From a peak above A$300 to A$95, Cochlear Limited has shed roughly two-thirds of its value since the start of 2025, a collapse measured in billions of dollars of market capitalisation for one of Australia’s most recognised medical device companies. The COH share price decline is not a single-event story. It reflects layered pressures: a guidance cut from A$435-460m in underlying net profit after tax (NPAT) down to A$290-330m, surgery volume softness in developed markets, a troubled product rollout, and a broader derating of high-PE ASX healthcare names. Against that backdrop, the price-to-sales ratio has fallen from a five-year average of 9.18x to 2.82x, a gulf that raises a legitimate question: is this a bargain, or a value trap?

This analysis walks through the actual earnings deterioration, what valuation metrics can and cannot tell investors at this price level, and how the analyst community is currently split on whether the structural growth case for Cochlear remains intact.

How Cochlear’s share price fell from premium darling to ASX laggard

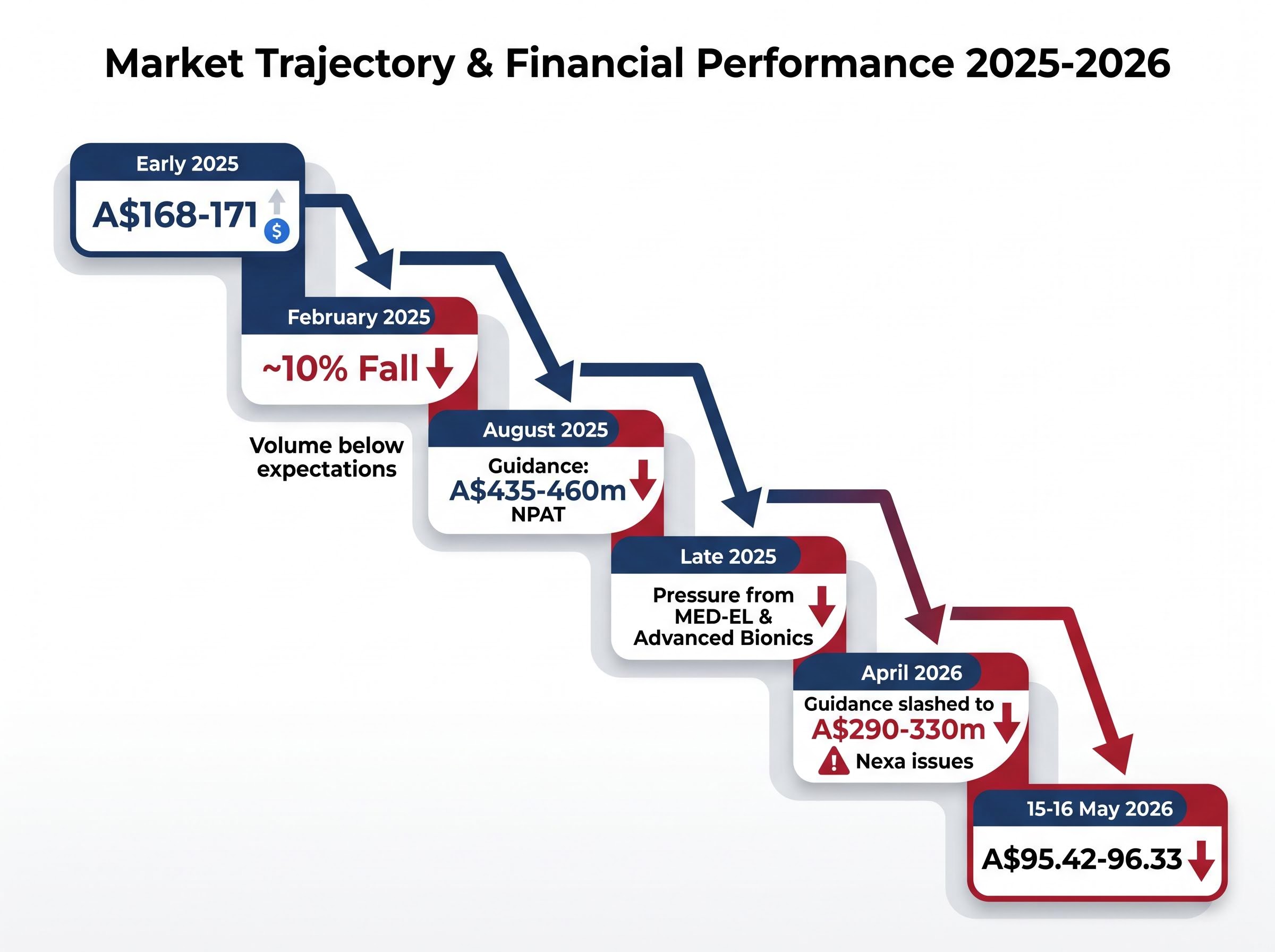

As recently as early 2025, Cochlear traded above A$168-171. By 15-16 May 2026, the stock sat at A$95.42-96.33, representing a market capitalisation of roughly A$6.3-6.5 billion. The 63% decline was not the product of a single shock. It was an accelerating feedback loop between earnings disappointment and multiple compression.

The sequence unfolded in stages:

