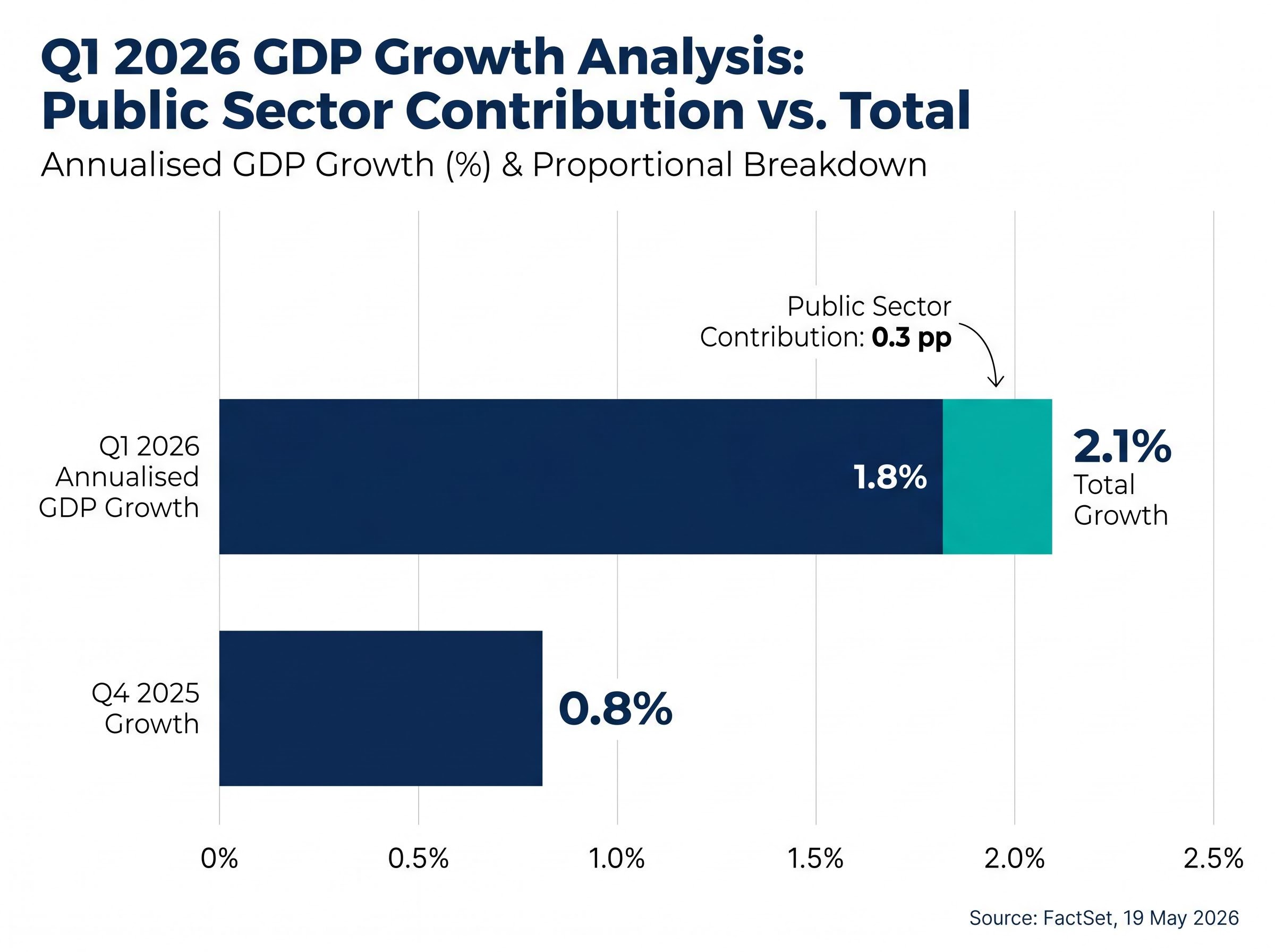

Japan’s economy expanded at an annualised rate of 2.1% in the first quarter of 2026, comfortably beating consensus expectations. The headline number, released by Japan’s Cabinet Office on 19 May 2026, tells a story of acceleration from the 0.8% annualised pace recorded in Q4 2025. But the more revealing detail sits beneath the surface: government spending contributed just 0.3 percentage points of that 2.1% print. The private sector, not fiscal stimulus, generated the momentum. This analysis unpacks what drove the Q1 expansion at the component level, explains why the private-sector share of growth carries more analytical weight than the headline rate, and assesses whether a forthcoming summer stimulus package would add genuine economic thrust or simply front-load demand that was already materialising on its own.

