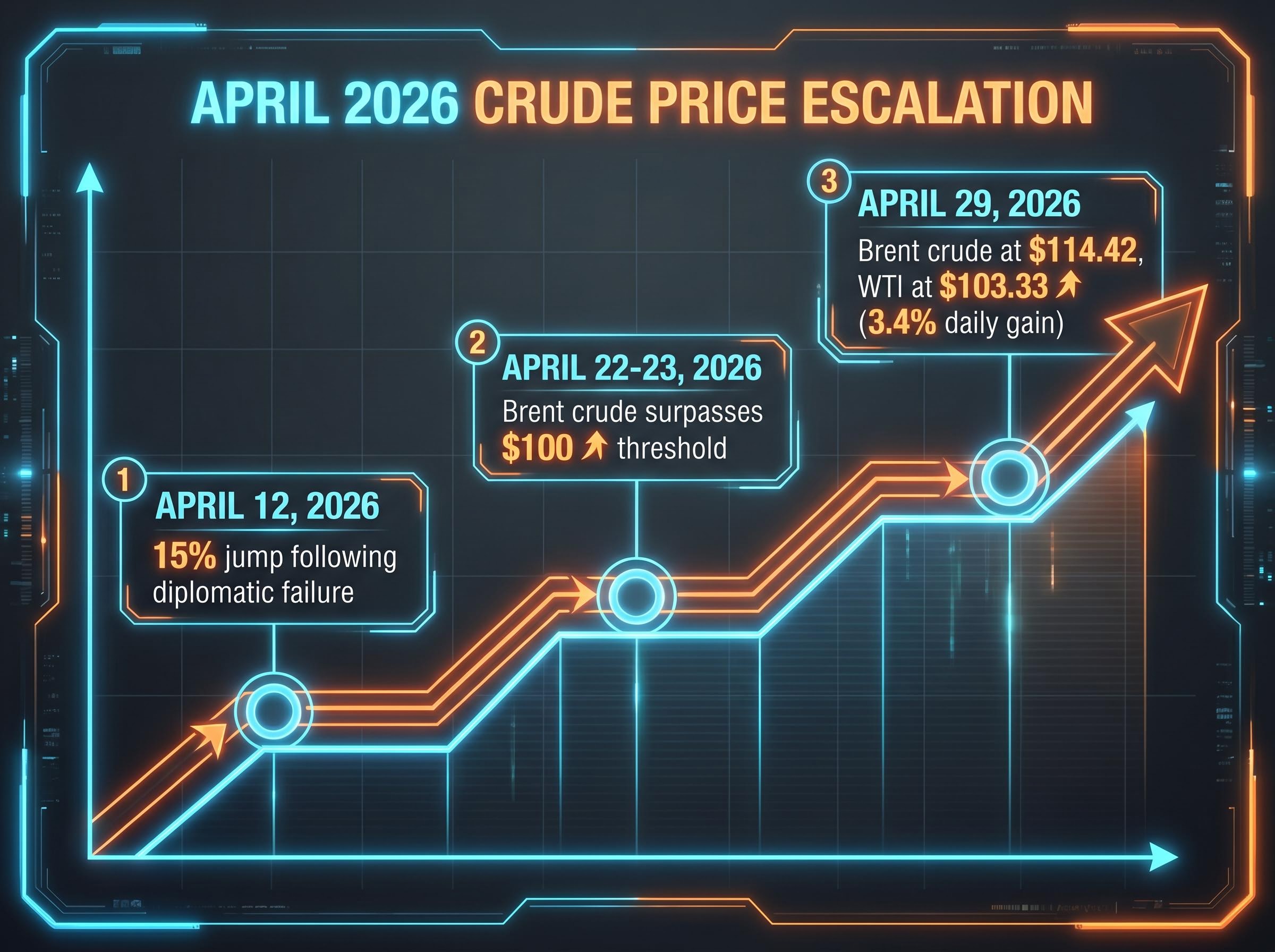

As of April 29, 2026, Brent crude breached the $114.42 mark while the international energy sector faces a staggering daily deficit. This severe constraint stems directly from stalled diplomatic negotiations between the United States and Iran over vital maritime shipping lanes. The ongoing standoff has escalated rapidly beyond a regional geopolitical conflict into a massive constraint on the global oil market.

