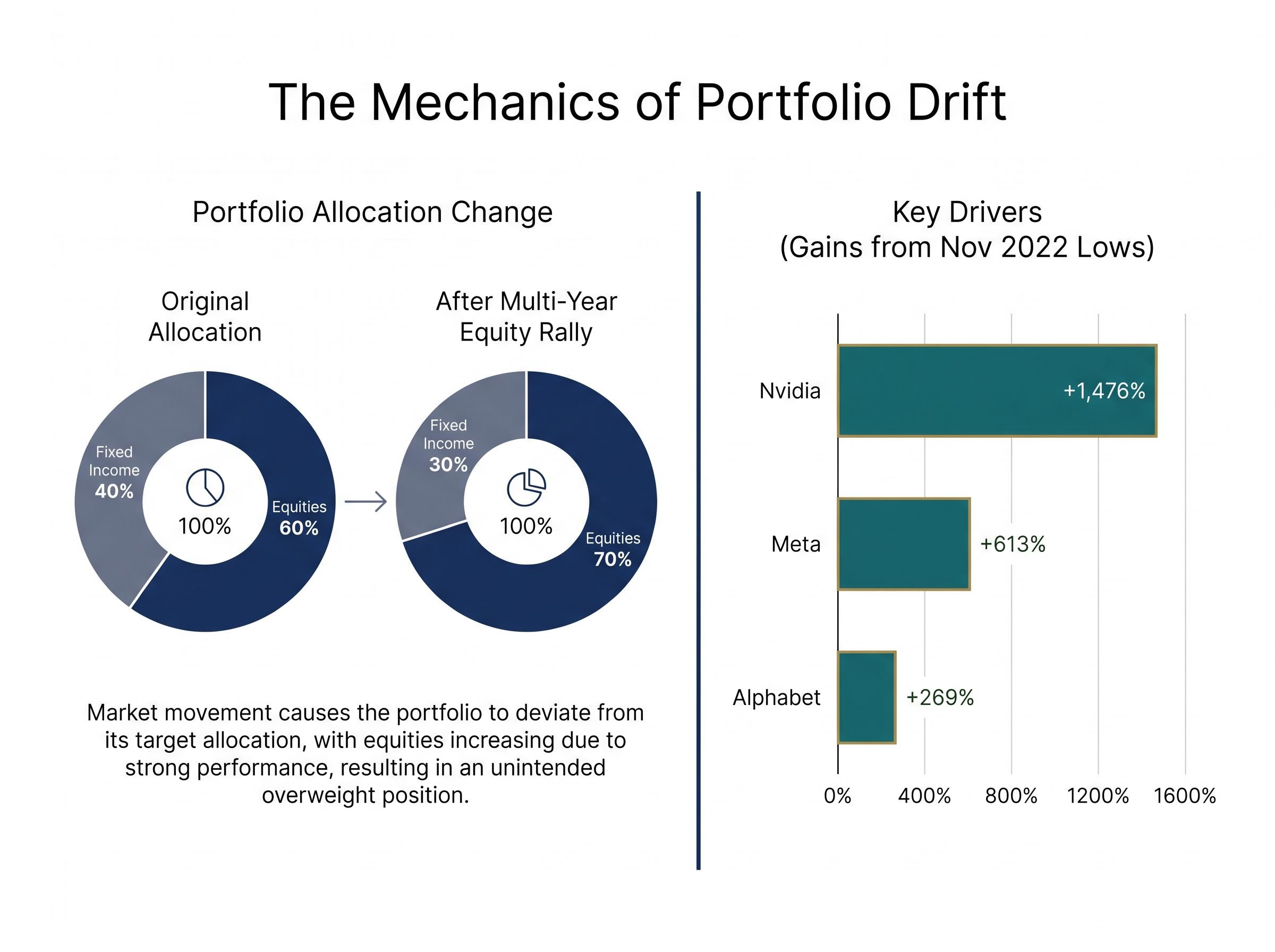

Three years ago, the portfolio was straightforward: 60% equities, 40% bonds, a deliberate split designed to match a specific tolerance for risk. No trades were made, no allocations changed. Yet the portfolio today looks nothing like the one that was built. Equities have quietly compounded their way to 70% of total value, and the 40% fixed-income cushion has shrunk to 30%. The investor did not choose this new allocation; the market chose it for them. After three consecutive years of equity strength, with names like Nvidia surging over 1,400% from their November 2022 lows and broad indices delivering layered gains, many portfolios now carry a risk profile that no longer reflects the original intention. Early 2026 has sharpened the stakes: the MSCI World Index fell 6.55% in March before rebounding 10.1% in April, a sequence that rewards preparation over reaction. This guide explains how portfolio drift happens, how to calculate when rebalancing is warranted, how to execute it tax-efficiently, and where reallocated capital can go to reduce concentration without abandoning return potential.

Why equity gains quietly reshape your portfolio without you noticing

The mechanics are simple. When one asset class outperforms another over an extended period, its share of total portfolio value grows automatically, even if the investor makes no active decisions. A portfolio allocated 60% to equities and 40% to bonds does not stay that way when equities deliver compounding annual gains and bonds deliver modest income. The equity slice grows; the bond slice shrinks as a proportion of the whole.

This is not a mistake. It is a structural feature of compounding returns. But the result is a portfolio the investor did not consciously choose, one that now carries more downside exposure than the original allocation was designed to absorb.

The scale of recent drift has been extraordinary for investors with technology exposure. Nvidia rose approximately 1,476% from its November 2022 low. Meta gained 613% over the same period. Alphabet added 269%. These are not niche positions; they sit inside virtually every global index fund, and their outperformance has mechanically pulled equity weightings upward across millions of portfolios.