- February 2025 (H1 FY25 result): Surgery volume growth in North America and Western Europe came in below expectations as post-COVID hospital backlogs normalised. The stock fell approximately 10% in a single session.

- August 2025 (FY25 full-year guidance): Management issued FY26 underlying NPAT guidance of A$435-460m, but commentary on FX headwinds, margin pressure from elevated R&D and marketing spend, and uneven emerging-market performance underwhelmed the market.

- Late 2025 (competitive and FX commentary): Broker notes flagged intensifying pricing pressure from rivals MED-EL and Advanced Bionics (Sonova), while a stronger Australian dollar weighed on reported earnings.

- April 2026 (guidance revision): FY26 NPAT guidance was slashed to A$290-330m, citing softer sales and issues with the Nexa platform rollout.

Guidance trajectory: Original FY26 NPAT guidance of A$435-460m (August 2025) was revised to A$290-330m (April 2026), a cut of more than 30% in nine months.

Each cut forced a fundamental earnings re-rating, not merely a sentiment shift. A stock that previously traded above 50x trailing earnings during peak years was repriced against a shrinking profit base.

When big ASX news breaks, our subscribers know first

What price-to-sales ratios reveal (and conceal) about a stock like Cochlear

A price-to-sales (P/S) ratio measures what the market is paying for each dollar of a company’s revenue. It strips away profitability decisions, debt structure, and cost management to isolate the market’s assessment of the top line. As a screening tool, it is useful. As a buy signal in isolation, it is unreliable.

