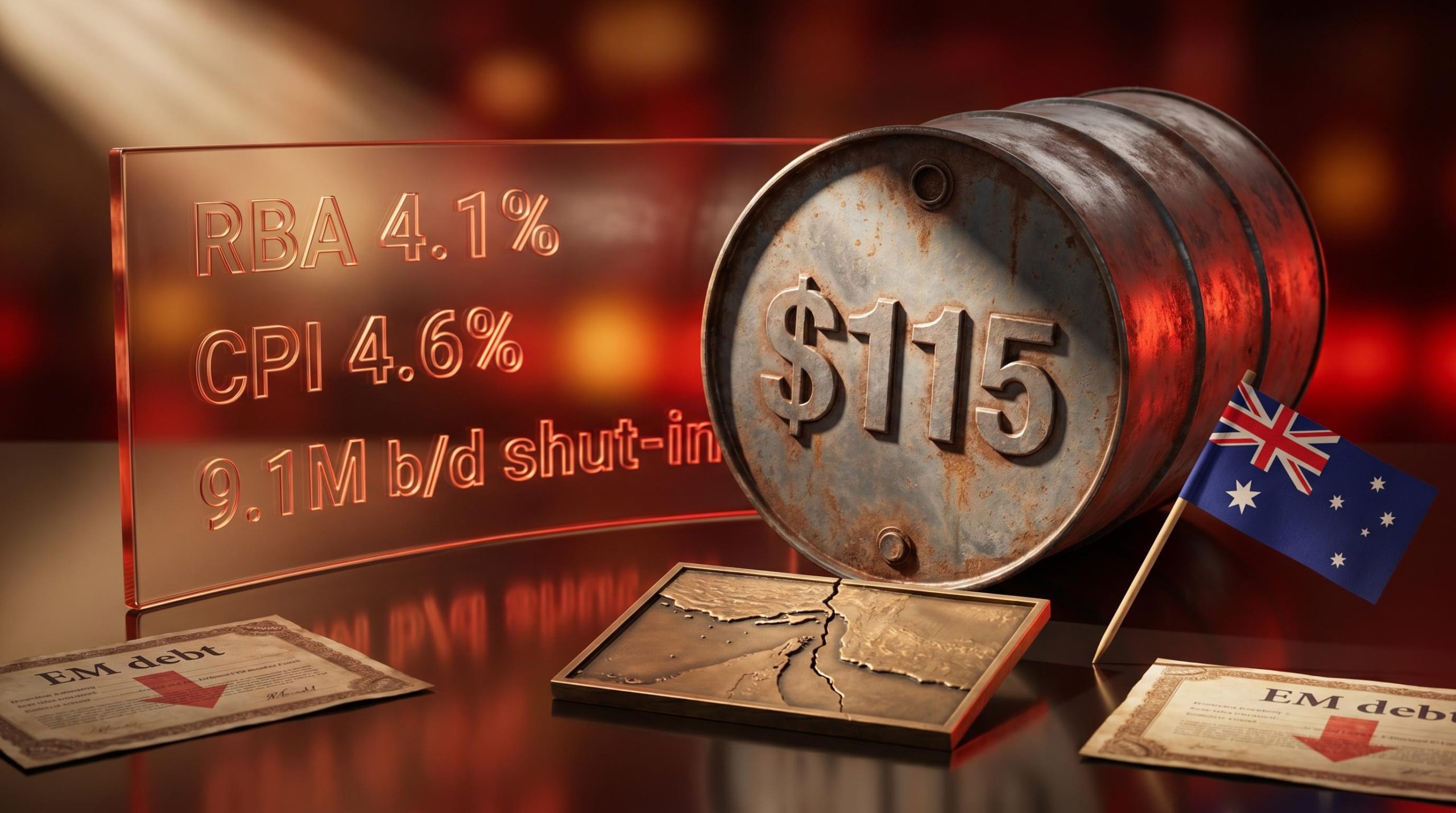

As recently as December 2025, futures markets had priced in roughly 0.50 percentage points of US rate cuts for 2026. Today, those same markets are pricing in rate hikes at the Bank of England and European Central Bank. The Iran conflict did that. The Strait of Hormuz has been effectively closed for nearly three months, a supply shock that has driven Brent crude toward a forecast peak of $115 per barrel, pushed Australian CPI to 4.6%, and prompted the Reserve Bank of Australia (RBA) to lift the cash rate to 4.1% in April 2026, with another hike expected in May. This is not a theoretical risk scenario; it is the current operating environment for Australian investors.

