Stock-Bond Correlation Hits 30-Year Extreme, Rattling 60/40 Investors

15 mins ago

The Etsy earnings report delivered on 29 April 2026 sent shares jumping, defying Wall Street’s pessimistic revenue forecasts. This first-quarter financial update marks a defining juncture for the US e-commerce giant following a sustained period of post-pandemic operational friction and user attrition. Investors have watched the platform struggle to retain the explosive growth recorded three years ago, leading to lowered expectations across the sector.

The new figures suggest management has finally found a floor for buyer retention, shifting the narrative from contraction to cautious expansion. The following analysis breaks down the key metrics driving this resurgence, the reality behind changing user engagement trends, and the long-term impact of its major subsidiary divestiture. Understanding these components provides clarity on how the company plans to secure its market position throughout the remainder of the year.

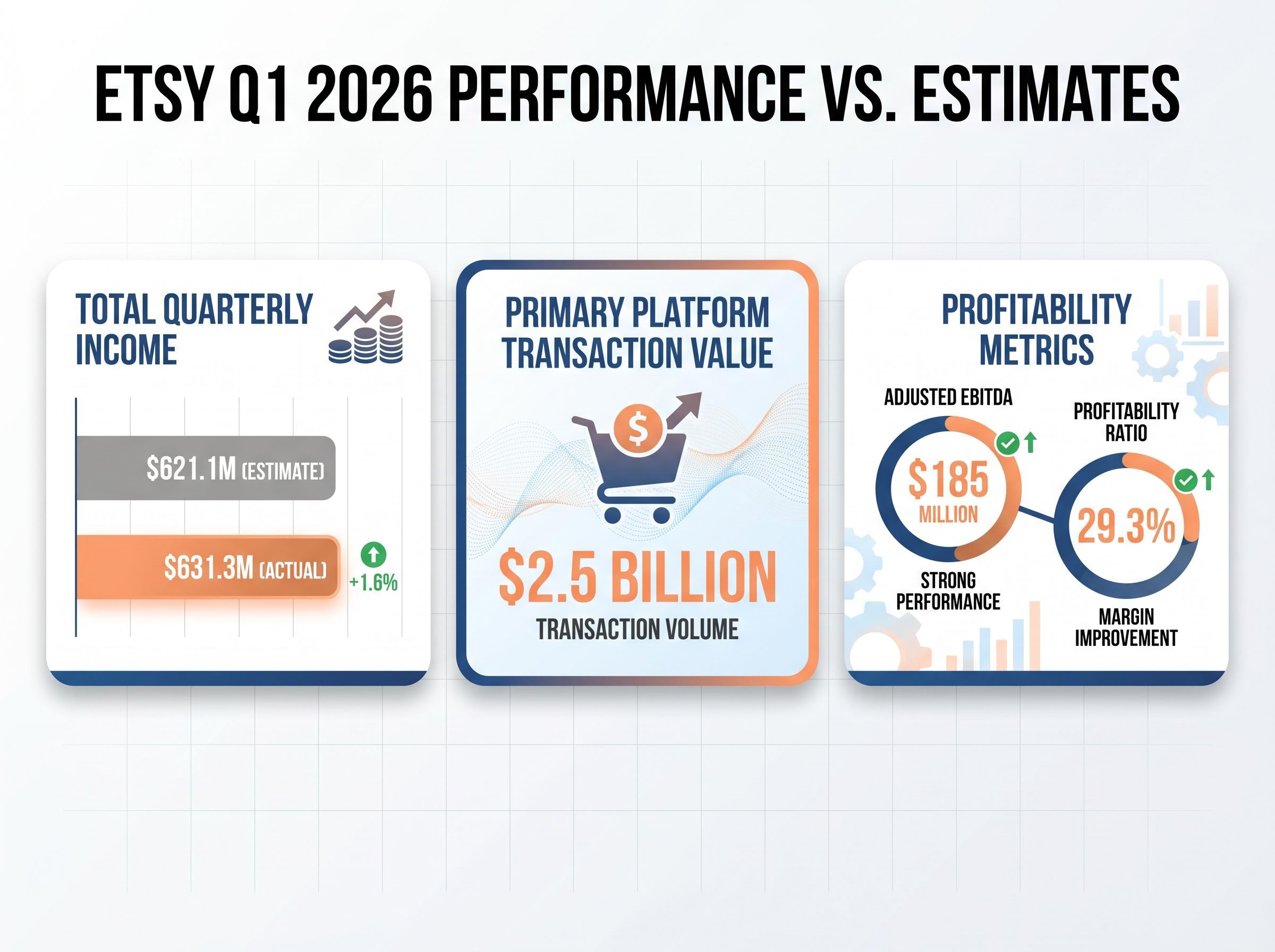

The reality of the financial turnaround stands in sharp contrast to the pessimistic pre-earnings estimates that defined recent market sentiment. Wall Street analysts projected a top-line contraction, but the actual figures revealed a 1.6% outperformance on total quarterly income. According to company data, the company reported $631.3 million in total quarterly income, topping the consensus estimate of $621.1 million.

