Endeavour Group’s Dividend Reset: Income Stock or Reinvestment Bet?

30 mins ago

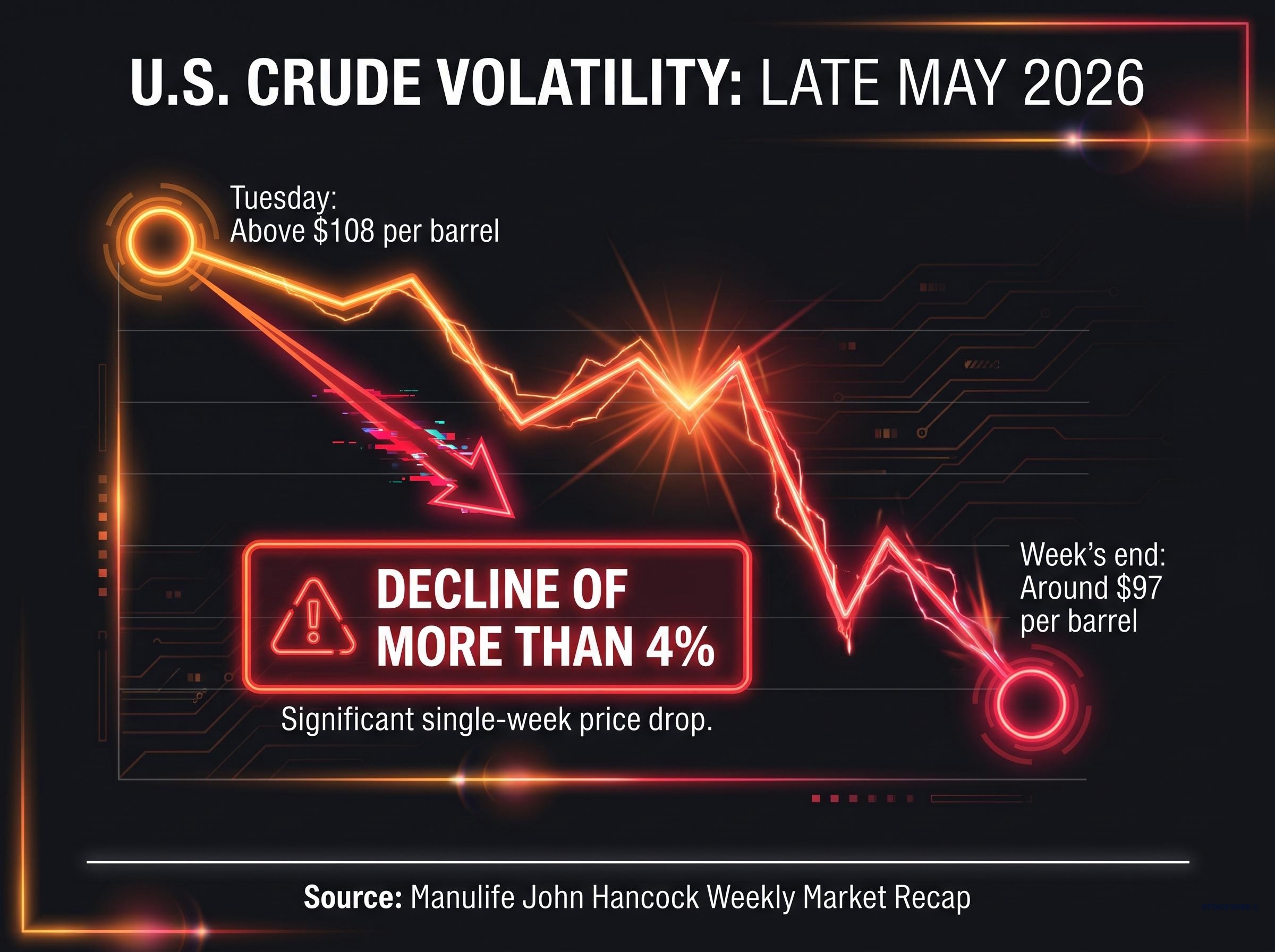

U.S. crude swung from above $108 per barrel to below $100 in a single week in late May 2026, a price arc that captures exactly the kind of geopolitical whipsaw BCA Research is warning investors not to bet on. With peace negotiations advancing in both the Middle East and Eastern Europe, a growing segment of the market appears to be pricing in a “peace dividend” that BCA Research analysts, publishing on 30 May 2026, argue is unlikely to fully materialise. The firm’s framework holds that even confirmed ceasefires may deliver far less market relief than expected, while the path to those agreements carries escalation risks that investors are currently underweighting.

