BOQ Pays 6.39% Fully Franked, but the Risks Are Real

4 hrs ago

UK politics in early 2026 delivered the kind of drama that financial headlines typically treat as a market-moving event: a prime ministerial resignation, a parliamentary scandal, cabinet walkouts, and sustained speculation over a Chancellor who might unsettle the fiscal settlement. The media narrative practically wrote itself.

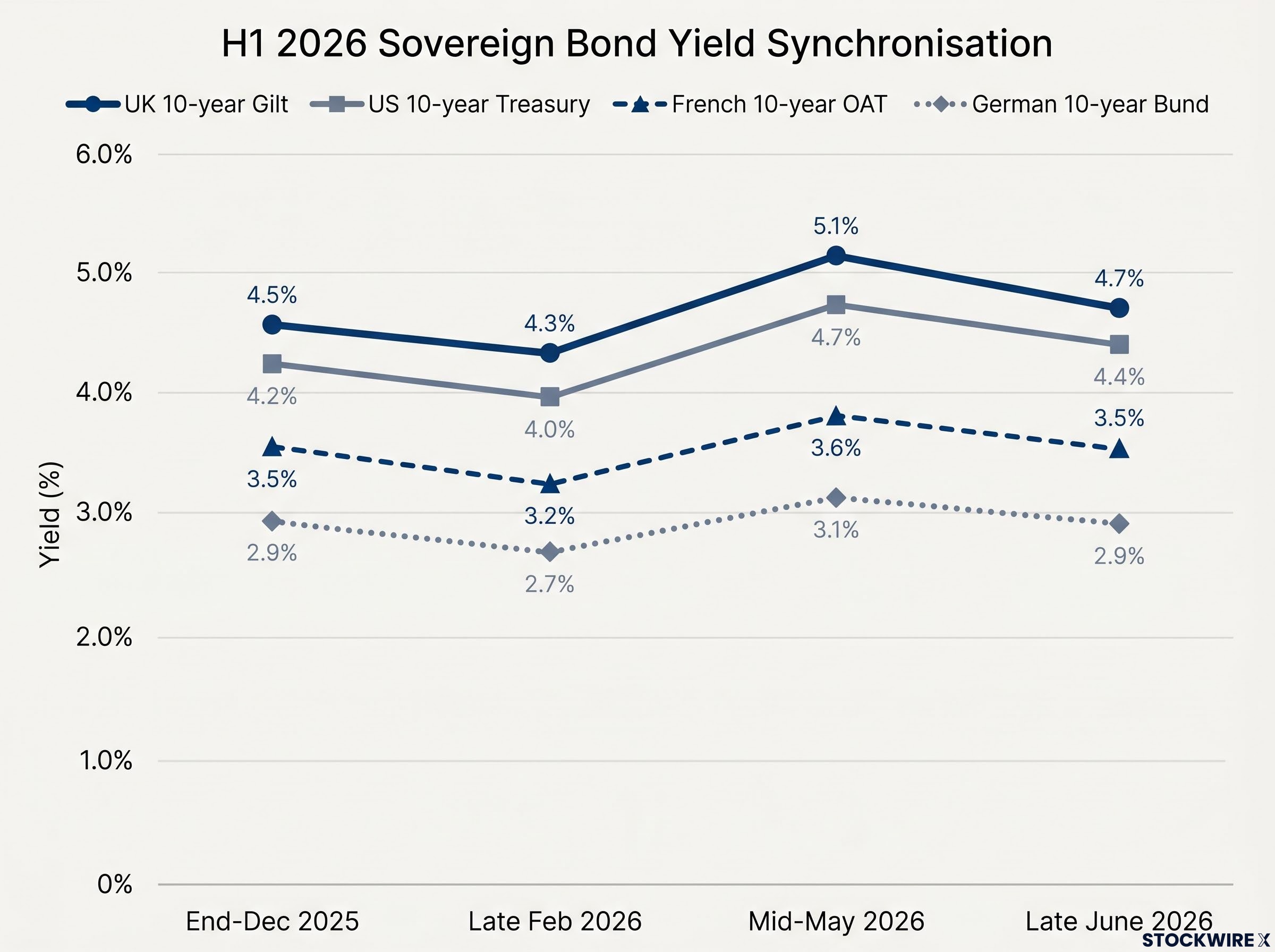

And yet the data tells a quieter story. UK gilt yields in mid-2026 tracked US Treasuries, German Bunds, and French OATs through an almost identical arc, regardless of whatever was happening in Westminster on any given week. That alignment is the analytical puzzle this piece works through, because understanding why politics failed to move bonds in 2026 is at least as useful as understanding why it did in 2022.

