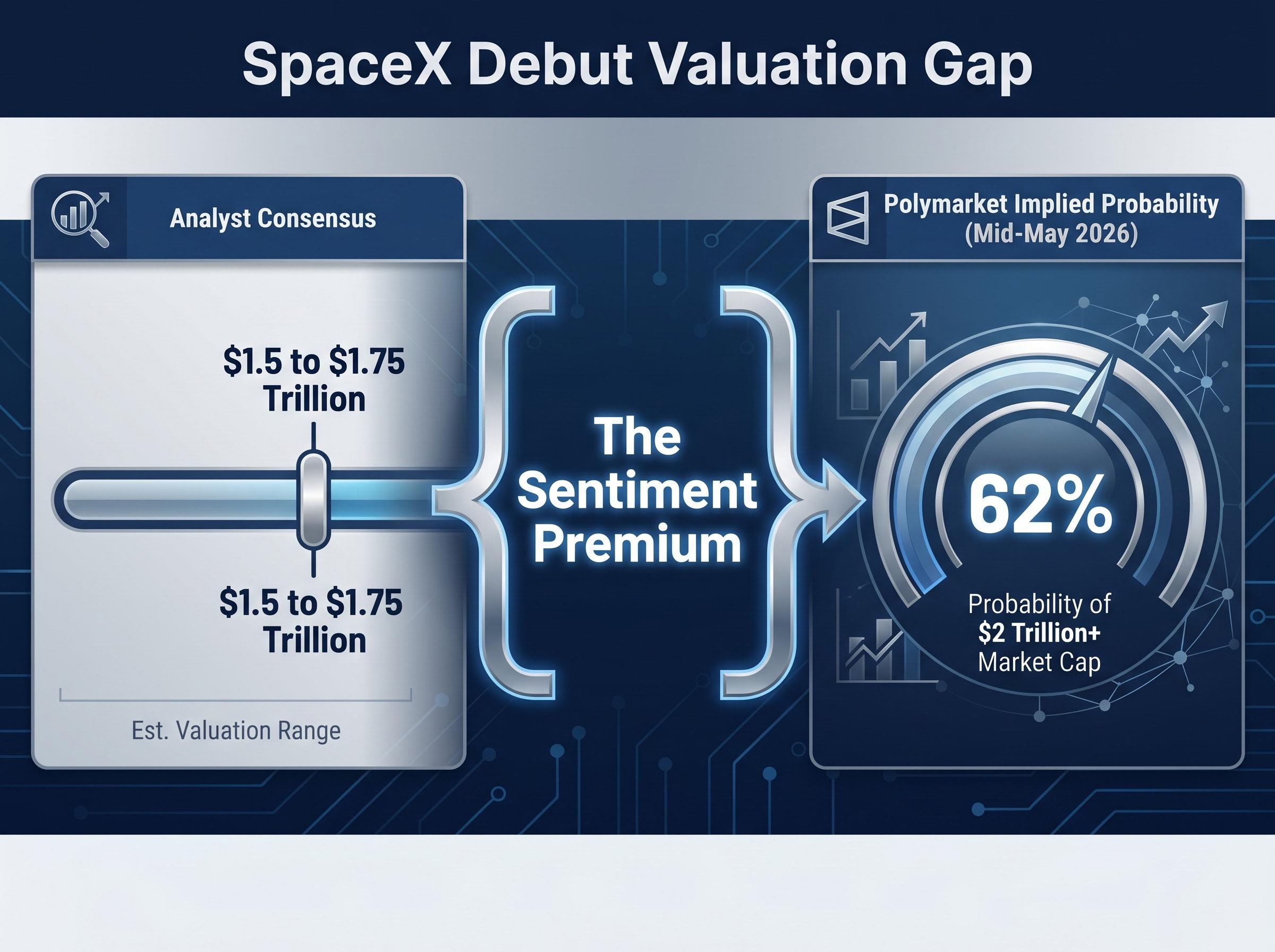

Prediction market participants are pricing SpaceX’s debut market capitalisation above $2 trillion. Analyst consensus sits closer to $1.5 trillion. That gap is not a minor rounding disagreement; it is the clearest available illustration of the premium that excitement commands around marquee initial public offerings, and the first signal that public investors should study before they act.

SpaceX filed its S-1 registration statement with the Securities and Exchange Commission (SEC) on 20 May 2026. OpenAI and Anthropic are preparing their own moves toward public markets. Oura Health filed on the same day as SpaceX. The cluster has produced a surge of retail investor attention not seen since the 2021 SPAC wave, and financial media coverage has shifted from identifying risks to amplifying reasons for optimism. What follows is an evidence-based explanation of why the most anticipated IPOs in any given cycle tend to be structurally disadvantageous for public investors who buy at or near debut, and what a more deliberate framework looks like in practice.