| Asset Class | Original Allocation | After Multi-Year Equity Rally |

|---|---|---|

| Equities | 60% | 70% |

| Fixed Income | 40% | 30% |

When the MSCI World dropped 6.55% in a single month in March 2026, a portfolio sitting at 70% equities absorbed a meaningfully larger drawdown than the same portfolio at 60% would have. The drift was invisible until the volatility arrived.

Unintended concentration risk: the portfolio you did not choose

Concentration risk, in plain terms, means holding a larger proportion of a single asset class or sector than intended, which increases sensitivity to that specific area’s drawdowns. Asset-class drift is one dimension of this problem. Sector-level drift is a second.

AI-driven concentration in U.S. large-cap technology has been a specific concern for globally diversified portfolios. An investor who owns a broad global index fund may discover that the fund itself has drifted toward a handful of mega-cap technology names, compounding the portfolio-level drift with sector-level concentration the investor never selected.

The drift described above is compounded by index fund concentration risk: five mega-cap stocks controlled roughly 23% of the broad US market index as of mid-April 2026, meaning a portfolio that appears diversified across hundreds of companies may carry far more single-sector exposure than the fund name suggests.

When big ASX news breaks, our subscribers know first

How to know when it is time to rebalance

Recognising drift is the first step. The second is knowing when it warrants action. Two frameworks exist, and each solves a different problem.

Calendar-based rebalancing means reviewing allocations on a fixed schedule, typically quarterly or annually, regardless of what markets have done. Year-end reviews are a widely practised standard. The advantage is simplicity and discipline; the limitation is that it may trigger trades in stable markets where drift has not reached a meaningful level.

Threshold-based rebalancing means acting only when allocations drift beyond a defined percentage from their target. This approach avoids unnecessary trades but requires ongoing monitoring to detect when the threshold has been crossed.

