BOQ Pays 6.39% Fully Franked, but the Risks Are Real

59 mins ago

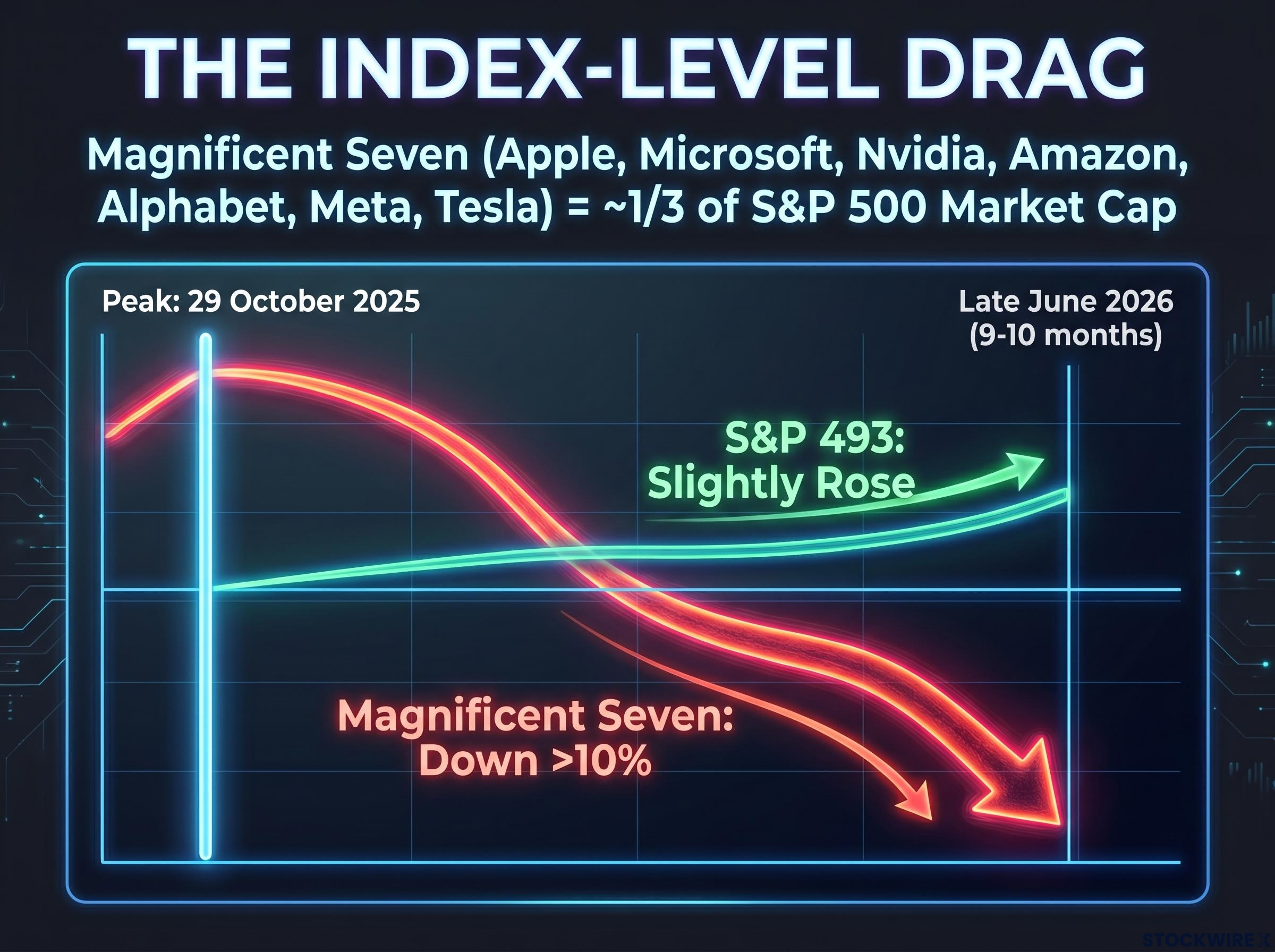

The Magnificent Seven have lost more than 10% since peaking on 29 October 2025, even as artificial intelligence dominates global market conversation and the AI infrastructure build-out accelerates. That divergence is not a glitch.

Deutsche Bank strategist Jim Reid argues it is the predictable result of four cyclical headwinds converging on the same group at the same time. His analysis, published 30 June 2026, reframes nine to ten months of mega-cap tech weakness not as a sentiment wobble but as a structural rotation with identifiable causes. For U.S. equity investors who built significant exposure to these names during 2023 and 2024, understanding why the former engine of index performance stalled matters more than watching the daily price action.