Here is a concrete, data-grounded framework for separating political noise from genuine bond market drivers, tested against a live case study with cross-country evidence. After working through it, you will know exactly what questions to ask the next time a political crisis is framed as a yield-moving event.

Opening the year near 4.5%, the UK 10-year gilt yield edged downward through January and February, settling at a period low of around 4.3% in the final days of that month, close to when Peter Mandelson’s arrest took place on approximately 23 February 2026.

A sharp reversal then followed. From March onwards, yields climbed steeply, surpassing 4.9% before the month was half done, and carried on rising into April and beyond. The 5% level was breached in late April, shortly after Keir Starmer’s admission around 20 April that he had misled Parliament. A further leg higher brought yields to a six-month peak just above 5.1% in mid-May, after which a gradual pullback took hold, returning the yield to around 4.7% by late June 2026.

The mid-May peak above 5.1% marked the highest point for the UK 10-year gilt across the entire six-month period, a level not sustained for more than a few sessions before yields began retreating.

| Period | Approximate yield level |

|---|---|

| End-December 2025 | ~4.5% |

| Late February 2026 | ~4.3% (low point) |

| Mid-March 2026 | Above 4.9% |

| End of April 2026 | Above 5% |

| Mid-May 2026 (peak) | Above 5.1% |

| Late June 2026 | ~4.7% |

Source: Fisher Investments Editorial Staff; FactSet data as of 26 June 2026.

A political story fits this arc comfortably. Yields rose as Starmer’s position weakened. They peaked around maximum uncertainty. They retreated as an orderly transition appeared more likely. The narrative is tempting, which is precisely why it needs to be tested against what happened in other bond markets over the same window.

The political inputs were not trivial. Taken together, the sequence from January through June 2026 amounted to one of the most turbulent stretches in recent UK political history:

A conventional markets-react-to-politics framework would have predicted sustained selling pressure on gilts through this period: leadership vacuum, fiscal policy uncertainty, and a possible leftward shift in economic management. The question is whether gilts reacted to Westminster specifically, or whether something else was driving the bus.

Here is where the political narrative runs into trouble. When the same December-to-June window is examined across US Treasuries, German Bunds, and French OATs, the pattern in gilts stops looking like a UK-specific story.

| Country / Instrument | End-Dec 2025 | Late Feb 2026 | Mid-May 2026 | Late June 2026 |

|---|---|---|---|---|

| UK 10-year Gilt | ~4.5% | ~4.3% | Above 5.1% | ~4.7% |

| US 10-year Treasury | ~4.2% | Just under 4.0% | ~4.7% | ~4.4% |

| French 10-year OAT | ~3.5% | ~3.2% | 3.6%-3.8% | ~3.5% |

| German 10-year Bund | ~2.9% | Below 2.7% | 2.9%-3.1% | ~2.9% |

Source: Fisher Investments Editorial Staff; FactSet data as of 26 June 2026.

All four markets dipped into late February, rose from March through mid-May, then partially retreated through June. The UK, the US, France, and Germany each had distinct domestic political circumstances during this period. None of them shared a political story. All of them shared a yield pattern.

For domestic politics to be the primary driver of a country’s bond yields, those yields would need to break meaningfully away from the peer group, a sustained divergence that cannot be explained by the shared macro backdrop. In 2026, gilt yields remained within a globally elevated but internally consistent band. No sustained break from US Treasuries, Bunds, or OATs appeared at any point across the six months.

The UK-Germany spread is the most direct real-time measure of country-specific fiscal risk: when gilts sell off in line with Bunds, the spread holds roughly steady and the signal is global; when gilts sell off while Bunds stay anchored, the spread widens and investors have grounds to treat the move as a domestic warning.

If 2026 did not clear the threshold for country-specific yield divergence, the natural question is: what does clear it? The answer sits four years back.

The September 2022 mini-budget was the last time UK politics genuinely moved gilts independently of the global backdrop, and the mechanism was entirely different from anything that happened in 2026:

The Bank of England was forced to intervene in the long-end gilt market in September 2022, purchasing bonds to prevent a self-reinforcing spiral in pension fund liabilities. That intervention remains the clearest modern example of domestic politics overriding global bond market forces in a developed economy.

