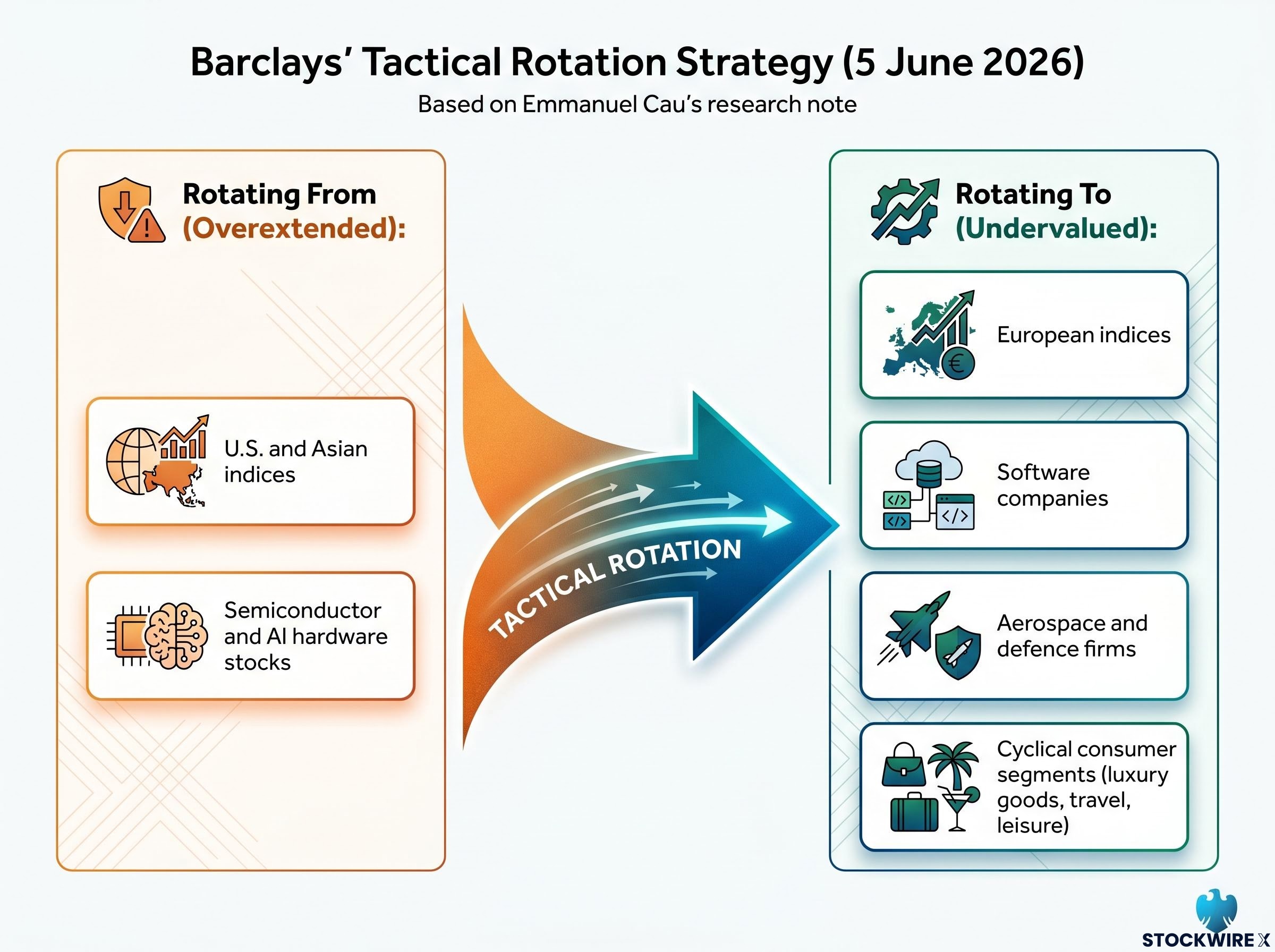

Barclays strategists are not calling time on equities. They are calling time on the part of the market that has delivered most of the gains. In a research note published 5 June 2026, lead strategist Emmanuel Cau flagged that the narrow rally concentrated in semiconductor and AI hardware stocks is showing signs of overextension, and that capital has a more productive destination if chip momentum stalls. The call lands at a moment of compounding uncertainty: a new Federal Reserve chair preparing for his first FOMC meeting, a European Central Bank expected to hike into a softening economy, and elevated oil prices sustaining inflationary pressure across major markets. The conditions that made momentum trades so rewarding are quietly shifting. What follows is a detailed examination of Barclays’ full rotation thesis, covering which sectors and regions are positioned to absorb capital, what the macro calendar means for positioning, and how investors can think about redeploying exposure without abandoning equities altogether.

The momentum trade is showing cracks, and Barclays sees where the exits lead

The starting point of Barclays’ argument is not bearish. The firm maintains a positive stance on equities overall, anchored by earnings resilience and the persistence of what it describes as a sustained investment supercycle. The concern is narrower than that: momentum within specific sectors has outrun fundamentals, and the concentration of gains has created vulnerability rather than strength.

Semiconductor stocks sit at the centre of this tension. Cau characterised the price movement in chip stocks as “parabolic,” a pace that leaves the sector exposed to a pause or correction even without a deterioration in underlying demand. If that pause arrives, it becomes the catalyst for capital to seek out undervalued areas of the market rather than simply exit equities.

Goldman Sachs identified the current AI-driven S&P 500 momentum concentration as one of only 11 comparable episodes since 1980, each of which reversed within roughly one additional month of peaking, with hedge fund gross leverage near five-year highs amplifying the potential scale of any unwind.

Deloitte’s 2026 semiconductor industry outlook identifies record AI-driven revenues concentrated in a narrow band of high-value chip categories, a revenue profile that illustrates precisely why the sector’s price momentum has outpaced the broader earnings base and left it exposed to the rerating Barclays anticipates.