What follows unpacks BCA Research’s analytical framework, explains the specific mechanics behind their cautious view, and translates their asset allocation calls into actionable context for investors tempted to front-run a resolution that may not arrive cleanly.

The intuitive trade is straightforward: ceasefire equals relief, relief equals lower energy costs, lower energy costs equal a risk-on environment. BCA Research’s 30 May 2026 analysis argues each link in that chain is weaker than the market assumes.

The firm’s central thesis is that near-term agreements in Iran and Ukraine are likely to produce modest stabilisation, not a restoration of pre-conflict market conditions. Three structural reasons underpin this view:

Emergency reserves and supply rebalancing efforts have failed to halt inventory drawdowns running at more than double their historic pace, and the IEA projects no supply-demand balance before October 2026, reinforcing BCA’s structural case that commodity prices will remain elevated well past any ceasefire announcement.

The Manulife John Hancock Weekly Market Recap for late May 2026 illustrates the point in real time: U.S. crude climbed above $108 per barrel on Tuesday before finishing the week around $97, a decline of more than 4%, with the volatility explicitly tied to Middle East conflict negotiations.

BCA Research warns that markets may have already factored in much of the upside potential from Middle East de-escalation, meaning a confirmed deal could deliver less positive price action than investors currently expect.

Investors who reposition aggressively on ceasefire headlines risk being caught by a market that reprices upward again as the underlying supply dynamics reassert themselves.

BCA Research’s most counterintuitive claim is that the closer the Russia-Ukraine conflict gets to a resolution, the higher the short-term danger. The logic runs against the grain of standard peace-process optimism, and it deserves careful unpacking.

BCA assessed on 30 May 2026 that the probability of a significant Russian provocation has risen, not fallen, as settlement discussions advance. The firm identifies three drivers behind this dynamic:

BCA’s framing is distinctive: a ceasefire would ultimately serve Russia’s long-term economic interests, yet the path to that ceasefire passes through a period of heightened, not diminished, risk.

The implication is that peace-process headlines should not be read as unambiguous risk-off signals. The process of reaching a settlement can itself generate the kind of shock event, a provocation designed to expose fractures in NATO cohesion, that destabilises portfolios positioned for resolution. “Ceasefire approaching” and “risk receding” are not synonymous, and BCA’s framework urges investors to treat them accordingly.

Geopolitical risk is among the most frequently cited and least precisely understood forces in market commentary. BCA Research’s framework becomes more useful when placed against a working model of how conflict-related uncertainty actually moves asset prices.

A geopolitical risk premium is the additional return investors require to hold assets exposed to conflict-related uncertainty. It is not a fixed number; it inflates and deflates with news flow, often moving faster than the underlying fundamentals justify. The oil price swing in late May 2026 (above $108 intraday, settling near $97 by week’s end) is a textbook illustration: the barrel’s value did not change by $11 in fundamental terms, but the risk premium attached to it did.

The recurring gap between geopolitical risk and stock market behaviour is not a 2026 anomaly: markets process conflict-related events as probability-adjusted inputs to future earnings rather than proportional headline shocks, which is why the S&P 500 can sit near record levels while a major supply route remains contested.

Energy markets serve as the primary transmission channel between geopolitical events and broader portfolio performance. When a conflict threatens supply routes or production capacity, energy costs rise, feeding into corporate margins, transportation costs, and consumer prices globally.

NBER research on geopolitical shocks and commodity markets documents how conflict-driven supply disruptions create persistent price effects that outlast the underlying military events, a finding that supports BCA’s view that commodity prices retain structural elevation even after preliminary agreements are announced.

The front-running problem: Investors who reposition ahead of a confirmed resolution often absorb the downside if that resolution is delayed, partial, or followed by renewed tension. The S&P 500 recorded eight consecutive weekly gains as of late May 2026, the longest such streak since late 2023, according to the Manulife John Hancock Weekly Market Recap. That streak reflects optimism being priced in before formal confirmation; if confirmation falters, the repricing can be swift.

The table below outlines how different geopolitical scenarios tend to propagate through asset classes:

| Geopolitical Scenario | Typical Market Impact | Asset Classes Most Affected |

|---|---|---|

| Ceasefire announced | Short-term relief rally; energy prices may ease modestly | Oil futures, defence equities, safe-haven currencies |

| Escalation event | Risk-off move; flight to safety | Equities broadly, government bonds, USD and JPY |

| Sanctions tightened | Sector-specific repricing; supply-chain disruption | Energy, industrials, emerging-market equities |

| Energy supply disruption | Commodity spike; margin compression in energy-intensive sectors | Oil and gas, airlines, shipping, consumer staples |

Understanding these transmission mechanics allows investors to evaluate conflict-era market commentary, including BCA’s own recommendations, with greater precision.