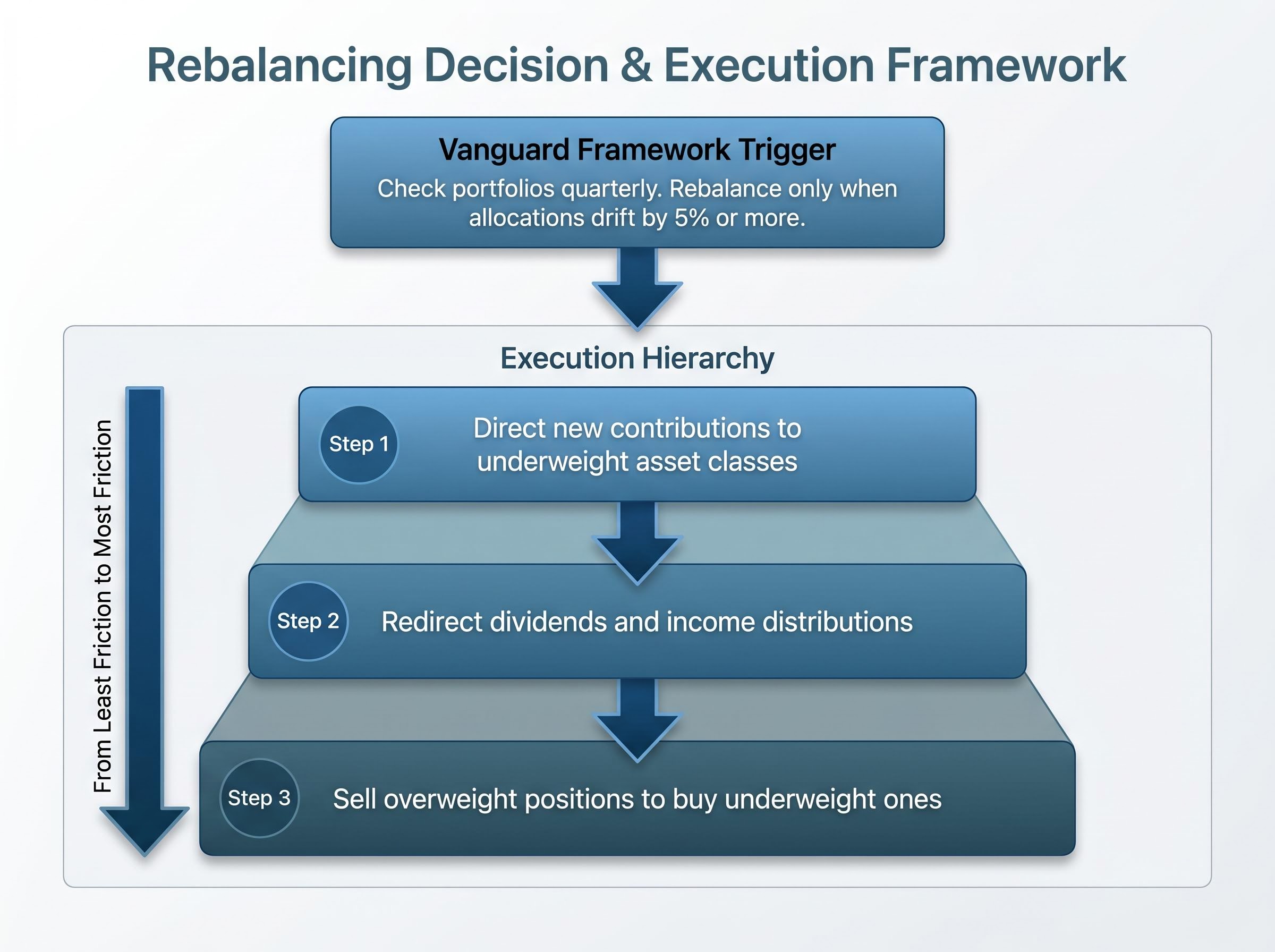

Vanguard recommends checking portfolios quarterly but rebalancing only when allocations drift by 5% or more from targets, a framework that balances transaction costs against the benefit of maintaining target risk exposure.

Vanguard’s rebalancing best practices establish that annual or semi-annual monitoring combined with a 5% threshold trigger produces a reasonable balance between risk control and transaction cost minimisation for broadly diversified equity and bond portfolios, providing the empirical basis for the quarterly-check framework described here.

The strongest approach combines both: a scheduled quarterly review paired with a threshold trigger. If allocations remain within tolerance at the review date, no action is needed. If they have drifted beyond 5%, the rebalance is executed.

The illustrative 60%-to-70% equity drift described above represents a 10-percentage-point overshoot, an unambiguous trigger under Vanguard’s framework. For most investors who have not rebalanced since early 2024, the threshold has almost certainly been breached.