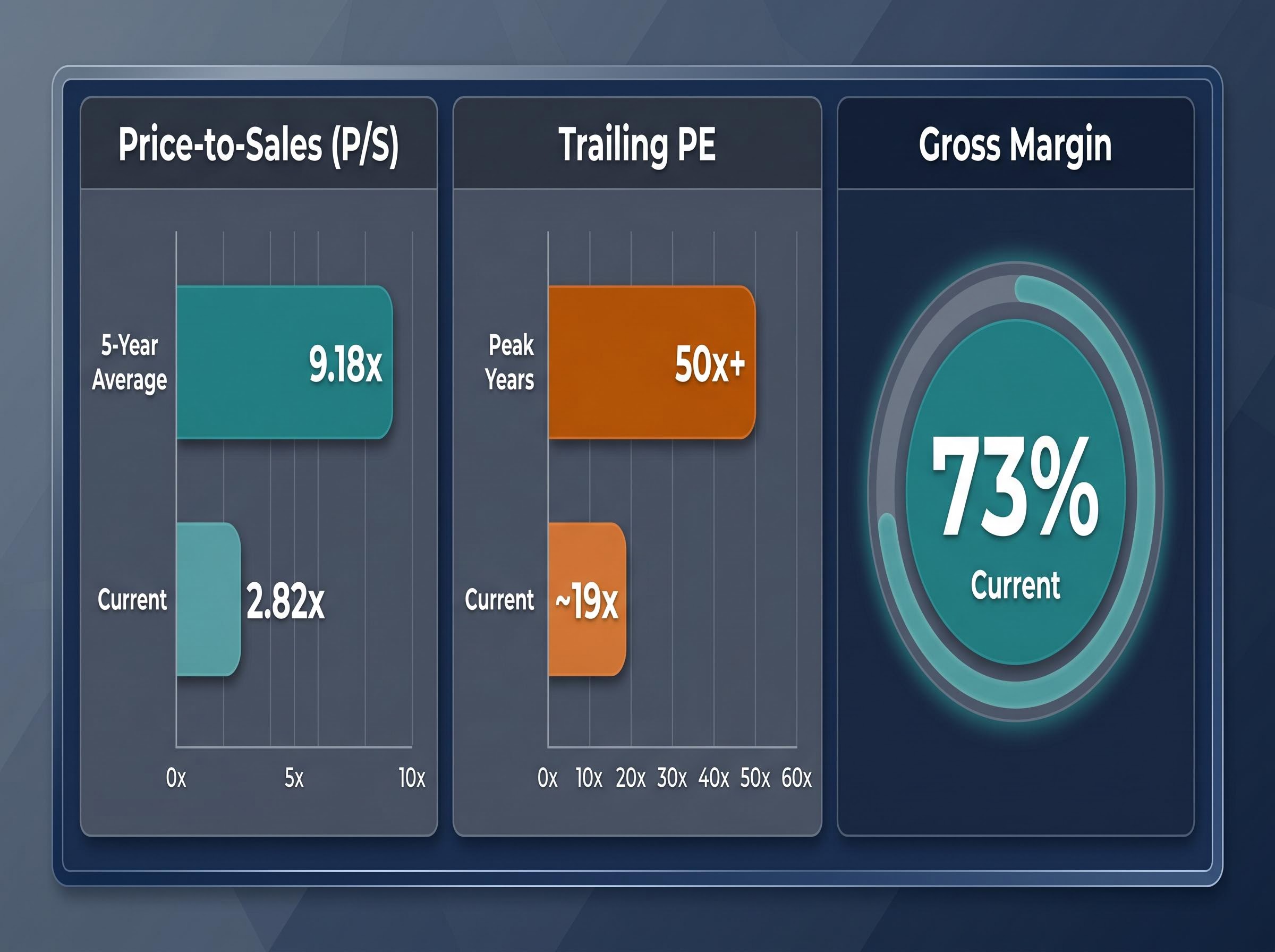

Cochlear’s current P/S of 2.82x sits far below its five-year average of 9.18x. That gap looks dramatic, but it reflects two forces operating simultaneously: the share price has collapsed, and revenue has continued to grow modestly. In H1 FY26, sales revenue reached A$1,176m (+1% reported, -2% in constant currency), while underlying NPAT fell 9% to A$195m.

The core limitation is that P/S ignores what happens below revenue. A compressed P/S on a company with declining earnings is fundamentally different from the same multiple on a business with stable or growing profits. Cochlear’s gross margin remains at 73%, so the profitability structure has not collapsed. But earnings are moving in the wrong direction.

| Metric | Current (May 2026) | Five-Year Average |

|---|---|---|

| Price-to-Sales | 2.82x | 9.18x |

| Trailing PE | ~19x | 50x+ (peak years) |

| Gross Margin | 73% | Not available |

Preferred valuation approaches for a company like Cochlear include Discounted Cash Flow (DCF) and Dividend Discount Models. P/S is a screening tool that identifies where to look more closely; it does not provide a conclusion on its own.

A multi-method valuation framework that sequences a P/S screen, an EV/EBITDA benchmark, a DCF, and a DDM cross-check is structurally better suited to a business like Cochlear than any single ratio, because each method exposes different risks: P/S ignores margin trajectory, DCF is sensitive to terminal growth assumptions, and EV/EBITDA anchors implied multiples to sector peers.

The business underneath the valuation: what Cochlear’s fundamentals actually show

Before assessing whether the discount is justified, the operating profile matters. Cochlear has distributed more than 750,000 devices globally, operates in over 50 countries, and employs more than 5,000 people. This is not a speculative or pre-revenue name. It is a scaled medical device franchise with decades of clinical evidence and global regulatory approvals.

