In April 2026, Australian investors face a stark economic reality defined by a Reserve Bank of Australia cash rate at 4.10% and persistent Consumer Price Index inflation holding at 4.6% year-over-year. Geopolitical energy supply shocks and shifting domestic conditions have disrupted historical market assumptions. These dual pressures make defensive positioning a critical priority, demanding an inflation portfolio strategy that actively protects capital against erosion.

Historical correlations between asset classes are shifting, requiring a deliberate departure from passive holding patterns. This breakdown provides a detailed blueprint for fortifying wealth using a modern asset allocation framework. It outlines specific ASX-listed exchange-traded fund strategies designed to manage these volatile environments effectively.

Understanding the Mechanics of Modern Market Volatility

Simultaneous declines in broad equities and traditional bonds leave many investors questioning the efficacy of standard diversification. The historical positive correlation between these two asset classes frequently re-emerges during periods of persistent high inflation. When consumer prices surge, central banks raise rates mechanically, compressing equity valuations while simultaneously driving down the face value of existing bonds.

Current domestic inflation is not merely a cyclical fluctuation but a product of deep structural forces that resist quick policy fixes. Three primary catalysts are currently driving this sustained economic imbalance:

- Geopolitical energy supply shocks that create immediate, unavoidable cost pressures across the logistics and manufacturing sectors.

- Currency depreciation risks that elevate the cost of imported goods, directly impacting domestic consumption.

- Elevated wage expectations that threaten to embed consecutive price increases permanently into the domestic service economy.

These combined dynamics force aggressive, sustained monetary policy responses from the central bank. Major institutions, including Westpac, have subsequently revised their models to forecast the cash rate could reach 4.85% by August 2026.

Recent Westpac institutional economic forecasts confirm this restrictive stance, projecting further central bank tightening as policymakers attempt to anchor long-term price expectations.

Energy commodity markets are currently exhibiting a pronounced backwardation, a condition where near-term futures trade at significant premiums to longer-dated contracts. This structural pricing indicates that geopolitical supply shocks may be short-lived, but they still require immediate defensive portfolio adjustments to manage the acute short-term volatility.

The economic toll of sustained price pressure extends far beyond daily market fluctuations and portfolio drawdowns.

“According to International Monetary Fund projections, persistent inflation diminishes real GDP expansion.”

This data validates investor concerns regarding long-term capital erosion in the current market. Understanding these exact macroeconomic mechanics is the strict prerequisite for implementing the strategic solutions required to fix underlying portfolio vulnerabilities.