The overheating, in Barclays’ framing, is geographically narrow. It is concentrated in U.S. and Asian indices, where technology weighting is highest. That geographic concentration is what opens the door to the second dimension of the rotation thesis: not just a sector shift, but a geographic one.

Barclays’ core framing: A positive overall equity outlook, grounded in earnings resilience and a sustained investment supercycle, paired with tactical rotation away from crowded momentum trades and into undervalued sectors and regions.

When big ASX news breaks, our subscribers know first

What stock market rotation looks like in practice: from chips to software, defence, and cyclicals

Barclays identifies three primary destinations for rotated capital, each with its own structural logic rather than a speculative hope that something else might work:

- Software companies: The natural adjacent trade to hardware-heavy semiconductor positions. As AI infrastructure spending matures, the value capture shifts toward the software layer that monetises the hardware buildout.

- Aerospace and defence firms: Underweighted relative to their earnings profile and geopolitical tailwinds. Sustained global defence spending creates a revenue floor that momentum-driven tech sectors lack.

- Cyclical consumer segments (luxury goods, travel, and leisure): Beneficiaries of consumer resilience outside the narrow tech trade, offering exposure to spending patterns that remain strong even as semiconductor momentum compresses.

The distinction matters. This is a within-equities rotation thesis, not a shift to cash or bonds. Barclays is not recommending a risk-off posture. The firm is arguing that the same earnings resilience supporting the broader market is better captured, on a risk-adjusted basis, through sectors where positioning is lighter and valuations have more room to expand.

Why the timing of this call matters

The 5 June 2026 publication date is not incidental. The Federal Reserve’s FOMC meeting falls on 17 June 2026, and the ECB is expected to deliver its own rate decision in the same period. Positioning ahead of central bank decisions introduces a timing dimension that purely sector-focused analysis would miss. Investors weighing when to act on a rotation thesis, not just whether to act, need the macro calendar as a reference point.