BCA Research’s analytical framework translates into three concrete positioning recommendations, each flowing directly from the dynamics outlined above. These are BCA’s own calls, not a consensus view among major strategy houses.

The simultaneous oil, inflation, and bond repricing triggered by the May 2026 conflict environment means that de-escalation would not automatically unlock rate cuts, because central banks have adopted a conditional look-through posture on energy-driven inflation rather than explicitly linking policy to the geopolitical premium.

| Asset Class | BCA Recommendation | Rationale |

|---|---|---|

| U.S. equities | Overweight | Lower direct exposure to energy-price volatility and conflict spillovers |

| European equities | Underweight (relative) | Higher exposure to Russia-Ukraine economic impact and energy costs |

| USD | Hold / safe-haven allocation | Maintain until formal ceasefire confirmation in both conflict zones |

| JPY | Hold / safe-haven allocation | Maintain until formal ceasefire confirmation in both conflict zones |

| Broad equities and bonds | Cautious | Much of Middle East de-escalation upside may already be priced in |

Each position is designed to perform adequately whether the geopolitical situation resolves or deteriorates, rather than betting on either outcome.

BCA Research’s framework distils to a single decision rule: formal confirmation of resolution is the trigger for repositioning, not the announcement of negotiations or preliminary agreements. The distance between “peace is coming” and “peace has arrived” is exactly where portfolio risk concentrates right now.

The oil price arc of late May 2026 reinforces this in miniature. A barrel of U.S. crude moved from above $108 to around $97 in a matter of days, driven entirely by shifts in negotiation sentiment rather than changes in physical supply. That kind of volatility does not disappear when a preliminary agreement is announced; it disappears when the supply chain, the insurance markets, and the shipping routes confirm the agreement is holding.

There is, of course, a legitimate possibility that ceasefires materialise quickly and markets rally further. BCA’s framework does not deny this scenario. Rather, the firm’s positioning is designed to survive it comfortably while protecting against the more probable outcome: that resolution is partial, delayed, or followed by renewed tension that catches repositioned portfolios off guard.

Investors who understand the structural limitations of ceasefire relief, the mechanics that keep commodity prices elevated even after agreements, the escalation risk that precedes settlements, are better equipped to respond to headlines without being driven by them. The geopolitical premium is priced in until the paperwork is signed, and not a moment before.

For investors who recognise the intellectual case for patience but find it difficult to hold discipline when ceasefire headlines hit, our full explainer on avoiding reactive geopolitical trades examines the behavioural research behind why retail investors consistently underperform during high-attention geopolitical events and provides a concrete decision filter for separating systematic rebalancing from costly headline-driven repositioning.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements are speculative and subject to change based on market developments and geopolitical conditions.

A geopolitical risk premium is the additional return investors require to hold assets exposed to conflict-related uncertainty. It inflates and deflates with news flow, often faster than underlying fundamentals justify, which is why U.S. crude moved from above $108 to around $97 in a single week in late May 2026 driven by shifts in negotiation sentiment rather than changes in physical supply.

BCA Research recommends maintaining positions in the U.S. dollar and Japanese yen as safe-haven currencies because preliminary peace agreements are insufficient triggers for repositioning; the firm's view is that formal, confirmed ceasefires in both the Middle East and Ukraine are required before reducing safe-haven exposure.

BCA Research's framework suggests overweighting U.S. equities relative to European assets, holding safe-haven currencies (USD and JPY), and maintaining broad caution on equities and bonds until ceasefires are formally confirmed, since much of the upside from Middle East de-escalation may already be priced into markets.

BCA Research assessed in May 2026 that the probability of a significant Russian provocation rises as settlement discussions advance, because Russia may execute a major military action to strengthen its negotiating position or satisfy domestic political pressures before agreeing to terms, meaning the peace process itself can generate destabilising shock events.

BCA Research argues that any near-term U.S.-Iran deal would address immediate hostilities but is unlikely to unwind the supply-chain disruptions and infrastructure damage already embedded in energy markets, with the IEA projecting no supply-demand balance before October 2026, meaning oil prices are expected to remain considerably elevated relative to year-start levels even after an agreement.