The Bank of England gilt market operation, announced on 28 September 2022, confirmed that the purchases were designed to restore orderly market conditions and reduce risks to UK financial stability, with the Bank explicitly citing the significant repricing of UK and global financial assets as the triggering condition.

Every one of those elements was absent in 2026:

The structural lesson is straightforward. Markets respond to policy and institutions, not personalities. A change of prime minister without a credible, near-term threat to fiscal or monetary frameworks does not justify sustained repricing of a sovereign’s risk relative to peers.

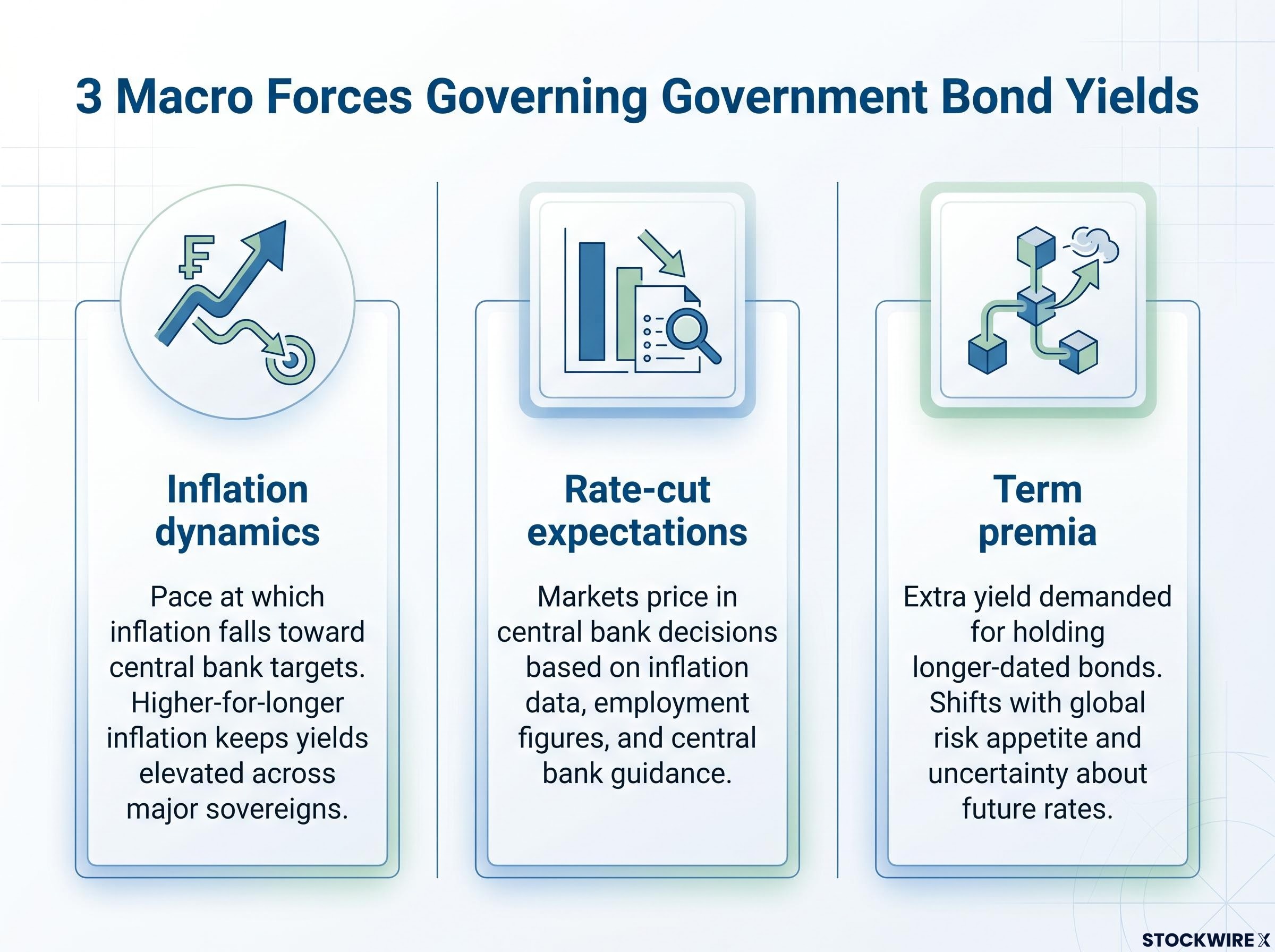

The cross-country data points to a common conductor. Institutional fixed-income analysis for 2026 consistently identifies three macro forces governing developed-market yield movements:

These three forces operated simultaneously across Treasuries, Bunds, gilts, and OATs throughout the first half of 2026, producing the synchronised pattern the data showed. For domestic politics to override this coordination, a country would need to generate a fiscal or institutional shock large enough to reprice its bonds independently. That is a high bar, and 2026 Westminster did not come close to clearing it.

