Nvidia Clears All Three HBM4 Suppliers for Vera Rubin Platform

1 hr ago

Micron Technology secured its place as an Nvidia Vera Rubin HBM4 supplier on 5 June 2026, a confirmation that positions the company inside one of the most consequential AI infrastructure buildouts in semiconductor history. The stock fell 7.74% on the same session. That disconnect, between a long-term supply chain win and a sharp single-day decline, captures the forces colliding across the AI trade today. Two separate catalysts drove the selling: a Broadcom earnings hangover that reset sector sentiment earlier in the week, and a May jobs report that printed at nearly double the expected payroll gain, compressing risk appetite across growth equities. What follows unpacks why the AI stock selloff is happening, what Micron’s certification actually signals about Vera Rubin supply chains, and what investors should weigh when a stock drops on what looks like good news.

Two catalysts converged on 5 June 2026, each powerful enough to move markets independently. Together, they produced the sharpest single-session decline in AI-related equities in months:

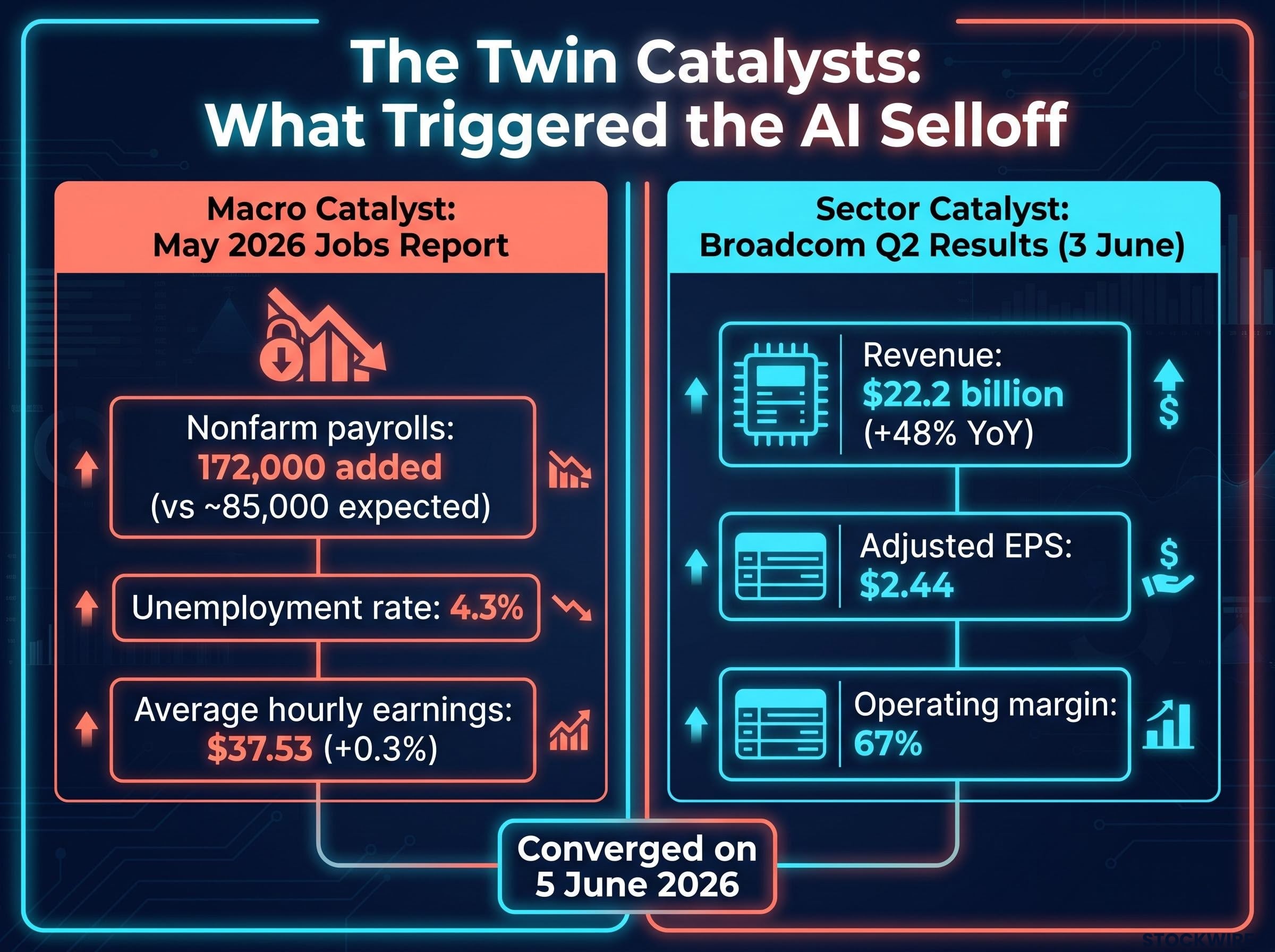

The May 2026 jobs report printed at 172,000 nonfarm payrolls, nearly double the 85,000 consensus estimate, with April’s figure simultaneously revised upward by 64,000, confirming that spring 2026 labour market strength had been materially underestimated at first release.

172,000 jobs added in May 2026, against expectations of approximately 85,000. The unemployment rate held steady at 4.3%. Average hourly earnings rose 0.3% to $37.53.

