KOSPI Drops 10% as Crowded AI Trade Unwinds Across Global Markets

8 hrs ago

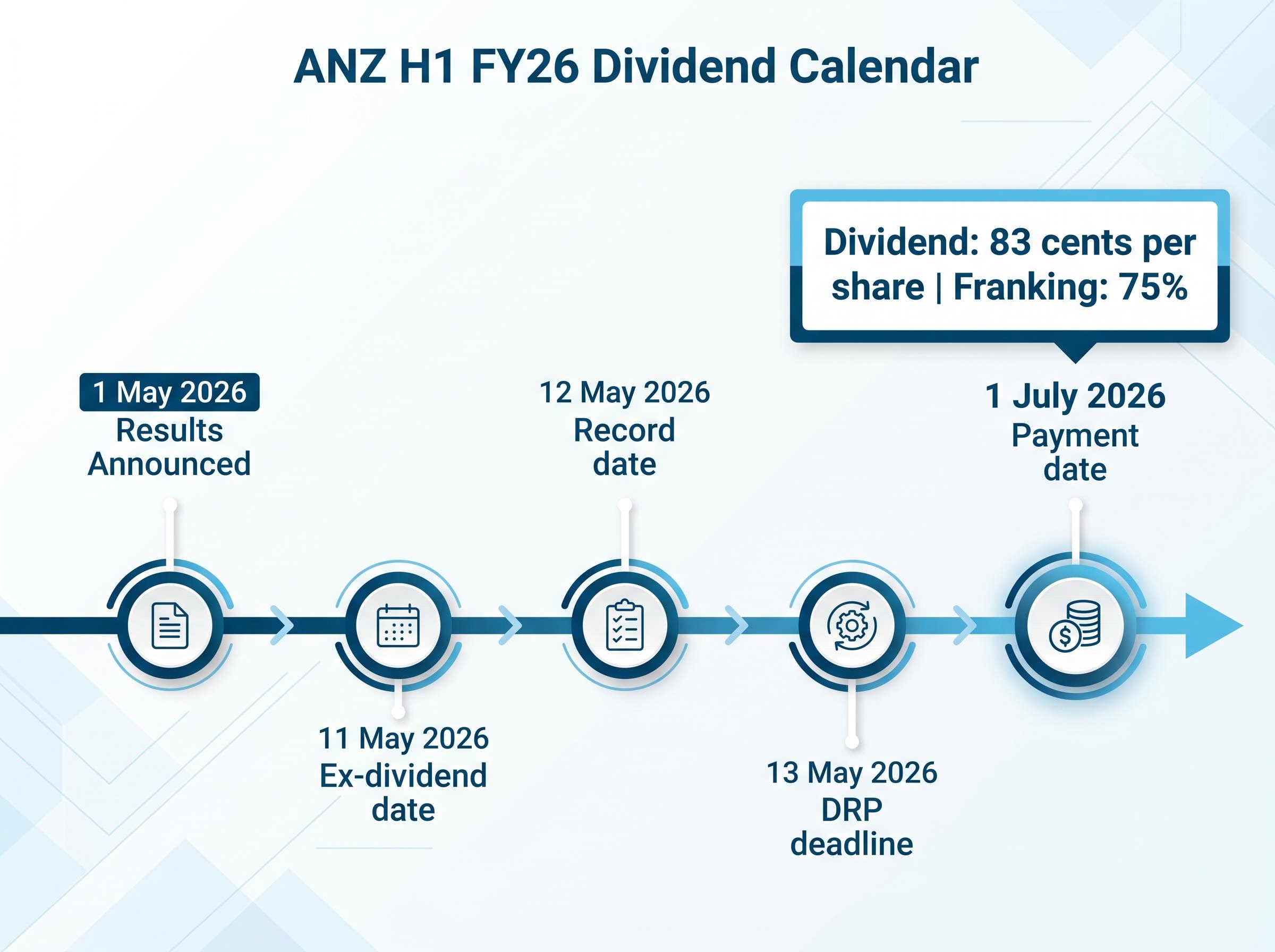

ANZ has kept its dividend steady at 83 cents per share for every payout since July 2024, but the 2026 interim announcement carries one meaningful change: the franking level has ticked up from 70% to 75%, putting more tax-offset value in the hands of eligible Australian investors.

