Japan is simultaneously one of the best-performing MSCI World markets in 2026 and the subject of some of the most conspicuously negative investor commentary of the year. That divergence is the story. Over the prior six months, sentiment around Japan shifted sharply: from optimism about fiscal expansion under Prime Minister Sanae Takaichi to a cluster of anxieties around sovereign debt, yen depreciation, Bank of Japan rate hike timing, and fears that the Strait of Hormuz closure would disrupt naphtha and energy supply. The bearish narrative has become the consensus framing in financial media. This analysis examines whether that consensus is pricing in real structural risks or overfitting to headlines, drawing on Q1 2026 GDP data, IMF and OECD sovereign debt assessments, BOJ guidance, FX strategist forecasts, and commodity market reports to give readers a grounded framework for evaluating Japan’s equity market through mid-2026.

From consensus long to consensus short: how Japan sentiment flipped

By multiple measures, Japan remains among the top-performing MSCI World constituent markets year-to-date. The Financial Times reported on 2 May 2026 that Japan and Switzerland were leading developed market returns in 2026, while Reuters characterised Japan on 13 May 2026 as “among the best-performing major developed markets in 2026” in local-currency terms.

The performance makes the sentiment shift harder to explain. Approximately six months ago, investors were positioning for fiscal expansion and corporate governance reform. By May 2026, the dominant framing had rotated entirely toward sovereign debt anxiety, yen weakness, and rate hike risk.

Bank of America (9 January 2026) described Japan as having shifted from “undiscovered value” to a “consensus long,” flagging crowding and positioning reversal risk.

That framing itself telegraphed the fragility. When a trade becomes consensus, it takes less to trigger the unwind. The specific bearish concerns now dominating headlines include:

- Sovereign debt sustainability and fiscal trajectory

- Yen depreciation and the risk of further weakness

- BOJ rate hike timing and its effect on equity multiples

- Strait of Hormuz energy and naphtha supply disruption

Each of these has a specific evidence base. The question is whether the evidence supports the severity of the sentiment shift, or whether the narrative has run ahead of the data.

