International crude benchmarks surged past $114 per barrel in late April 2026, driven by a perfect storm of structural alliance fractures and immediate maritime blockades. The global energy market is currently absorbing its most significant supply shock in a generation. Oil valuations are reflecting both a permanent structural shift and a severe geopolitical crisis unfolding simultaneously.

The geopolitical fracture became formal on 28 April 2026 with the announcement that the UAE leaves OPEC effectively on 1 May 2026. This historic exit coincides with an ongoing United States maritime blockade of Iranian ports and the physical closure of the Strait of Hormuz. Together, these events have created unprecedented volatility across global energy markets.

This analysis explores why Abu Dhabi is dismantling decades of coordinated production policy. The simultaneous Middle Eastern geopolitical crisis is currently masking the true long-term impact of this structural departure. Investors must look past the immediate supply deficit to understand the new sovereign energy dynamics.

Abu Dhabi’s Commercial Pivot and Production Ambitions

The official reasoning for the departure strips away political rhetoric to reveal a purely commercial calculation. UAE Energy Minister Suhail Al Mazrouei stated the exit serves the national interest following a comprehensive review of production policy and capacity limits. Abu Dhabi has determined that the constraints of international petroleum coalitions no longer align with its vast infrastructure investments.

The state-owned Abu Dhabi National Oil Company (ADNOC) will now pursue an independent output strategy. The company plans to gradually increase extraction outside of previous quota frameworks to capture market share once regional shipping routes reopen. This departure represents a permanent commercial repositioning that will dictate global supply ceilings for the next decade.

| Production Metric | Historical Alliance Framework | Independent Sovereign Target |

|---|---|---|

| Daily Output Baseline | According to reports, 3.5 million barrels per day | 5.0 million barrels per day |

| Operational Authority | Subject to coalition consensus | Fully independent state control |

| Implementation Timeline | Restricted indefinitely | Effective 1 May 2026 |

The Strategic Blueprint for Independent Output

According to reports, state-owned infrastructure has been steadily scaling to meet the new 5 million barrels per day objective. The company has invested heavily in advanced extraction technologies and expanded export terminal capabilities over the past three years. These facilities are now positioned to operate at maximum efficiency without the artificial constraints of alliance limits.

The accelerated timeline for these facility upgrades aligns with Energy Outlook Advisors capacity forecasts, which indicate that operating outside quota constraints is essential for Abu Dhabi to fully capitalise on its heavy upstream investments by 2027.

Abandoning quota limitations provides Abu Dhabi with immediate operational freedom. The nation can now negotiate direct, long-term supply contracts with major Asian importers without seeking coalition approval. This independence fundamentally shifts the balance of power among Middle Eastern producers.

When big ASX news breaks, our subscribers know first

The Structural Mechanics of Global Energy Alliances

International petroleum coalitions function primarily to stabilise prices through coordinated artificial supply constraints. When demand falls, member nations agree to reduce their collective output to prevent a collapse in barrel valuations. This mathematical leverage relies entirely on the group controlling a dominant percentage of total global supply.

The mechanism requires a strict separation between physical production capacity and permitted quota output. A member state might possess the infrastructure to pump millions of barrels daily, but they must artificially restrict that flow to meet their assigned quota. This unused capacity acts as a buffer to manage sudden market fluctuations.

The loss of the second-largest producer fundamentally weakens the remaining alliance’s ability to orchestrate global valuations. According to reports, the departure removes approximately 12% of the coalition’s existing output capabilities overnight.

The remaining members lose leverage through three primary channels:

Market Share Dilution: The coalition controls a smaller percentage of global exports, reducing the mathematical impact of any future coordinated cuts. Enforcement Failure: Independent actors with massive spare capacity can immediately replace any barrels the coalition removes from the market. * Signalling Weakness: Forward guidance from the alliance carries less weight when major regional producers operate outside its jurisdiction.

The Geopolitical Paradox Keeping Prices Elevated

The energy market is currently navigating a severe paradox. Crude prices are rising rapidly despite a major producer preparing to flood the market with new independent supply. Immediate geopolitical risk premiums are entirely overshadowing the bearish long-term signal of the Abu Dhabi departure.

