Why AUD/USD Hinges on the Strait of Hormuz, Not the RBA

1 hr ago

Thursday morning brings a highly anticipated pre-market release for investors tracking the latest Insperity earnings figures. The April 30, 2026 report serves as a demanding test for management following a challenging fourth quarter in 2025. The previous period was marked by elevated benefit expenses and unexpected customer attrition, leaving market participants looking for signs of an operational rebound.

A detailed breakdown of disparate financial forecasts, insider buying activity, and Wall Street sentiment reveals the stakes ahead of the opening bell. The human resources services provider faces scrutiny from market experts who are weighing the prospects of a quick recovery against ongoing structural headwinds. Investors must manage a complex set of expectations, balancing optimistic internal projections with more conservative consensus estimates.

The upcoming call will clarify whether recent strategic adjustments are translating into tangible financial improvements. Management must provide clear answers regarding profit margins and client retention rates. The market reaction will likely depend on the forward guidance as much as the backward-looking data.

Conflicting financial expectations dominate the narrative for the first quarter of 2026. According to some reports, optimistic top-end targets suggest profits could reach $1.69 per share alongside $1.96 billion in total sales. However, official company guidance presents a wider range, placing expected earnings per share between $1.03 and $1.50.

These Form 8-K disclosures establish the fundamental baseline expectations that management must now address during their presentation to investors.

Recent Wall Street consensus sits closer to the middle, projecting earnings of $1.24 per share and $1.89 billion in revenue. There is a clear absence of late April whisper numbers, indicating that analysts are largely holding their positions steady ahead of the release. Full-year 2026 projections further illustrate this uncertainty, with guidance spanning from $1.69 to $2.72 per share.

These varying metrics provide the exact benchmarks required to evaluate Thursday’s print. Investors can use this data to immediately determine whether the actual results represent a fundamental beat, a routine meet, or a disappointing miss.

| Metric | Q4 2025 Actuals | Q1 2026 Guidance | Q1 2026 Consensus |

|---|---|---|---|

| Earnings Per Share | -$0.60 | $1.03 to $1.50 | $1.24 |

| Total Revenue | Not Disclosed | Not Disclosed | $1.89 Billion |

The professional employer organisation business model is uniquely vulnerable to specific macroeconomic pressures. When companies outsource their human resources functions, the provider assumes significant financial exposure to healthcare costs and client workforce fluctuations. A perfect storm of these factors emerged during the final months of 2025.

These company-level headwinds are playing out against a broader backdrop of underpriced stock market risk, meaning any signs of unexpected customer attrition could trigger outsized reactions in today’s high-valuation environment.

According to some reports, the company reported a fourth-quarter deficit of $0.60 per share, falling short of market projections by 27.66%. According to some reports, the historical 12-month gross profit rate compressed to 13.21% during this period. Management must now demonstrate they have overcome these baseline challenges in the current quarter.

Three distinct margin pressures continue to test the operational resilience of outsourced providers:

Benefit costs: Unexpected spikes in medical claims directly erode profitability when pricing contracts are locked. Customer attrition: Client business closures or headcount reductions immediately lower processing volumes and service fees. * Regulatory burdens: Increasing compliance requirements force providers to allocate more capital toward administrative overhead rather than growth initiatives.

Executive leadership has initiated direct strategic responses to recent operational difficulties. The launch of the Workday-partnered human capital management solution, HRScale, arrived in February 2026. This partnership aims to expand long-term capabilities but carries unavoidable short-term financial realities.

Analysts report that the integration is currently generating near-term expenses that are expected to subside later in 2026. The market is actively weighing these immediate costs against the projected future benefits of an upgraded software offering. Meanwhile, internal conviction appears remarkably strong based on recent executive trading activity.

According to some reports, Chief Executive Officer Paul Sarvadi acquired nearly 202,000 shares between March 17 and March 19, 2026. This massive insider buying serves as a strong signal of internal confidence in the broader turnaround strategy.

The SEC Form 4 filings confirm the specific transaction details, revealing the chief executive executed the multi-million dollar purchase at an average price of $23.21 per share.

Executive Conviction Signal According to some reports, Chief Executive Officer Paul Sarvadi committed approximately $4.6 million of personal capital to acquire company shares over a three-day period in March 2026.