What follows is an analysis of what the oil shock actually means for central bank rate paths, how Morningstar Investment Management’s three-scenario framework structures the range of outcomes, and which specific fixed income exposures are most at risk.

From Hormuz to the high street: how a strait became a rate problem

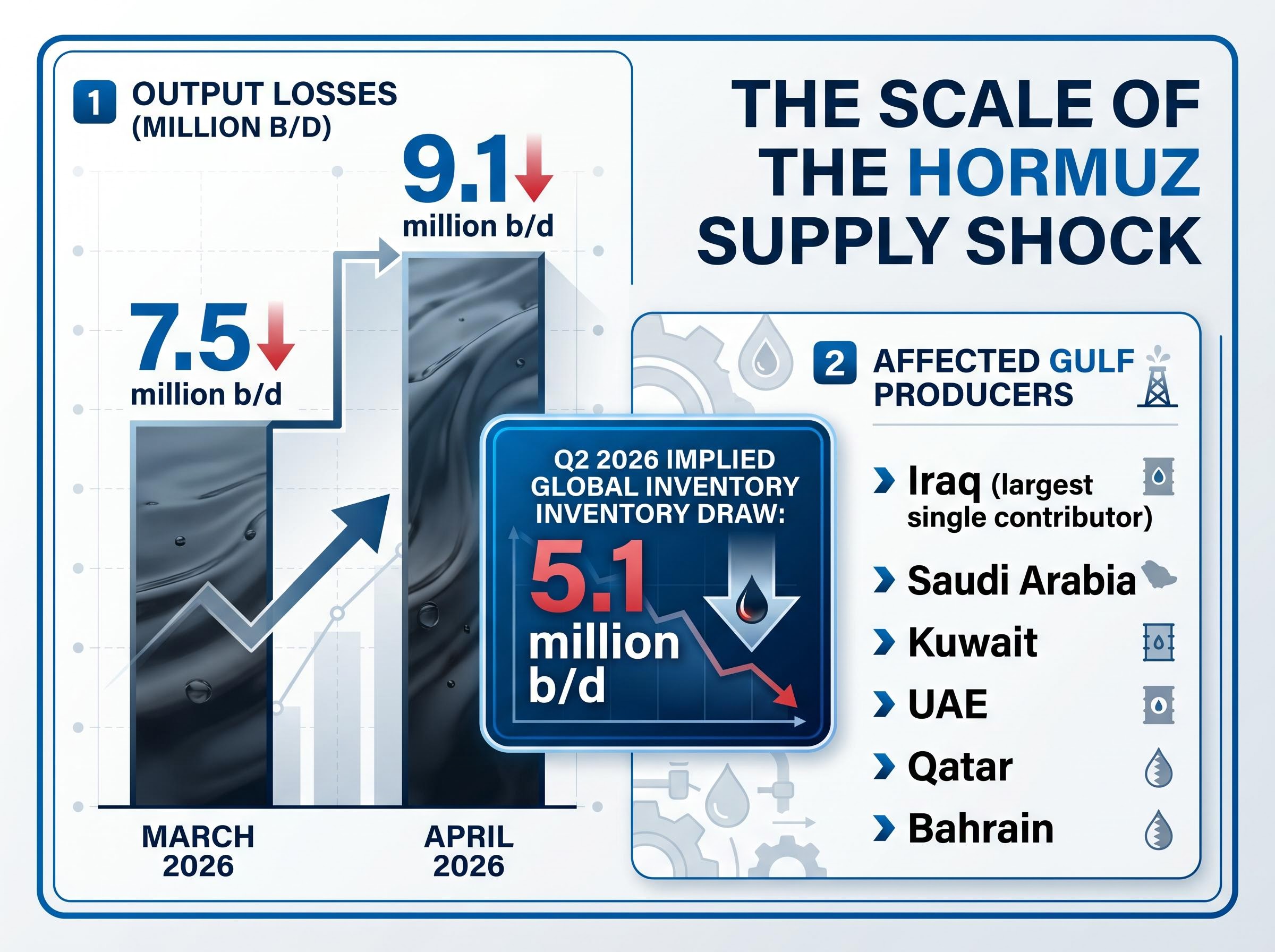

Roughly 20% of global oil supply transits through the Strait of Hormuz. Iran effectively closed it from late February 2026, and as of 1 May, that closure is approaching its third month with no sustained resumption of normal traffic.

