Australia Axes 50% CGT Discount in Biggest Tax Overhaul Since 1999

6 hrs ago

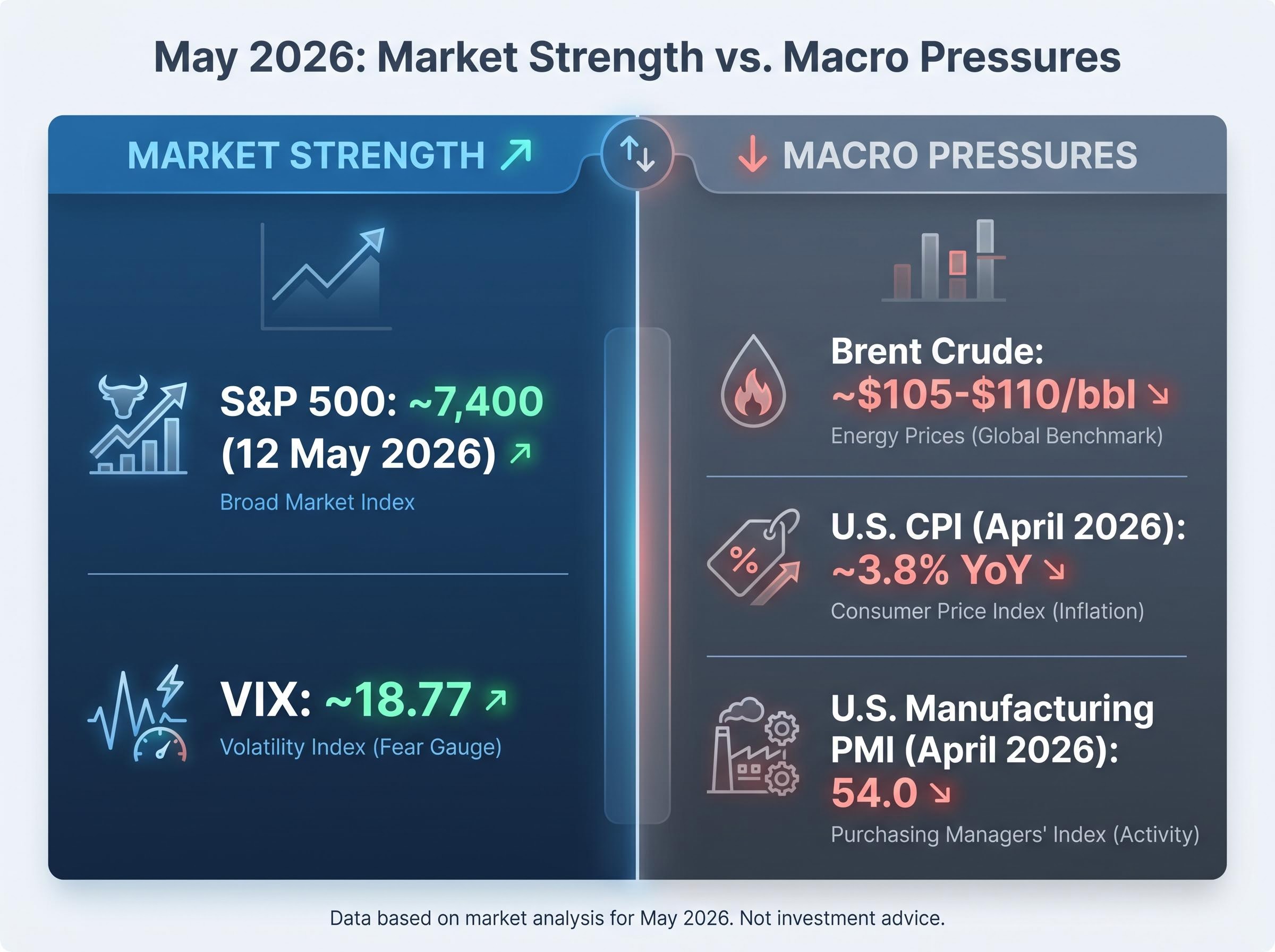

The S&P 500 closed at approximately 7,400 on 12 May 2026, within striking distance of record territory. Brent crude sits at roughly $105-$110 per barrel. Middle East tensions remain unresolved. And HSBC’s chief multi-asset strategist, Max Kettner, has not trimmed a single unit of the bank’s maximum overweight equity position.

HSBC’s May Monthly View, published on 13 May 2026, maintains the most aggressive pro-risk stance in the bank’s tactical framework and raises its S&P 500 year-end target to 7,650. The note’s core argument is that sentiment and positioning data, not geopolitical headlines, should govern the sell decision. Neither signal has triggered.