Neither catalyst is company-specific to Micron. Both are macro and sector-level forces washing over the entire AI equity complex. The jobs number landed first on Friday morning, hitting futures that were already soft from the Broadcom-driven sentiment shift. Within the first hour of trading, the selling broadened from semiconductor names into the wider technology sector.

The distinction matters. This is not a story about one company losing investor confidence. It is a story about an entire sector repricing simultaneously under two separate sources of pressure.

Broadcom’s fiscal Q2 headline numbers were, by any standalone measure, strong.

| Metric | Result | Significance |

|---|---|---|

| Revenue | $22.2 billion | Up 48% year over year |

| Adjusted EPS | $2.44 | Beat analyst consensus estimates |

| Operating margin | 67% | Reflects pricing power and scale |

A 48% revenue increase and a margin approaching 70% would, in most quarters, have been celebrated. The problem was positioning. AI semiconductor stocks had reached record highs heading into the report, and market expectations were priced well beyond the consensus numbers analysts published.

Broadcom’s fiscal Q2 2026 results, released via official press release on 3 June, confirmed revenue of $22.2 billion and adjusted diluted EPS of $2.44, figures that beat analyst consensus yet still failed to satisfy a market that had priced in a more euphoric outcome.

The result was a pattern familiar to anyone who has watched a momentum trade mature: the numbers beat estimates, yet the stock sold off. Analyst commentary described AI semiconductor demand as “insatiable,” but that word landed alongside a different discussion, one about whether peak-cycle narratives and rotation risk were now live concerns rather than theoretical ones. The earnings were strong. The market had already priced stronger.