The production shut-ins that followed have been severe. By April 2026, output losses across the six most affected Gulf producers had reached 9.1 million barrels per day (b/d), up from 7.5 million b/d in March:

- Iraq: The largest single contributor to the shut-in total, given its landlocked export dependence on Gulf terminals

- Saudi Arabia: Substantial volumes stranded by Hormuz closure despite Red Sea alternatives

- Kuwait: Near-total export disruption through Gulf channels

- UAE: Partial mitigation through Fujairah pipeline capacity, but the majority of volumes affected

- Qatar: LNG and condensate exports severely curtailed

- Bahrain: Smaller volumes, but essentially full disruption

The implied global inventory draw for Q2 2026 stands at 5.1 million b/d, a deficit large enough to tighten physical markets within weeks. The US Energy Information Administration (EIA) raised its full-year 2026 Brent average forecast to $96 per barrel, up from $79 per barrel one month prior, with a projected peak of $115 per barrel in Q2.

Goldman Sachs’s estimate of the global supply deficit reached 9.6 million barrels per day by late April 2026, a figure that reinforces the EIA’s own inventory draw projections and helps explain why central banks from Washington to London are recalibrating rather than waiting for the disruption to self-correct.

JPMorgan warned in late April that Iran’s oil system could hit shut-in thresholds within 15 days, due to storage limits at Kharg Island. If those thresholds are breached, long-term reservoir damage becomes a possibility, meaning lost production capacity that persists well beyond any ceasefire.

Fuel prices, inflation, and the RBA’s reversal

The transmission from closed strait to Australian petrol pump to RBA board room has been direct. Fuel price shocks from the Hormuz disruption were a substantial driver of Australian CPI reaching 4.6% in March 2026.

The RBA responded by hiking to 4.1% in April, with economists broadly expecting a further increase at the May meeting. This represents a full reversal of the prior rate-cutting cycle, not a routine adjustment. Six months ago, Australian borrowers were pricing in relief. Today, the direction of travel has flipped.

The fuel price transmission was the dominant driver of Australian CPI reaching 4.6% in March 2026, with trimmed mean inflation holding at 3.3%, a split that reveals the shock as energy-led rather than broadly embedded across the basket.

When big ASX news breaks, our subscribers know first

What the rate markets are now pricing in around the world

In December 2025, US fed-funds futures implied approximately 0.50 percentage points of rate cuts for 2026. That expectation has been erased entirely. The US is now pricing zero cuts. The Bank of England has shifted from pricing cuts to pricing hikes. The ECB faces elevated inflation from the conflict that has introduced uncertainty into the timing of any further reductions.

| Central Bank | Dec 2025 Expectation | Current Pricing | Direction of Change |

|---|---|---|---|

| RBA | Rate cuts expected | 4.1%; further hike expected May | Cuts → Hikes |

| US Federal Reserve | ~0.50pp of cuts priced | Zero cuts for 2026 | Cuts → Hold |

| Bank of England | Cuts priced | Hikes priced | Cuts → Hikes |

| ECB | Rate reductions expected | Timing uncertain; inflation elevated | Cuts → Uncertain |

The scale of the repricing reflects the mechanism that economist Justin Wolfers has identified as making oil shocks particularly disruptive to rate-cutting cycles.

Wolfers’ framework identifies three transmission channels: rapid gasoline price pass-through to headline inflation, second-round effects on transport and industrial costs, and broader business cost impacts that feed into services inflation. These second-round effects are what make oil shocks stickier than they appear on arrival.

Federal Reserve research on second-round oil price effects documents how energy cost pass-through into transport, industrial inputs, and services inflation tends to persist well beyond the initial price spike, reinforcing why central banks treat sustained oil shocks as a more durable inflation problem than headline figures initially suggest.

For Australian investors, a synchronised global tightening bias reduces the likelihood of meaningful rate relief domestically. The RBA is not acting alone; it is operating within a global environment where every major central bank is recalibrating in the same direction.

Understanding the oil shock: why this disruption is different from past episodes

Investors who recall the 2019 Saudi Aramco attack or the 2011 Libyan civil war may be inclined to treat this as another sharp but brief supply disruption. The specific anatomy of the Hormuz closure suggests otherwise.