When big ASX news breaks, our subscribers know first

The Revised Defensive Asset Allocation Framework

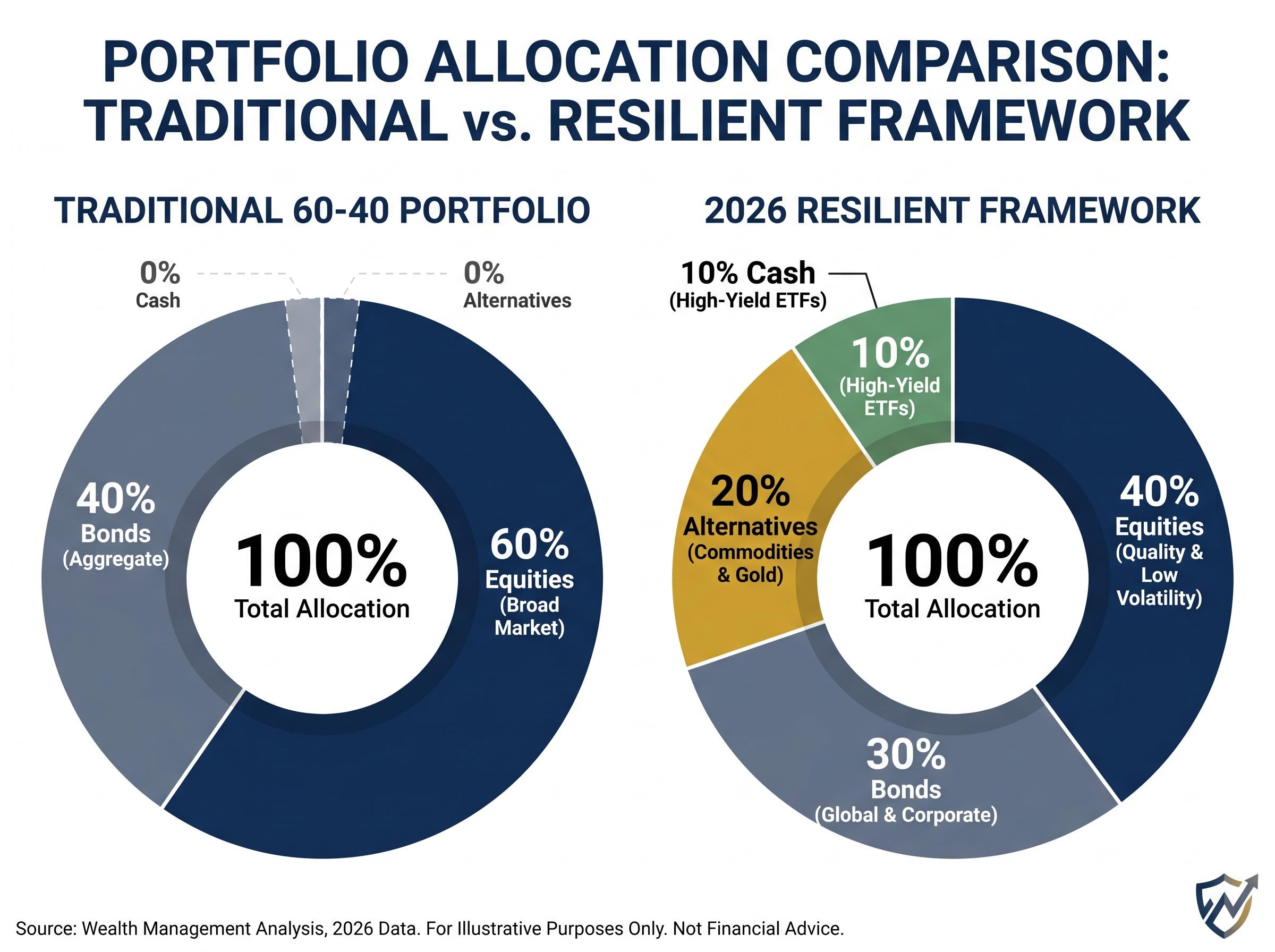

The traditional 60-40 portfolio struggles immediately when both growth and defensive assets draw down simultaneously. A modern asset allocation framework provides a structured, mathematical solution tailored specifically for the 2026 inflationary environment. This institutional model actively moves beyond outdated splits to increase reliance on alternative assets and strategic liquidity.

This revised framework explicitly balances long-term structural disinflationary forces with acute short-term energy inflation risks. It dictates a stringent benchmark breakdown of 40% equities, 30% bonds, 20% commodities and alternatives, and 10% cash. The strategy deliberately shifts away from broad, passive equity exposure toward highly targeted low-volatility and quality factor tilts.

This targeted allocation serves as an immediate, actionable roadmap for wealth preservation. Investors can directly compare this benchmark against their current holdings to identify and mathematically resolve their defensive gaps.

| Asset Class | Traditional 60-40 Portfolio | 2026 Resilient Framework | Primary Strategic Objective |

|---|---|---|---|

| Equities | 60% (Broad Market) | 40% (Quality & Low Volatility) | Capture pricing power and protect capital. |

| Bonds | 40% (Aggregate) | 30% (Global & Corporate) | Generate yield from higher base rates. |

| Alternatives | 0% | 20% (Commodities & Gold) | Hedge against acute energy and currency shocks. |

| Cash | 0% | 10% (High-Yield ETFs) | Maintain strategic liquidity for market corrections. |

Deploying this structure ensures that capital is not left exposed to correlated drawdowns across legacy asset classes.

For investors wanting to mathematically model this specific shift, our deep dive into resilient 2026 asset allocation strategies breaks down the mechanics of securing high Australian yields while systematically capturing discounted international equities.

Selecting High-Quality Equities for Downside Protection

Capital preservation does not require abandoning equity markets entirely. The focus must instead shift from high-beta growth stocks toward mature companies with fortified balance sheets and the direct ability to dictate consumer pricing. Exchange-traded funds that specifically capture this pricing power transform equities from a portfolio vulnerability into a resilient growth engine.

Targeting ASX companies with pricing power, particularly those maintaining high returns on equity alongside low debt levels, provides a direct buffer against rising input costs.