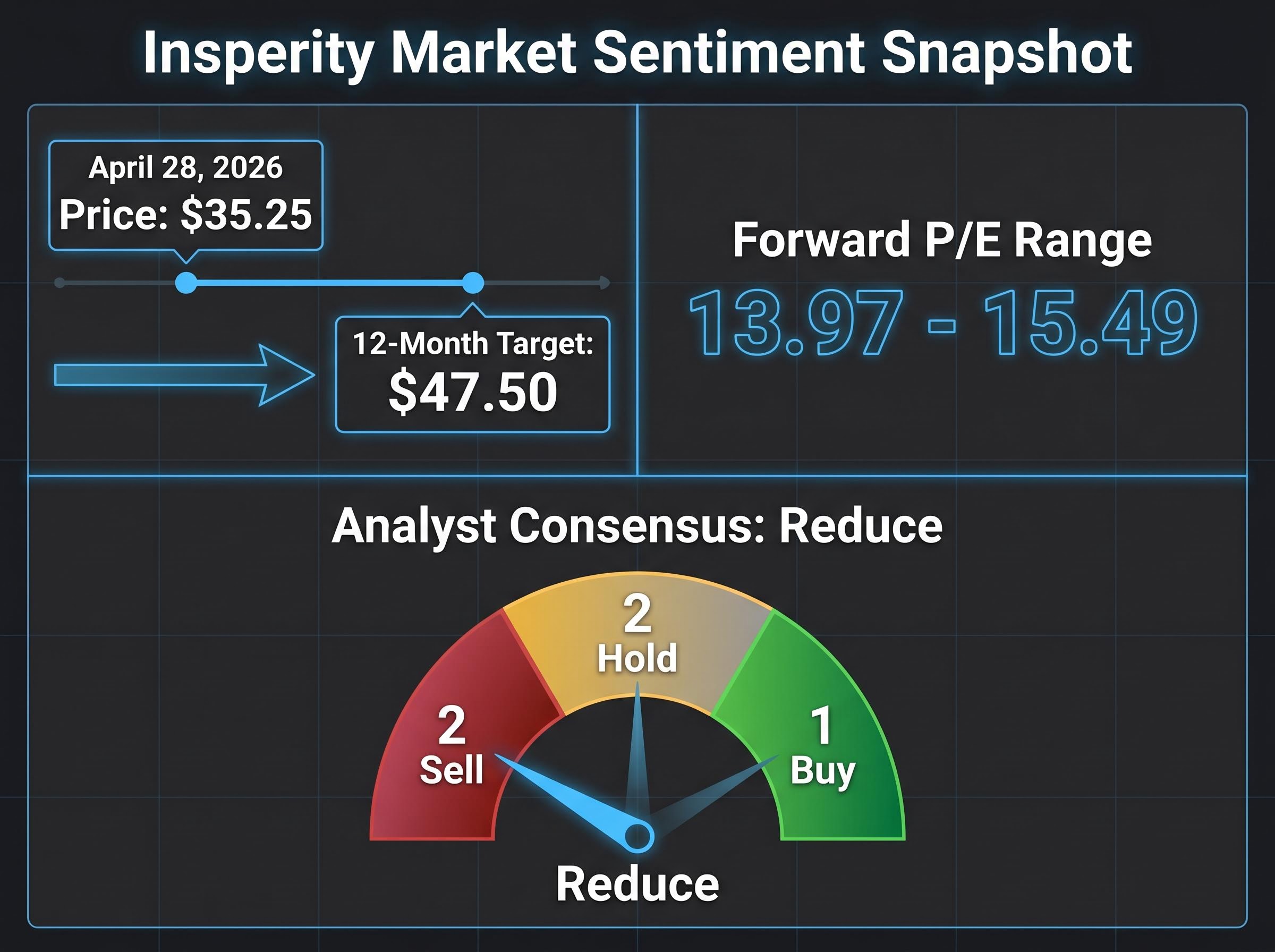

Wall Street maintains a stubborn wait-and-see attitude toward the stock despite recent recovery efforts. Shares closed at $35.25 on April 28, 2026. Current pricing multiples suggest the market is only pricing in a partial turnaround.

According to some reports, the forward price-to-earnings multiple sits between 13.97 and 15.49, depending on which profit projections are applied. Expert ratings reflect this prevailing caution, as analysts require concrete proof of execution before upgrading their outlooks.

The consensus rating currently sits at Reduce, comprising two sell recommendations, two hold positions, and a single buy rating. Average 12-month price targets stand at $47.50. These figures present a clear picture of market positioning, outlining a specific risk-versus-reward profile just hours before the numbers drop.

For investors looking to quantify this event risk, our comprehensive walkthrough of earnings season options pricing details how to use implied volatility metrics to evaluate the market’s true expectations ahead of the opening bell.

The challenges facing individual payroll providers are occurring alongside a wider industry shift toward automation. The ADP National Employment Report released on April 28, 2026, showed private employers added an average of 39,250 jobs per week. This moderate job creation occurs as overarching industry trends heavily favour artificial intelligence integration and digitised compliance tracking.

Competitor results confirm this structural evolution is rewarding specific operational models. Paychex reported 20% revenue growth in its third-quarter 2026 earnings on March 25, 2026, attributing success to AI-driven solutions. Conversely, broader industry-wide expansion remains constrained to low single-digit percentages.

Strategic consolidation is also shaping the labor services space; international acquisitions focusing on cross-border infrastructure recruitment have recently demonstrated how targeted scale can offset broader employment stagnation.

The upcoming Thursday release will serve as a barometer for mid-market employment health in the United States. Investors will use the data to separate company-specific execution issues from unavoidable macroeconomic headwinds.

Market participants should monitor specific operational metrics when the conference call begins at 8:30 a.m. Eastern Time. Progress on customer retention and the stabilisation of benefit expenses will likely matter more to analysts than a slight top-line revenue beat. These fundamental drivers dictate long-term margin health.

This quarter’s results will set the tone for the remainder of the 2026 fiscal year. The market requires evidence that the integration costs are peaking and operational discipline is returning.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Insperity faced elevated benefit expenses and unexpected customer attrition in Q4 2025, leading to a reported deficit of $0.60 per share and a compressed gross profit rate of 13.21%.

Insperity's official Q1 2026 guidance places earnings per share between $1.03 and $1.50, while Wall Street consensus sits at $1.24 per share.

CEO Paul Sarvadi acquired nearly 202,000 shares in March 2026, representing an investment of approximately $4.6 million and signaling strong internal conviction in the company's turnaround strategy.

Outsourced HR providers are vulnerable to fluctuating benefit costs, customer attrition due to client business changes, and increasing regulatory burdens that raise administrative overhead.

Wall Street analysts hold a cautious "Reduce" consensus rating for Insperity, with an average 12-month price target of $47.50, reflecting a wait-and-see approach.