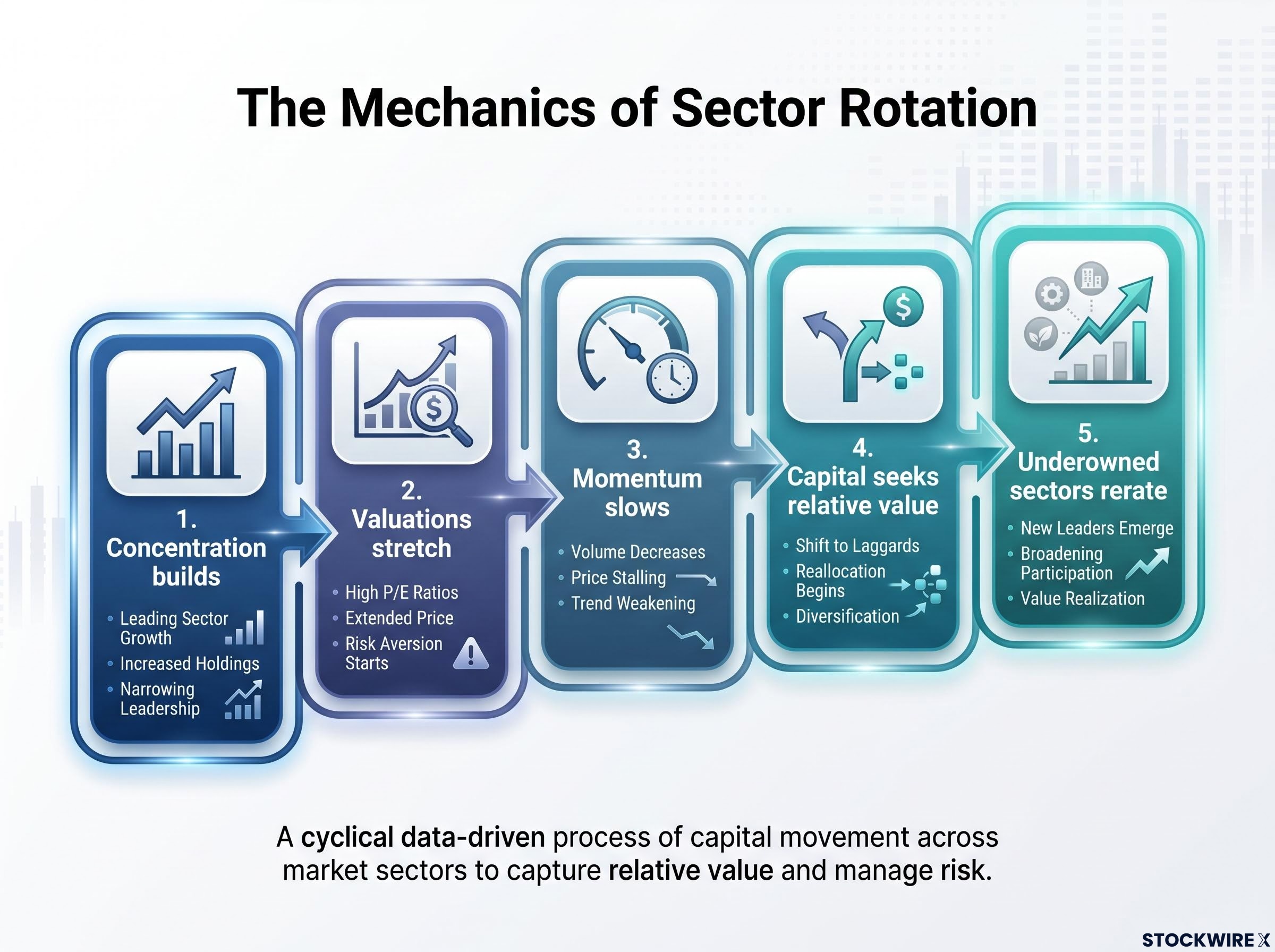

Understanding why momentum trades stall, and why rotation follows

Sector rotation is one of the most frequently cited concepts in equity strategy, yet the mechanics are often left vague. In practical terms, the sequence follows a repeatable pattern:

The sector rotation mechanics that drive these episodes are well-documented: institutional capital repositions ahead of confirmed economic data, meaning sector leadership shifts often precede official readings by weeks, and the AI capital spending cycle projected at $725 billion in 2026 creates a secular demand driver that complicates straightforward cycle-phase rotation calls.