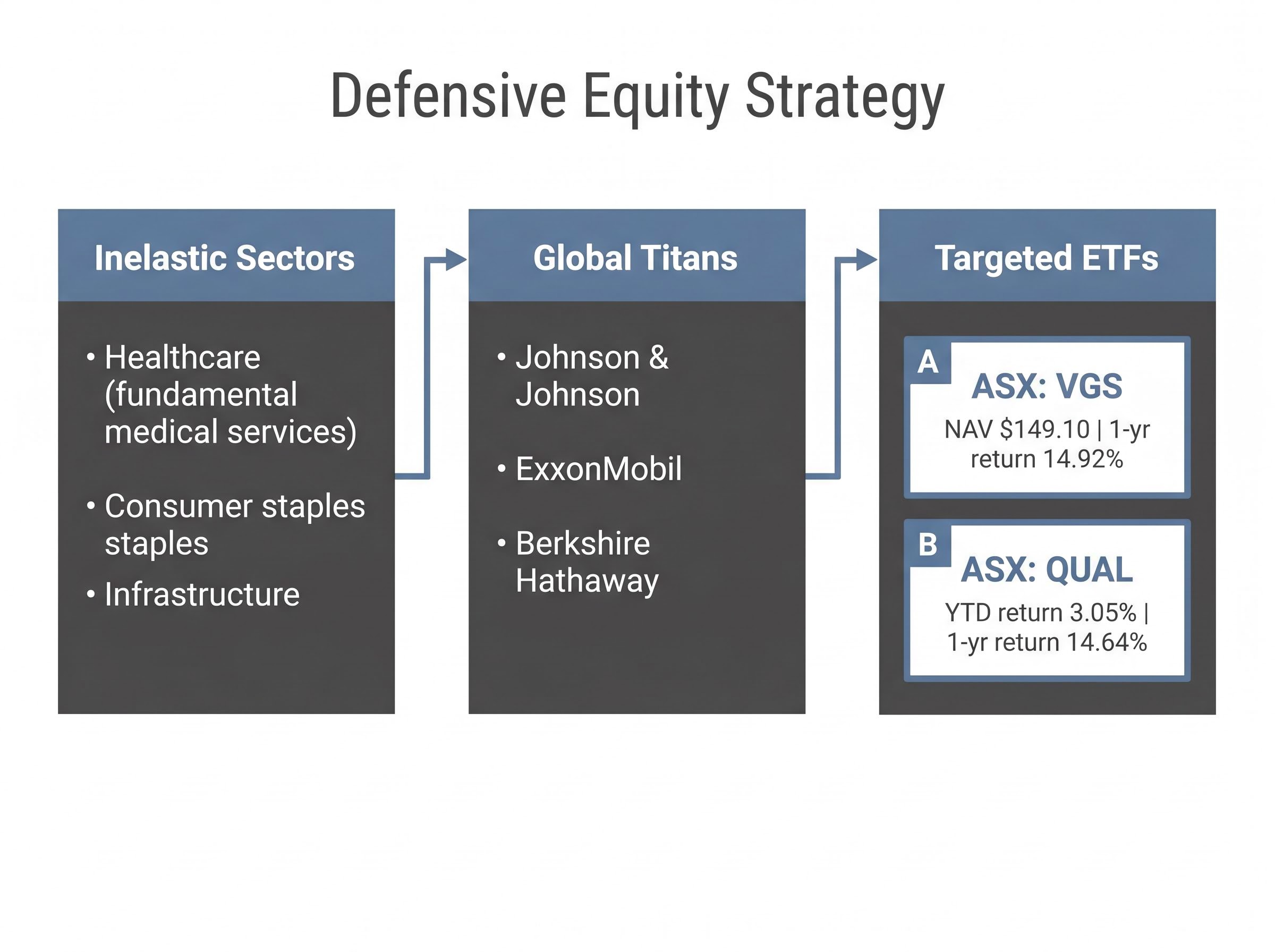

International diversification is necessary to protect against localised Australian economic deterioration and domestic consumption slowdowns. Global minimum volatility strategies offer proven downside protection during volatile periods while maintaining continuous exposure to structurally stable giants like Johnson & Johnson, ExxonMobil, and Berkshire Hathaway.

The Vanguard MSCI Index International Shares ETF (ASX: VGS) provides this necessary global scale for Australian portfolios. As of late April 2026, the fund holds a net asset value of $149.10 and has delivered a resilient one-year return of approximately 14.92%.

Factor-based strategies offer another distinct layer of mathematical defence. The VanEck MSCI International Quality ETF (ASX: QUAL) filters specifically for fundamental strength, posting a year-to-date return of 3.05% and a one-year return of 14.64%. These vehicles systematically ensure capital is deployed only into businesses capable of absorbing sudden input cost shocks.

A resilient equity defence requires deliberate exposure to key sectors that demonstrate highly inelastic consumer demand.

Healthcare providers and pharmaceutical manufacturers offering fundamental, non-discretionary medical services. Consumer staples businesses that maintain their operating margins consistently during cost-of-living crises. * Infrastructure assets fortified with inflation-linked revenue contracts that adjust automatically.

Balancing Domestic Moats with Global Titans

Investors must carefully balance international scale with protected domestic advantages. Australian wealth managers strongly recommend pairing global exposures with localised, high-quality ASX options to optimise total returns.

The BetaShares Australian Quality ETF (ASX: AQLT) and the VanEck Morningstar Wide Moat ETF (ASX: MOAT) serve as ideal domestic anchors within this framework. These specific funds allow investors to maintain local franking credit benefits while exclusively accessing companies with deeply entrenched competitive advantages.