Three structural features distinguish this episode:

- Single chokepoint control. The Strait of Hormuz is not a distributed production outage across multiple fields. It is a strategic waterway controlled by a single actor, meaning the disruption can be imposed, lifted, and reimposed at will. The conflict has already demonstrated this pattern, with temporary reopenings around 8 April and 17-18 April followed by immediate reclosure.

- Compounding shut-in dynamics. The longer Gulf producers remain shut in, the greater the risk of long-term reservoir damage. JPMorgan’s warning about Kharg Island storage limits is the concrete expression of this risk: extended shut-ins do not simply pause production; they can permanently reduce future output capacity.

- Extended restoration timeline. EIA Administrator Tristan Abbey stated on 7 April that full Hormuz restoration could take months post-conflict, even after a ceasefire is achieved. Infrastructure damage, mine clearance, and insurance recertification all contribute to a lag that persists well beyond diplomatic resolution.

The EIA’s 2027 average forecast of $76 per barrel implies a long normalisation tail even in the base case. This is not a spike-and-recovery pattern.

The UAE’s exit from OPEC in May 2026, with ADNOC targeting independent production of 5 million barrels per day, introduces a structural variable that the EIA’s normalisation forecasts do not fully capture; a fragmented cartel is less able to coordinate the production response that would accelerate the return to pre-crisis price levels.

Why historical precedent offers limited comfort

Morningstar has noted that few short-term geopolitical events have caused lasting equity market damage over extended time horizons. That observation holds for equities. Fixed income, however, is a different proposition. Bond markets are directly sensitive to sustained inflation repricing, and the duration of this disruption, approaching three months at time of writing, already exceeds most precedent episodes in the modern era.

The distinction matters: equity investors may reasonably hold through the volatility, but fixed income investors face a structural repricing that historical precedent does not adequately address.