Recent ship seizures and military posturing have driven weeks of heavy volatility, countering prior temporary price declines. The momentum behind this rally has fundamentally altered forward projections across major financial institutions. This momentum is raising the stakes for global central banks as imported inflation threatens to derail years of careful monetary policy.

This analysis breaks down the immediate supply deficit and the severe physical constraints facing Iranian extraction infrastructure. Furthermore, the impending United Arab Emirates exit from the major international petroleum coalition will permanently restructure cartel dynamics. Understanding how these international pressures converge is vital for determining exactly how they will dictate domestic inflation and Federal Reserve policy.

Calculating the Massive Daily Crude Shortfall

The sheer scale of the supply deficit translates directly from abstract geopolitical tension into cold mathematical reality for commodity traders. International crude benchmarks recorded severe price action today, April 29, 2026, confirming the market’s worst fears regarding sustained supply constraints. Brent crude is currently trading at approximately $114.42 per barrel, cementing a steady climb that began when it officially surpassed the $100 threshold between April 22 and April 23, 2026.

Meanwhile, West Texas Intermediate sits at approximately $103.33 per barrel, representing a significant 3.4% gain today alone. The narrowing spread between international benchmarks reflects a global scramble for secure barrels, bypassing traditional regional discounts. This recent spike compounds weeks of heavy market volatility, including a sharp 6% surge following weekend escalations earlier in the month.

This prior volatility included Iran’s official declaration of closing the Strait of Hormuz, a move that immediately countered prior temporary price declines. Analysts have quantified the exact missing volume, highlighting the systemic risk to global energy portfolios.

Specifically, the latest Goldman Sachs Q2 deficit projections estimate a severe shortfall of 9.6 million barrels per day, underscoring the immediate impact of these regional disruptions on global availability.

Goldman Sachs Supply Deficit Estimate The ongoing maritime blockades have removed barrels per day from international availability, creating a structural deficit that markets cannot easily replace through strategic reserves.

The diplomatic impasse between Washington and Tehran guarantees these restrictions will persist without a definitive end date. The US administration demonstrates a clear preference for maritime restrictions over direct military engagement, effectively locking in the supply shortfall. Readers must understand the sheer volume of missing supply to contextualise why petroleum valuations are surging and why short-term market corrections remain highly unlikely.

When big ASX news breaks, our subscribers know first

Onshore Capacity Limits and the Impending Containment Deadline

Market dynamics ultimately bow to physical constraints on the ground, making the remaining storage timeline a critical breaking point for international energy stability. Onshore and floating storage traditionally acts as a buffer during maritime blockades by absorbing unexported crude while negotiations proceed. However, petroleum supply chains are not infinitely elastic, and the physical reality of limited tanks eventually dictates production decisions.

Iran has historically demonstrated resilience in surviving extraction halts through expansive floating reserves, but the current situation exposes an acute lack of available containment facilities. The industry is closely monitoring satellite imagery of these floating reserves, as they represent the final shock absorber before onshore limits are breached. According to late April 2026 intelligence from Kpler, the nation’s unused oil storage has rapidly shrunk to a viable timeline of just 12-22 days.

Currently, the country possesses around 8-10 million barrels of available onshore spare capacity. The current blockade threatens to remove roughly 2.0 million barrels per day from global markets altogether.

| Production Metric | Volume / Timeline Estimate |

|---|---|

| Pre-Blockade Export Baseline | 1.7 to 1.8 million barrels per day |

| Available Onshore Spare Capacity | 8-10 million barrels maximum limit |

| Remaining Storage Timeline | 12-22 days until critical threshold |

| Total Global Market Removal Threat | 2.0 million barrels per day |

This specific calendar-based countdown provides investors with a critical metric to monitor over the coming weeks. If storage fills entirely within the next 13 days, the industry is on the brink of forced operational changes.

Mechanics of Well Shut-Ins

When an active well has nowhere to pump its crude, operators face the mechanical consequence of reaching maximum containment thresholds. The resulting pressure forces engineers to initiate deliberate flow reductions or mandate complete well shut-ins across the network. Experts warn that this process threatens irreversible damage to mature oil fields.

Mature fields rely on delicate subterranean pressure balances to maintain steady flow rates. Once shut down, the natural geological pressure drops, and engineers must deploy expensive artificial lift mechanisms to re-establish the baseline flow. Restarting these mature fields requires massive long-term capital expenditure to restore necessary reservoir pressure safely.