When big ASX news breaks, our subscribers know first

What Japan’s Q1 2026 GDP data actually shows about the economy

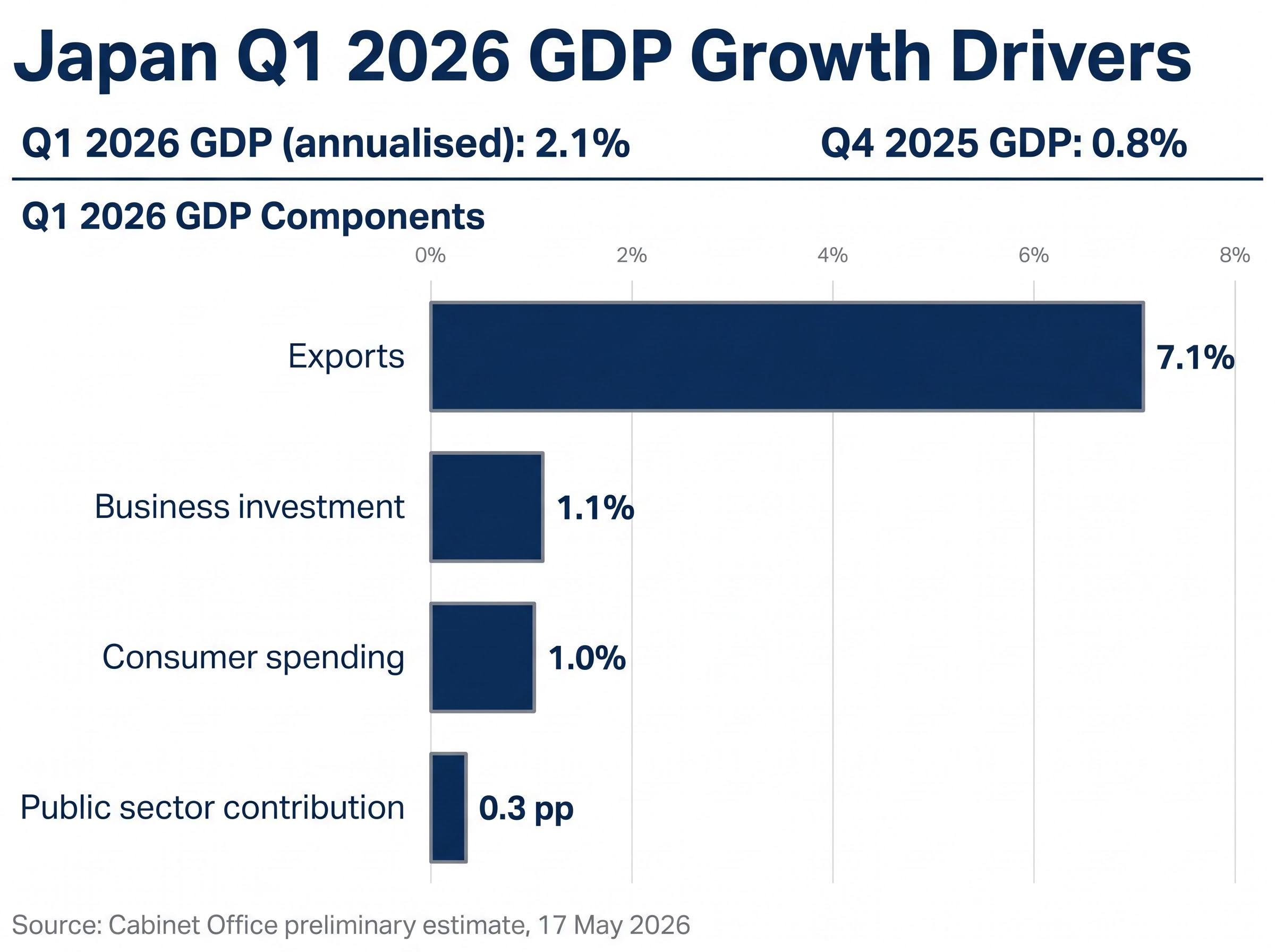

The Cabinet Office’s preliminary estimate, published 17 May 2026, put annualised real GDP growth at 2.1% in Q1 2026, up from 0.8% annualised in Q4 2025. The headline number matters less than what drove it.

Consumer spending expanded 1.0% in Q1 2026, following a flat Q4 2025 reading. Business investment rose 1.1% annualised. Export volumes surged 7.1%. The public sector’s contribution was just 0.3 percentage points of the 2.1% total.

Japan’s Q1 2026 performance sits within a broader pattern of global GDP divergence in 2026, where the UK beat consensus expectations, the eurozone posted near-stagnant growth at 0.1% quarter-on-quarter, and China’s demand recovery remained unconfirmed; understanding those cross-economy dynamics matters because Japan’s export surge partly reflects trade re-routing and demand shifts across the same diverging blocs.

| Component | Q4 2025 | Q1 2026 |

|---|---|---|

| GDP (annualised) | 0.8% | 2.1% |

| Consumer spending | 0.0% (flat) | 1.0% |

| Business investment (annualised) | — | 1.1% |

| Exports | — | 7.1% |

| Public sector contribution | — | 0.3 pp |

Private domestic demand contributed roughly double the public sector’s share. That composition matters. An expansion driven by private consumption and business investment is structurally more durable than one sustained by government transfers.

Goldman Sachs, in a 9 May 2026 note, concluded that domestic demand was strong enough to support mid-single-digit earnings growth even if global trade softens. The GDP data supports that reading: the private sector is doing this itself.

Understanding Japan’s sovereign debt risk: what institutions actually say

Sovereign debt is the most frequently cited structural bear case for Japan. The debt level is the highest among advanced economies. That much is not disputed. What the institutional assessments actually say about the risk, however, is materially different from how the bearish commentary frames it.

The three institutions investors most defer to on sovereign credit each published assessments in April and May 2026:

The institutional framing around sovereign debt sustainability thresholds matters more than the raw ratio: academic research places meaningful fiscal stress above 140% of GDP, and Japan’s experience sustaining debt above 200% since 2020 through domestic bond ownership, yield curve management, and deep savings pools illustrates how structural conditions can make headline ratios a poor predictor of market crisis.

- IMF (2 April 2026, Article IV Consultation): Debt “sustainable under the baseline” with very low effective interest costs, a strong domestic investor base, and BOJ JGB holdings as mitigating factors. Recommends a credible medium-term consolidation plan but frames no imminent crisis.

