The MSCI World Semiconductors index has surged roughly 50% in just two months, marking the second-largest two-month gain since November 2001. On 5 June 2026, Barclays strategists led by Emmanuel Cau published a note identifying multiple signs that the AI-driven chip rally may be running out of fuel.

The warning is specific and technical: stretched positioning among algorithmic momentum funds, an incoming wave of technology IPOs expected to absorb liquidity, and overheating concentrated in a narrow slice of global markets. What follows unpacks exactly what Barclays flagged, why the geographic and positioning picture matters for investors holding semiconductor and AI-adjacent equities, and what signals to watch in the weeks ahead.

A 50% surge in two months: putting the semiconductor rally in historical context

The numbers alone command attention. The MSCI World Semiconductors index gained approximately 50% over a two-month period ending in early June 2026, a move so large it ranks second only to the semiconductor rally that followed November 2001.

Historical context: The current two-month semiconductor gain is the second-largest recorded since November 2001, according to Barclays strategists led by Emmanuel Cau.

That comparison matters. The 2001 rally came during a recovery from a severe technology crash, a period when semiconductors were repricing from deeply depressed levels. The current surge, by contrast, arrives after an extended period of AI-driven demand narratives that have already pushed chip valuations well above their long-term averages.

The MSCI World Semiconductors index methodology classifies constituents using GICS sector definitions, capturing companies across the full semiconductor equipment and fabrication value chain, which means the index’s 50% two-month gain reflects concentrated exposure to the precise segment of global equities most directly tied to AI infrastructure buildout.

Barclays characterises the rally as AI-driven, connecting surging demand for artificial intelligence infrastructure to the index performance. The link between AI spending and chip equities is real, but the scale of the move has pushed beyond what even strong fundamental demand typically produces in two months. For investors who have watched the climb, the historical framing provides a baseline: this is not a routine bull run. It is a statistically rare event, and rare events invite scrutiny.

The AI supercycle thesis behind the rally rests on verifiable data points: Microsoft and Meta alone have committed over $160 billion in AI infrastructure capital expenditure for 2026, and Bank of America projects global chip sales of approximately $975 billion for the year, roughly 25% higher year on year, figures that explain why the move has fundamental backing even as positioning indicators flash caution.

When big ASX news breaks, our subscribers know first

How algorithmic momentum funds are signalling a shift in rally fuel

One of the sharpest warnings in the Barclays note concerns positioning among commodity trading advisors (CTAs) and other fast-money participants. These funds were a significant driver of the semiconductor rally’s upswing, and Barclays identifies their positioning as now stretched and losing momentum.

The distinction matters. CTA positioning is not a vague sentiment indicator. It describes a specific, measurable condition in which one class of market participant has accumulated large directional bets, and the mechanics of how those bets unwind carry real consequences for listed chip equities.

What are CTAs and why do their flows matter?

CTAs are systematic, trend-following funds that use algorithmic models to take positions in the direction of prevailing market momentum. Several characteristics make their behaviour particularly relevant to the current semiconductor rally:

- Trend-following mandate: CTAs buy assets that are rising and sell assets that are falling, purely based on price signals rather than fundamental analysis.

- Algorithmic execution: Positions are opened and closed by models, meaning reversals can happen quickly across the entire CTA complex when momentum signals shift.

- Amplification effect: CTA participation amplifies upward moves when momentum is positive; elevated long positioning creates a concentrated source of potential selling if models trigger a reversal.

- Leverage capacity: Many CTAs operate with leverage, meaning their selling pressure during a reversal can exceed the capital they initially deployed.

Barclays frames the current CTA positioning not as a prediction of collapse but as a sign that one of the rally’s key fuel sources is becoming depleted. When trend-following capital has already been deployed, the marginal buyer that sustained the rally’s momentum is harder to find.

Technology capital raises set to compete for the same investor dollars

The second catalyst Barclays identifies is structural rather than speculative: a wave of sizeable technology-sector IPOs and capital raises expected in the coming weeks.

The concern is not about sentiment. It is about capital allocation mechanics. Large IPOs and secondary offerings compete for the same pool of institutional investment capital currently flowing into listed chip and AI stocks. When a major technology company prices a new listing, institutional investors must source the capital to participate, and that capital often comes from trimming existing positions.

The step-by-step mechanism works as follows:

- A technology IPO is priced, typically requiring large institutional allocations at or before listing.

- Institutional investors reallocate capital from existing positions, including listed semiconductor holdings, to fund the new allocation.

- Net selling pressure emerges in listed chip equities as capital rotates toward the new issuance.