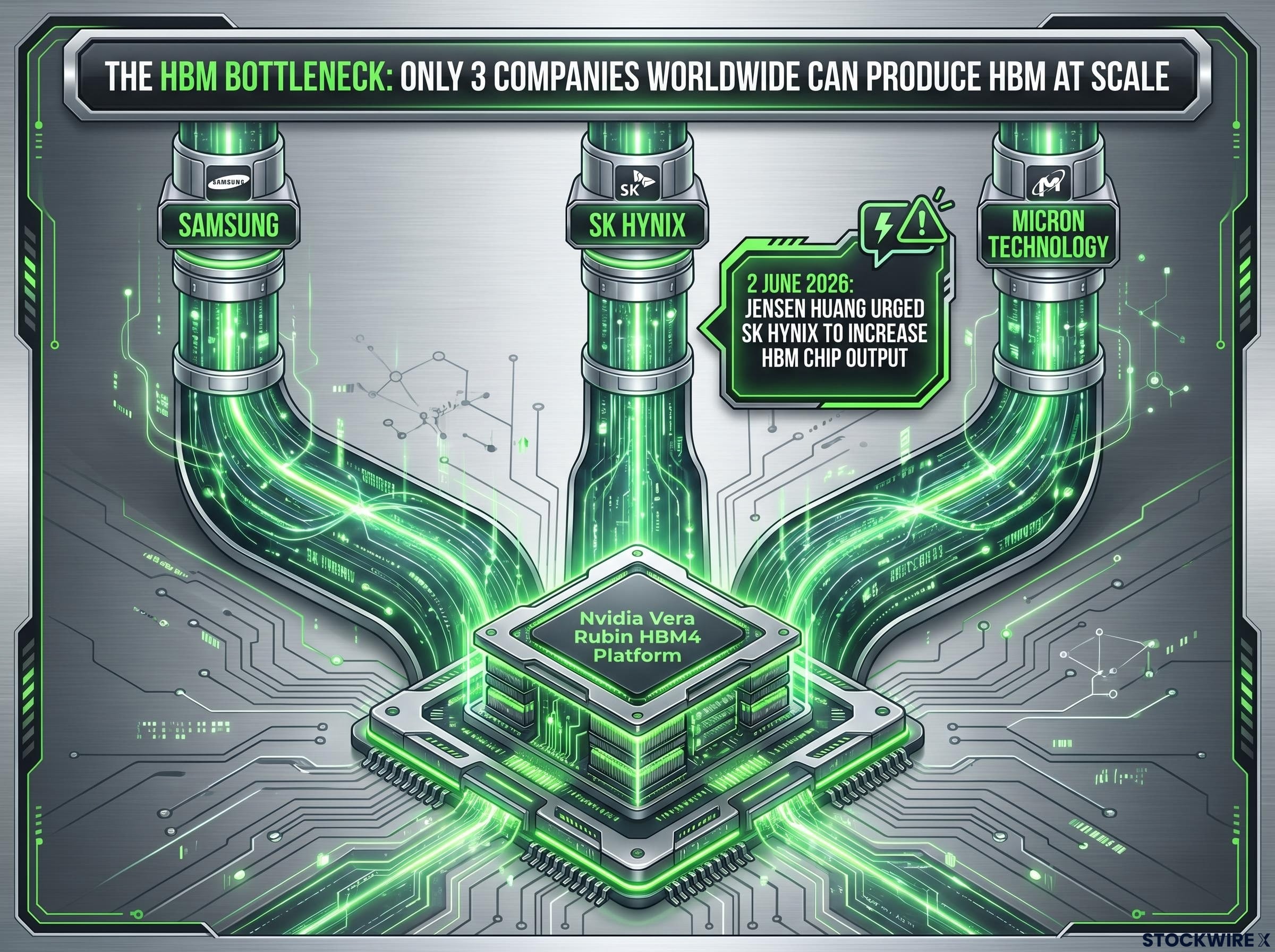

Nvidia CEO Jensen Huang confirmed on 5 June 2026 that Samsung, SK Hynix, and Micron Technology have all been certified to supply HBM4 memory for the Vera Rubin platform. It was the kind of announcement that, in isolation, would be expected to lift a supplier’s stock.

Micron had already fallen approximately 4.4% in pre-market trading before the regular session began. By the close, the decline reached 7.74%.

The mechanism is straightforward, if counterintuitive. When institutional investors de-risk in response to macro catalysts, they sell liquid large-cap technology names regardless of daily company-specific news. Certification does not change Micron’s near-term earnings. It is a long-duration revenue signal, confirming the company has cleared Nvidia’s technical and yield qualification bar. The market on 5 June was pricing near-term rate risk and sector sentiment, not long-term supply chain positioning.

Vera Rubin is Nvidia’s next-generation AI accelerator platform, and HBM4 memory is a critical component of its compute architecture. Micron’s certification confirms it has secured a position in one of the most capital-intensive semiconductor supply chains being built today.

Jensen Huang’s public statement on 2 June, urging SK Hynix to increase HBM chip output, underscored that demand is outpacing current manufacturing capacity. Only three companies worldwide can produce HBM at the scale Nvidia requires. Micron is now confirmed as one of them.

The term “HBM” has appeared in headlines with increasing frequency over the past year. What it actually refers to, and why it matters, is less widely understood.

The HBM supply constraint binding AI infrastructure deployment runs deeper than near-term capacity allocation: SK Hynix projects global DRAM tightness through 2030, HBM inventory across the industry sits at just 3-4 weeks, and Google CEO Sundar Pichai has publicly identified memory availability, not capital, as the primary limiter on AI expansion even with approximately $180 billion in planned annual capex.

On 2 June 2026, Jensen Huang publicly urged SK Hynix to increase its HBM chip output, stating that worldwide semiconductor supply remains constrained.