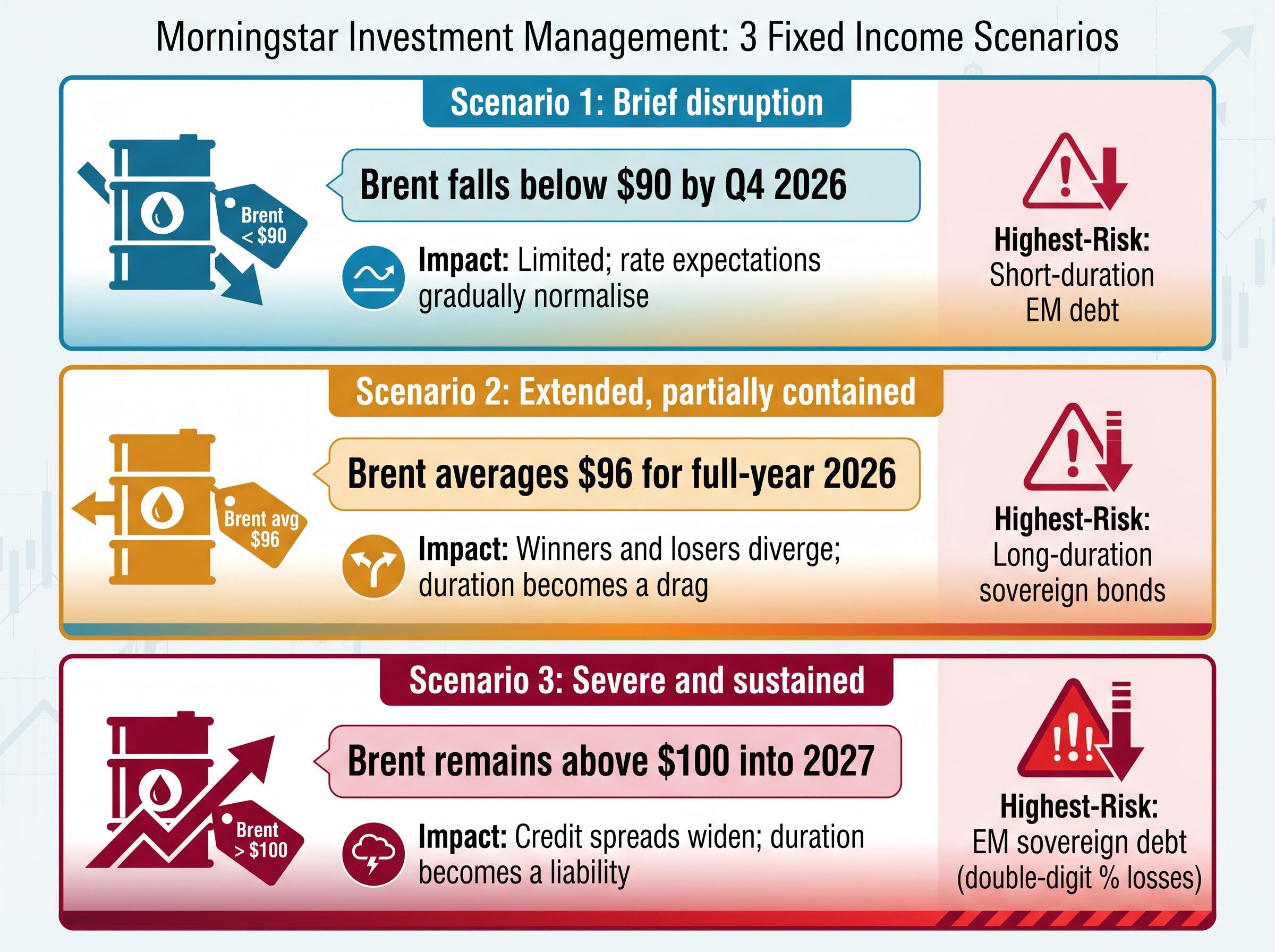

Three market scenarios and what each means for your bonds

Morningstar Investment Management published a three-scenario framework in the Morningstar Markets Observer on 1 May 2026 (authored by Zachary Evens et al.) that offers investors a structured way to stress-test their fixed income allocations without requiring them to predict the geopolitical outcome.

| Scenario | Oil Price Trajectory | Fixed Income Impact | Highest-Risk Asset Class |

|---|---|---|---|

| Brief disruption | Brent falls below $90 by Q4 2026 | Limited; rate expectations gradually normalise | Short-duration EM debt (modest volatility) |

| Extended, partially contained | Brent averages $96 for full-year 2026 | Winners and losers diverge; duration becomes a drag | Long-duration sovereign bonds |

| Severe and sustained | Brent remains above $100 into 2027 | Credit spreads widen; duration becomes a liability | EM sovereign debt (double-digit % losses) |

The severe scenario is where the consequences become acute. Morningstar’s analysis indicates emerging-market sovereign debt could face double-digit percentage losses in a sustained shock environment.

In the severe scenario, Morningstar Investment Management projects that emerging-market sovereign debt could face double-digit percentage losses, reflecting the combined pressure of currency depreciation, current account deterioration, and rising risk premiums among oil-importing economies.

The Morningstar Emerging Markets Index was already down 12.6% in March 2026 alone, while the Morningstar Developed Markets ex-US Index fell 9.9% in the same month. For context, the EM Index still delivered nearly 27% gains over the prior 12-month period, but the pace of the drawdown signals how quickly sentiment can shift.

Scenario severity maps directly to how much duration risk an investor should be comfortable holding. Investors who cannot tolerate the severe scenario’s fixed income losses need to assess that exposure now, not after the scenario materialises.

Oil importers versus exporters: why not all emerging-market bonds are equal right now

The phrase “emerging-market debt” obscures a split that the conflict has made decisive. Oil-exporting EM sovereigns and oil-importing EM sovereigns are experiencing this crisis in fundamentally different ways.

- Fiscal position: Oil exporters are seeing revenue windfalls from elevated prices, strengthening fiscal balances. Oil importers face widening deficits as energy import bills surge.

- Current account trajectory: Exporters benefit from improved trade balances. Importers face current account deterioration, currency pressure, and rising external financing costs.

- Duration risk: Exporters can absorb rate volatility with stronger fiscal buffers. Importers face compounding risk as currency weakness forces tighter domestic monetary policy, extending the duration drag.

State Street Global Advisors noted in its Q1 2026 EM Debt Commentary that the asset class is navigating elevated commodity-driven volatility with differentiated performance across these two categories. Barron’s reported that EM bond investors are selectively adding exposure to commodity exporters while reducing duration in oil-importing economies. Lombard Odier and AllianceBernstein have both published positioning analysis reinforcing this importer-exporter distinction.

