Two Undervalued Dividend Kings at 15-Year Lows: the Return Math

54 mins ago

On 30 April 2026, South32 disclosed a 50% capital cost increase and a 12-month production delay at its Hermosa Taylor zinc-manganese project in Arizona. The company’s shares fell 5.4% the same day. Three brokers cut their price targets within 24 hours.

Mining capital cost overruns are not rare events. By the available evidence, they are the norm. What makes the Hermosa announcement analytically useful is that it is unusually well documented, large enough to move institutional sentiment, and recent enough to serve as a live case study in how the market reprices risk when a flagship development project misses its own estimates. This article uses Hermosa as an anchor case to examine how overruns happen, how analysts translate project revisions into price target cuts, what the pattern looks like across the broader industry, and what Australian investors should watch for when a mining company in their portfolio announces a capex revision.

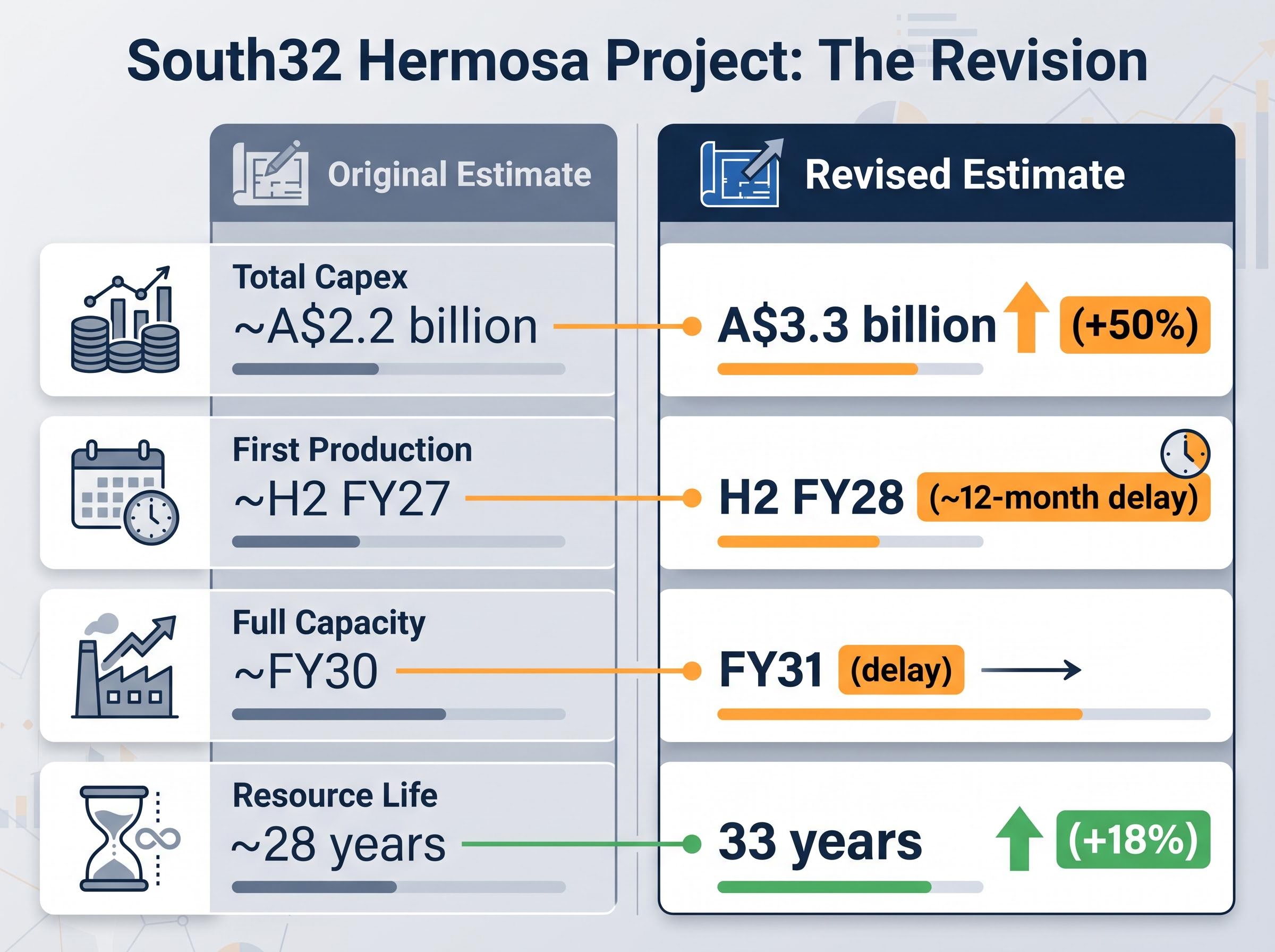

South32 presented the revision in stark terms. The total capital budget for Hermosa Taylor now sits at A$3.3 billion, up approximately 50% from the prior estimate. First production has been pushed to the second half of FY28, roughly 12 months later than previously guided, with full nameplate capacity now expected in FY31.

The company paired the negative update with a partial offset: an 18% resource life extension, taking the project’s productive lifespan to 33 years. Management cited labour costs and engineering revisions within the Arizona permitting environment as the primary drivers.

The extension is meaningful. It does not, however, change the near-term arithmetic. Macquarie observed that Hermosa’s inflection point as a net contributor to the South32 group has shifted approximately 24 months and is now expected around FY30, after roughly five years of net investment. For that entire period, the project absorbs capital rather than generating it.

| Metric | Original estimate | Revised estimate | Change |

|---|---|---|---|

| Total capex | ~A$2.2 billion | A$3.3 billion | +50% |

| First production | ~H2 FY27 | H2 FY28 | ~12-month delay |

| Full capacity | ~FY30 | FY31 | Deferred |

| Resource life | ~28 years | 33 years | +18% |

A 50% capex blowout on a project of this size does not just affect near-term earnings. It alters the net present value (NPV) calculus, the estimated value of all future cash flows adjusted back to today, pushes cash breakeven further out, and changes the risk profile of the stock for years.

Broker price targets for mining development stocks are substantially driven by NPV models, where project timing and capital intensity are the two most sensitive inputs. When both move adversely at once, the mathematical impact on the target price is multiplicative, not additive. A project that costs more and takes longer to reach production delivers a smaller present value of future cash flows, and the target price drops accordingly.