Here is a concrete four-factor checklist for monitoring when the Magnificent Seven may be positioned to reclaim market leadership, rather than guessing at headlines. Each factor has its own cycle. Tracking them offers more signal than tracking the AI narrative itself.

The timeline anchors everything that follows:

Nine to ten months outlasts most positioning corrections. It outlasts earnings-driven sentiment swings. It outlasts the kind of brief drawdowns that momentum stocks routinely absorb and reverse. The duration alone demands a structural explanation, not a narrative one.

While the Magnificent Seven fell more than 10% from their October 2025 peak, the other 493 stocks in the S&P 500 slightly rose over the same period.

That contrast is what makes this analytically significant. The broader market is not weak. The headline index looks stagnant because the names that carry the most weight are the ones dragging it lower. For investors who anchor their U.S. equity thesis to mega-cap tech, the question is no longer whether this dip is temporary. It is why the drag has lasted long enough to constitute a regime shift in market leadership.

The full picture on how index concentration has distorted market-level signals emerges from S&P 500 market breadth in 2026, which examines April’s historic monthly return alongside the fourth-narrowest breadth reading in nearly four decades, showing exactly how a small cohort of names can make a headline index mislead.

The Magnificent Seven refers to seven mega-cap technology companies:

Together, these seven names account for an estimated one-third of the S&P 500’s total market capitalisation (a widely cited approximate figure). That concentration is the mechanism that turns a sector-level rotation into an index-level problem. When the median S&P 500 stock is slightly positive over the same period the headline index appears flat, the disconnect tells you exactly where the weakness lives: it is not broad, it is concentrated in the names that weigh most heavily on the index.

In a cap-weighted index, a 10% fall in the Magnificent Seven moves the headline number by more than a 10% rise across a comparable number of smaller-cap stocks. That arithmetic means 2026’s index-level stagnation is not a story about a weak U.S. economy or broad earnings failure. It is specifically a story about what happens when a concentrated set of former leaders rotate out simultaneously, and every other stock doing well is not enough to offset the drag.

