AI Chip Rally Up 50% in Two Months: Barclays Sees Cracks

4 hrs ago

HSBC’s chief multi-asset strategist is not worried about a market crash. He is worried about a rally that feels too good. On 4 June 2026, Max Kettner published a strategy note maintaining HSBC’s aggressive pro-risk positioning across equities and credit, then immediately identified the one scenario that would force the firm to abandon it: a broad, simultaneous rally sparked by positive Middle East developments. The warning did not emerge from routine scenario planning. It came as a direct response to client questions about what it would take to change the firm’s bullish conviction, making it an unusually candid disclosure of internal trigger points. What follows unpacks why HSBC treats a euphoric rally as more dangerous than a geopolitical shock, how the firm’s positioning model converts good news into a sell signal, and what that framework means for investors currently riding the pro-risk trade.

Kettner’s 4 June 2026 note is not hedged or tentative. HSBC’s multi-asset team is positioned aggressively for risk, and the note reaffirms that stance across asset classes with no immediate plans to reduce exposure. The conviction is deliberate and maintained, not a drift into risk by default.

HSBC’s maximum equity overweight is anchored not in directional optimism alone but in a specific reading of sentiment indicators and systematic positioning data that, as of the May 2026 Monthly View, had not yet reached the extreme thresholds Kettner associates with elevated drawdown risk.

What makes the note unusual is the catalyst behind it. Clients, many of them benefiting directly from the pro-risk positioning, kept asking the same question: what would it take for HSBC to change its mind? Kettner responded by structuring the note around two categories: risks the firm takes seriously and risks it dismisses.

The note’s candour is itself the story. Institutional research rarely maps its own exit conditions with this level of specificity; Kettner’s response tells investors not just where HSBC stands, but approximately where HSBC would stop standing there.

That transparency has practical value. Investors following HSBC’s positioning now know the thesis has defined limits rather than open-ended conviction, and they can monitor whether those limits are approaching.