- Momentum indicators soften as the incremental demand that sustained the rally is redirected.

Barclays identifies this pipeline as a near-term liquidity absorption catalyst. While the specific deal names and sizes have not been disclosed publicly, the bank’s characterisation points to a meaningful volume of expected issuance. For investors holding semiconductor equities, IPO announcements in the weeks ahead may carry more significance for existing positions than the headlines about the new listings themselves suggest.

The AI IPO absorption pressure Barclays identifies is already being quantified elsewhere: Standard Chartered global CIO Steve Brice warned on 2 June 2026 that SpaceX, Anthropic, and OpenAI targeting public listings within the same compressed mid-2026 window would create market digestion difficulties across the summer months, a concern that runs in parallel with the CTA positioning risk the bank’s strategists have separately flagged.

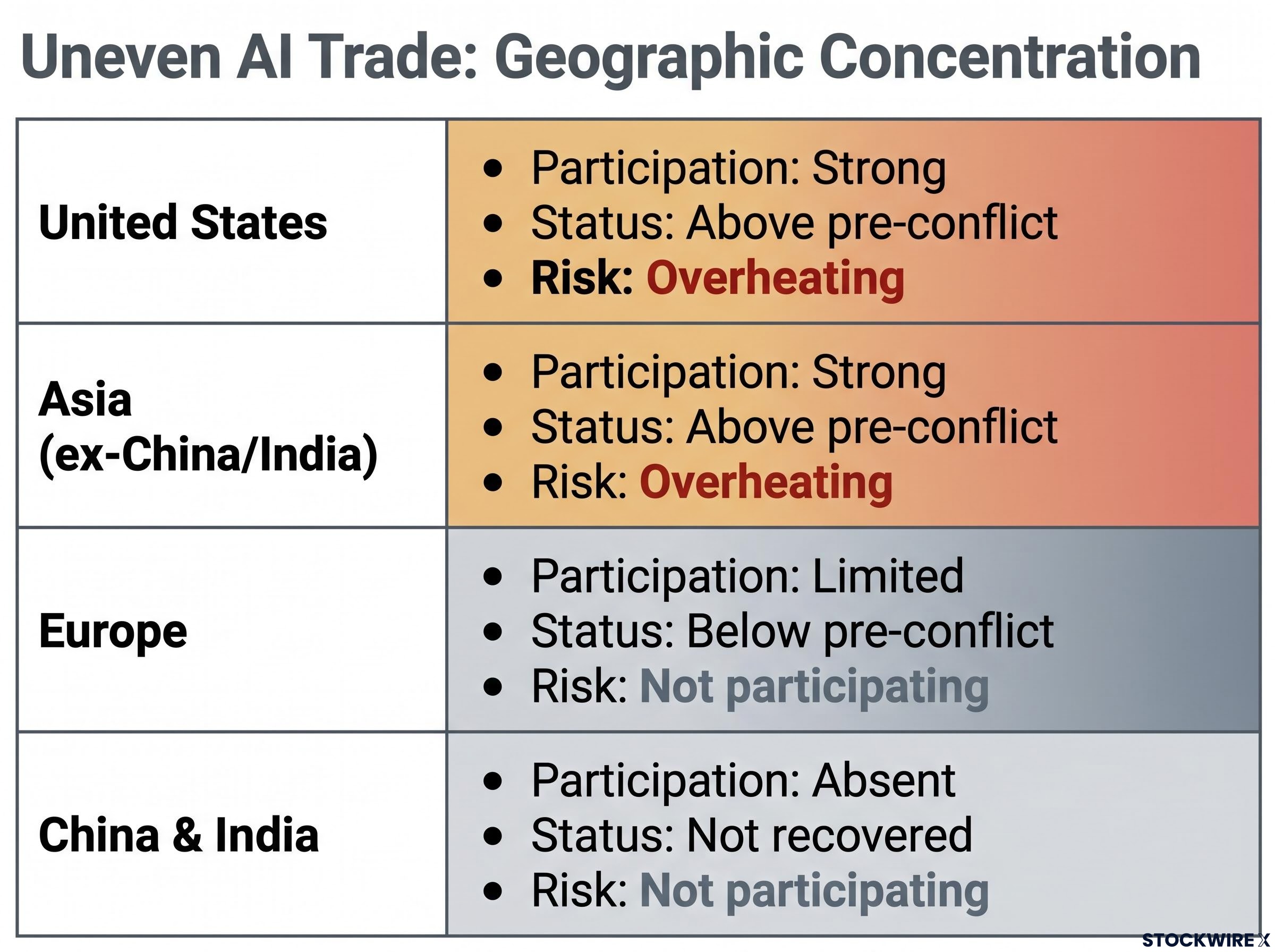

Geographic concentration reveals how unevenly the AI trade has spread

The AI chip rally has not been a global phenomenon. Barclays identifies overheating as concentrated narrowly within U.S. and Asian indices, a geographic pattern that itself constitutes a risk signal.