H1 FY26 cochlear implant unit sales reached 27,016, up 6% on the prior comparable period. Clinical demand for the underlying product continues to grow even as financial metrics disappoint. The 73% gross margin confirms the pricing power embedded in the franchise has not been structurally impaired.

Three structural demand drivers underpin the long-term thesis:

- Ageing global demographics: The addressable population for hearing loss intervention expands as life expectancy rises across developed and emerging markets.

- Chronically underpenetrated hearing loss market: Only a fraction of eligible patients currently receive cochlear implants, suggesting decades of volume growth ahead if access and awareness improve.

- Broadening reimbursement access: US Medicare coverage expansion and ongoing government-backed screening programmes in Europe continue to lower barriers to adoption.

The WHO global hearing loss estimates project that more than 700 million people will have disabling hearing loss by 2050, with prevalence rising sharply above age 60, a demographic profile that directly underpins the long-run volume growth assumptions embedded in Cochlear’s bull case.

Why fund managers are still watching Cochlear closely

Airlie Funds Management initiated a small position in February 2026, arguing that the multiple had compressed to levels where long-term growth could justify it. Airlie characterised the near-term headwinds around hospital constraints and foreign exchange as cyclical rather than structural.

Wilson Asset Management named Cochlear as a high-quality franchise in its January 2026 monthly report but stated it was “watching for a better entry point or clearer evidence of accelerating volume growth.” Morgan Stanley maintained an Overweight rating, arguing the market was “over-penalising short-term volatility” in surgery volumes. These positions suggest that quality-oriented fund managers have not abandoned the stock, even as they remain cautious on timing.

The real risks: earnings trajectory, the Nexa stumble, and competitive heat

The bear case against Cochlear at A$95 is not abstract. It is documented in the company’s own guidance revisions and confirmed by broker downgrades.

- Nexa platform rollout execution: Issues with the Nexa platform were explicitly cited by management as a contributor to the April 2026 guidance cut. This is not a market-driven headwind; it is an internal operational failure that has directly reduced earnings expectations.

- Earnings guidance trajectory: The move from A$435-460m to A$290-330m in NPAT guidance over nine months represents more than 30% of expected earnings evaporating. H1 FY26 underlying NPAT of A$195m was already 9% below the prior comparable period, and revenue fell 2% in constant currency terms.

- Competitive pricing pressure: Both MED-EL and Advanced Bionics have launched updated processor platforms and are competing more aggressively on pricing in paediatric and bilateral segments. This limits Cochlear’s ability to push price increases and requires higher sales and marketing expenditure to defend market share.

- FX and hospital capacity constraints: Guidance assumptions embed AUD1 = USD0.66 and EUR0.61. Any movement in the Australian dollar above those levels compresses reported earnings further. Developed-market hospital capacity constraints, particularly in North America, add a demand-side ceiling that unit volume growth alone may not overcome.

Short interest and supply chain pressures add further texture to the valuation picture: professional short positions running at 4-5.7% of the register signal active institutional scepticism about a near-term recovery, while China rare earth export restrictions caused approximately 5-7% shipment delays in Q1 2026, a headwind not fully captured in the April guidance revision.

The earnings gap: FY26 NPAT guidance has been cut from A$435-460m to A$290-330m, a reduction of more than 30% since August 2025.

Where analysts stand: targets, ratings, and the divide between bulls and bears

A March 2026 consensus snapshot showed 3 Buy/Overweight ratings, 7 Hold/Neutral, and 3 Sell/Underweight. That snapshot pre-dates the April 2026 guidance cut and the subsequent decline to A$95-96, meaning current sentiment has likely shifted further negative.

The divide between bulls and bears is not about valuation arithmetic. It is about growth rate assumptions.

| Broker | Rating | 12-Month Target | Key View |

|---|---|---|---|

| Morgan Stanley | Overweight | A$210 | Structural growth intact; market over-penalising short-term volume volatility (FY26 NPAT forecast: A$360m) |

| UBS | Sell | A$165 | Insufficient growth to justify residual premium vs global med-tech peers (FY26 EPS: A$4.55) |

| Citi | Neutral | A$185 | Solid but not spectacular; FX headwinds and modest developed-market unit growth |

| Macquarie | Neutral | A$195 | Target cut from A$220; lower long-term volume assumptions; services revenue provides offset |

Important caveat: All published broker targets above (ranging from A$165 to A$210) pre-date the April 2026 guidance cut and should be treated with caution at current price levels. Consensus average at the March 2026 snapshot was approximately A$195, well above the current A$95-96 range.