SpaceX confirmed its intention to go public with an S-1 filing on 20 May 2026, lodged with the SEC. As of the filing date, several details remain unresolved:

The filing itself was anticipated. What deserves closer attention is the gap between how professional analysts and how the broader market are valuing the company before a single public share has traded.

SpaceX’s actual disclosed financials, published with the 20 May 2026 registration statement, place full-year revenue at $18.67 billion against a $1.94 billion operating loss in Q1 2026 alone, confirming that the company generating the most IPO excitement in years is not yet profitable at the operating level.

The valuation gap: Analyst consensus places SpaceX’s debut market capitalisation in the $1.5-1.75 trillion range. Polymarket prediction data, as of mid-May 2026, implies approximately 62% probability of a $2 trillion-plus closing market cap on debut day.

That spread matters. It means the enthusiastic end of the market has already priced in a best-case outcome. When the most optimistic scenario is the one the crowd expects, the question for any prospective buyer becomes structural: where does outperformance come from if the price already reflects peak confidence?

The filing is not just a corporate event. It is a live case study in how sentiment runs ahead of fundamentals, and why the mechanics of IPO pricing deserve scrutiny before capital is committed.

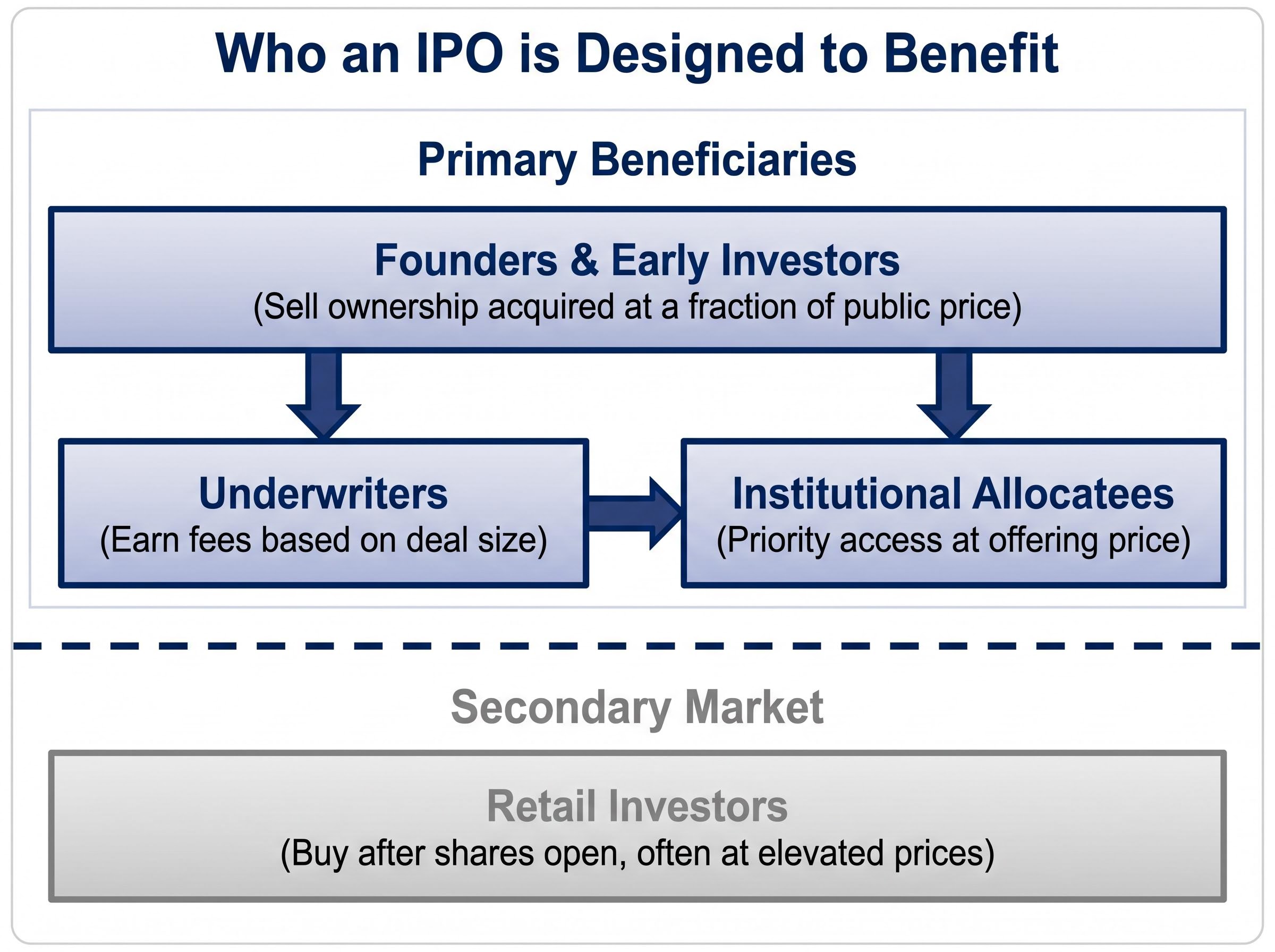

An initial public offering is, at its core, a liquidity event. It allows founders, early employees, and venture capital investors who funded the company’s growth to convert their ownership stakes into cash by selling shares to the public. The capital raised may fund operations or expansion, but the transaction’s primary function is to provide an exit for those who invested earliest at the lowest prices.