- Concentration builds. A narrow group of stocks captures most of the market’s momentum-driven inflows, drawing capital from passive funds, algorithmic strategies, and retail investors chasing performance.

- Valuations stretch. The influx of capital pushes prices beyond what near-term earnings can justify, creating a gap between price and fundamentals.

- Momentum slows. Any catalyst (a disappointing earnings print, a macro shock, or simply the exhaustion of new buyers) causes the momentum to stall.

- Capital seeks relative value. Investors who remain constructive on equities but recognise the stretched positioning begin redeploying into sectors that are underowned and undervalued relative to their earnings trajectories.

- Underowned sectors rerate. The inflow of capital into these areas narrows the valuation gap, and a new set of sector leaders emerges.

Barclays’ characterisation: The overheating in equity markets is narrow in scope, limited mainly to U.S. and Asian indices, not a signal that the broader equity market is at risk.

The semiconductor trade is the concrete illustration of this sequence. Barclays frames the parabolic price movement not as a crash prediction but as a trigger condition: the point at which the gap between momentum and fundamentals becomes wide enough that rotation is the rational response for investors who want equity exposure without the concentration risk.

Europe’s turn: why lower tech weighting and cheaper valuations make the geographic case

The geographic dimension of Barclays’ rotation argument rests on a structural asymmetry between European and U.S. markets. European indices carry a materially lower technology weighting, have underperformed U.S. benchmarks, and trade at cheaper valuations. For capital rotating out of overextended tech positions, Europe offers a destination where the rotation trade and the valuation trade point in the same direction.

The European equity underperformance relative to the S&P 500 now spans roughly three months and roughly 9 percentage points, with Barclays identifying a potential US-Iran agreement as the single catalyst most capable of triggering a sharp repricing in consumer discretionary, banking, and luxury names that have accumulated elevated short positioning during the conflict period.

| Attribute | European markets | U.S. / Asian markets |

|---|---|---|

| Technology weighting | Lower | Higher, concentrated in semiconductors |

| Recent relative performance | Underperformed U.S. indices | Led by narrow momentum trades |

| Valuation | Cheaper on relative basis | Stretched by momentum inflows |

| Key risk | ECB hiking into softening economy | Fed hawkish surprise under new chair |

The case is not without complication. Barclays views a June 2026 ECB rate hike as more likely than not, and that hike is expected even as the European economic backdrop deteriorates. Tightening monetary conditions into a weakening economy creates a headwind for the very market Barclays is recommending as a rotation destination. Investors need to weigh the valuation opportunity against the monetary policy cost.

Geopolitical wildcard: A hypothetical U.S.-Iran peace agreement, if realised, could amplify momentum reversals and accelerate capital flows into European and other underperforming markets. Barclays presents this as a potential accelerant, not a base-case assumption.

The central bank calendar is the wildcard that shapes rotation timing

Even a well-constructed rotation thesis depends partly on timing, and the June 2026 macro calendar introduces two distinct sources of uncertainty that sit outside the sector analysis itself.

The central bank decision compression in June 2026 is without close modern precedent: four systemically important central banks including the ECB, Bank of Japan, Federal Reserve, and Bank of England deliver rate decisions within an eight-day window, collapsing the sequential digestion period markets typically rely on and exposing equities, bonds, and currencies to simultaneous repricing from independent policy signals.

On the Fed side, Barclays’ base case is no rate change at the 17 June FOMC meeting. A shift toward a more hawkish stance, however, is framed as a realistic possibility rather than a tail risk. Two converging forces sustain the inflationary backdrop: robust U.S. economic activity data, which reduces the urgency for rate cuts, and elevated oil prices, which together with strong activity data point toward persistent price pressure.