Q1 2026’s growth composition reveals an economy driven by private demand, not public spending

The headline figures from the Cabinet Office release deserve a clean read before the interpretation begins:

- Q1 2026 GDP growth: 0.5% quarter-on-quarter, 2.1% annualised

- Q4 2025 comparison: 0.8% annualised

- Public sector contribution: 0.3 percentage points of the 2.1% annualised figure

That last data point, sourced from FactSet on 19 May 2026, reframes the entire release. A 2.1% annualised print sounds like a strong quarter. A 2.1% print where government activity accounted for barely one-seventh of the total sounds like a structurally different kind of quarter.

The release arrived against a backdrop of genuine pressure: the Strait of Hormuz closure had been disrupting energy supply chains since late February, sovereign debt concerns were intensifying, and the yen’s trajectory remained a source of market anxiety. Against that context, the question worth answering is not whether Japan grew, but who drove the growth. The composition suggests the private sector did the heavy lifting while the government barely showed up.

When big ASX news breaks, our subscribers know first

Inside the numbers: how each demand component performed

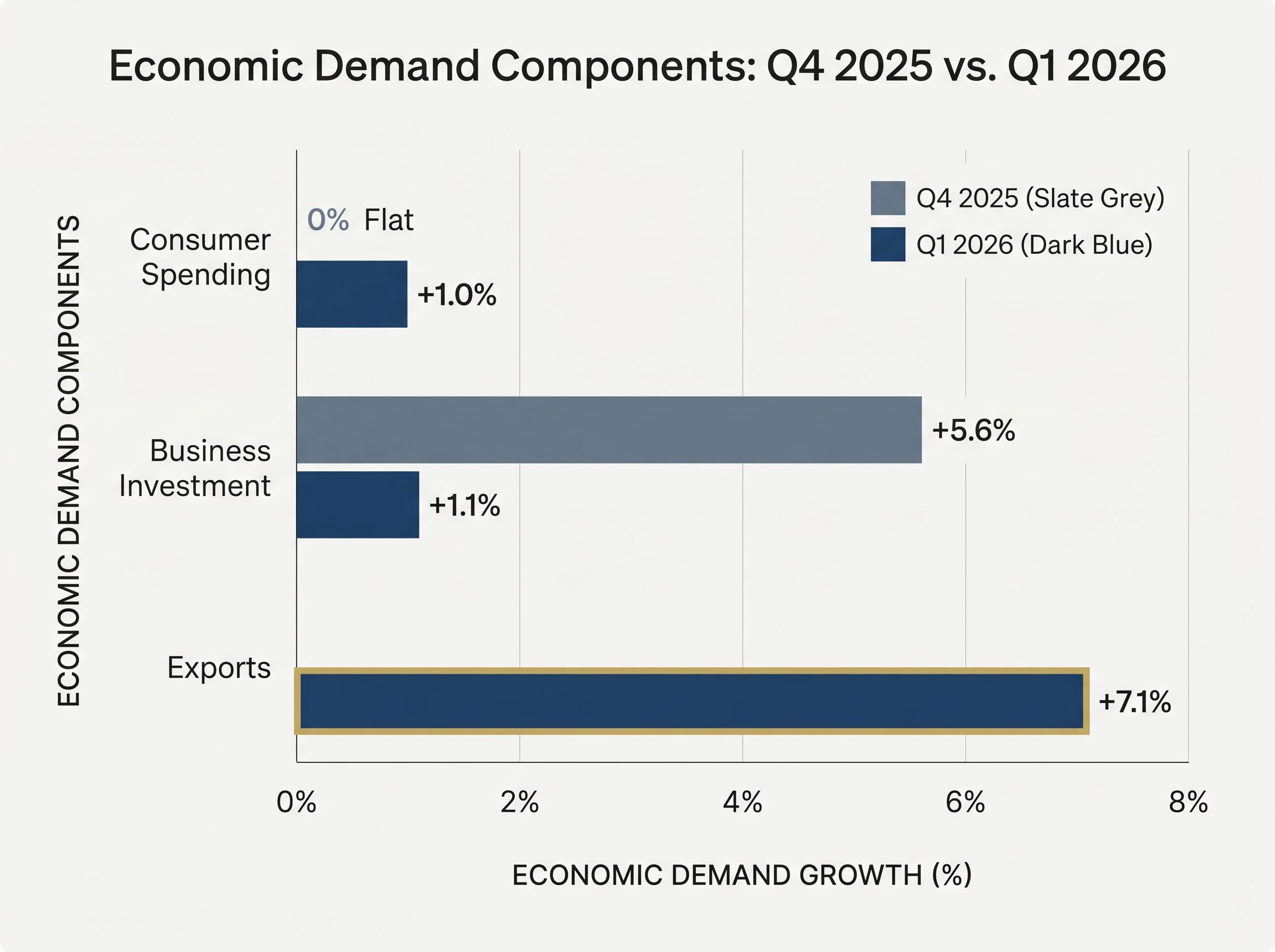

Consumer spending rose +1.0% in Q1 2026, a notable shift from the flat reading recorded in Q4 2025. That quarterly improvement, however, sits in tension with the most recent monthly data: household consumption expenditures fell -2.9% as of March 2026, according to the Statistics Bureau of Japan. Whether the monthly weakness represents a temporary pullback within a positive quarterly trend or an early signal of fading momentum is a question the Q2 data will need to resolve.

The following table summarises the demand-side breakdown, with component figures cited via FactSet on 19 May 2026. Full Cabinet Office table confirmation remains pending.

| Demand Component | Q4 2025 | Q1 2026 | Direction | Notes |

|---|---|---|---|---|

| Consumer Spending | Flat | +1.0% | Improving | Monthly data (March) shows -2.9% decline |

| Exports | N/A | +7.1% | Strong | Standout component of the release |

| Business Investment | +5.6% annualised | +1.1% | Decelerating | Sharp slowdown from prior quarter |

| Residential Construction | Recovery phase | Continued recovery | Improving | Ongoing rebound after Q3 2025 building code disruption |

+7.1% export growth was the single strongest component in the Q1 2026 release, making net trade the primary engine of headline GDP acceleration.

Business investment decelerated sharply, from +5.6% annualised in Q4 2025 to just +1.1% in Q1 2026. That divergence between surging exports and slowing capital expenditure raises a legitimate durability question: if global trade conditions shift, particularly given ongoing Hormuz-related supply chain disruption, the export pillar supporting the headline number could soften without a compensating pickup in domestic investment.

Why the 0.3-percentage-point public sector share is the most significant number in the release

Government activity contributed 0.3 percentage points of the 2.1% annualised GDP growth in Q1 2026. Private domestic demand, which in Japan’s national accounts framework encompasses household consumption, business investment, and residential construction (excluding net trade and government expenditure), contributed roughly double that share, according to FactSet data published on 19 May 2026.

