Brent crude closed above $101 per barrel on 28 April 2026, the first time oil has sustained that threshold since 2022. The Strait of Hormuz, carrying a significant share of the world’s daily seaborne oil supply, remains effectively closed to commercial tanker traffic. What began as a geopolitical event has become a direct economic transmission mechanism.

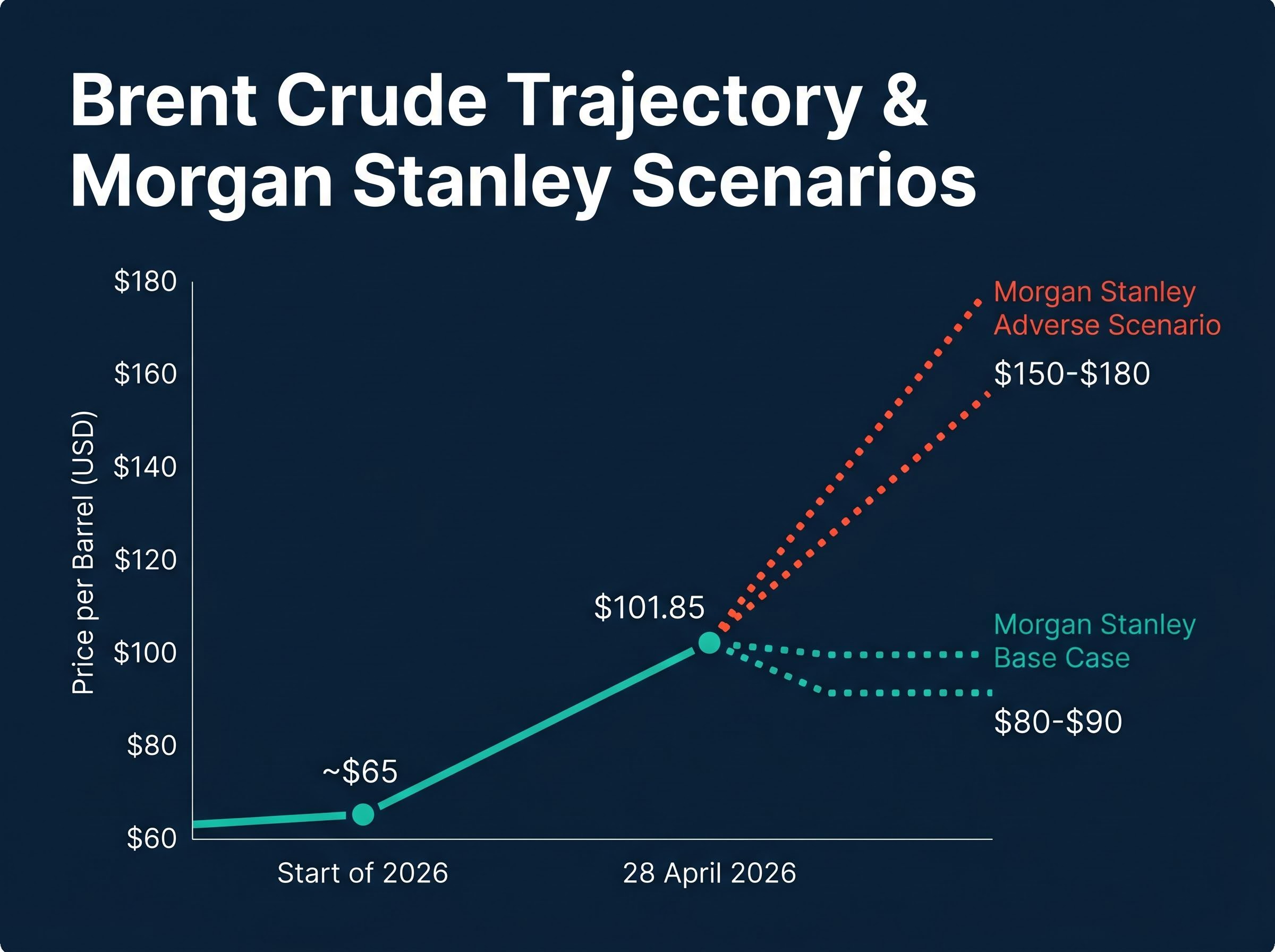

Crude started 2026 near $65 per barrel. It now sits more than 50% higher. Morgan Stanley analysts have modelled an adverse scenario where prices reach $150 to $180 per barrel if the blockage persists for several months. Mark Zandi of Moody’s Analytics has placed the 12-month U.S. recession probability at 48.6%, describing an economy where no meaningful GDP or jobs growth is expected for the rest of 2026.

What follows is an explanation of how an oil price shock of this scale transmits into a U.S. recession, what historical precedents reveal about the likely timeline, and what specific signals readers should monitor as conditions develop.

How the Strait of Hormuz closure turned a geopolitical event into an economic one

The Strait of Hormuz is a narrow waterway between Iran and Oman through which a substantial portion of globally traded crude oil passes daily. Its closure is categorically different from a pipeline outage or a single-country production cut because it removes an entire transit corridor, affecting multiple exporting nations simultaneously.

Early in the crisis, markets treated the disruption as logistical. The assumption was that tankers would reroute and that diplomatic channels would produce a resolution within weeks. That assumption collapsed as the timeline extended. Damaged port infrastructure and onshore storage limitations forced producers reliant on the Strait to reduce output, converting a transit problem into actual supply loss.

Key facts about the current disruption:

- The Strait of Hormuz remains effectively closed as of 28 April 2026, with no partial reopening reported.

- Brent crude has risen from approximately $65 per barrel at the start of 2026 to $101.85 at the close on 28 April 2026, a gain of more than 50% year to date.

- Morgan Stanley’s full-year 2026 base case projects Brent averaging $80 to $90 per barrel under favourable conditions.

- No near-term catalyst for resolution has been identified by analysts or governments.

Martijn Rats, Morgan Stanley, has outlined an adverse scenario in which Brent crude reaches $150 to $180 per barrel if the Strait remains blocked for several months.

The window for a swift resolution, the only scenario under which price increases might have proved temporary, has now passed. The disruption is no longer a headline risk. It is a structural supply deficit.

When big ASX news breaks, our subscribers know first

A 50% oil price surge in four months: what the numbers mean for American households

The barrel price matters to commodity traders. The number American households encounter is the one posted at the petrol station.