Kevin Warsh’s debut as Fed chair adds a layer of institutional uncertainty that extends beyond the rate decision itself. Markets have no track record of Warsh’s communication style under live FOMC conditions. The June meeting will serve as a first read on how the new chair frames policy trade-offs, and any departure from the tone markets have grown accustomed to could itself move positioning.

- FOMC meeting (17 June 2026): Base case is hold, but hawkish shift is a realistic possibility given inflationary data.

- Warsh’s debut: Institutional uncertainty as markets assess a new communication style for the first time.

- ECB June meeting: Rate hike expected despite deteriorating European economic conditions, creating a tightening-into-weakness tension.

- Elevated oil prices: Sustaining inflationary pressure across both the U.S. and European policy environments.

The ECB’s uncomfortable position

The ECB’s dilemma sharpens the complexity of the European rotation trade. Hiking rates into a softening economy is, by definition, a restrictive choice that weighs on growth-sensitive sectors and consumer demand. For investors acting on Barclays’ recommendation to rotate toward European equities, the ECB’s stance introduces a timing question: does the valuation discount compensate for the near-term monetary headwind?

Barclays does not dismiss this tension. The European thesis is presented as a structural opportunity that coexists with a cyclical risk, and the June rate decision is the event that will clarify how much of that risk is already priced.

Barclays is not alone in watching this inflection, and what happens if the rotation fails to materialise

A rotation thesis without a failure condition is a sales pitch. The scenario in which semiconductor momentum does not stall is entirely plausible. If chip stocks continue their run, driven by another wave of AI infrastructure spending or by earnings that justify the elevated valuations, the trigger for capital reallocation simply does not fire.

In that scenario, the identified beneficiaries (software, defence, cyclical consumer segments, European equities) may underperform the very momentum trade Barclays is advising investors to reduce. The thesis loses its catalyst, even if the structural arguments remain intact.

Investors should monitor specific signals to assess whether the rotation is actually underway rather than merely anticipated:

- Relative performance divergence: Semiconductor indices underperforming software or defence benchmarks over a sustained period, not just a single session.

- Market breadth expansion: Gains broadening across U.S. and non-U.S. markets rather than remaining concentrated in the same narrow group of names.

- Central bank tone from June meetings: Hawkish surprises from either the Fed or the ECB would accelerate the case for lower-momentum positioning; dovish outcomes would extend the runway for the existing momentum trade.

- Geographic flow data: Evidence of capital shifting from U.S. and Asian indices into European and other underperforming markets.

Barclays’ overarching positive equity stance provides the anchor here. The firm’s framing of earnings resilience and a sustained investment supercycle means the failure of the tactical rotation call does not equate to a broader equity decline. It means staying in the same part of the market that has already worked, for longer.

Positioning for a selective summer: what the Barclays call means for investors thinking beyond the index

The Barclays rotation thesis operates across three dimensions simultaneously. By sector, the call favours software, defence, and cyclical consumer segments over crowded semiconductor positions. By geography, it favours European and underperforming international markets over U.S. and Asian indices where the froth is concentrated. By timing, it is contingent on the June central bank events and the semiconductor trajectory itself.

Emmanuel Cau’s framework is a positive-within-equities argument, not a risk-off signal. The appropriate response, if the thesis is accepted, is reweighting rather than wholesale repositioning. Capital stays in equities; it moves to where Barclays sees the risk-adjusted return profile as more favourable.

The forward-looking question is direct. If Warsh’s Fed debut introduces hawkish surprises and the ECB hikes as expected, the case for international diversification and lower-momentum sectors becomes more urgent, not less. The geopolitical wildcard of a U.S.-Iran agreement, should it materialise, would amplify the thesis further. Published on 5 June 2026, the call gives investors twelve days before the FOMC meeting to assess their positioning.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding central bank decisions, sector performance, and geopolitical developments are speculative and subject to change based on market developments.