This distinction matters because it reframes who the IPO serves. The structure is designed to maximise value for three parties:

Retail investors are notably absent from that list. They typically buy in the secondary market, after shares have already opened, often at prices elevated by first-day demand.

Private capital’s role in IPO timing is a structural underpinning of the dynamic described above: venture capital and private equity markets function as a filter that keeps high-growth companies private until valuations are near peak and then releases them into public markets at the moment that best serves existing shareholders rather than incoming ones.

Underwriters set the offering price through a process called bookbuilding. They canvas institutional investors, hedge funds, and large asset managers to gauge demand, then set a price range designed to clear the offering and produce a modest first-day price increase.

A large first-day pop, the kind celebrated in financial media headlines, is frequently misunderstood. It does not signal that public buyers got a bargain. It signals that the company sold its shares below their market value, transferring wealth from the issuer to the institutional investors who received allocations and can sell into the opening-day demand.

The information asymmetry compounds the structural disadvantage. Insiders, institutional allocatees, and underwriters possess far more granular detail about a company’s financial trajectory, competitive risks, and operational challenges than a retail investor reading the S-1 filing for the first time. The public buyer is not getting in early. They are last in a chain of investors who entered at much lower prices and with much better information.

The structural disadvantage described above would matter less if IPOs, as a category, delivered superior long-term returns. The academic record suggests otherwise.

Jay Ritter, a finance professor at the University of Florida’s Warrington College of Business, maintains the most widely cited academic database on IPO performance. His research documents a consistent pattern: most IPOs underperform the broader market, specifically the S&P 500, over three-year and five-year horizons following their debut.

Jay Ritter’s IPO data, maintained at the University of Florida’s Warrington College of Business and updated through 2024, provides the primary empirical basis for the long-run underperformance pattern, showing that newly public companies have consistently lagged the S&P 500 across three- and five-year measurement horizons spanning multiple market cycles.

Research from Jay Ritter’s University of Florida database indicates that IPOs, as a category, have historically underperformed the S&P 500 over three- and five-year post-listing periods. The pattern has persisted across multiple market cycles.

The pattern is not limited to obscure listings. Some of the highest-profile debuts in modern market history have illustrated the same dynamic. Facebook’s 2012 IPO is perhaps the most instructive example: a company with exceptional underlying business quality that nevertheless declined in value immediately after listing, spending months below its offering price before eventually recovering. Investors who bought on debut day endured significant drawdowns despite being correct about the company’s long-term trajectory.

The dot-com era of 2000 represents the extreme case, when speculative IPO excess reached its peak and scores of newly listed companies lost the majority of their value within months.

| Company | Debut Year | 1-Year vs. S&P 500 | 3-Year vs. S&P 500 |

|---|---|---|---|

| 2012 | Underperformed (traded below IPO price for months post-debut) | Outperformed (recovery driven by mobile advertising growth) | |

| Uber | 2019 | Underperformed (declined approximately 30% from IPO price within six months) | Underperformed (remained below IPO price through 2021) |

| Snap | 2017 | Underperformed (fell below IPO price within months of debut) | Underperformed (traded significantly below IPO price at the three-year mark) |

The pattern documented by Ritter is not a judgement about SpaceX specifically. It is a decades-long empirical record that provides the baseline against which any IPO enthusiasm should be measured. The burden of proof rests on demonstrating why a specific offering will be the exception, not on assuming it will be.

When multiple high-profile companies rush to list in a compressed window, the instinct is to interpret it as a sign of market health. The historical record suggests a different reading.

IPO volume and composition function as a contrarian sentiment indicator. Clusters of marquee listings tend to appear when company insiders and their financial advisers believe valuations have peaked or are near peak levels. Sellers, not buyers, drive the timing. A surge in listings reflects confidence among those exiting their positions, not an abundance of opportunity for those entering.

The conditions that characterise a sentiment peak in IPO markets are recognisable:

Technology sector positioning extremes reinforce the directional signal: the BofA Global Fund Manager Survey shows global managers are more overweight US technology than at any point since before the 2021 peak, and Fisher Investments has moved underweight the sector on the basis that expectations are already embedded in prices rather than any deterioration in underlying business quality.