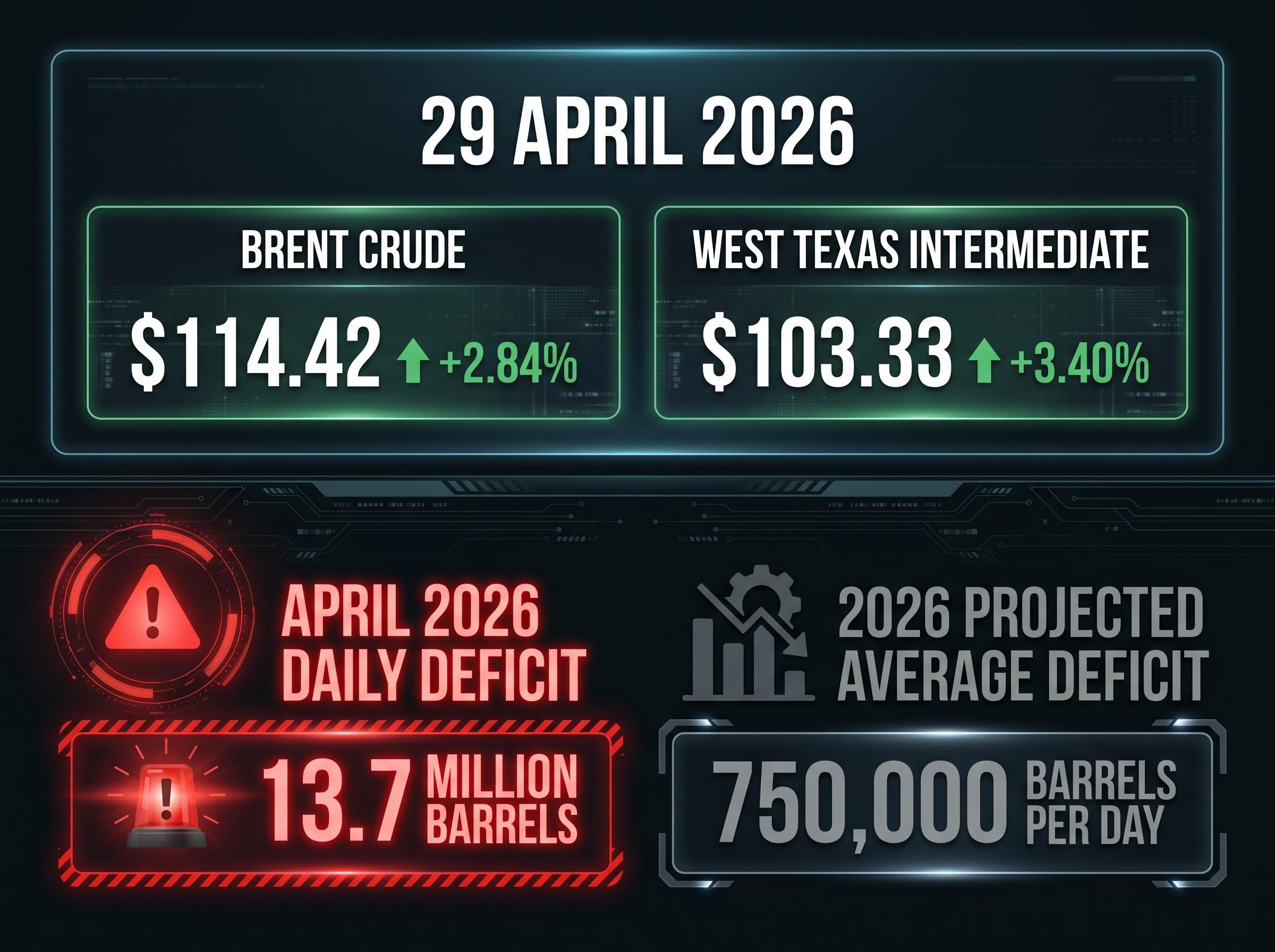

Real-time valuations reflect intense physical anxiety rather than future capacity projections. Brent Crude reached $114.42 on 29 April 2026, representing a 2.84% daily increase. West Texas Intermediate climbed to $103.33, posting a 3.40% daily gain. The market is pricing in the immediate reality of blocked transport routes over the impending reality of independent production.