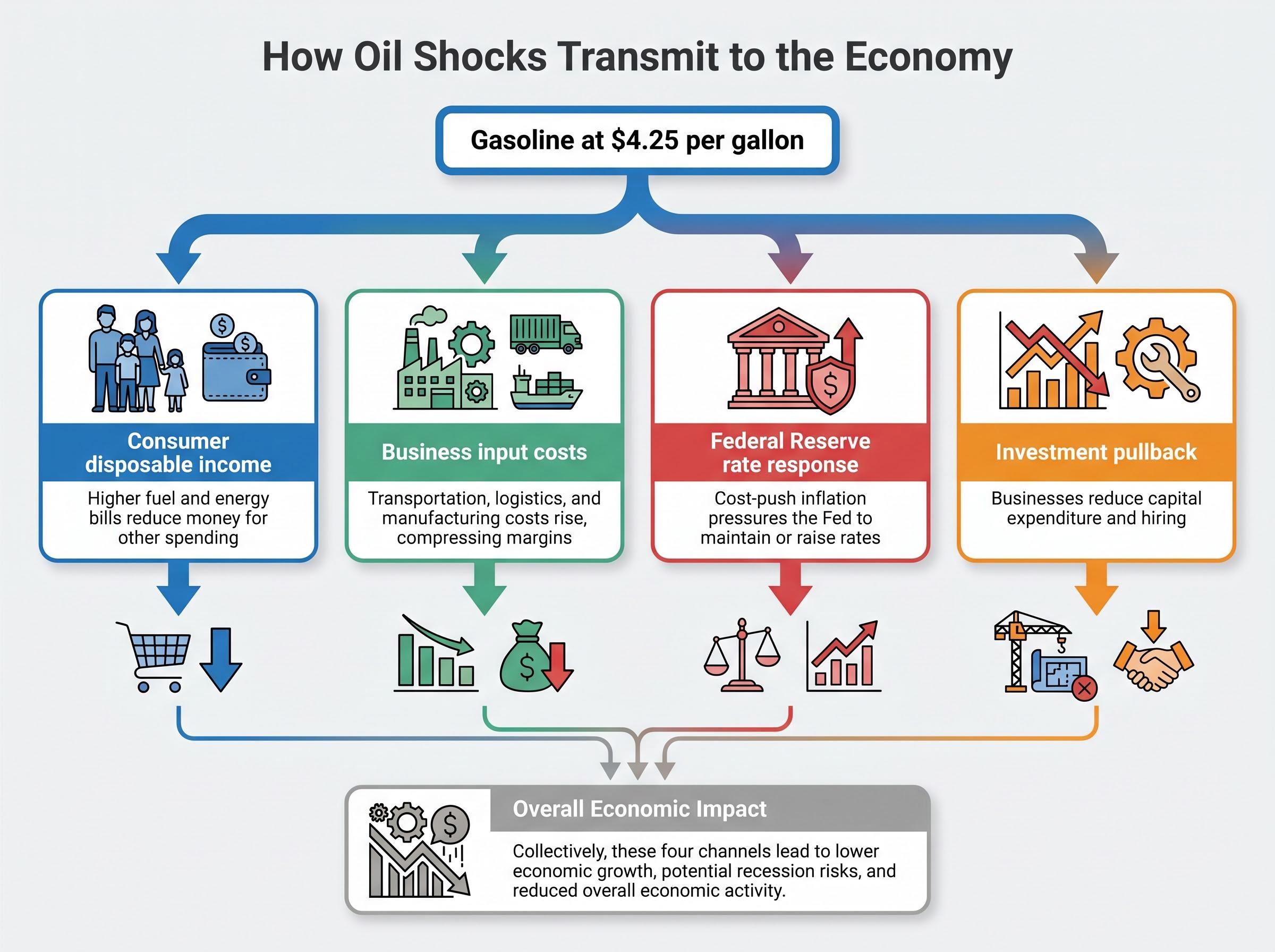

The U.S. Energy Information Administration (EIA) reported the national average gasoline price (all grades) at $4.25 per gallon for the week ending 27 April 2026. GasBuddy’s average stood at approximately $4.07 per gallon as of 28-29 April 2026. Gasoline prices have risen approximately 45% since the start of the year, tracking the crude surge with a slight lag.

The EIA weekly gasoline price data, updated each Monday, provides regional and national breakdowns that allow investors and households to track whether the current pass-through from crude prices to the pump is accelerating, stabilising, or reversing.

That $4.00-plus threshold carries historical weight. Over the past three decades (1993 to present), average U.S. gasoline prices exceeded $4.00 per gallon in only 44 weeks total, representing fewer than 3% of all weeks in the period.

Gasoline prices above $4.00 per gallon have occurred in fewer than 3% of all weeks since 1993, making the current price level a historically rare condition for U.S. consumers.

Following those 44 weeks, the S&P 500 declined by an average of 11% over the subsequent six-month window. The pattern does not guarantee a repeat, but it represents a documented statistical relationship between sustained high fuel costs and equity market deterioration.

| Period | Avg. Gasoline Price | S&P 500 (Subsequent 6 Months) |

|---|---|---|

| August 2022 peak | ~$4.00+/gallon | Declined, consistent with historical pattern |

| 2011-2012 elevated period | ~$3.80-$4.00/gallon | Mixed; market volatility elevated |

| April 2026 (current) | $4.07-$4.25/gallon | Pending; matches August 2022 peak level |

The current price level matches the most recent prior peak observed in August 2022. The difference this time is the cause: a supply disruption with no visible end date, rather than a demand-driven spike that market forces could self-correct.