What follows unpacks how Kettner’s framework operates, what the earnings and macro data actually show, and where HSBC is placing its most differentiated regional bets, providing a clear picture of the institutional logic behind holding maximum conviction at elevated levels.

Geopolitical risk is not absent from Kettner’s framework. It is simply not the variable that triggers the exit. HSBC’s May note argues that positive developments on the Middle East front have not yet been fully priced into equity markets, meaning upside optionality remains even as headlines generate volatility.

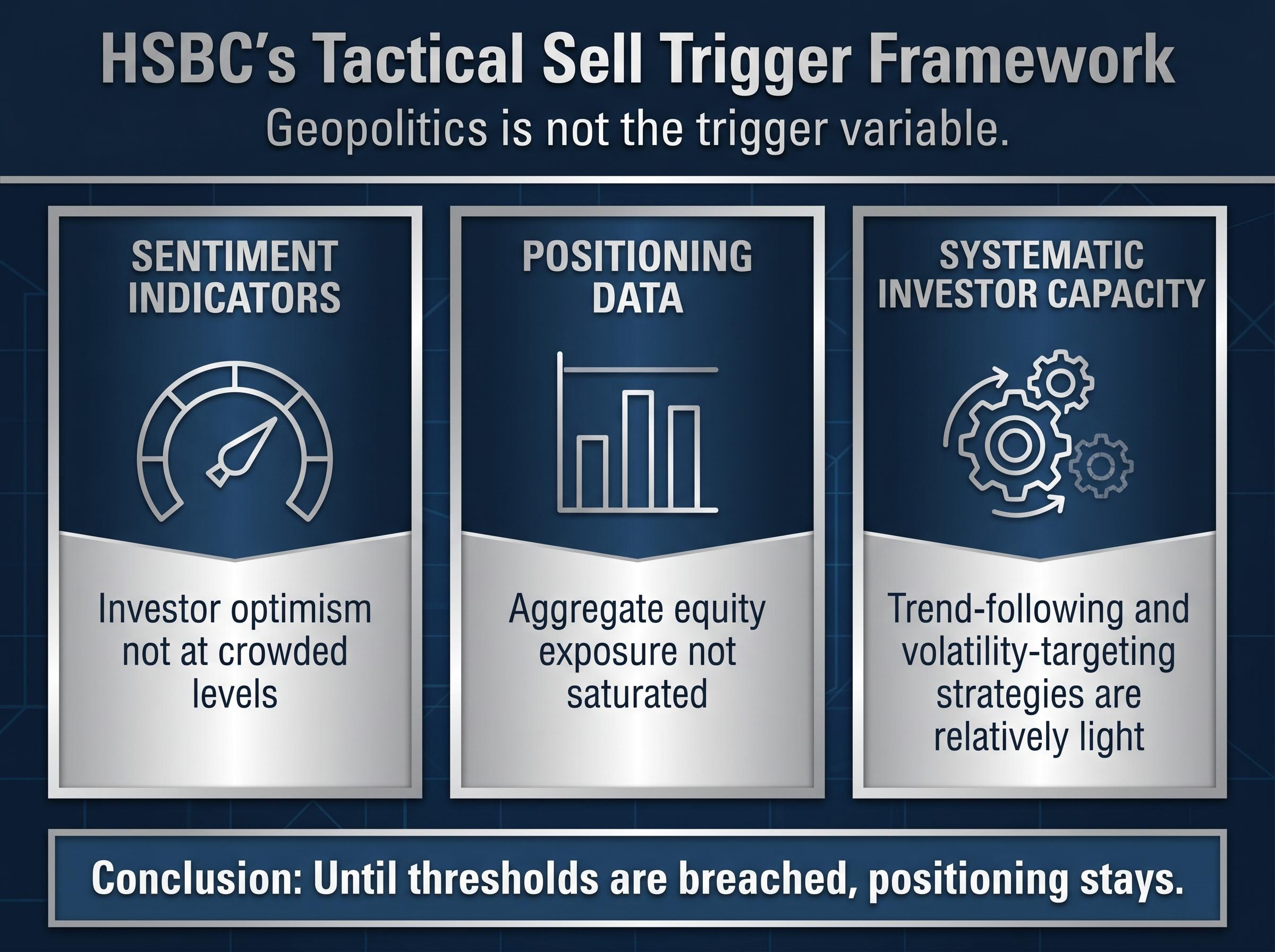

Kettner’s core position: The case for geopolitically driven profit-taking does not hold when sentiment indicators remain below extreme thresholds and systematic investor positioning is still relatively light.