According to company data, while modified per-share profits of $0.60 narrowly trailed the $0.62 prediction, the broader balance sheet signals strong underlying platform health. According to company data, adjusted EBITDA reached $185 million, yielding a solid 29.3% profitability ratio. Investors and market observers focused on the revenue beat and margin strength over the minor per-share profit miss, evidenced by the 6.3% stock surge immediately after the disclosure.

The official Etsy Form 8-K filing details the specific operational efficiencies that drove this margin strength, providing a clear breakdown of the adjusted EBITDA calculations that fueled early market optimism.

| Metric | Wall Street Estimate | Q1 2026 Actual |

|---|---|---|

| Total Quarterly Income | $621.1M | $631.3M |

| Modified Per-Share Profits | $0.61 | $0.60 |

According to company data, the primary platform transaction value expanded by 5.5% to hit $2.5 billion. This represents a stark recovery from the 0.5% contraction recorded in the preceding period. Income specifically from the main digital storefront grew 7.6% compared to the prior year, proving the core business can generate organic demand independent of secondary acquisitions.

Top-line dollars confirm financial stability, but the strategic relief for management comes from finally halting a 24-month slide in active purchasers. For the first time in two years, the platform achieved quarter-over-quarter purchaser expansion. This renewed momentum contrasts sharply with the challenging fourth quarter of 2025, when active buyers dropped to 93.54 million.

The increase in active shoppers connects directly to recent operational initiatives and shifting US consumer habits. Financial beats can be engineered through cost-cutting, but user growth represents true organic demand. The latest metrics prove that real people are returning to the digital storefront in meaningful numbers.

While headline US retail sales data occasionally presents an optimistic picture of domestic consumption, deeper analysis reveals a widening divide where affluent households are driving the majority of discretionary volume.

The company recorded annual increases across three critical engagement metrics:

Newly acquired shoppers Active merchants * Average transaction volume per user

E-commerce financials often require looking past simple user counts to understand how a platform converts transactions into corporate profit. A digital marketplace generates revenue by keeping a specific percentage of every transaction processed on its infrastructure. This mechanism explains why pricing power serves as the engine driving the current quarterly results.

Marketplace Take Rate A marketplace take rate is the percentage of the total transaction value that a platform retains as revenue through listing fees, payment processing charges, and optional advertising services.

The relationship between Gross Merchandise Sales (GMS) and actual revenue generation dictates overall profitability. When the company facilitated $2.5 billion in transaction value during the first quarter, the take rate determined exactly how many of those dollars became corporate income. A platform can increase profitability without requiring a proportional explosion in new users, provided the take rate and transaction volumes align effectively, a dynamic management expects to continue with a projected take rate of approximately 25.7% for the second quarter of 2026.