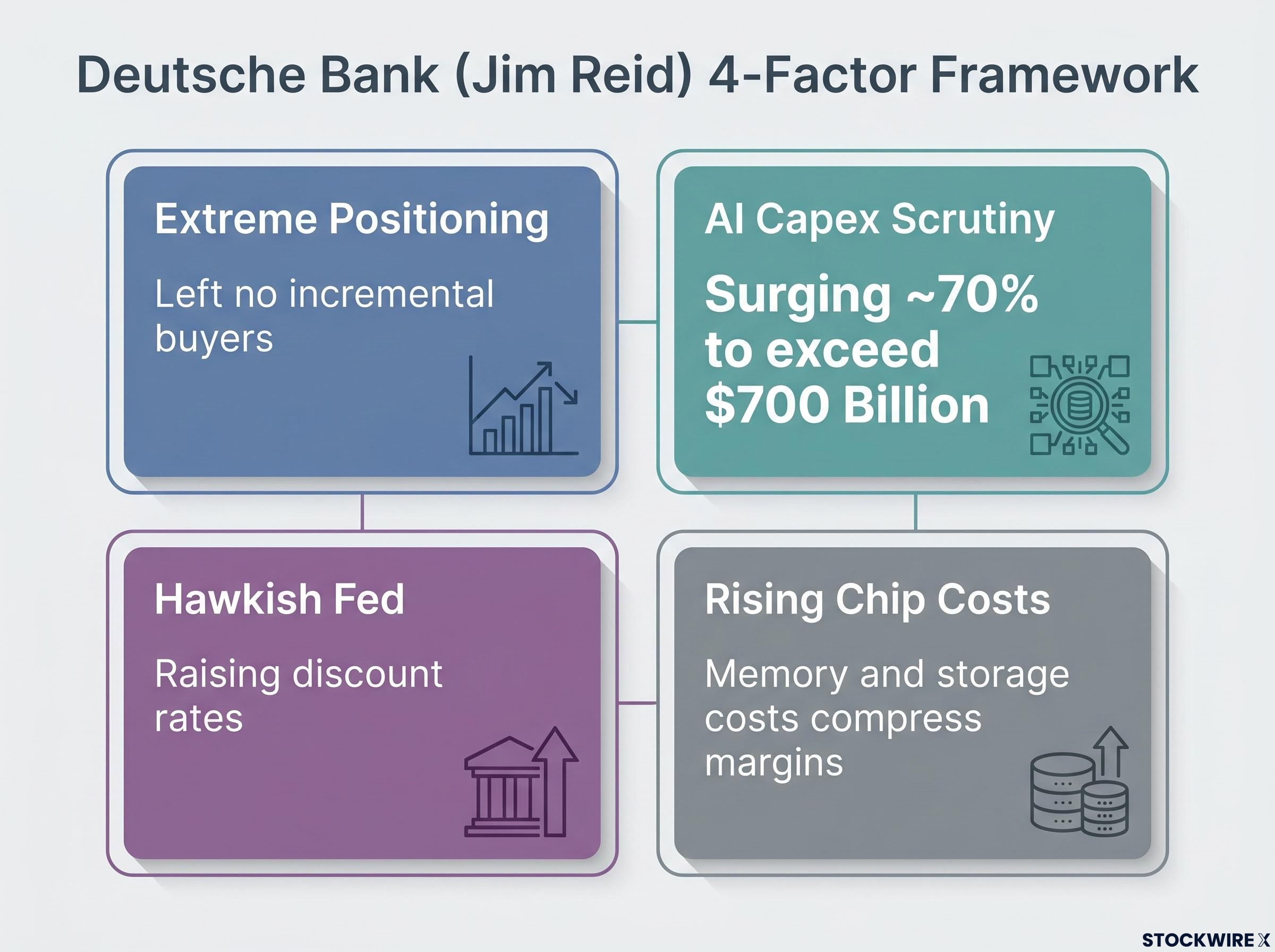

Jim Reid, a strategist at Deutsche Bank, identified the four headwinds that explain why the Magnificent Seven have underperformed despite persistent global AI enthusiasm. His contribution is not simply naming four problems. It is showing that they arrived together, which is why the weakness has been durable rather than self-correcting.

Reid noted that the weak performance of these stocks ran against the grain of the prevailing environment: the first half of 2026 was defined by the Iran conflict and what he described as widespread global “AI fever,” a backdrop that would ordinarily have been favourable for mega-cap technology names.

The four headwinds:

| Headwind | Core mechanism |

|---|---|

| Extreme positioning | Consensus long exposure shrank the pool of incremental buyers, amplifying downside from even modest negative catalysts |

| AI capex scrutiny | Investor stance shifted from enthusiasm about AI infrastructure scale to demanding evidence of durable free cash flow returns |

| Hawkish Fed | Higher discount rates compress valuation multiples on long-duration growth stocks, making distant payback periods less tolerable |

| Rising chip costs | Memory and storage shortages raise input costs for platform companies running large AI workloads, squeezing margins |

What the reader should take from this table: once you can name the four conditions, you can monitor each one independently for signs of abatement rather than relying on sentiment headlines to tell you when the group’s fortunes might turn.

According to Deutsche Bank’s equity strategy team, large-cap tech positioning had climbed to an extreme level by end of May 2026. After years in which these stocks contributed a disproportionate share of S&P 500 gains, investor exposure had become very large and highly consensus. The pool of incremental buyers had shrunk to the point where even modest negative news triggered outsized de-risking.

That is where the second headwind, AI capital expenditure scrutiny, stepped in as the catalyst. Industry estimates suggest AI-related capex could surge approximately 70% to exceed $700 billion in a single year (a widely cited forecast, though not independently verified). The scale of that commitment shifted the market’s posture from excitement about AI infrastructure to something more demanding.

Hyperscaler capex commitments reached approximately $130 billion in Q1 2026 alone across Amazon, Microsoft, Alphabet, and Meta, with full-year 2026 combined guidance approaching $725 billion — numbers that give concrete scale to the ‘show me’ pressure investors began applying once AI infrastructure spending crossed into historically unprecedented territory.

Investors moved to a “show me” stance: demanding evidence that aggressive AI spending translates into durable, monetisable free cash flow rather than just top-line growth.

The interaction between these two headwinds created an amplifying loop. Crowded positioning meant any catalyst hit harder than it would in a normally distributed ownership base. Capex scrutiny provided exactly that catalyst at scale, and the resulting de-risking pushed prices lower, which in turn made the remaining holders more nervous.

By June 2026, Deutsche Bank observed that positioning had normalised toward neutral. That removes one headwind: the mechanical seller is largely gone. But it does not resolve the capex credibility overhang. Management teams still need to demonstrate that aggressive AI spending produces returns. Positioning normalising is a necessary condition for a leadership reversal; it is not a sufficient one.