The announcement landed alongside ANZ’s H1 FY26 results on 1 May 2026, giving income-focused shareholders a narrow window to act. The ex-dividend date falls on 11 May 2026, meaning investors who do not already hold ANZ shares have days, not weeks, to position themselves for the July payment. What follows covers exactly what was announced, what the improved franking means in dollar terms for Australian shareholders, how ANZ’s yield stacks up among the Big Four banks, and what eligible shareholders should know about the dividend reinvestment plan.

The number itself tells the story. ANZ declared an interim dividend of 83 cents per share for H1 FY26, the same figure it has paid on every distribution since July 2024. Six consecutive payouts at the same level is a deliberate signal of stability, and for shareholders accustomed to the rhythm, the confirmation removes one variable from their income planning.

ANZ has maintained its dividend at 83 cents per share across every distribution since July 2024, covering both interim and final payments for FY25 and now the FY26 interim.

The dates that matter are tight:

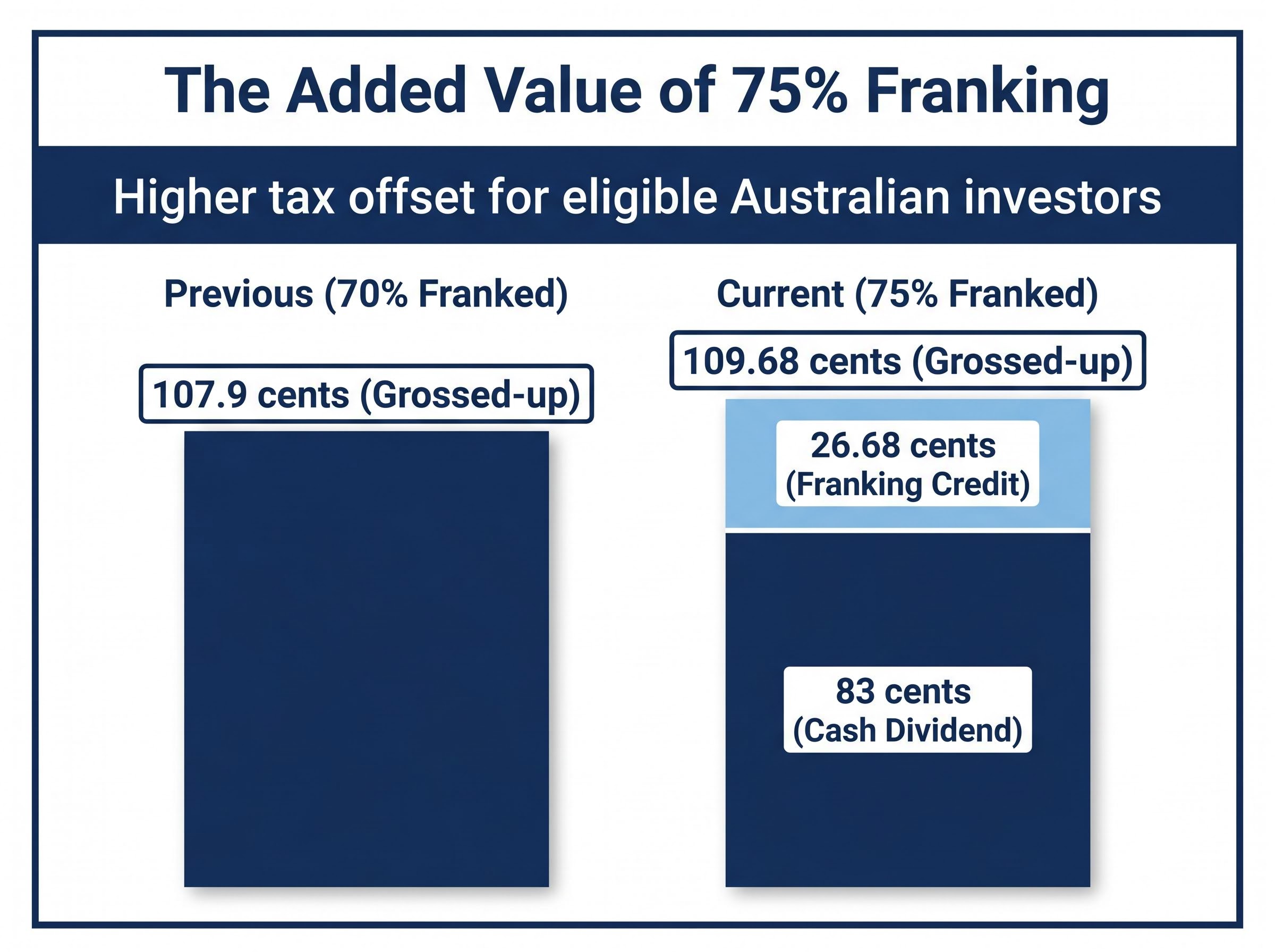

What separates this announcement from its predecessors is a single adjustment. The franking level has risen from 70% (applied to both FY25 distributions) to 75%. It is not a dramatic shift, but for eligible Australian taxpayers, it represents a measurably larger tax offset on the same cash payment.

ANZ’s H1 FY26 numbers arrived strong on the headline. Statutory profit reached $3.65 billion, up 62% on the prior half, while cash profit came in at $3.78 billion, a 70% increase (or 14% excluding significant items). A sharp reduction in operating expenditure, down 22% to $5.54 billion, drove much of the improvement.

| Metric | H1 FY26 Result | Change vs Prior Half |

|---|---|---|

| Statutory profit | $3.65 billion | Up 62% |

| Cash profit | $3.78 billion | Up 70% (14% ex. significant items) |

| Total operating income | $11.2 billion | Up 3% |

| Operating expenditure | $5.54 billion | Down 22% |