How Australian investors are exposed to EM debt volatility

Australian investors hold EM sovereign debt exposure through three primary channels. ASX-listed international bond funds carry direct EM allocations that vary by mandate. Superannuation funds, particularly in balanced and growth options, commonly allocate to EM sovereign debt as part of their fixed income or alternatives sleeves. The Australian dollar itself is sensitive to global risk-off sentiment; when EM volatility spikes, AUD-denominated assets can face indirect pressure through capital flow channels.

The actionable question is not whether to hold EM bonds, but which EM sovereign exposures warrant scrutiny given the oil-importer concentration within a given fund’s holdings.

Volatility as a portfolio moment, not a portfolio emergency

Morningstar analysts have explicitly recommended in the 1 May 2026 Markets Observer that long-term investors treat geopolitically driven market volatility as a portfolio review and rebalancing opportunity, not a trigger for reactive repositioning. Historical evidence supports this: few short-term geopolitical events have caused lasting equity market damage over extended time horizons.

The distinction that matters is between short-term price volatility, which equity portfolios can absorb, and structural repricing of inflation expectations, which creates lasting fixed income consequences. Australian investors face the latter.

A three-step portfolio review framework applies:

- Assess duration exposure against a higher-for-longer rate environment. The RBA cash rate sits at 4.1% with further hikes anticipated. Portfolios calibrated for rate cuts are mispositioned.

- Review EM sovereign debt for oil-importer concentration. The exporter-importer split is not a marginal consideration; it determines whether EM fixed income is a headwind or a tailwind in the current environment.

- Compare current allocation against the December 2025 baseline that is now obsolete. The rate environment investors were planning around six months ago no longer exists.

Morningstar Investment Management describes the current volatility as a rebalancing opportunity: a moment when the information available to investors is clearer, not murkier, than it was before the conflict. The repricing has created visibility into rate paths that were previously obscured by optimistic assumptions.

What happens when the Strait reopens (and why it may not change everything)

The EIA’s projections already assume the conflict ends in April, yet still forecast Brent averaging $96 per barrel for full-year 2026 and $76 per barrel in 2027. Normalisation, even in the base case, is measured in years.

Three factors explain why a Hormuz reopening does not immediately restore the December 2025 rate environment:

- Infrastructure restoration lag. EIA Administrator Tristan Abbey has stated that full Hormuz restoration could take months post-conflict. Mine clearance, terminal recertification, and insurance recalibration all impose delays on the physical resumption of trade flows.

- Inflation CPI lag. Energy shocks run 6-12 months into headline CPI. Australian inflation at 4.6% is the starting point for that lag calculation, not the endpoint. Even if oil prices fall, the inflation already embedded in the pipeline takes quarters to dissipate.

- Central bank credibility constraints. The RBA cannot ease while inflation remains above target. Cutting rates prematurely after an inflation shock would undermine the credibility the central bank has spent the past two years rebuilding. The bar for easing has moved higher.

The May RBA meeting and what it signals

The May RBA meeting is the immediate near-term marker for Australian investors. A further hike at that meeting would confirm that the central bank is operating in a fundamentally different rate regime from the one investors were pricing in December 2025. The question is no longer when rate cuts arrive. The question is how long rates stay elevated, and whether the conflict’s inflation tail extends the timeline into 2027.

The conflict has already repriced the rate environment; investors should act accordingly

The Iran conflict has not created temporary noise in financial markets. It has structurally repriced the interest rate environment that Australian investors were planning around six months ago. The Strait of Hormuz closure, production shut-ins approaching 9.1 million b/d, and a synchronised global central bank pivot toward tightening have made the December 2025 baseline obsolete.

Morningstar Investment Management’s three-scenario framework remains a standing analytical tool. Investors do not need to predict the geopolitical outcome, but they do need to stress-test their portfolios against each scenario’s fixed income implications, particularly the severe case where EM sovereign debt faces double-digit percentage losses.

The EIA base case points to gradual oil price normalisation through 2027, but that normalisation is conditional on conflict resolution that has not yet occurred. The portfolio work of adjusting to the new rate environment cannot wait for resolution.

For Australian investors ready to translate the scenario analysis into specific allocation decisions, our dedicated guide to building an inflation portfolio strategy covers a revised framework with 40% equities, 30% bonds, 20% alternatives, and 10% cash, including specific ASX ETF selections for each sleeve and the rationale for integrating physical gold and commodity exposure as a geopolitical risk hedge.

Investors holding fixed income and EM sovereign debt exposures should review those positions in light of the analysis above and consult a financial adviser for personalised guidance on rebalancing in the current rate environment.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.