Reid’s third factor is the Federal Reserve’s more hawkish stance. Growth equities like the Magnificent Seven are structurally sensitive to discount rates: the higher the rate applied to distant cash flows, the less those future earnings are worth today. A more hawkish Fed compresses the valuation multiples that were central to these stocks’ premium, and it interacts directly with the capex concern. Higher discount rates make distant payback periods from AI infrastructure spending less acceptable, compounding the “show me” posture.

Growth stock valuations are structurally sensitive to discount rate changes because the present value of cash flows projected many years out shrinks disproportionately when rates rise, which is precisely why a hawkish Federal Reserve inflicts more damage on long-duration names like the Magnificent Seven than on companies with near-term earnings.

The fourth headwind, rising memory and storage chip prices, adds a supply-chain layer that splits the technology sector in two. Market reports describe a shortage of memory chips critical for AI workloads, data centres, and cloud computing, contributing to higher component prices. That creates an internal divergence within what investors often treat as a single trade:

Memory chip price dynamics extend well beyond 2026 according to S&P Global Ratings, which confirmed in June 2026 that the repricing cycle runs through at least 2028, with Samsung, SK Hynix, and Micron collectively redirecting capacity toward high-bandwidth memory for AI customers and structurally tightening the commodity memory supply that platform companies depend on.

| Headwind | Who it pressures | Who it benefits |

|---|---|---|

| Fed hawkishness | Long-duration growth stocks | Rate-sensitive value sectors |

| Rising chip costs | Platform companies with large compute loads | Semiconductor manufacturers |

The three interaction effects across all four headwinds reinforce one another:

For a U.S. equity investor holding broad technology exposure, this means “being in tech” in 2026 is not a coherent position. The Fed and chip cost dynamics have split the sector into winners and losers moving in opposite directions, and the Magnificent Seven sit predominantly on the cost-pressure side.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The rotation away from the Magnificent Seven has funded leadership elsewhere, and Reid’s most striking data point illustrates how far the momentum has migrated.

As of 30 June 2026, South Korea’s KOSPI index had posted year-to-date gains in excess of 100%, a figure Reid cited as concrete evidence of where AI-related enthusiasm has been rewarded in 2026.

That is not a curiosity. It is Reid’s concrete illustration that AI enthusiasm in 2026 has been rewarding markets that can express the trade without carrying the four headwinds the Magnificent Seven bear. If you want AI-adjacent exposure with less cyclical drag, that is where the global market has been telling you to look.

The rotation is partly self-reinforcing: capital moving into non-tech sectors and select international markets has been funded by selling the Magnificent Seven, which perpetuates their underperformance even as fundamentals remain intact.

Reid’s forward implication translates into a concrete monitoring checklist. All four conditions need to begin abating before a sustained leadership reversal is plausible:

Tracking these four conditions offers a more durable framework for timing any re-engagement with the Magnificent Seven than one that depends on sentiment reversals or AI news cycles alone.

Reid’s framework does not declare an end to AI or to mega-cap tech’s long-term relevance. That distinction matters for how you size and position exposure.

What has changed:

What has not changed:

The question facing investors is not whether to own these names long-term. It is whether the four cyclical conditions justify premium exposure at current multiples right now. Reid’s analysis gives you a framework for answering that question on a rolling basis: watch the four headwinds, not the headlines.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Deutsche Bank's Jim Reid identified four converging headwinds: extreme consensus positioning that left no incremental buyers, investor scrutiny shifting from AI capex enthusiasm to demanding proof of free cash flow returns, a more hawkish Federal Reserve compressing long-duration growth multiples, and rising memory and storage chip costs squeezing margins for platform companies running large AI workloads.

The Magnificent Seven declined more than 10% from their 29 October 2025 peak through approximately late June 2026, a drawdown lasting nine to ten months, which outlasts typical positioning corrections and sentiment-driven pullbacks.

The four conditions are: positioning normalising toward neutral (already the most advanced, largely resolved by June 2026), management teams demonstrating durable returns from AI infrastructure spending, the Federal Reserve shifting to a less hawkish stance, and memory and storage chip prices easing through their own supply-demand cycle.

Because the Magnificent Seven account for roughly one-third of total S&P 500 market capitalisation, a 10% decline in these seven names exerts more downward pressure on the headline index than gains across a comparable number of smaller-cap stocks can offset, turning a sector-level rotation into an index-level drag.

No. Reid's framework is explicit that the underlying AI infrastructure build-out and the competitive moats of these seven companies remain intact; the underperformance reflects four identifiable cyclical pressures on valuation and positioning, not a structural impairment of the AI thesis itself.