The markets that have not participated tell the story as clearly as those that have. European indices have broadly failed to recover to pre-conflict levels. China and India have not joined the AI-related trade. The result is a rally that looks broad from a sector perspective but is strikingly narrow when mapped geographically.

| Region | Rally Participation | Index Recovery Status | Barclays Risk Characterisation |

|---|---|---|---|

| United States | Strong | Above pre-conflict levels | Overheating identified |

| Asia (ex-China/India) | Strong | Above pre-conflict levels | Overheating identified |

| Europe | Limited | Below pre-conflict levels | Not participating |

| China | Absent | Not recovered | Not participating |

| India | Absent | Not recovered | Not participating |

A rally that is narrow is more vulnerable to reversal than one broadly distributed across regions. For globally diversified investors, the geographic picture is directly relevant to portfolio risk: exposure to U.S. and Asian semiconductor equities carries a materially different risk profile right now than European or emerging-market technology positions. Barclays also notes that both equity and bond volatility are hovering near multi-period lows as of early June 2026, a condition that can mask underlying fragility until a catalyst forces repricing.

The narrow semiconductor leadership driving global index returns in 2026 is even more concentrated than the geographic picture suggests: just 19 chip stocks representing roughly 15% of S&P 500 weight have driven approximately 70% of the index’s year-to-date market capitalisation gains, a breadth divergence so extreme that on 14 May 2026 the cap-weighted index hit an all-time high while 46 constituents simultaneously touched 52-week lows.

Calm markets and a difficult summer ahead: the case for protective positioning

Barclays’ note moves beyond diagnosis to a specific recommendation: establish hedges ahead of what the bank characterises as a historically challenging summer period for markets.

The low-volatility environment is relevant context. With equity and bond volatility near multi-period lows, the cost of establishing hedges through options or other protective structures is relatively low. That pricing dynamic means the risk-reward of hedging is more attractive now than it would be after volatility spikes, when the cost of protection rises sharply.

Seasonal context: Barclays specifically references historically challenging summer market conditions as part of its rationale for recommending hedge establishment in early June.

The three specific risk signals Barclays identifies can be summarised in plain terms:

- Stretched CTA positioning: The algorithmic, trend-following capital that fuelled the rally’s momentum is elevated and losing steam.

- Incoming IPO supply: A wave of technology capital raises is expected to absorb the institutional liquidity currently supporting listed chip equities.

- Narrow geographic concentration: The rally’s gains are concentrated in U.S. and Asian markets, with Europe, China, and India sitting on the sidelines.

It is worth emphasising what Barclays is not saying. The note is a caution signal, not a crash call. The bank does not predict an imminent collapse or assign a probability to a specific drawdown. The recommendation to hedge is framed as prudent risk management in a market where multiple indicators suggest the rally’s fuel sources are becoming depleted, not as a directive to exit AI-related equities entirely.

For investors wanting to act on the hedging recommendation rather than simply note it, our full explainer on Barclays’ lookback put strategy covers why analyst Stefano Pascale warns that standard put options carry strike drift risk in the current environment, how lookback puts remove the need to time the market peak precisely, and why equity-rate hybrid hedges are flagged for the scenario where equities and bonds fall simultaneously.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The rally is real, but so are the cracks: what to watch from here

The semiconductor rally of early 2026 is a genuine reflection of AI-driven demand. The 50% two-month move is not fabricated; the capital flows behind it are real, and the structural case for AI infrastructure spending has not disappeared.

What Barclays identifies is not a fundamental breakdown but a set of near-term conditions that warrant attention: depleted momentum fuel, incoming competition for capital, and a geographic concentration that leaves the trade exposed to region-specific shocks. The timing and depth of any reversal remain genuinely unknown. Whether the IPO pipeline materialises as expected, and whether CTA flows reverse or simply slow, are open questions.

For investors holding semiconductor and AI-adjacent equities, the practical frame is straightforward. The Barclays note is a signal to reassess positioning and hedging strategy while the cost of protection remains low. It is not a directive to sell. The weeks ahead will clarify whether these cracks widen or whether the rally finds new fuel to sustain itself.