- OECD (15 May 2026, Economic Outlook): Debt manageable in the near term. Calls for gradual fiscal normalisation rather than urgent consolidation. Views domestic demand as the main growth driver.

- Moody’s (30 April 2026, Credit Opinion): A1 rating, stable outlook. High debt mitigated by large domestic savings, deep local capital market, and BOJ support. Sustainable but vulnerable to growth and funding cost shocks.

The IMF’s framing is worth isolating: Japan’s debt is “sustainable under the baseline,” with risk scenarios tied to unexpectedly high rates, weaker growth, and reduced domestic savings absorption. That is a materially different statement from the market commentary suggesting an imminent fiscal reckoning.

The institutions are clear-eyed about the conditions under which the risk would materialise. They are equally clear that those conditions have not arrived.

How BOJ policy fits into the debt picture

The BOJ’s April 2026 Outlook stated it would “patiently continue monetary easing” while adjusting only if the price stability target is sustainably achieved. Markets have interpreted this as a signal of very gradual normalisation.

The BOJ Outlook for Economic Activity and Prices sets out the conditions under which the central bank would adjust its policy stance, specifically tying further normalisation to sustained achievement of the price stability target rather than a fixed calendar schedule.

Nomura expects one or two modest rate increases over the next 12 months, keeping policy accommodative to avoid destabilising JGB markets. Goldman Sachs sees the BOJ moving cautiously toward neutral by late 2027, with hikes remaining data-dependent.

Real rates are expected to remain negative even after further normalisation. As Nikkei Asia reported on 10 May 2026, buy-side analysts argue that negative real rates continue to support equities. The refinancing cost shock that bears cite as the trigger for a debt spiral requires a rate path materially steeper than any major forecaster currently expects.