That split is analytically meaningful because it occurred in the absence of a large supplementary budget providing household or business subsidies. No major fiscal injection was in play during Q1. The private sector self-generated momentum.

Three supporting indicators reinforce the picture of an economy where household income and employment stability enabled organic consumption growth:

- Unemployment rate: 2.7% as of March 2026 (Statistics Bureau of Japan), indicating a tight labour market

- Consumer Price Index: +1.5% year-on-year in March 2026 (Statistics Bureau of Japan), suggesting inflation was present but not at levels that would severely erode purchasing power

- Real household income: Average decline of -0.9% across 2025, a headwind that persisted into Q1 but did not prevent the consumption pickup

An economy where private demand carries the growth burden is structurally more resilient than one dependent on government spending cycles. For global investors modelling earnings growth and expansion durability, that distinction is material. When the government steps back and growth continues, the signal is different from when the government steps in and growth appears.

Understanding Japan’s national accounts: why GDP composition matters more than the headline rate

Gross domestic product, measured by the expenditure approach, is the sum of four broad categories of spending in an economy:

- Consumption (C): Household spending on goods and services, the largest single component in most developed economies

- Investment (I): Business capital expenditure and residential construction, reflecting private-sector confidence in future demand

- Government spending (G): Public-sector expenditure on goods, services, and infrastructure

- Net exports (NX): The value of exports minus imports, capturing the contribution of trade to overall output

A single GDP growth figure, such as Japan’s 2.1% annualised Q1 2026 print, compresses all four categories into one number. That compression is useful for comparison but masks the composition. The same 2.1% headline could result from very different internal mixes, and those mixes carry very different implications for durability.

What Japan’s Q1 mix tells us about economic resilience

Consider two versions of a 2.1% growth rate. In the first, government spending drives the majority of the expansion while household consumption and business investment are flat or negative. That profile suggests the economy needs fiscal support to function, and growth may fade when the spending programme ends. In the second, government spending contributes modestly while consumption, investment, and exports each contribute positively. That profile suggests underlying economic activity is self-sustaining.

Japan’s Q1 2026 data fits the second profile. Public sector activity contributed just 0.3 percentage points. Consumer spending, business investment, and exports all posted positive readings. This is consistent with the pattern that Fisher Investments’ November 2025 analysis identified when it argued that the Q3 2025 GDP contraction was a one-time distortion caused by new building code effects on residential investment, not a signal of underlying weakness. The Q1 2026 private-sector rebound supports that reading.