The mechanics of actually executing a rebalance

Knowing when to rebalance is a decision. Executing it efficiently is a process. The three primary execution levers, listed in order from least friction to most, are:

- Direct new contributions to underweight asset classes. If bonds are underweight, allocate fresh savings entirely to fixed income until the gap narrows. No selling required, no tax event triggered.

- Redirect dividends and income distributions. Rather than reinvesting equity dividends into more equities, direct them toward the underweight allocation. This is a slower rebalancing mechanism but generates zero capital gains.

- Sell overweight positions to buy underweight ones. If the gap is too large for contributions and dividends to close within a reasonable timeframe, selling is necessary. This is where tax efficiency becomes the primary consideration.

Using contributions and income first is not merely a preference; it avoids triggering capital gains events, which is the most common execution error investors make when rebalancing. Selling should be the final lever, not the first.

The arithmetic is straightforward. If equities represent 70% of a $500,000 portfolio and the target is 60%, the overweight amount is $50,000. That sum needs to move from equities to the underweight asset class, whether through contributions over time or a direct sale.

Julius Baer has advocated shifting from buy-and-hold to tactical rebalancing in 2026, framing global diversification as a structural positioning theme rather than a one-off trade. The implication is that this is not a single transaction but an ongoing discipline.

Executing the trade in the right account first

The tax-advantaged-first principle is simple: rebalancing inside IRAs, SIPPs, pensions, or equivalent structures incurs no capital gains event. Fidelity recommends bifurcating execution between taxable and tax-advantaged accounts, using the latter for the bulk of selling activity where possible.

Regional variation applies. In the U.S., long-term capital gains attract lower tax rates than short-term gains, making holding period awareness relevant for taxable sales. In the UK, ISAs shelter gains entirely. EU jurisdictions vary by country. The principle remains consistent across regions: execute the highest-friction trades (selling appreciated positions) inside the most tax-efficient wrapper available.

What portfolio rebalancing actually means (and why it is not the same as retreating from markets)

Rebalancing is the process of restoring a portfolio to its intended risk profile by returning asset class weights to their target allocations. It is a risk management discipline, not a market forecast.

This distinction matters because the most common objection to rebalancing is that it feels like selling winners. The instinct is understandable. Equities have performed well; selling a portion to buy bonds or alternatives can feel like a bet against continued growth.

It is not. The decision to rebalance is triggered by portfolio drift, not by a prediction that markets will fall. Target allocations exist because they reflect the investor’s risk tolerance, time horizon, and return objectives, all of which remain constant even when asset prices move. Rebalancing restores the portfolio to the risk level the investor actually chose.

The risk-return trade-offs across asset classes explain why the 60/40 split was chosen in the first place: each allocation reflects a deliberate acceptance of a specific volatility range and return expectation, a balance that compounding equity gains quietly dismantle over time.

- What rebalancing is: Returning asset class weights to a predetermined target based on the investor’s risk profile

- What rebalancing is not: A forecast that equities will decline, a retreat from growth exposure, or a market-timing decision

Bubbles are only verifiable after the fact, as source material from institutional research notes. Rebalancing does not require identifying a bubble. It requires recognising that a portfolio’s actual risk exposure has diverged from its intended risk exposure.

Global real GDP growth continues at approximately 3% in 2026. The case for maintaining equity exposure is intact. Rebalancing simply right-sizes that exposure to match the investor’s original parameters.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Where to put the capital you move out of equities

The question that follows every rebalancing decision is practical: where does the reallocated capital go? Three alternative asset categories offer genuinely different risk characteristics from public equities, making them destinations rather than consolation prizes.

Private credit funds, particularly those focused on senior secured direct lending, offer stable income with lower correlation to public equity markets. The appeal lies in predictable cash flows from loan portfolios. Quality criteria matter: suitable funds favour short loan duration, monthly liquidity, no lock-up periods, and avoidance of property developer concentration.

Private credit target returns range from approximately 6-9% annually with monthly income distributions, according to institutional research.

Market-neutral arbitrage funds generate returns largely uncorrelated with public equities. These strategies, spanning quantitative, long/short, and multi-strategy approaches, aim to deliver positive returns regardless of equity market direction. They function as a genuine diversifier rather than a lower-beta substitute for equities.