This growing energy risk has pushed domestic gasoline prices to historic highs, a threshold that traditionally triggers a sharp contraction in broad equity market valuations over the subsequent six months.

According to reports, global petroleum markets experienced a daily deficit amounting to 13.7 million barrels in April 2026. Analysts project an average global deficit of 750,000 barrels per day throughout 2026, assuming the conflict timeline extends into the third quarter.

International Energy Agency Assessment “Severe physical shortages are expected to persist abroad through April. The global market is struggling to absorb an unprecedented supply severance driven by closed maritime corridors.”

Supply Chain Severance in the Middle East

The United States maritime blockade and the closure of the Strait of Hormuz have severed the primary arteries of global crude transport. Tankers are unable to safely navigate the corridor, trapping millions of barrels of previously scheduled deliveries within the Persian Gulf. Insurance syndicates have effectively paused coverage for vessels attempting the route.

Investors must separate these short-term logistical constraints from long-term structural supply trends. The physical realities of halted shipping routes create immediate localised shortages across European and Asian markets. However, these bottlenecks temporarily mask the massive incoming volume from independent state producers once maritime security returns.

The Ticking Clock on Iranian Infrastructure

The standoff between Washington and Tehran regarding maritime restrictions has introduced a strict logistical timeline to the crisis. Blocked export terminals are placing severe strain on Iranian domestic energy infrastructure. The inability to load crude onto international vessels means oil must be diverted into onshore holding facilities.