The naphtha panic: separating supply chain noise from investment signal

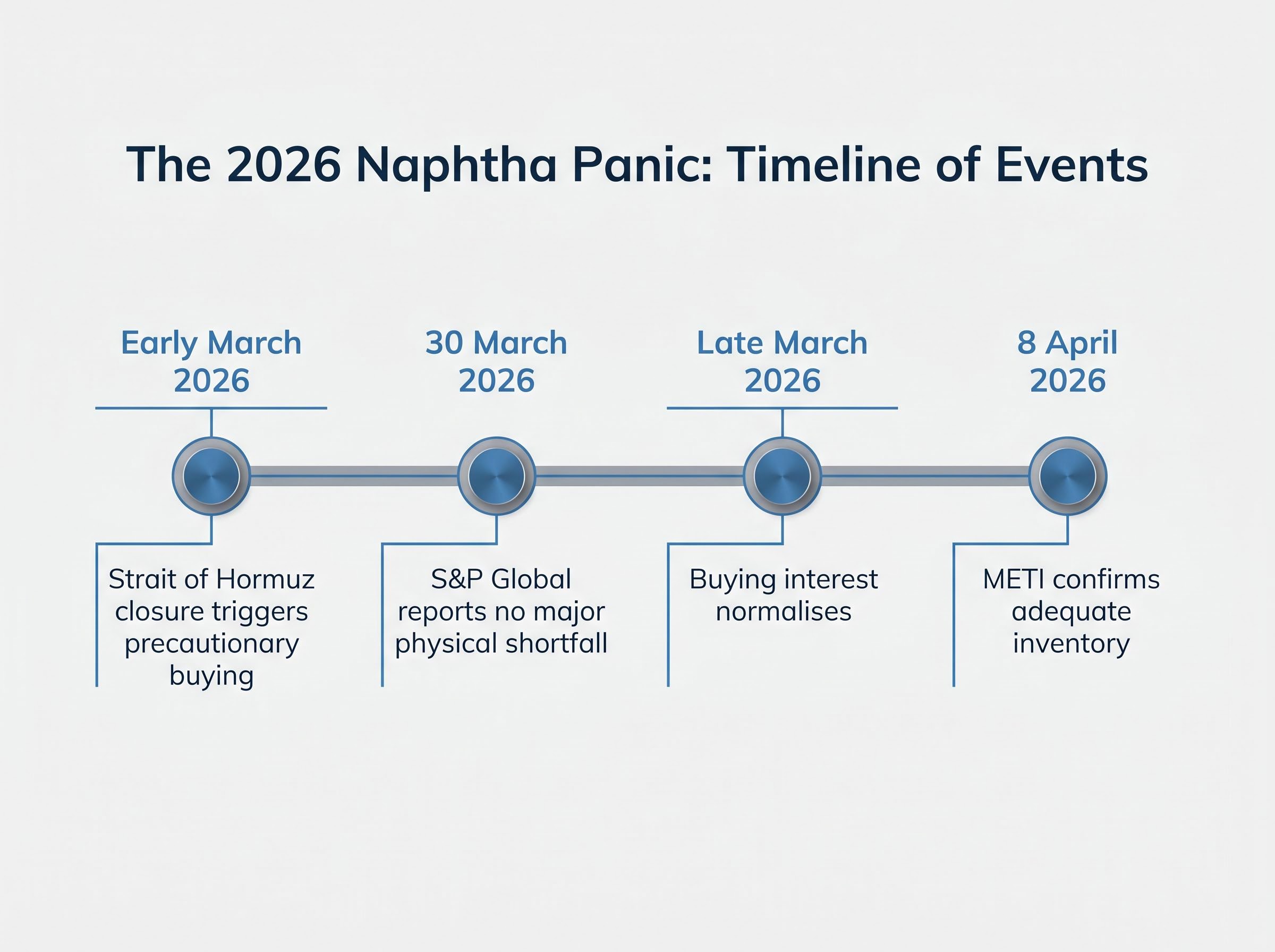

The Strait of Hormuz closure triggered precautionary buying by Japanese petrochemical buyers in early March 2026. Spot naphtha prices spiked. Financial media coverage amplified the disruption narrative.

The sequence of what actually happened tells a different story:

- The Hormuz closure prompted precautionary purchasing by Japanese petrochemical firms, pushing spot naphtha prices higher.

- Spot prices spiked as buyers scrambled to secure supply ahead of anticipated shortfalls.

- Physical markets were assessed: S&P Global Commodity Insights reported on 30 March 2026 that there had been “no major physical shortfall in Japanese naphtha imports so far.”

- By late March, buying interest normalised as supply disruption fears eased.

- METI confirmed on 8 April 2026 that naphtha imports continued, inventory levels were adequate, and the spot price increase was attributed to “precautionary purchasing” rather than physical shortage. A follow-up on 23 April 2026 confirmed no material disruption, with refineries and petrochemical plants operating normally.

S&P Global Commodity Insights (30 March 2026): “No major physical shortfall in Japanese naphtha imports so far.”

Nikkei Asia reported on 18 April 2026 that naphtha shortage fears had more to do with market psychology than physical scarcity. Nuclear restarts and eased restrictions on coal-fired generation added domestic energy capacity as contingency.

The investment-relevant implication is specific: when a bearish thesis depends on a supply disruption that has already been absorbed and reversed, the risk premium attached to that thesis becomes orphaned. By the time energy fears reached peak media coverage, the physical market had already moved past them.

The Hormuz closure macro risk carries a transmission lag of approximately four quarters before appearing in GDP data, which means the physical resolution of Japan’s naphtha supply concerns does not fully neutralise the macro tail risk: institutional recession probability estimates range from 20% to 70% depending on the scenario, and BCA Research has flagged June 2026 as the point where inventory depletion and futures market repricing converge.

The legitimate bearish case and why it is not the same as a crisis thesis

The institutional cautious views on Japan are coherent. They deserve engagement on their own terms.

| Institution | Primary Concern | Investment Implication |

|---|---|---|

| Morgan Stanley (22 April 2026) | Valuation stretch in cyclical and AI-related exporters; yen rebound risk compressing exporter earnings | Recommends selectivity, not exit |

| UBS (5 March 2026) | Margin reversion if wage growth exceeds productivity; BOJ tightening repricing JGB yields | Rotate toward defensive, domestically oriented stocks |

| HSBC (19 February 2026) | Demographic decline and high debt limit long-term growth potential; ROE gains may stall without deeper governance reform | Questions durability of re-rating story |

| BlackRock (15 April 2026) | Good news “largely priced in”; global risk appetite shifts could drive volatility given high foreign ownership | Future returns likely more modest even if structural improvements continue |

These are arguments that future returns from Japan will be more modest. They are not arguments that the economy or market faces an imminent structural break. The distinction matters for portfolio positioning: Morgan Stanley recommends selectivity, not exit. UBS advises sector rotation, not liquidation.