Private infrastructure provides exposure to stable cash flows through assets such as data centres and power generation facilities. Returns are often linked to inflation, and correlation to public markets tends to be lower than traditional fixed income.

When the MSCI World fell 6.55% in March 2026, uncorrelated return streams demonstrated practical value, not just theoretical appeal. Specific fund performance metrics for private credit and hedge funds are not publicly available and typically require access to databases such as Preqin or Cambridge Associates; investors are directed to conduct due diligence through professional channels.

For investors wanting a step-by-step framework for deploying capital across each of these categories in the current macro environment, our dedicated guide to tactical allocation in 2026 covers specific positioning in Treasury Inflation-Protected Securities, REITs, physical gold, and high-quality equities with pricing power, including the case for a 10-15% cash buffer to capture market dislocations.

| Alternative Destination | Expected Return Profile | Liquidity Terms | Correlation to Public Equities | Key Risk Considerations |

|---|---|---|---|---|

| Private Credit | 6-9% annually | Monthly (varies by fund) | Low | Credit default risk, loan quality, manager selection |

| Market-Neutral Funds | Variable, return-target driven | Monthly to quarterly | Very low | Strategy complexity, manager dependence, capacity constraints |

| Private Infrastructure | Inflation-linked, stable yield | Quarterly to semi-annual | Low | Illiquidity, regulatory risk, long capital commitment |

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

What a rebalanced portfolio looks like in the current environment

The end state of this process is not a defensive portfolio. It is a more deliberate one.

A rebalanced portfolio in early 2026 carries several characteristics: restored target equity weight, geographic diversification beyond U.S. mega-caps, and meaningful alternative asset exposure. The market context supports each of these dimensions.

Alternative asset allocation frameworks that combine a reduced equity weighting with meaningful positions in bonds, alternatives, and cash, such as a 40/30/20/10 structure, offer a worked example of how the rebalanced portfolio can be positioned across multiple scenarios rather than optimised for a single growth outcome.

- Non-U.S. equities have shown strength, with the MSCI World ex-US gaining approximately 5.2% in January 2026 versus 2.3% for the MSCI World overall, indicating that international developed and emerging market exposure has delivered meaningful outperformance

- Defensive sectors such as healthcare and high-dividend, low-volatility stocks provide portfolio stability during drawdown periods

- Alternative assets spanning private credit, infrastructure, and market-neutral strategies add uncorrelated return streams

Julius Baer has advocated shifting toward global diversification, defensive sectors, and high-dividend positions as structural themes for 2026, a view consistent with the broadening of market leadership beyond U.S. technology names.

The MSCI ACWI IMI rebound of approximately 10.1% in April 2026 illustrates that rebalancing does not mean missing recoveries. A portfolio rebalanced to target still holds equities; it simply holds them at the weight the investor intended.

Once rebalanced, the discipline becomes ongoing. Vanguard’s quarterly-check-with-5%-trigger framework provides the maintenance rhythm: review every three months, act only when drift warrants it.

The 2026 environment, characterised by sharp drawdowns, strong rebounds, and broadening leadership, rewards portfolios built for resilience across multiple scenarios rather than optimised for a single outcome.

A more deliberate portfolio is not a smaller ambition

Rebalancing after a multi-year equity rally is not a retreat from growth. It is the act of ensuring the portfolio still reflects the investor’s actual risk tolerance and return objectives rather than the market’s random drift.

The action sequence is three steps. First, calculate current equity weight as a percentage of total portfolio value and compare it against the original target. Second, choose a rebalancing trigger framework: the 5% threshold, a calendar schedule, or both. Third, execute in tax-efficient order: new contributions first, dividends second, tax-advantaged account sales third, taxable sales last.

The investors who tend to navigate volatile periods most effectively are those who made deliberate allocation decisions before volatility arrived, not during it.

These statements are speculative and subject to change based on market developments and company performance.

The first step is concrete and immediate: calculate the current equity percentage as a share of total portfolio value. If the number is higher than intended, the process outlined above provides a framework for action. Before making material allocation changes, consulting a licensed financial adviser is recommended.