All four conditions are present in the current cycle. Coverage analysed in late May 2026 characterised financial media as having shifted from cautious risk assessment to optimism amplification across the technology sector, consistent with elevated sentiment.

The specifics reinforce the general principle. SpaceX filed on 20 May 2026. Oura Health filed the same day. OpenAI and Anthropic are both reported to be preparing moves toward public markets, though neither has confirmed structure, timing, or valuation details.

The Polymarket data showing 62% implied probability of a $2 trillion-plus SpaceX debut, well above the $1.5-1.75 trillion analyst consensus, suggests enthusiasm has already moved ahead of the fundamentals that analysts can verify. The current cluster has not reached the extremes of the dot-com era, when unprofitable companies flooded the market. But the directional signal warrants scepticism: sellers are motivated, sentiment is elevated, and the price of participation is being set by optimism rather than by evidence.

Readers planning to act on OpenAI or Anthropic should note that no confirmed structural details, filing dates, or valuation ranges are available for either company as of 23 May 2026. Making capital allocation decisions based on unconfirmed reporting introduces an additional layer of risk.

The evidence above does not mean every IPO is a poor investment. It means the default assumption, that buying a great company at its moment of maximum public excitement produces great returns, is not supported by the historical record. A more deliberate framework begins with five questions every retail investor should be able to answer before committing capital:

The companies most worth owning long-term are not necessarily best bought at the moment of maximum public enthusiasm. SpaceX may prove to be a generational business. That does not automatically make it a well-priced investment on its first day of public trading.

Missing a first-day price pop feels costly in the moment. The data suggests otherwise. If an IPO subsequently underperforms, the opening-day pop was simply a wealth transfer from later buyers to institutional allocatees who sold into the initial demand.

Post-lock-up expirations regularly create short-term price pressure as insiders sell for the first time. The first one or two quarterly earnings reports after listing frequently reveal whether the debut-day pricing reflected reality or aspiration. Institutional research coverage typically builds over six to twelve months following an IPO, providing the kind of independent analysis that is absent on day one.

Jay Ritter’s research reinforces this position: early enthusiasm can be costly for retail buyers, and the most reliable returns in newly public companies have historically come to those who waited for the initial excitement to subside.

For investors who want a complete breakdown of the listing mechanics before committing capital, our full explainer on the SpaceX IPO timeline and deal structure covers the June 12 Nasdaq debut date, anticipated proceeds of $50-75 billion that would surpass the combined IPO totals of Saudi Aramco and Alibaba, and the practical access pathways available to retail investors who are unlikely to receive primary allocations.

SpaceX is a genuinely extraordinary business. Its competitive position in launch services, its Starlink revenue trajectory, and the scale of its ambitions are difficult to parallel in any recent IPO cycle. None of that is in dispute.

What is in dispute is the price. The gap between $1.5 trillion in analyst consensus and $2 trillion-plus in prediction market expectations represents the premium that excitement commands. Every dollar of that premium is a dollar of future return that has already been consumed by sentiment before the first public share changes hands.

A great company and a great investment are not the same thing. The distinction depends entirely on the price paid relative to the value received.

The evidence base for IPO underperformance is decades deep. It spans bull markets and bear markets, technology cycles and financial crises. The burden of proof rests on demonstrating why any specific offering will be the exception, not on assuming it will be. Readers who apply this framework to SpaceX, OpenAI, Anthropic, and every future high-profile filing will make better-structured decisions than those who allow excitement to determine timing.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections and valuations discussed are subject to market conditions and various risk factors.

IPO investing involves buying shares in a company at or after its initial public offering, when it first lists on a stock exchange. Retail investors typically cannot access shares at the offering price and instead buy in the secondary market after trading opens, often at prices already elevated by institutional demand.

Academic research by Jay Ritter at the University of Florida shows that IPOs as a category have consistently underperformed the S&P 500 over three and five year periods following debut, largely because debut prices reflect peak enthusiasm rather than verified fundamentals, and because institutional investors receive preferential allocations at lower prices than public buyers.

A lock-up period, typically 90-180 days after a company lists, restricts insiders and early investors from selling their shares. When the lock-up expires, increased selling pressure frequently pushes share prices lower, which can create more attractive entry points for investors who waited rather than buying on debut day.

As of mid-May 2026, analyst consensus places SpaceX's debut market capitalisation in the $1.5-1.75 trillion range, while Polymarket prediction data implies approximately a 62% probability of a $2 trillion or higher closing market cap on debut day, a gap that reflects how sentiment has moved ahead of verified fundamentals.

Investors should assess the post-IPO lock-up schedule, the implied growth rate embedded in the debut valuation, the company's current profitability trajectory, how the valuation compares to peers with similar revenue and margin profiles, and the historical performance of IPOs in the same sector over one and three year periods.