These selected ETF structures utilise stringent quantitative screening criteria to filter out highly leveraged, vulnerable companies. By strategically blending global titans with domestic moats, investors can execute a precise equity strategy that strictly limits downside capture without sacrificing long-term compounding.

Maximising Yield Through Fixed Income and Cash Vehicles

The aggressive central bank tightening cycle that damaged legacy bond portfolios has simultaneously created compelling opportunities for fresh capital deployment. Investors can now reframe fixed income and cash from passive safe havens into highly active yield-generating engines. The sharp, mathematical decline in existing bond face values means that new capital allocations secure significantly higher distribution rates.

Managing forward duration risk requires a deliberate, balanced mix of global aggregate bonds and domestic corporate credit. Global aggregate bonds provide necessary broad sovereign diversification, while Australian investment-grade corporate credit offers highly attractive spreads over standard government yields.

The Vanguard Global Aggregate Bond Index (ASX: VBND) serves as a foundational global fixed-income exposure, offering an annual yield of approximately 5.93% at a net asset value of $40.7772. For targeted domestic corporate exposure, the BetaShares Australian Investment Grade Corporate Bond ETF (ASX: CRED) has generated a resilient year-to-date return of 0.48% alongside a cumulative total return of 27.74%.

Cash allocations must also work demonstrably harder in a high-inflation environment. Cash ETFs should be viewed explicitly as strategic liquid reserves, yielding immediate, compounding returns while remaining instantly deployable during sudden market corrections.

The BetaShares Australian High Interest Cash ETF (ASX: AAA) provides a consistent 3.90% trailing yield, functioning as a highly stable portfolio anchor. Similarly, the iShares Enhanced Cash ETF (ASX: ISEC) delivers an optimised 4.19% annual yield. These specific vehicles allow investors to safely generate strong, reliable returns on the defensive portions of their portfolio without taking on unnecessary, correlated equity risk.

| Ticker | Asset Class | April 2026 Yield | Primary Role |

|---|---|---|---|

| ASX: VBND | Global Aggregate Bonds | 5.93% | Broad sovereign diversification and baseline yield. |

| ASX: CRED | Domestic Corporate Bonds | Total Return Driven | Targeting corporate spreads and duration management. |

| ASX: AAA | High Interest Cash | 3.90% | Capital preservation and instant liquidity. |

| ASX: ISEC | Enhanced Cash | 4.19% | Optimised cash returns with immediate deployment capability. |

Integrating Alternative Assets and Tactical Hedges

Geopolitical energy shocks present unique mathematical hazards that traditional equities and government bonds cannot fully mitigate. Assigning a full 20% portfolio weight to alternative assets acts as a direct, structural buffer against these highly unpredictable external events. This specific allocation provides the necessary financial safety valves to weather acute global supply disruptions.

When severe correlation breakdowns expose failing traditional safe haven assets, investors are forced to restructure their defensive layers to establish immediate liquidity.

Precious metals consistently function as a critical non-correlated asset during periods of severe currency depreciation and geopolitical stress. Wealth management frameworks currently recommend maintaining a strict 5% to 10% portfolio weight in physical gold. This specific strategic allocation serves as a direct, highly responsive inflation hedge when fiat purchasing power rapidly declines.

Historical market context demonstrates that commodity-driven price spikes typically force brief but highly aggressive monetary tightening from central banks. Investors can directly counter this specific risk by actively employing Australia-specific inflation-linked bonds or basic derivatives to hedge against severe consumer price spikes.

The 20% alternatives bucket relies entirely on distinct assets performing highly specific defensive functions.

Physical gold allocations defend immediately against sudden currency devaluation and systemic financial stress. Broad commodity exposures directly capture the pricing upside of global energy and agricultural supply constraints. * Inflation-linked bonds provide guaranteed real yields that adjust mechanically alongside the official consumer price index.

This alternative layer completes the resilient portfolio construction, ensuring investment capital remains heavily insulated from the unique macroeconomic hazards of 2026.

Sustaining Wealth Through Geopolitical and Economic Shifts

Managing an inflationary environment requires active, mathematical structural adjustments rather than emotional panic selling. The severe macroeconomic shifts defining 2026 demand a portfolio built explicitly for resilience, consistently prioritising pricing power, strategic yield, and uncorrelated alternative hedges. Systematic, continuous investing remains the single most reliable mechanism for capturing eventual recovery gains over the long term.

Investors must critically evaluate their current portfolio positions against the stark realities of a prolonged central bank tightening cycle. Review your existing asset split directly against the proposed 40-30-20-10 resilient framework to identify critical defensive gaps. Rebalancing systematically toward high-quality equities, active fixed income, and targeted alternative assets is the definitive action required to safely sustain wealth through ongoing geopolitical volatility.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.