Why high oil prices act as a tax on the entire economy

The transmission from barrel price to recession risk follows a chain, and each link compounds the one before it. Understanding this mechanism is what separates a temporary price inconvenience from a structural economic threat.

The process begins at the household level. When gasoline costs $4.25 per gallon instead of $2.90, the difference comes directly out of discretionary spending. Fewer restaurant meals, deferred purchases, cancelled subscriptions. Consumer spending accounts for roughly two-thirds of U.S. GDP, so when tens of millions of households simultaneously reduce spending, the aggregate effect registers in national output data.

The four transmission channels, in order of directness:

- Consumer disposable income: Higher fuel and energy bills reduce the money households have available for all other spending.

- Business input costs: Transportation, logistics, and manufacturing costs rise across supply chains, compressing margins and prompting price increases that further squeeze consumers.

- Federal Reserve rate response: Cost-push inflation pressures the Fed to maintain or raise interest rates, increasing borrowing costs for households and businesses even as economic activity slows.

- Investment pullback: Businesses facing higher costs, weaker demand, and expensive credit reduce capital expenditure and hiring plans.

The jet fuel cost transmission from crude price to consumer fare is among the fastest of any industry: Qantas reported jet refining margins surging from US$20 to approximately US$120 per barrel since February 2026, forcing domestic capacity cuts and fare increases that illustrate precisely how the business input cost channel reaches ordinary travellers.

These channels do not operate in sequence. They operate simultaneously, creating a compounding effect where each reinforces the others.

The Federal Reserve’s impossible position

The Federal Reserve faces a structural bind in an oil-driven supply shock. Cost-push inflation, prices rising because input costs have increased rather than because demand is overheating, argues for tight monetary policy. Yet tightening into a supply-driven slowdown does not resolve the underlying cause. It simply reduces demand further, potentially accelerating the contraction.

Unlike demand-driven inflation, the Fed cannot fix a supply shock by raising rates. The oil is not expensive because Americans are consuming too much of it. It is expensive because a shipping lane is closed. The only tool available to the Fed, reducing demand through higher borrowing costs, risks deepening the downturn it is trying to prevent.

This creates the stagflationary dynamic that makes oil shocks particularly dangerous: inflation and economic contraction occurring at the same time, with no clean policy response available.

Three historical oil shocks, three recessions: the pattern the data reveals

The current episode is not without precedent. Three prior oil shocks in the past half-century followed a strikingly similar sequence, and each ended in recession.

| Episode | Trigger | Oil Price Movement | Resulting Recession |

|---|---|---|---|

| 1973 Oil Embargo | Arab oil embargo (Yom Kippur War) | Prices quadrupled | 1973-1975 recession with stagflation |

| 1979 Iranian Revolution | Iranian Revolution disrupted supply | Prices approximately doubled | 1980 recession |

| 1990 Gulf War | Iraqi invasion of Kuwait | Sharp price spike | 1990-1991 recession |

In 1973, the Arab oil embargo quadrupled crude prices and produced a recession defined by stagflation, the simultaneous appearance of high inflation and stagnant growth that policymakers had previously believed could not coexist. The episode established the foundational economic understanding of oil shocks as recession catalysts.

In 1979, the Iranian Revolution approximately doubled oil prices by disrupting supply from the same geographic region now at the centre of the 2026 crisis. The parallel is direct: a political upheaval involving Iran, a supply disruption channelled through the Persian Gulf, and a Federal Reserve forced into tightening during an already weakening economy.

In 1990, the Iraqi invasion of Kuwait triggered a sharp price spike that preceded the 1990-1991 recession. While other factors contributed, the oil shock amplified existing economic vulnerabilities.