The mechanical reality dictates that a temporary geopolitical blockade could easily translate into permanent production degradation. This physical limitation effectively places a hard deadline on the diplomatic standoff before irreversible infrastructure damage occurs.

For investors wanting to understand how these physical supply threats affect equity valuations, our full explainer on stock market geopolitical risk examines why major indices appear to be pricing in a rapid conflict containment that logistics data does not support.

Analysing the Upcoming UAE Departure and Coalition Instability

The international petroleum coalition is fracturing at exactly the moment global markets demand structural supply stability. In a major shift for global energy markets, the United Arab Emirates announced its official departure from the major oil cartel, effective May 2026. This pending exit forces investors to look beyond the immediate Middle Eastern standoff to understand a permanent restructuring of cartel dynamics.

According to data, the departure removes the coalition’s existing output capabilities in a single motion. The UAE aims to aggressively increase its daily extraction once freed from internal quotas. Industry experts note that this exit will likely boost overall production and could help lower global petroleum prices over the long term.

The planned UAE departure from OPEC quotas empowers the nation to pursue higher independent output, fundamentally altering the strategic balance among major Middle Eastern producers.

While this increased output offers a theoretical short-term benefit, experts caution that the geopolitical and institutional fallout will be significant. The primary consequences of this institutional shift include:

Severely strained diplomatic and economic relations with Saudi Arabia over competing production quotas. A fundamental weakening of the cartel’s historical pricing power and broader geopolitical influence. * The creation of a potent catalyst that could trigger a cascade of other member states exiting the coalition.

This permanent restructuring will alter baseline petroleum pricing mechanisms for years to come. The decision reflects a broader strategic shift where nations prioritise sovereign market share over collective price maintenance.

The loss of coordinated supply management removes the traditional floor beneath crude valuations once the current maritime crisis inevitably resolves. Capital allocators must recalibrate their long-term models to account for a fragmented supply environment where major producers operate independently.