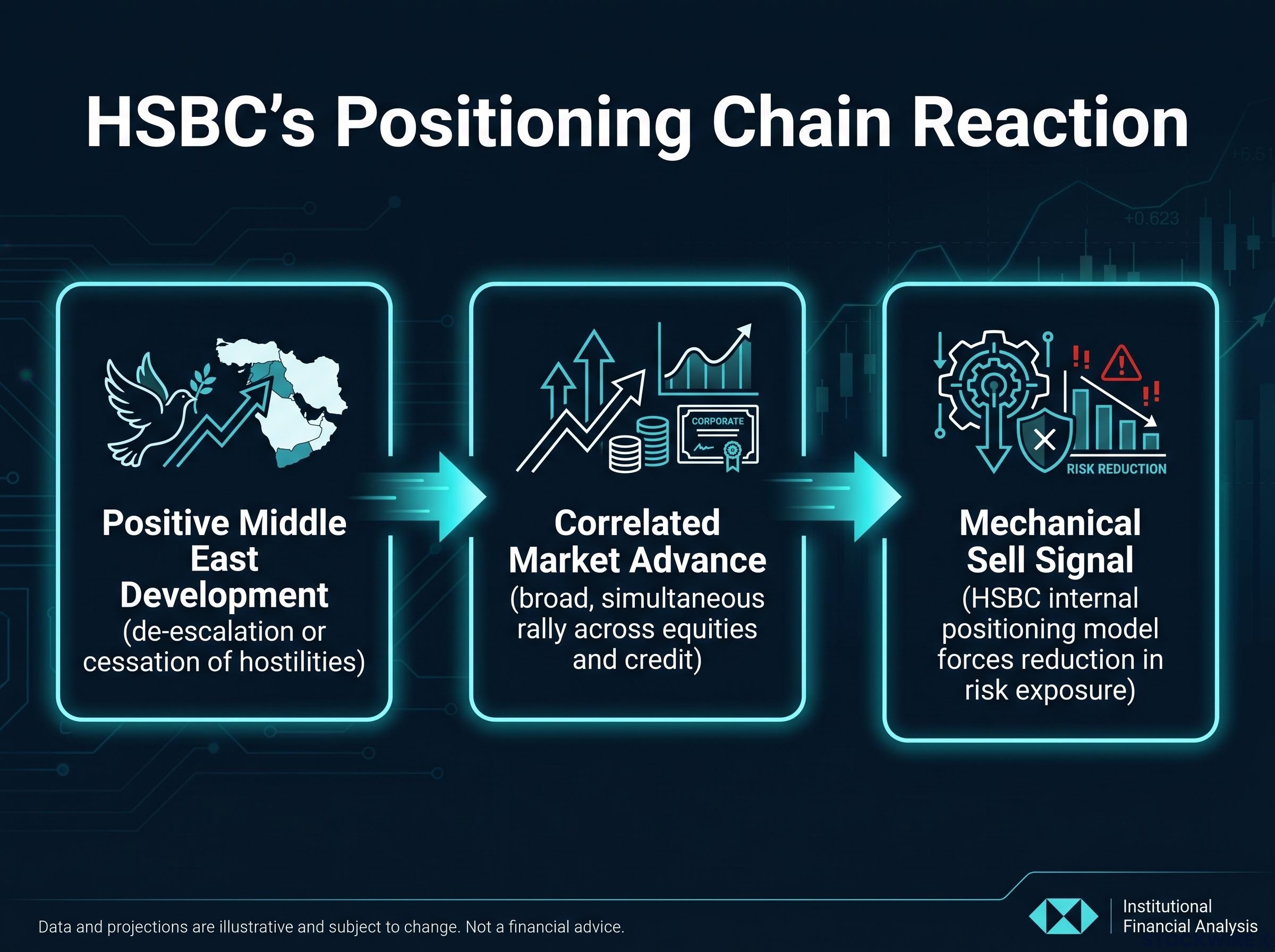

The counterintuitive core of Kettner’s warning requires a precise sequence to make sense. It is not a general unease about markets being too high. It is a specific causal chain with identifiable steps.

The distinction between the second and third steps matters. The rally itself does not cause losses for investors already positioned for risk. It generates gains. The problem is what comes next: the positioning signal the rally produces. When aggregate exposure across asset classes reaches extreme levels simultaneously, the model reads that as over-extension and flags it as a point to reduce, not add.

HSBC’s stated view is that this upside-driven positioning risk is the firm’s primary near-term concern. Not a recession. Not a rate shock. Not a geopolitical escalation. The risk is the market’s collective reaction to good news, specifically the over-positioning that a feel-good rally would produce.

On the surface, the phrase “upside risk” sounds like a contradiction. Risk, in most investors’ experience, means losing money. A rally is supposed to be the reward, not the threat.

In professional portfolio strategy, the concept operates differently. Risk-parity and volatility-targeting strategies, the quantitative frameworks that govern how large institutional portfolios allocate capital, respond mechanically to changes in cross-asset correlations and aggregate exposure levels. When equities and credit rally simultaneously, the diversification benefit that normally separates those asset classes compresses. The portfolio’s aggregate risk score rises, not because of losses, but because of correlated gains, and the model responds by forcing exposure reduction at the worst possible moment: near the top.

| Conventional risk signal | Positioning-model risk signal |

|---|---|

| Rate shock triggers a sell-off | Euphoric simultaneous rally triggers over-extension |

| Geopolitical escalation suppresses risk appetite | Geopolitical de-escalation produces sentiment extreme |

| Fundamental deterioration drives losses | Positioning concentration forces mechanical selling |

HSBC is not the only institution that treats extreme bullishness as a technical warning.

BofA’s Bull and Bear Indicator reached 8.0 in late May 2026, its 18th such reading since 2002, a threshold that has historically preceded average global equity declines of 2-3% within three months and that operates on precisely the same contrarian logic HSBC’s positioning model applies: extreme aggregate enthusiasm is the sell signal, not fundamental deterioration.