The common mechanism across all three episodes was consistent: high oil prices increased inflation, reduced consumer spending power, raised business costs, and slowed growth, often prompting Federal Reserve tightening that further suppressed economic activity.

James Hamilton, an economist at UC San Diego, has published research establishing this historical link between oil price shocks and U.S. recessions. The pattern is well documented in academic literature. The current shock fits the same structural profile.

Hamilton’s foundational research on oil price shocks and U.S. recessions, published in the Journal of Political Economy, established the empirical case that crude price disruptions of sufficient magnitude and duration reliably precede U.S. recessions — a finding that has shaped macroeconomic forecasting for four decades.

What economists are projecting for the U.S. in 2026

The range of expert projections runs from difficult to severe, with the Strait of Hormuz timeline as the determining variable.

Mark Zandi of Moody’s Analytics placed the 12-month U.S. recession probability at 48.6% as of 7 April 2026, a near coin-flip assessment that was already elevated before the most recent crude price increases pushed Brent past $101.

Mark Zandi, Moody’s Analytics, has indicated that no meaningful GDP or jobs growth is expected for 2026 and that unemployment is projected to rise, regardless of how quickly the conflict resolves.

That “damage already done” framing matters. Even a swift resolution of the Strait blockage would not reverse the inflationary pass-through, supply chain disruption, and consumer spending compression that has already occurred over four months of elevated prices. The recessionary mechanism has been engaged; the question is severity, not onset.

Morgan Stanley’s forward-looking oil price framework distinguishes between two paths:

- Base case: Brent averages $80 to $90 per barrel for full-year 2026 under favourable conditions, implying a resolution and partial demand recovery. Recession risk remains elevated but not dominant.

- Adverse scenario: Brent reaches $150 to $180 per barrel if the Strait remains blocked for several months. Under this scenario, Morgan Stanley’s own assessment is that recession probability increases substantially.

For equity investors, the S&P 500 provides its own historical anchor. The index has declined an average of 32% during recessionary periods since 1957. In the current episode, the S&P 500 fell approximately 9% from its March 2026 peak before recovering those losses, even as the underlying conflict remains unresolved. That divergence between equity prices and economic fundamentals is worth close attention.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The Strait of Hormuz timeline is now the variable every U.S. investor must track

The transmission chain is clear. A closed waterway has produced elevated crude prices, which have compressed household budgets, raised business costs, and placed the Federal Reserve in a position where its available tools risk deepening the problem. The severity of every link in that chain depends on how long the Strait of Hormuz remains blocked.

The S&P 500’s recovery from its 9% drawdown, even as the disruption persists, reveals a market pricing in a resolution that has not yet materialised. No U.S. government policy response, such as Strategic Petroleum Reserve releases, has been announced as of 28 April 2026, limiting the available cushions.

Historical precedent offers one more lesson: even after oil prices eventually fall, the recessionary damage can be well underway before the relief arrives. The feedback loop, where economic slowdown reduces energy demand and brings prices down, operates on a lag. The risk window does not close the day the headline price retreats.

Four indicators to watch as the situation develops

- Strait of Hormuz status: Any partial reopening or confirmed diplomatic progress would be the single most direct catalyst for a reduction in oil price pressure and associated recession risk.

- EIA weekly U.S. gasoline price data: Continued increases above $4.25 per gallon would signal deepening consumer spending compression; a stabilisation or decline would indicate the pass-through is peaking.

- Federal Reserve rate signals and meeting statements: Any shift toward rate cuts would suggest the Fed is prioritising growth over inflation containment; continued hawkish language would indicate the stagflationary bind is unresolved.

- Monthly U.S. employment and unemployment figures: Rising unemployment or slowing job creation would confirm the transmission mechanism is reaching the labour market, the stage that most directly precedes a formal recession determination.

These statements are speculative and subject to change based on market developments and geopolitical conditions.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.