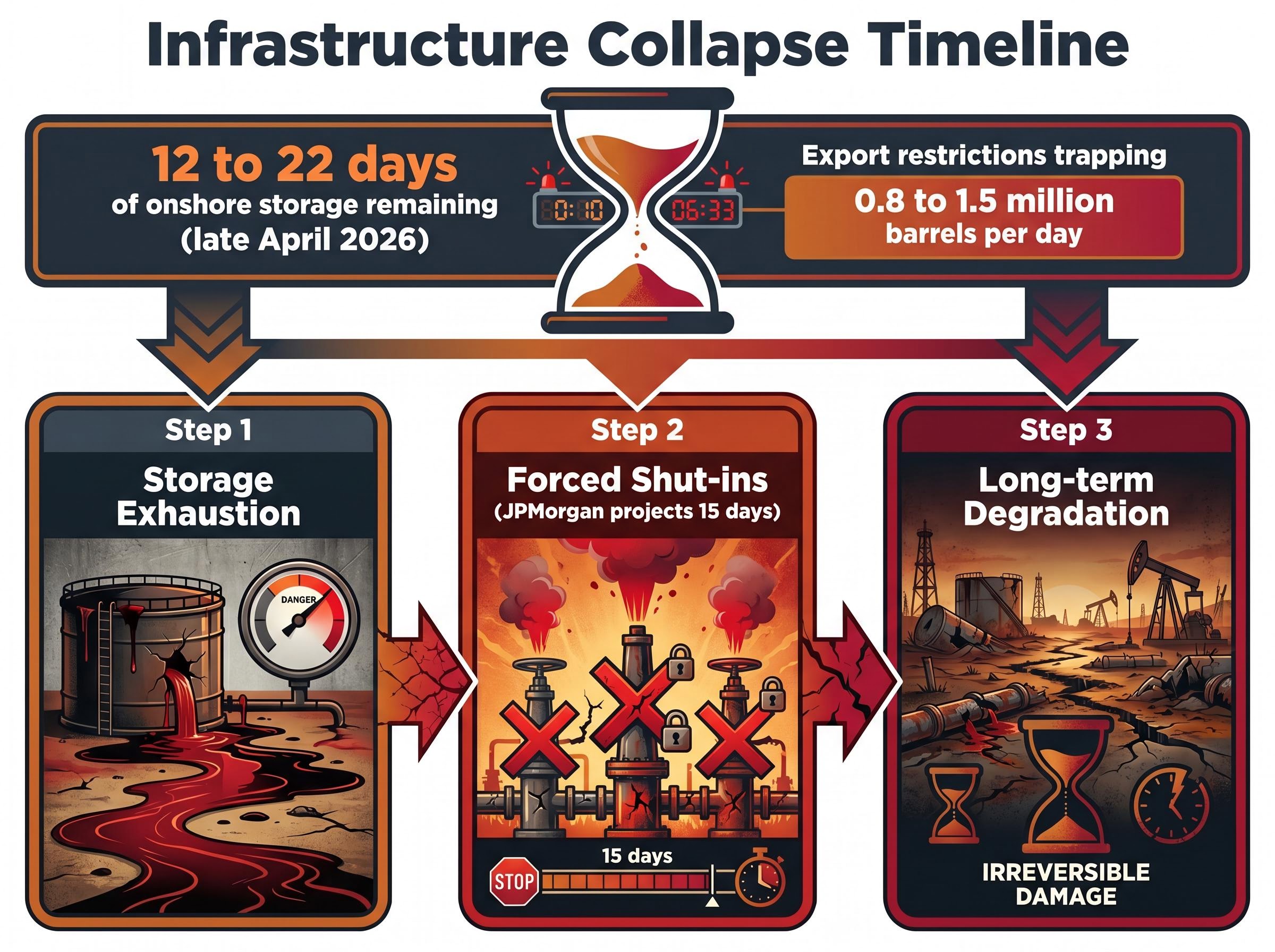

Intelligence calculations show Iran has only 12 to 22 days of unused onshore storage capacity remaining as of late April 2026. Current export restrictions are holding steady at 0.8 to 1.5 million barrels per day. The physical limits of steel tanks and pipeline pressures are rapidly approaching their breaking points.

JPMorgan projections indicate absolute shut-in thresholds could hit within 15 days.

The infrastructure collapse timeline is expected to follow a sequential pattern:

- Storage Exhaustion: Maximum onshore holding capacity is reached within the immediate two-to-three-week window.

- Forced Shut-ins: Domestic extraction facilities must halt production as crude flows back up through the pipeline network.

- Long-term Degradation: Abrupt pressure changes and mandatory well closures risk causing permanent geological damage to mature extraction sites.

Understanding this strict logistical timeline gives investors a predictive framework. The physical energy market will experience its next major shock not from diplomatic announcements, but from the mechanical necessity of shutting down active wells.

Past performance does not guarantee future results. Financial projections and supply calculations are subject to market conditions and various geopolitical risk factors.

Macroeconomic Contagion and Central Bank Calculations

These isolated energy shocks threaten broader global financial stability just as central banks plan their next monetary policy adjustments. Sustained $114 oil threatens to reverse recent inflation victories across major Western economies. Energy input costs pass rapidly through the supply chain, inflating transport, manufacturing, and consumer goods pricing.

The dual pressures of the coalition fracture and the maritime blockade act as primary drivers of global economic uncertainty. Markets are heavily focused on upcoming Federal Reserve meetings to gauge how policymakers will absorb this commodity shock. Broad expectations suggest Federal Reserve Chairman Jerome Powell will maintain current borrowing costs to counter the inflationary pressure of the crude deficit.

Federal Reserve Forward Stance “Conflict-driven economic pressures and sustained commodity inflation complicate the trajectory for interest rate adjustments. The central bank must account for the broad inflationary pass-through of sustained energy market disruptions.”

Elevated crude valuations force central banks into a defensive posture. The isolation of the commodity market vanishes as high fuel costs drain consumer discretionary spending power.

For investors wanting to model the macroeconomic fallout, our full explainer on oil price recession transmission details the simultaneous channels of rising business input costs, tightening central bank policy, and subsequent hiring pullbacks.

A Permanent Realignment of Petroleum Economics

The 1 May 2026 departure marks the definitive end of an era for coordinated global supply. The market structure will look vastly different once the immediate maritime crisis resolves and shipping lanes reopen. The target 5 million barrels per day objective will eventually collide with the current 13.7 million barrel daily deficit, completely rewriting global supply mathematics.

Independent state actors will dictate the next decade of energy economics. Abu Dhabi’s operational freedom sets a precedent that prioritises sovereign commercial interests over collective price stabilisation. Investors must prepare for a market where structural alliance leverage is permanently diminished, and sovereign production capacity sets the baseline for global economic growth.

This sovereign control over supply removes a key stabilising mechanism for Western economies, amplifying equity market warning signals as investors face prolonged exposure to volatile commodity pricing.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.