Total operating income grew a more modest 3% to $11.2 billion, which means cost discipline, not revenue acceleration, was the primary earnings driver. The market appeared to agree that the result was already priced in. ANZ shares fell approximately 1.01% to $36.29 on results day, even as the broader S&P/ASX 200 rose 0.94%.

The ANZ half-year results also revealed that non-interest operating income surged 28% to $2.316 billion, offsetting a 2% decline in net interest income and signalling a deliberate shift toward revenue diversification that the headline profit figure alone does not capture.

That divergence is worth noting. A 62% statutory profit jump and a steady dividend would typically draw buyers, not sellers. The sell-off suggests investors had already positioned ahead of the result, or that the underlying revenue growth rate left questions the headline profit figure papered over.

Australia’s dividend imputation system exists to solve a specific problem: without it, company profits would be taxed once at the corporate level and again in the shareholder’s hands. Franking credits represent the portion of corporate tax ANZ has already paid on the profits funding the dividend. When those credits are attached to a distribution, eligible Australian shareholders can use them as an offset against their personal income tax.

The ATO’s dividend imputation rules establish that franking credits flow from tax already paid at the corporate rate, meaning the credit value available to a shareholder is directly tied to the 30% corporate tax rate applied to the distributable profit, not to the dividend amount itself.

At 75% franking, the calculation works as follows:

At 75% franking, the grossed-up value of ANZ’s interim dividend rises to approximately 109.68 cents per share, up from approximately 107.9 cents at the previous 70% franking level.

The difference between 107.9 cents and 109.68 cents may appear modest on a per-share basis. Across a meaningful holding, however, the additional franking credit accumulates. The benefit is most pronounced for investors in lower marginal tax brackets or self-managed super fund (SMSF) trustees in the 15% accumulation tax phase, where the credit can exceed the tax liability and generate a refund.