What the yen trajectory actually implies

J.P. Morgan and Morgan Stanley both forecast gradual yen appreciation rather than a disorderly rebound. The Financial Times reported on 1 May 2026 that fears of a yen “freefall” had materially receded, with asset managers noting undervaluation but reduced extreme pessimism.

Bloomberg reported on 6 May 2026 that FX strategists emphasise stabilisation as the base case, with the wide US-Japan rate differential still limiting the pace of yen recovery. A gradually stronger yen is a headwind for exporters but a tailwind for domestically oriented sectors. The implication is sector rotation risk, not market-wide collapse.

The BOJ’s cautious rate path and the MoF’s intervention activity are not independent variables; the IMF episode limits on yen intervention impose a structural ceiling on how aggressively Japan can defend exchange rate levels before its free-floating classification comes under review, which in turn affects sovereign borrowing costs and the credibility the IMF assessment of debt sustainability implicitly assumes.

The next major ASX story will hit our subscribers first

Japan’s market signal and what the sentiment gap means for positioning

The analytical threads converge on a specific conclusion: Japan’s Q1 2026 GDP composition, institutional debt assessments, resolved naphtha fears, and cautious-but-not-crisis institutional views collectively suggest the bearish narrative has overshot the evidence.

Japan was approaching pre-conflict highs as of mid-May 2026, according to Fisher Investments editorial analysis. Nomura Research characterised the expansion on 13 May 2026 as “increasingly self-sustaining,” citing broad-based wage increases and inbound tourism as stabilisers.

Nomura Research (13 May 2026): The expansion is “increasingly self-sustaining,” with broad-based wage increases and strong inbound tourism acting as stabilisers for domestic demand.

Real wages are improving versus 2025 as inflation moderates, according to MHLW data from April 2026. Major firms granted robust base-pay increases in the 2026 shunto negotiations, as Reuters reported on 12 March 2026. The OECD expects domestic demand to remain the main growth driver, with gradual fiscal withdrawal feasible if structural reforms proceed.

The prior episode confirms the pattern. Fisher Investments’ November 2025 assessment that Q3 2025 GDP pessimism was excessive was subsequently validated by the Q1 2026 expansion data. Sentiment gaps of this nature, where performance diverges from the prevailing narrative, have historically been significant for patient investors.

The specific question investors should be asking is not whether Japan has risks. It does. The question is whether the identifiable risks (valuation stretch, gradual yen strengthening, modest rate normalisation) are already priced into current valuations, or whether they represent genuinely unpriced tail risk. A three-part diagnostic helps frame that assessment:

- Is the risk new information, or is it already known and reflected in positioning?

- Has the physical or economic outcome the risk implies actually materialised?

- Does the institutional consensus frame the risk as a crisis, or as second-derivative moderation of returns?

Applied to each of the bearish concerns dominating Japan commentary in 2026, the answers consistently point toward the latter.

Japan’s fundamentals have not caught up with the headlines; the headlines have run ahead of the fundamentals

The gap between Japan’s 2026 market performance and the prevailing bearish narrative reflects sentiment drift, not economic deterioration. Q1 2026 GDP composition shows a private-sector-led expansion. Three major institutions frame sovereign debt as sustainable under baseline conditions. The naphtha supply disruption resolved before peak media coverage arrived. Institutional caution centres on valuation moderation and sector rotation, not structural economic breakdown.

The legitimate structural considerations, demographics, the long-run debt path, gradual yen appreciation, and valuation compression, remain real. They warrant monitoring, not panic. Investors who distinguish between identifiable, partially priced-in risks and the crisis-level macro scenarios implied by the most pessimistic commentary are better positioned to evaluate Japan’s equity market on the evidence rather than the narrative.

Tracking BOJ rate guidance, real wage data, and naphtha market conditions offers a more granular early-warning system than headline sentiment.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.