The inverse relationship between price and yield is central to reading any sovereign market: bond yield mechanics mean that a fixed coupon payment produces a higher return when the purchase price falls, which is why a broad sell-off in government debt automatically pushes yields upward across all markets simultaneously.

The late-February dip across all four markets aligns with a period when rate-cut expectations were relatively elevated, pulling yields lower. The March-through-May rise aligns with those expectations being pushed back as inflation data proved more persistent than anticipated. The June retreat reflects some stabilisation in the outlook. The analytical consensus view, drawn from institutional commentaries, is that this macro backdrop explains the shared pattern more completely than any single country’s domestic politics.

Post-QE yield normalisation provides an important backdrop for reading the 2026 arc: a decade of artificially suppressed yields through central bank asset purchases created an abnormally low baseline, meaning the return toward 4.5-5% territory across developed markets in 2025 and 2026 is consistent with pre-QE historical norms rather than a signal of structural fiscal stress.

The 2026 UK episode distils into four practical questions you can apply the next time a political crisis is framed as a bond market event:

For investors wanting to go further and build a pre-event framework for mapping political announcements onto portfolio exposures before yields move, our deep-dive into policy-driven market risk examines three 2026 case studies where the transmission from policy announcement to asset price was faster and more asset-specific than broad political risk narratives anticipated.

In 2026, the macro floor held across developed markets. UK political drama played out above it, generating headlines and commentary, but never breaking through to produce the kind of country-specific yield divergence that would justify treating Westminster as the primary driver.

That finding comes with an honest conditional. Global macro dominance is not permanent. The 2022 mini-budget proved that a credible, near-term fiscal shock can override the shared macro backdrop and produce real, measurable divergence in a single country’s bond market. The framework is a default presumption, not a guarantee.

The macro floor holds until fiscal or institutional credibility is directly threatened. At that point, country-specific repricing is warranted, and the peer-yield comparison will show you the divergence in real time.

The late-June gilt yield of approximately 4.7%, broadly consistent with contemporaneous market quotes, sits in line with the peer group’s partial retreat. The signal is not that UK politics never matters. The signal is that you can identify in advance the specific conditions under which it would matter: a credible fiscal commitment that diverges materially from peers, or a genuine threat to central bank independence. Until those conditions are met, the macro layer deserves your analytical weight, and the political headlines deserve your scepticism.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The three primary bond market drivers are inflation dynamics, central bank rate-cut expectations, and term premia. These forces operate simultaneously across developed markets, which is why UK gilts, US Treasuries, German Bunds, and French OATs frequently move in the same direction regardless of each country's domestic political situation.

The March-through-May 2026 gilt yield rise, from around 4.3% to above 5.1%, aligned with inflation data proving more persistent than markets anticipated, pushing back rate-cut expectations. The same pattern appeared in US Treasuries, Bunds, and OATs over the identical period, pointing to a global macro cause rather than UK-specific political turbulence.

Domestic politics becomes a primary bond market driver only when it creates a credible, near-term threat to fiscal sustainability or central bank independence. The September 2022 UK mini-budget is the clearest modern example: unfunded tax cuts in an inflationary environment blew out gilt yields relative to peers and forced a Bank of England emergency intervention, conditions entirely absent during the 2026 political turbulence.

The most reliable test is to check whether peer yields, particularly US Treasuries and German Bunds, are moving in the same direction. If they are, global macro is the dominant force. A country-specific political driver would show up as a sustained widening of that country's yield spread against peers, such as the UK-Germany spread, not a move that tracks across all four major sovereign markets simultaneously.

The UK-Germany spread measures country-specific fiscal risk in real time: when gilts sell off in line with Bunds the spread holds steady and the signal is global, but when gilts sell off while Bunds stay anchored the spread widens and investors have grounds to treat the move as a domestic warning. In H1 2026, no sustained spread widening appeared, confirming the move was macro-driven rather than a Westminster-specific repricing.