Franking credit allocation in superannuation is not always straightforward: pooled fund structures can create gaps between the credits a fund receives at the entity level and what individual members effectively benefit from, a structural issue that matters particularly for SMSF trustees who control their own direct share holdings and receive credits without dilution.

Only Australian tax residents can claim franking credits against personal tax obligations. Non-resident shareholders receive the 83-cent cash payment but cannot access the imputation benefit.

At $36.29 per share, ANZ carries a trailing dividend yield of approximately 4.58%. At the time of the announcement, that figure was described as the highest among Australia’s four major ASX-listed banks, though confirmed peer-specific yields for Commonwealth Bank, Westpac, and NAB were not available at the time of publication.

The three yield-related figures worth noting:

These are point-in-time measures. A share price move of even $1 shifts the trailing yield by roughly 20 basis points at current dividend levels. Updated post-results broker consensus was not available at the time of publication, so the forward yield figure reflects pre-results expectations and may be revised.

Yield leadership among the Big Four is a meaningful data point for income-focused investors screening ASX bank shares. It does not, on its own, constitute a complete income comparison; franking levels, payout sustainability, and capital growth potential all shape the full picture.

A Big Four bank income comparison published the same week as ANZ’s H1 FY26 results placed ANZ’s grossed-up yield at approximately 5.95%, ahead of CBA but behind NAB’s 6.06%, while also noting that Westpac’s trajectory toward 100% franking could shift the ranking for patient investors over a multi-year horizon.

ANZ’s Dividend Reinvestment Plan (DRP) offers eligible shareholders the option to receive new ANZ shares in lieu of a cash dividend, typically at a discount to the prevailing market price. No brokerage is charged on DRP shares, which makes it a straightforward cost efficiency for long-term holders seeking to compound their position.

The DRP suits a specific type of investor: one who does not rely on the cash income and prefers to build their ANZ holding over time. It is not a universal recommendation; shareholders who depend on the quarterly cash flow or who want to rebalance their bank exposure may prefer to take the payment.

Franking credits and DRP compounding work together to widen the gap between a headline share price return and the total return an investor actually receives, a dynamic that played out clearly in CBA’s case, where a 52% two-year price gain translated to an estimated 72% total return once fully franked dividends were reinvested.

The key DRP action points:

That deadline sits just two days after the ex-dividend date of 11 May 2026. Shareholders who intend to elect the DRP for this interim payment should not wait until the last day.

The 2026 interim dividend is confirmed at 83 cents per share with 75% franking, and the ex-dividend date of 11 May 2026 is the operative deadline for investors seeking to qualify for the 1 July 2026 payment. Eligible shareholders face two decisions before 13 May 2026: take the cash dividend or elect into the DRP.

Official documentation, DRP election forms, and the full H1 FY26 results presentation are available at the ANZ investor centre (anz.com/shareholder/centre). Shareholders seeking to calculate the personal value of franking credits based on their individual tax circumstances should consult a qualified tax adviser.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

ANZ declared an interim dividend of 83 cents per share for H1 FY26, maintaining the same amount paid on every distribution since July 2024, with a payment date of 1 July 2026.

The ex-dividend date for ANZ's H1 FY26 interim dividend is 11 May 2026, meaning investors must hold ANZ shares before this date to qualify for the 1 July 2026 payment.

At 75% franking, ANZ's 83-cent interim dividend carries an attached franking credit of approximately 26.68 cents, bringing the grossed-up dividend value to approximately 109.68 cents per share for eligible Australian tax residents.

At a share price of $36.29 on 1 May 2026, ANZ carried a trailing dividend yield of approximately 4.58%, which was described as the highest among Australia's four major ASX-listed banks at the time of the announcement.

Eligible shareholders can elect into ANZ's Dividend Reinvestment Plan via the ANZ investor centre at anz.com/shareholder/centre, with the DRP election deadline set at 13 May 2026, two days after the ex-dividend date.