The bank’s tactical sell trigger rests on three components working in combination:

Systematic investor positioning data from the week ending 8 May 2026 reinforces the HSBC read: Bank of America’s Bull and Bear Indicator reached 7.2, just 0.8 points below its contrarian sell-signal threshold, while $136 billion simultaneously rushed into cash funds, a split that is precisely consistent with a market where sentiment has not yet reached the extreme optimism levels that historically precede drawdowns.

HSBC’s S&P 500 year-end target of 7,650, set against the index’s current level of approximately 7,400, implies roughly 3% additional upside. The conviction is systematic, not casual: until the framework’s thresholds are breached, the positioning stays.

Start with the aggregate picture. The Q1 2026 S&P 500 earnings beat rate came in at its highest level since the COVID-19 economic reopening in 2021. S&P 500 net income excluding technology grew 11% quarter-over-quarter. These are not marginal improvements; they represent broad-based earnings strength across sectors.

The Q1 2026 earnings season produced a blended S&P 500 growth rate of 27.1%, nearly double the 13.1% pre-season analyst forecast, with an aggregate earnings surprise of roughly three times the five-year average, a result that shifted analyst assumptions about what the full-year earnings trajectory could support.

Then consider the technology sector specifically. Not a single U.S. technology company reported a below-consensus earnings-per-share result in Q1. Zero. In a quarter where macro uncertainty and elevated energy costs offered plausible reasons for misses, every major tech name cleared the bar.

| Metric | Q1 2026 Result | Significance |

|---|---|---|

| EPS beat rate | Highest since 2021 reopening | Broadest earnings strength in five years |

| Non-tech net income growth | +11% QoQ | Earnings breadth beyond tech leadership |

| HSBC 2026 EPS estimate | ~$325 | Implies approximately 20% YoY growth |

| U.S. tech below-consensus results | Zero | Perfect sector-wide beat in a volatile quarter |

Beat rates are backward-looking. What makes this earnings season unusual is what is happening to forward estimates. Full-year 2026 consensus EPS projections are rising rather than declining, which runs counter to the typical mid-year pattern where analysts trim expectations as economic uncertainty builds through the calendar.

HSBC’s own $325 EPS estimate implies roughly 20% year-over-year growth, materially more aggressive than many sell-side figures. The S&P 500’s current level of approximately 7,400 is already trading consistent with this bullish framing, meaning the market is not waiting for the data to catch up. It is pricing the earnings trajectory in real time.

The labour market remains the strongest pillar of HSBC’s macro case. U.S. initial jobless claims are running at a seasonal historical low on a non-seasonally adjusted basis, which the bank reads as consistent with a resilient employment backdrop. High-income households, supported by wealth effects from equity gains, stable employment, and tax refunds, continue to underpin the consumption story.

The U.S. Department of Labor jobless claims data for the week ending 2 May 2026 showed initial claims at 200,000, with the four-week moving average dropping to a cycle low of 203,250, providing the concrete labour market foundation for HSBC’s assertion that employment conditions remain historically strong.

Four verified data points frame the current macro environment:

HSBC’s counterintuitive read on consumer spending: Apparent softness in credit card data reflects base effects from tariff-driven front-loading in the prior-year period, not genuine consumer deterioration.

The inflation complication deserves direct acknowledgement. U.S. CPI at 3.8% means the “imminent Fed cuts” narrative is overstated. HSBC’s bull case rests on strong growth, not cheap money. The macro picture is better characterised as a strong-but-complicated backdrop: expanding output, tight labour, and persistent price pressure coexisting simultaneously.

HSBC’s call is not a story about buying a dip. It is a conviction hold at elevated absolute levels, and the verified market data make this clear.

| Index / Asset | Level (12 May 2026) | Context |

|---|---|---|

| S&P 500 | ~7,400 | Record high territory |

| MSCI World | ~4,757-4,764 | Broad global equity strength |

| Nikkei 225 | 62,618 | Japanese equities at elevated levels |

| Hang Seng | 26,497 | Asian market participation |

| VIX | ~18.77 | Moderate vol; not complacent, not fearful |

| Brent Crude | ~$105-$110/bbl | Elevated despite equity gains |

The VIX at approximately 18-19 reflects a market that is pricing neither complacency nor systemic fear, which is consistent with HSBC’s sentiment-framework read. BlackRock’s confirmed 11 May weekly commentary, titled “Record US Stocks, Disconnect or Not?”, framed the same tension: record equities coexisting with high oil prices. That coexistence is the environment Kettner is choosing to stay fully invested in.

The maximum overweight headline covers a structured, differentiated portfolio, not a generic long-everything position.