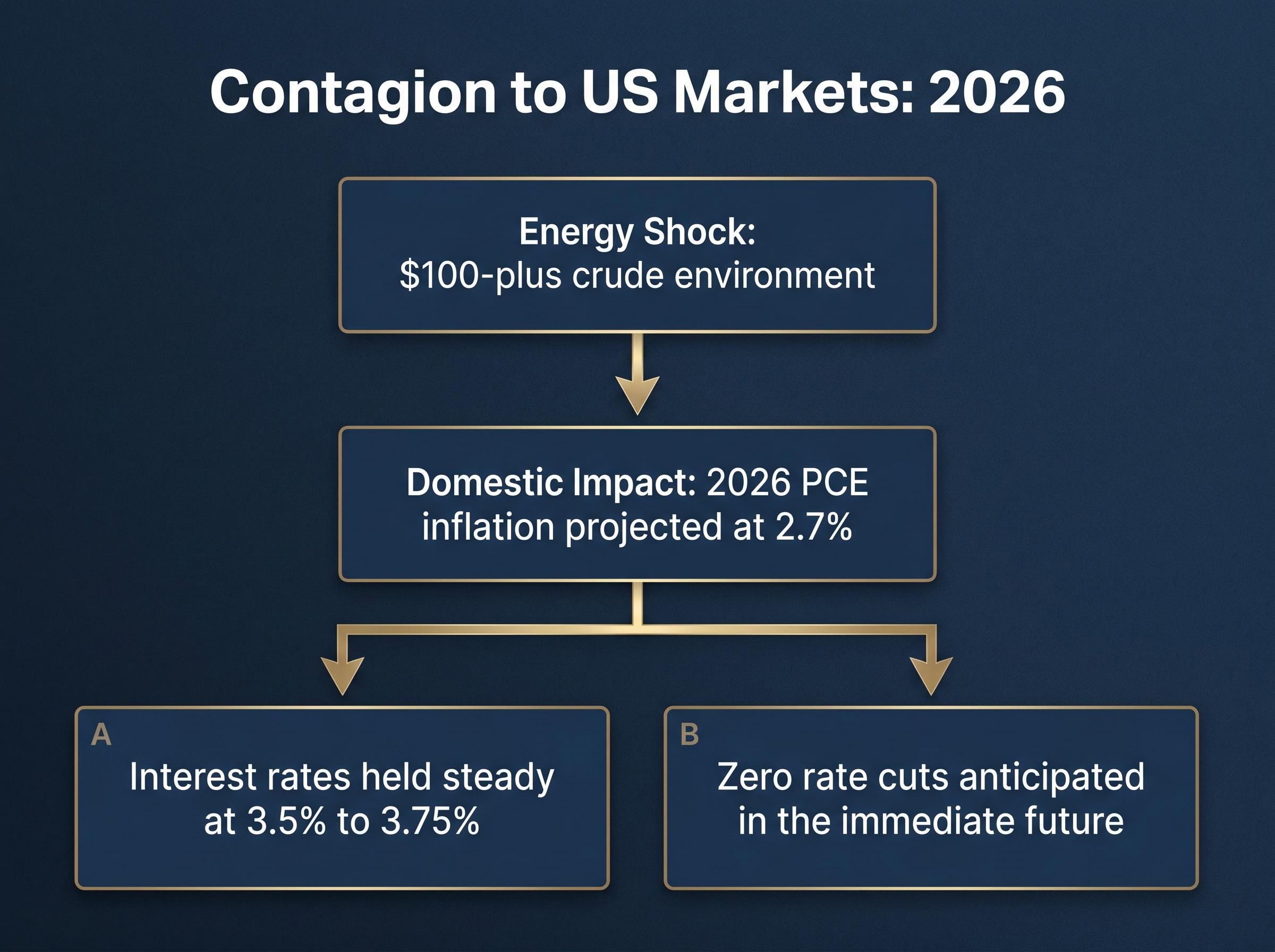

Contagion to US Markets and Federal Reserve Policy Limits

The overseas commodity crisis directly impacts domestic wallets by dictating the macroeconomic borrowing costs set by the Federal Reserve. Prolonged restrictions in the Strait of Hormuz and massive oil spikes are acting as primary drivers of global energy inflation. These spikes include a severe 15% jump immediately following the failure of diplomatic talks on April 12, 2026.

This persistent, oil-driven inflation threat forces the central bank into a highly defensive posture regarding interest rates. Financial market analysts now project that Personal Consumption Expenditures inflation will reach 2.7% for 2026, driven almost entirely by the energy component. The energy component of the PCE index is particularly sensitive to these maritime chokepoints, as transportation and manufacturing sectors pass elevated fuel costs directly to end consumers.

This stubbornly high inflation metric eliminates the mathematical possibility of near-term monetary relief. Consequently, financial markets anticipate zero rate cuts in the immediate future due to the ongoing energy crisis. The transmission mechanism from foreign supply blockades to domestic borrowing costs is operating with brutal efficiency.

Expectations for the Upcoming FOMC Meeting

The Federal Reserve is widely expected to hold interest rates steady at 3.5% to 3.75% during Chairman Jerome Powell’s upcoming final meeting. Traders are closely monitoring the specific language the committee will use regarding imported inflation risks and commodity-driven price instability. The outgoing chairman is managing a massive supply-side shock, drawing stark parallels to historical instances of energy-driven stagflation.

This anticipated policy hold coincides directly with mega-cap tech earnings reports, creating a volatile trading session as investors weigh artificial intelligence infrastructure spending against persistent macroeconomic headwinds.

Past performance does not guarantee future results, and financial projections regarding central bank policy are subject to market conditions and rapidly changing geopolitical risk factors.

This dynamic translates foreign policy deficits into the precise borrowing conditions US consumers and corporate entities will face throughout the remainder of 2026. The central bank remains essentially paralysed, unable to stimulate the domestic economy while international commodity markets dictate base inflation levels.

Long-Term Trajectory of a Constrained Energy Environment

The global economy faces an unprecedented convergence of maritime blockades, depleted storage capacity, and structural cartel fragmentation. The critical 12-22 day countdown window serves as the ultimate forward-looking metric for readers to watch as Iranian storage approaches its absolute physical limits. If diplomatic channels fail to open a release valve, the resulting well shut-ins will permanently alter global supply capacity.

Concurrently, the Federal Reserve remains strategically paralysed by the inflationary pressures of a $100-plus crude environment. This guarantees a sustained 3.5% to 3.75% interest rate environment for the foreseeable future, restricting corporate growth.

Financial markets have sharply adjusted their interest rate projections in response to this dynamic, with current modeling suggesting that monetary easing will not realistically begin until late 2027.

The permanent restructuring of Middle Eastern output will outlast the current diplomatic impasse. Investors must prepare for an environment where central banks cannot provide liquidity support without immediately exacerbating energy-driven inflation.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.