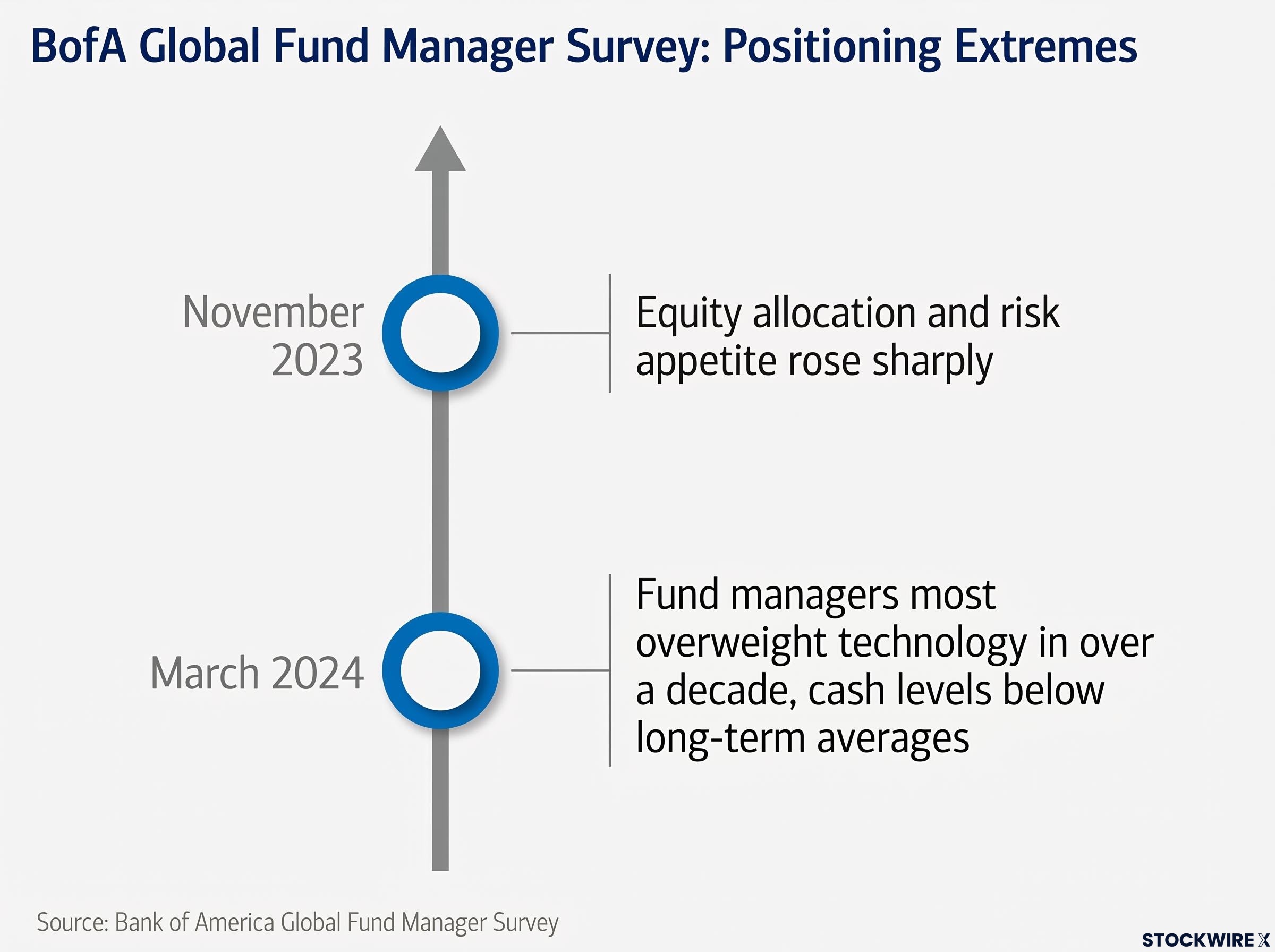

Comparable framework: Bank of America’s Bull and Bear Indicator operates on a similar principle. When the indicator approaches its upper bound, BofA treats the reading as a contrarian sell signal rather than a bullish confirmation. The BofA Global Fund Manager Survey reported in November 2023 that equity allocation and risk appetite had risen sharply; by March 2024, fund managers were the most overweight technology in over a decade, with cash levels below long-term averages.

HSBC’s concern is not fundamental deterioration. It is the positioning extreme that a broad rally would create, the same type of condition BofA’s framework is designed to flag.

Kettner’s note does not ignore conventional risks. It acknowledges them and then systematically sets them aside. This is a deliberate analytical choice, not an oversight.

HSBC’s assessment is that geopolitical developments, taken on their own terms, do not currently represent a high-level threat to risk assets. Two conditions underpin that view:

The distinction at the heart of the note is worth stating plainly. Geopolitical escalation is not the concern. Geopolitical de-escalation producing euphoria is the concern. The conventional worry, that a crisis in the Middle East sends markets lower, is the scenario HSBC has evaluated and dismissed. The unconventional worry, that a resolution in the Middle East sends markets too high too fast, is the one keeping Kettner’s team watchful.

By clearing the conventional risks from the board in an ordered way, the note sharpens rather than softens its central argument. The bullish thesis is intact precisely because the usual threats are manageable. The threat that is not manageable sits on the other side of the ledger.

HSBC’s warning does not mean investors should exit risk assets today. The firm’s pro-risk stance remains intact, and the sell signal Kettner described is conditional. It requires a specific, not-yet-triggered scenario: a broad, simultaneous rally across both equities and credit driven by a credible Middle East development.