What the summer stimulus package would and would not do for Japan’s economy

Reuters reported on 18 May 2026 that the Japanese government is actively planning a supplementary budget for summer 2026, including energy subsidies and fresh debt issuance, motivated by the economic impact of the Middle East conflict. The package addresses a real vulnerability: the Strait of Hormuz closure has pressured energy import costs, and households entered 2026 after a year in which real incomes declined by -0.9% on average.

The question is whether stimulus directed at an economy already generating private-sector growth adds meaningful incremental momentum, or whether it primarily pulls forward demand that was already materialising.

Japan’s history with supplementary budgets offers a pattern. Prior stimulus programmes have tended to produce short-term demand acceleration followed by a corresponding softening once the fiscal impulse fades. When elevated expectations are already factored into asset pricing, the eventual outcomes have tended to disappoint relative to the initial political framing.

Applied to the current context, two scenarios follow logically:

- The stimulus adds marginal short-term support in an economy already growing organically, cushioning the energy cost shock without meaningfully lifting the growth trajectory above where private demand was already taking it.

- The stimulus pulls forward consumption and investment activity that was already materialising, creating a flattering but temporary Q2-Q3 boost followed by a payback period.

The OECD’s Japan Economic Snapshot frames fiscal consolidation and a credible medium-term fiscal framework as ongoing priorities, given Japan’s elevated public debt levels. Additional stimulus carries a structural cost that extends beyond its near-term GDP contribution.

Investors who price in a large stimulus-driven acceleration may be overestimating the marginal GDP impact. The Q1 data suggests the growth engine is already running; adding government fuel may generate less incremental thrust than the political framing of the package implies.

The next major ASX story will hit our subscribers first

Japan’s economic performance in 2026 has outpaced what the pessimistic consensus anticipated

Six months ago, global investor sentiment toward Japan was notably more optimistic. Markets anticipated fiscal expansion under Prime Minister Sanae Takaichi, and the economy appeared positioned to benefit from structural reforms. By May 2026, the narrative had shifted considerably. Concerns about sovereign debt sustainability, yen depreciation risk, and the potential for Bank of Japan rate adjustments had hardened into a broadly cautious consensus.

The Q1 data complicates that pessimism. According to MSCI World index data referenced by Fisher Investments, Japan was among the top-performing countries in the index on a year-to-date basis as of 19 May 2026, and the stock market was approaching pre-conflict highs.

Japan’s stock market approaching pre-Hormuz-crisis highs while mainstream commentary warned of impending economic disruption represents a gap between sentiment and underlying performance that is itself analytically significant.

The energy vulnerability, often cited as the primary risk factor, also warrants a more granular assessment. Japan has deployed an active supply-side response toolkit since the Strait of Hormuz closure commenced on 28 February 2026. Reported measures include:

- Strategic petroleum reserve drawdowns

- Azerbaijani crude shipments as replacement supply

- TEPCO nuclear restarts

- Coal generation waivers

These specific measures, attributed to Fisher Investments editorial staff, are consistent with Japan’s established energy-security policy infrastructure, though primary-source confirmation for each as a 2026 Hormuz-specific response requires additional sourcing.

When market sentiment diverges materially from underlying economic data, that gap is a signal. A pessimism premium that exceeds what the fundamentals justify creates a different risk-reward profile than one grounded in deteriorating conditions. Q1 2026 data suggests Japan’s underlying conditions have not deteriorated to the degree the cautious consensus implies.

Private demand has earned the lead role in Japan’s economic narrative

The Q1 2026 GDP release tells a story that is more structurally interesting than the headline 2.1% figure conveys. Japan’s private sector generated growth independently of government stimulus, a pattern that marks a meaningful shift from prior cycles where fiscal spending was the dominant driver. If that pattern holds, it changes how the current expansion should be modelled.

Three specific data releases will determine whether it holds:

- Q2 2026 GDP: Whether private domestic demand maintains its share of total growth, or whether the summer stimulus package artificially inflates the government contribution

- Monthly consumption expenditure trend through Q2: Whether the -2.9% March reading was an outlier within a positive quarterly trajectory or the beginning of a genuine consumer pullback

- Wage growth confirmation: Whether nominal and real wage gains are sufficient to sustain the consumption recovery that Q1’s quarterly data implies

The monthly consumption weakness and the -0.9% real household income decline across 2025 are genuine risk factors, not dismissible noise. They represent the tension at the centre of the Japan growth story: an economy generating momentum from private activity while the household income backdrop remains fragile. The next two quarters of data will determine which side of that tension prevails.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections and forward-looking assessments are subject to market conditions and various risk factors.