South Korea’s benchmark equity index fell more than 5% on 5 June, a decline that reflects the country’s concentrated exposure to the semiconductor companies servicing Nvidia and the broader AI buildout. When the AI trade sells off, the supply chain geography absorbs the impact disproportionately.

The AI selloff on 5 June was not contained to U.S. exchanges. It propagated through global supply chains, with the sharpest effects landing on the most concentrated supplier economies.

South Korea’s outsized decline has a structural explanation. The country’s equity market carries concentrated exposure to the semiconductor companies servicing Nvidia and the broader AI infrastructure buildout. When AI-sector sentiment shifts, that concentration translates directly into benchmark-level moves.

AI semiconductor sentiment shocks originating in South Korea have demonstrated a consistent pattern in 2026: a single unverified social media post from a presidential aide erased more than $300 billion in market value on 12 May before three government bodies issued coordinated denials within hours, showing how concentrated supply chain geography translates directly into benchmark-level volatility on the Kospi.

Jensen Huang was physically in South Korea during this period, meeting with the chairs of SK Group, Samsung, LG Group, Hyundai Motor Group, and Naver. Supply chain relationships were being negotiated in person even as markets priced the sector lower.

The factors driving today’s decline and the factors supporting the AI infrastructure thesis operate on different time horizons. Separating them is the analytical task investors face this week.

Short-term headwinds:

Long-term tailwinds:

There is a legitimate concern embedded in today’s action. When expectations are priced to perfection and any negative catalyst triggers outsized selling, that itself is a valuation signal. AI-related equities had reached record highs prior to the 4-5 June pullback. The speed of the reversal suggests the trade had been carrying more fragility than daily price action had revealed.

AI equity sentiment heading into the 4-5 June pullback was already flashing caution: Goldman Sachs’s U.S. Equity Sentiment Indicator had reached 1.7, a level historically associated with below-average S&P 500 returns over the following 2-8 weeks, with semiconductor sector conviction having jumped from 24% to 73% in a single fund manager survey cycle, a positioning extreme that amplifies the speed of any reversal.

Micron’s session captures the tension in miniature: a confirmed long-term HBM4 supplier and a 7.74% single-session decliner on the same day. That is not a contradiction. It is two different time horizons colliding in a single price.

Micron enters 6 June as a confirmed Nvidia Vera Rubin HBM4 supplier and as a stock that just lost nearly 8% in a single session. The macro factors that drove the selloff, a hot jobs report, a Broadcom sentiment reset, and compressed rate-cut expectations, are not structural changes to the AI infrastructure demand thesis.

The open question is whether today’s price action represents a macro-driven opportunity in a fundamentally strong supply chain position, or an early signal that AI equity valuations are entering a period of sustained recalibration. That question will not be answered by a single session. It will be answered by whether the next round of earnings, deployment timelines, and HBM demand data confirm or contradict the long-term thesis that certified suppliers like Micron are positioned to serve.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

Two catalysts converged on the same session: a May 2026 nonfarm payrolls report that printed at 172,000, nearly double the expected 85,000, and a sentiment reset triggered by Broadcom's fiscal Q2 earnings, which beat estimates but failed to satisfy a market priced for a more euphoric outcome.

HBM4 is the latest generation of high-bandwidth memory, a stacked chip architecture that places memory directly adjacent to the processor to dramatically increase data transfer speeds; it is a hardware requirement for current-generation AI accelerators like Nvidia's Vera Rubin platform, and only three companies globally can produce it at scale.

The decline was driven by macro and sector-level forces, not company-specific news; institutional investors de-risked across liquid large-cap technology names in response to the jobs report and Broadcom sentiment shift, while Micron's HBM4 certification is a long-duration revenue signal that does not affect near-term earnings.

The stronger-than-expected payrolls print reinforced expectations that interest rates will remain restrictive for longer, compressing risk appetite and putting downward pressure on growth equities, including AI and semiconductor stocks that are sensitive to rate expectations.

Nvidia CEO Jensen Huang confirmed on 5 June 2026 that Samsung, SK Hynix, and Micron Technology have all been certified to supply HBM4 memory for the Vera Rubin platform, making these three companies the sole qualified suppliers for one of the most significant AI infrastructure buildouts in semiconductor history.