The note does not argue that a positive geopolitical headline alone is sufficient to trigger the exit. A Middle East development that lifts equities without producing a corresponding credit rally, or one that generates a brief sentiment spike before fading, would not meet the threshold. The trigger is breadth and simultaneity, not a single headline.

The practical value of Kettner’s transparency is that it converts an abstract institutional risk model into a set of observable conditions. Three indicators deserve attention:

Crowded equity positioning is not unique to HSBC’s internal model: Wolfe Research analyst Chris Senyek identified in May 2026 that U.S. equity exposure had reached its most extended levels since late 2021, with BofA, Goldman Sachs, and CFTC data all corroborating concentrated long exposure in AI and technology names that would amplify any forced unwind.

The warning itself is a form of risk management guidance. It tells investors approximately where the exit signal lies before it is triggered, an unusual degree of institutional transparency that is more useful than a general caution to “stay vigilant.”

For investors currently holding the pro-risk trade who want a practical framework for acting on the exit conditions Kettner described, our dedicated guide to rebalancing after a multi-year equity rally covers how to identify portfolio drift toward equity overweight, when a 5% threshold should trigger a rebalance, and how to execute the reduction tax-efficiently before a mechanical sell signal forces the move at an elevated level.

HSBC’s note illustrates a broader principle that extends beyond a single firm’s positioning model. In a mature bull market where conventional risks have been identified, evaluated, and absorbed into pricing, the most dangerous risks are often the ones that do not look like risks at all. Sophisticated positioning models at major institutions are specifically calibrated to catch the euphoria that consensus overlooks, precisely because fundamental analysts tend to focus on downside catalysts.

The fact that client pressure prompted this disclosure carries its own signal. Investors close to the trade are already sensing the limits of the rally, even if they cannot articulate exactly where those limits sit. The question they kept asking Kettner, “what would make you change your mind?”, is itself evidence of a market that has begun to price in its own success.

BofA’s contrarian-sell framework reinforces the same institutional logic from a different angle. When positioning models and sentiment surveys converge on the same reading, the signal sharpens. One bank’s warning is a data point. Two banks’ frameworks producing parallel logic is a pattern worth internalising.

The forward-looking implication is straightforward. Middle East de-escalation, if it comes, should prompt investors to watch positioning signals as closely as they watch the geopolitical headlines generating the move. The headline will tell you what happened. The positioning data will tell you what it means for your portfolio.

HSBC’s warning inverts the conventional risk map. The danger is not outside the market. It is inside the market’s own enthusiasm, waiting to be triggered by precisely the kind of news investors are hoping for.

No sell signal has been triggered. The pro-risk stance is intact. But the exit map is now visible, and its coordinates are specific: a broad, simultaneous advance across equities and credit, pushed by a credible Middle East development, generating positioning extremes that HSBC’s model cannot ignore.

Middle East developments, positive or negative, should now be read as positioning events as much as geopolitical ones. The next major headline from the region will move markets. What matters more is whether it moves positioning models into territory that forces the very institutions holding the trade to step away from it.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements are speculative and subject to change based on market developments and company performance.

HSBC's multi-asset strategist Max Kettner warned on 4 June 2026 that a broad, simultaneous rally across equities and credit, sparked by positive Middle East developments, is the firm's primary near-term concern because it would push internal positioning models into sell-signal territory.

Upside risk in portfolio strategy refers to the danger that a strong, correlated rally across asset classes compresses diversification benefits and pushes a portfolio's aggregate risk score so high that quantitative models are forced to mechanically reduce exposure near market peaks.

HSBC would reduce its aggressive pro-risk positioning if a credible Middle East de-escalation event produced a broad, simultaneous rally across both equities and credit, pushing internal positioning models to extreme over-extension levels; a rally in equities alone or a brief sentiment spike would not meet that threshold.

Both frameworks apply contrarian logic, treating extreme aggregate enthusiasm as a sell signal rather than a bullish confirmation; BofA's Bull and Bear Indicator reached 8.0 in late May 2026, a level that has historically preceded average global equity declines of 2-3% within three months, mirroring the over-extension logic built into HSBC's positioning model.

Investors should watch for simultaneous equity and credit rallies on a single geopolitical catalyst, the speed and magnitude of any sentiment repricing, and positioning survey data approaching historic over-extension levels comparable to the March 2024 BofA reading where fund managers were their most overweight technology in over a decade.