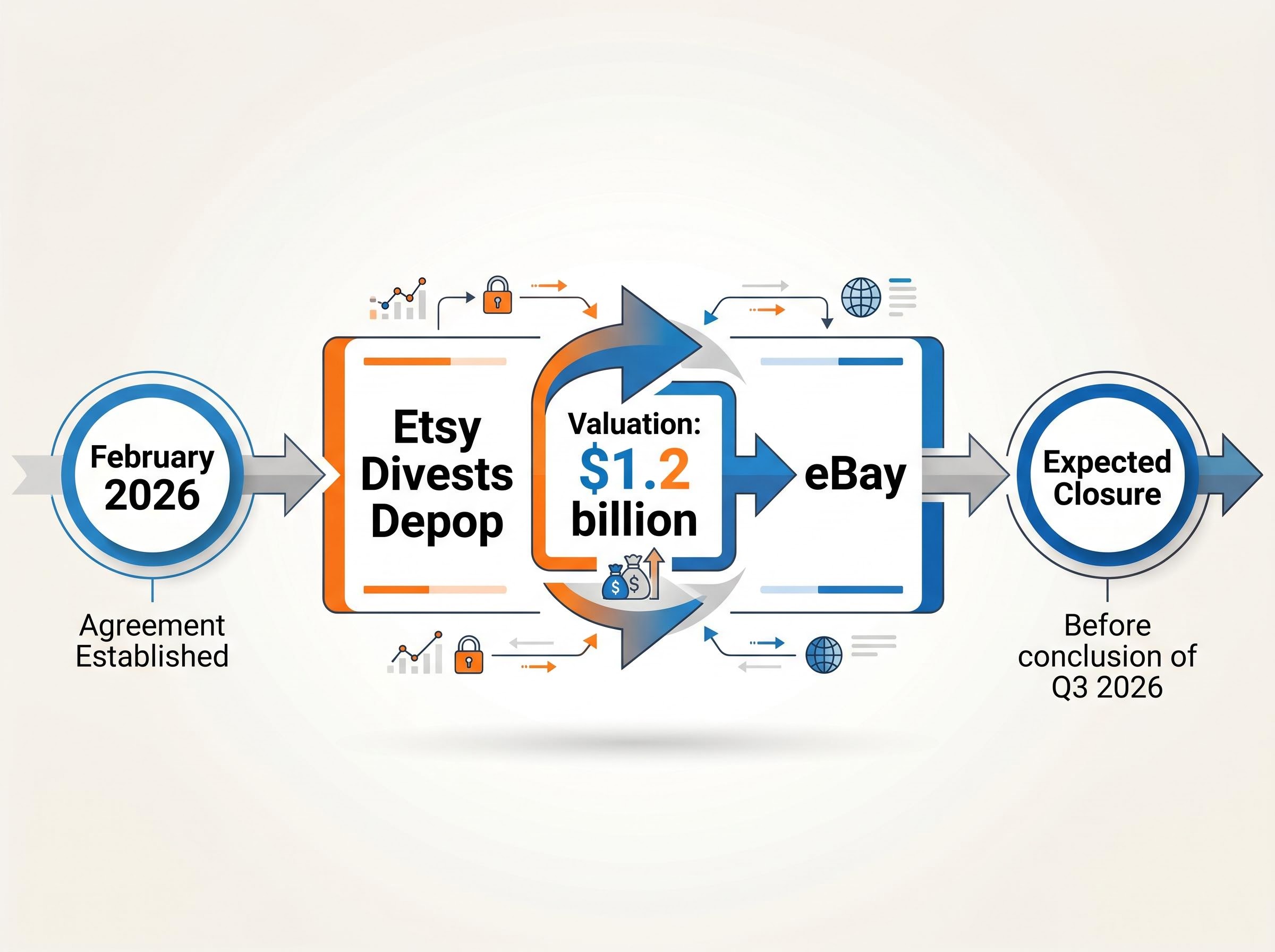

The broader corporate strategy involves more than just organic recovery, extending to a deliberate narrowing of the company’s core operational focus. In February 2026, the company established an agreement to divest its Depop subsidiary to eBay for a $1.2 billion valuation. Selling a major subsidiary to a direct rival changes the competitive structure of the US fashion resale sector.

Global coverage of the Depop acquisition notes that this transfer of assets specifically targets younger consumer demographics, an area where legacy auction sites have historically struggled to maintain relevance.

This influx of capital and reduction in operational distraction positions the company defensively against broader e-commerce pressures. The current financial report completely omits Depop metrics due to the pending nature of the transaction. Management framed the sale as a calculated decision to streamline operations and refocus resources entirely on the primary digital storefront.

The expected regulatory and financial closure of the deal is anticipated before the conclusion of the third quarter of 2026. Separating these metrics from the core financials allows investors to evaluate the primary marketplace without the accounting noise of a pending corporate divestiture.

Past performance provides context, but Wall Street will judge the company entirely on the new performance bar management has set for the remainder of the calendar year. The executive team highlighted upgraded confidence regarding transaction volumes for the upcoming quarter, connecting the forward guidance back to the baseline established in the first-quarter beat. These specific profitability forecasts signal sustained operational efficiency.

The official targets for the coming periods establish clear benchmarks:

The combination of the first-quarter revenue beat, the return of buyer growth, and the Depop divestiture forms a cohesive narrative of corporate streamlining. The $1.2 billion transaction with eBay will arm the company with significant capital for its next phase of US market competition. However, sustaining this momentum requires converting newly acquired first-quarter shoppers into loyal, repeat purchasers.

For investors wanting to contextualise this e-commerce recovery against broader macroeconomic headwinds, our detailed coverage of US recession risks examines the fragile state of household savings buffers that could constrain mass-market discretionary spending in the coming quarters.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Etsy reported total quarterly income of $631.3 million, exceeding estimates by 1.6%, and achieved an adjusted EBITDA of $185 million, despite a minor per-share profit miss.

Etsy successfully halted a 24-month decline in active purchasers, achieving quarter-over-quarter expansion in Q1 2026 through operational initiatives and favorable consumer habits.

Etsy is divesting Depop to eBay for $1.2 billion to streamline operations, refocus resources on its primary digital storefront, and strengthen its competitive position.

A marketplace take rate is the percentage of total transaction value a platform retains as revenue; it is crucial for Etsy as it allows the company to increase profitability without solely relying on proportional new user growth, with a projected Q2 2026 rate of 25.7%.