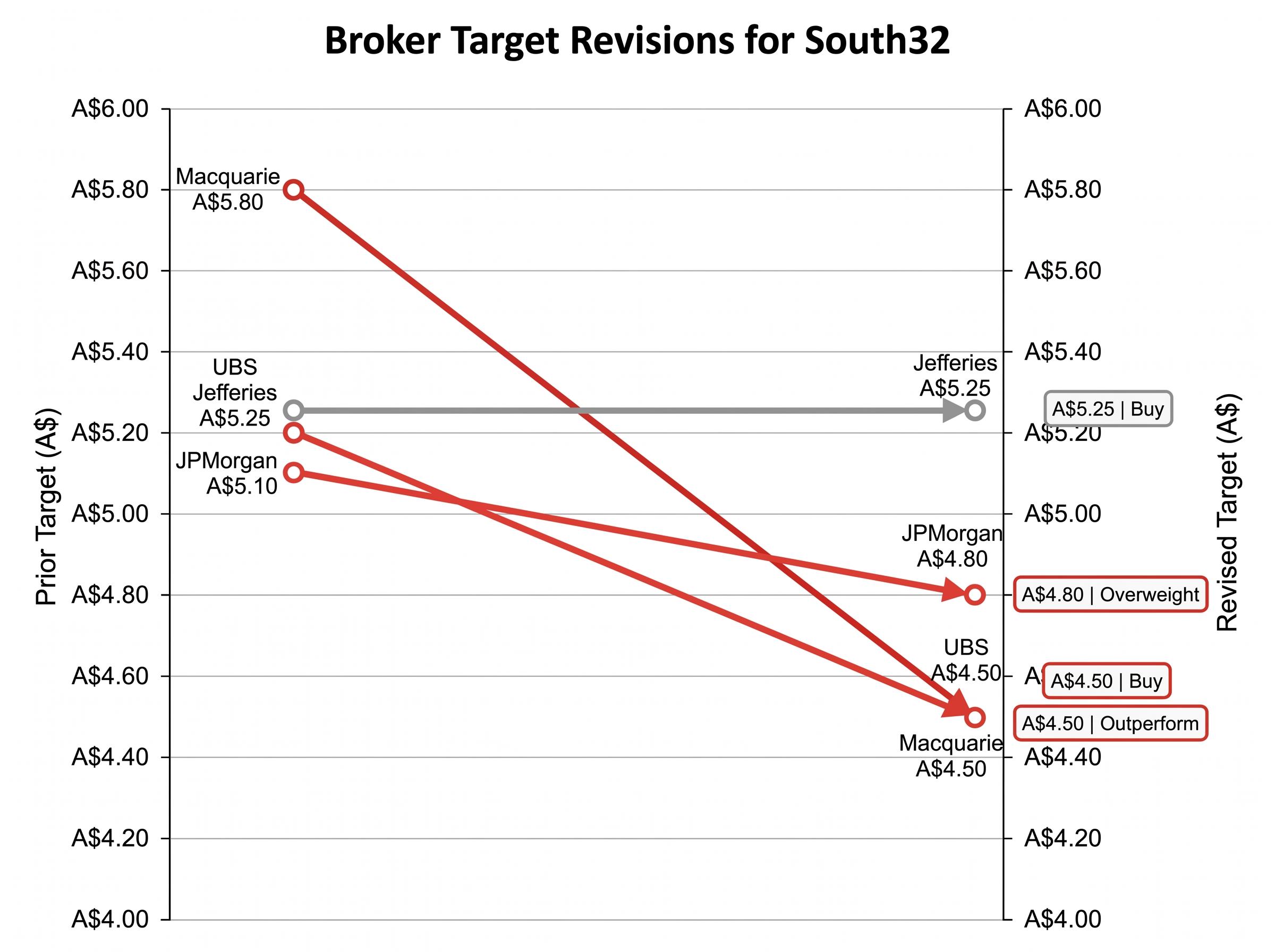

The broker responses to Hermosa illustrate this clearly. Macquarie cut its target to A$4.50 from A$5.80, a 22% reduction, and reduced group earnings estimates by 18% for both FY28 and FY29, and 9% for FY30. JPMorgan cut to A$4.80 from A$5.10. UBS cut to A$4.50 from A$5.20. Jefferies held at A$5.25 with no revision.

| Broker | Prior target | Revised target | Rating | Earnings revision |

|---|---|---|---|---|

| Macquarie | A$5.80 | A$4.50 | Outperform (retained) | -18% FY28/FY29; -9% FY30 |

| JPMorgan | A$5.10 | A$4.80 | Overweight (retained) | Not disclosed |

| UBS | A$5.20 | A$4.50 | Buy (retained) | Not disclosed |

| Jefferies | A$5.25 | A$5.25 | Buy (retained) | No change |

Macquarie noted that Hermosa’s inflection point as a net contributor to the group has shifted approximately 24 months, with the project now expected to begin generating returns around FY30 after roughly five years of sustained investment.

All four brokers retained positive ratings despite the target cuts. That distinction matters for retail investors. A project setback is not the same as a project failure. The maintained buy ratings signal that analysts still view the underlying asset as viable and the company as retaining long-term value. What has narrowed is the margin of safety between the current share price and the revised assessment of what the company is worth.

Hermosa’s 50% overrun is large. It is not, however, unusual. Wood Mackenzie’s Metals and Mining 2026 Outlook estimates that overruns of 40-50% are typical for critical minerals projects. By that benchmark, Hermosa sits within the documented range rather than above it.

The structural drivers are well understood and tend to compound during execution:

Directional context from other large projects supports the pattern. BHP’s Jansen potash project in Canada saw its cost estimate approximately double from roughly US$5 billion on a Stage 1 basis across both stages. Liontown Resources’ Kathleen Valley lithium project exceeded its original A$500 million budget by a material margin, though precise verified figures vary across reporting sources. Neither case is exceptional. Both reflect the same structural forces at work.

Energy transition commodities face a more severe version of this problem. New project activity is concentrated in jurisdictions with less established mining infrastructure. Historical cost benchmarking data is thinner for lithium, manganese, and rare earths than for iron ore or metallurgical coal, which have decades of comparable project data. Regulatory environments are also moving faster, introducing scope changes mid-construction that would be less likely in mature bulk commodity belts.

Pure-play lithium developers face compounded risk relative to diversified miners such as South32. When commodity price weakness and cost overruns strike simultaneously, as occurred across the lithium sector in early 2025, a single-asset developer has no offsetting cash flow to absorb the damage.

Energy transition capital expenditure now exceeds US$3 trillion annually globally, and the critical minerals projects feeding that cycle — manganese, lithium, and rare earths — are precisely the asset class facing the thinnest cost benchmarking data and the highest average overrun rates of any mining category.