Within equities, HSBC distinguishes sharply by region. U.S. and Asian markets carry the full weight of the maximum overweight allocation. European equities receive a more cautious treatment; the bank’s sector preference there has narrowed to financials. The rationale centres on deteriorating European business confidence: the German ifo index is signalling declining activity, which informs a broader preference for European sovereign bond duration over U.S. Treasury duration.

HSBC’s Asia equity thesis extends well beyond the broad regional overweight: the bank’s 10 May 2026 AI framework assigned Taiwan a 53% net AI-enabled revenue share, the highest of any national market, with South Korea ranked second at 33%, a country-level concentration in semiconductor and high-bandwidth memory exposure that gives the Asia allocation a structural AI-cycle rationale distinct from the sentiment-and-positioning logic driving the headline overweight.

The ifo Business Climate Index fell to 84.4 points in April 2026, down from 86.3 in March and its lowest reading since May 2020, with companies reporting considerably more pessimism about the coming months, a deterioration that directly informs HSBC’s preference for European sovereign bond duration over a broader European equity overweight.

| Asset Class / Region | HSBC Positioning | Rationale |

|---|---|---|

| Global equities (U.S. and Asia) | Maximum overweight | Sentiment and positioning framework intact |

| Local EM debt | More-than-double overweight | Yield and diversification appeal |

| High-yield credit | Overweight | Credit fundamentals supportive |

| U.S. Treasuries | Maximum underweight | Prefer European sovereign duration |

| European equities | Selective (financials preferred) | ifo weakness; narrow sector conviction |

| Consumer discretionary | U.S. preferred over Europe | Stronger U.S. consumer backdrop |

The asset class hierarchy beyond equities is equally revealing. HSBC holds a more-than-double overweight in local emerging market debt and an overweight in high-yield credit. At the opposite end, U.S. Treasuries carry a maximum underweight, particularly relative to European sovereign bonds. This is a portfolio that expresses conviction in growth and risk appetite while actively avoiding the duration risk embedded in U.S. government debt.

The tension at the heart of HSBC’s May view is not hidden. Brent crude at $105-$110. CPI at 3.8%. Geopolitics unresolved. Equities at record highs. This is precisely the kind of environment where systematic frameworks exist to prevent emotion from driving allocation decisions.

Kettner’s operative argument: The sell signal has not triggered. Until it does, the positioning stays at maximum overweight.

Three conditions would cause HSBC to revise its stance:

HSBC’s S&P 500 target of 7,650 implies approximately 3% additional upside from current levels, a modest figure that underscores this is a hold call rather than a chase. The broader peer consensus from Goldman Sachs, JPMorgan, Morgan Stanley, and BlackRock leans overweight equities for 2026, though HSBC’s maximum overweight stance sits among the most aggressive expressions of that view.

The peer consensus on S&P 500 targets from Goldman Sachs, Morgan Stanley, and JPMorgan is broadly supportive of elevated valuations for 2026, though the construction of their bull cases differs: Morgan Stanley’s revised target rests explicitly on an earnings expansion thesis projecting $339 EPS, a fundamentals-first framing that contrasts with frameworks anchored more heavily on sentiment and positioning data.

The most durable takeaway is the framework itself: not whether an institutional strategist is bullish or bearish, but what specific evidence would cause the view to change.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

HSBC's May 2026 Monthly View maintains a maximum overweight equity position, with a revised S&P 500 year-end target of 7,650. The bank's strategist Max Kettner argues that neither sentiment indicators nor systematic investor positioning have reached the extreme thresholds that would trigger a sell signal.

HSBC would revise its bullish positioning if sentiment indicators reached extreme optimism levels historically preceding drawdowns, if systematic investor positioning became saturated, or if full-year earnings estimate momentum reversed with analysts trimming rather than raising projections.

HSBC assigns maximum overweight allocations to U.S. and Asian equities, while European equities receive only selective exposure concentrated in financials, reflecting deteriorating business confidence signalled by the German ifo index falling to 84.4 in April 2026.

Q1 2026 produced the highest S&P 500 EPS beat rate since the 2021 COVID reopening, with non-technology net income growing 11% quarter-over-quarter and not a single U.S. technology company reporting a below-consensus result. HSBC's own full-year 2026 EPS estimate of approximately $325 implies roughly 20% year-over-year growth.

HSBC holds U.S. Treasuries at maximum underweight while favouring European sovereign bond duration, because deteriorating European business confidence (reflected in the ifo index at its lowest since May 2020) makes the region's bonds more attractive than U.S. government debt in a high-growth, persistent-inflation environment.