The post-announcement sequence follows a recognisable pattern, and Hermosa is tracking it closely:

The ASX continuous disclosure obligations that govern how listed companies must report material project changes require immediate notification when a capital revision is likely to influence investor decisions, which is precisely why the Hermosa announcement triggered same-day market response and rapid broker recalibration.

South32 management attempted to soften the Hermosa revision by announcing the 18% resource life extension to 33 years simultaneously. Combined with the maintained positive broker ratings, this positions the project as a delayed and more expensive asset rather than a failed one. Macquarie’s FY30 net contribution timeline now serves as the anchor for long-term modelling.

Institutional investors increasingly expect mining companies to maintain contingency buffers of 20-30% of total capex before reaching Final Investment Decision (FID), the point at which a company commits capital to build. Independent cost audits and contractor diversification evidence have also become baseline expectations.

Knowing this sequence helps investors avoid two common errors: panic selling on announcement day before broker analysis is available, and assuming that a maintained buy rating means the short-term outlook is unchanged. The ratings reflect long-term project viability; the target cuts reflect the near-term repricing.

The Hermosa revision is a retrospective event. For investors holding other mining development stocks, the more useful exercise is evaluating overrun risk before a revision is announced. Five criteria provide a practical starting framework:

South32’s position is structurally different from that of a pure-play developer facing the same overrun. Producing assets, including the Worsley alumina operation, continue generating cash flow while Hermosa’s development timeline extends.

Macquarie’s FY30 net contribution expectation implies roughly five years of net capital outflow for Hermosa. South32 can sustain that period in a way that a single-asset developer could not. This diversification buffer does not eliminate the overrun’s impact on shareholder value, but it materially reduces the probability that the cost revision threatens the company’s solvency or forces a dilutive capital raise.

For investors wanting to extend this framework beyond single-stock analysis, our deep-dive into critical minerals investment risks for Australian investors examines China’s dominance of critical minerals processing, currency exposure from AUD/USD movements, and the domestic policy uncertainty that shapes how Australian capital can access the energy transition opportunity.

The structural forces that drove Hermosa’s 50% capex blowout, labour shortages, materials inflation, permitting complexity, and thin cost benchmarking for critical minerals, are not cyclical. They are embedded in the current phase of mining investment, particularly for energy transition commodities.

Capex overruns are a predictable risk category, not a surprise event. The evidence now available, from Wood Mackenzie’s 40-50% industry estimate to the verified broker responses documented above, supports building overrun risk into investment analysis before an announcement, not reacting to it afterwards.

The commodity supercycle thesis that underpins much of the current institutional interest in mining development stocks rests on four demand pillars — copper for AI data centres, grid electrification, EV adoption, and rare earth defence applications — each of which increases the strategic value of assets like Hermosa even as near-term cost revisions weigh on NPV estimates.

Hermosa’s path to FY31 full capacity and FY30 net contribution will serve as a live reference point for how diversified miners manage and communicate through extended development overruns. Australian investors holding mining development stocks would benefit from applying the evaluation framework above to their own portfolios while the lesson is fresh.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Mining capital cost overruns occur when a project's final construction and development costs exceed the original budget estimate. According to Wood Mackenzie's Metals and Mining 2026 Outlook, overruns of 40-50% are typical for critical minerals projects, making them the norm rather than the exception.

South32 shares fell 5.4% on 30 April 2026 after the company disclosed a 50% capital cost increase to A$3.3 billion and a 12-month production delay at its Hermosa Taylor project in Arizona, prompting three brokers to cut their price targets within 24 hours.

Analysts use net present value (NPV) models where project timing and capital intensity are the most sensitive inputs; when both increase costs and extend timelines simultaneously, the impact on price targets is multiplicative rather than additive, reducing the present value of all future cash flows.

Investors should evaluate five factors: the size of the contingency buffer (ideally 20-30% of total capex), the project's jurisdiction and permitting complexity, the commodity type (critical minerals carry higher overrun risk than bulk commodities), contractor structure, and any early analyst signals such as earnings estimate reductions.

A maintained buy rating signals that analysts still view the underlying asset as viable and the company as retaining long-term value, but it does not mean the short-term outlook is unchanged; the accompanying price target cuts reflect a genuine near-term repricing of risk and a reduced margin of safety.