Morgan Stanley’s Overweight thesis rests on a FY26 NPAT forecast of A$360m, which now sits above the top end of management’s revised A$290-330m guidance. UBS maintained a Sell throughout, arguing that even after the derating, Cochlear carried a premium unjustified by mid-single-digit volume growth. The gap between these two positions is whether Cochlear’s growth rate can re-accelerate, not whether the business is high quality.

Management forecasting credibility has become a central bear-case argument in its own right: repeated guidance downgrades over a compressed nine-month period have raised the probability that further earnings resets are possible before an investable floor is established, a risk that valuation multiples alone do not price.

At A$95, is Cochlear a bargain or a value trap for ASX investors?

The case for and against Cochlear at current levels can be distilled into two coherent positions, each requiring specific assumptions to hold.

Bull case assumptions:

- The guidance cut from A$435-460m to A$290-330m reflects cyclical headwinds (hospital capacity, Nexa execution, FX) rather than permanent structural impairment.

- A 2.82x P/S on a business with 73% gross margins, 750,000+ devices distributed, and structural demand tailwinds is a setup that typically only emerges when a quality franchise faces temporary disruption.

- Unit volume growth of 6% in H1 FY26 suggests underlying clinical demand remains intact.

Bear case assumptions:

- The earnings trajectory (NPAT guidance cut by more than 30% in nine months) may signal issues deeper than one product cycle, including competitive share loss and margin erosion.

- A trailing PE of approximately 19x on falling earnings is not conventionally cheap, particularly if FY26 NPAT lands at the lower end of the A$290-330m range.

- The five-year average P/S of 9.18x was established during a period of abnormally loose monetary conditions and higher earnings growth; reversion to that average may not be appropriate.

The ASX Healthcare Index (XHJ) has delivered a five-year annualised return of -11.49%, compared to the ASX 200 at +4.08%. Cochlear’s decline sits within a broader sector-level reset, not solely a company-specific problem.

The ASX Healthcare Index underperformance over the past five years, a roughly negative 3.9% to 4.4% annualised return against the broader ASX 200’s positive 4.21%, reflects the unwinding of COVID-era valuation distortions rather than a collapse in underlying earnings quality across the sector’s global earners.

What to watch before making a decision

- FY26 full-year result: Whether NPAT lands within or below the revised A$290-330m guidance range will signal whether the earnings floor has been found.

- Updated broker targets: Major Australian brokerages have not yet published revised targets reflecting the April 2026 guidance cut and the move to A$95-96.

- Nexa platform resolution: Upcoming product and sales commentary should clarify whether the rollout issues that contributed to the guidance cut are being addressed.

- Developed-market unit volume trajectory: H2 FY26 unit volumes in North America and Western Europe will indicate whether the 6% H1 growth can accelerate or whether hospital capacity constraints persist.

The structural story is intact but the margin of safety depends on what you believe about earnings

Cochlear’s core franchise, global scale, 73% gross margins, and structural demand from ageing populations and an underpenetrated hearing loss market, remains one of the stronger on the ASX. The question is not whether this is a quality business. It is whether the price paid for that quality adequately accounts for an earnings trajectory that has deteriorated faster than the market expected.

The P/S compression from 9.18x to 2.82x has partly been driven by rising revenue, not only by a falling share price. And the five-year average was set during a period of abnormally loose monetary conditions that inflated multiples across the ASX growth-health sector. Reversion to that average is not a base case.

Platinum Asset Management characterised Cochlear as having moved “from overvalued to closer to fair value” after its 2025-26 pullback, but noted a preference for a larger discount to intrinsic value before significantly increasing exposure.

P/S is a starting point. More rigorous tools, including DCF and Dividend Discount Models, are needed before any investment decision at these levels. Data gaps remain: post-April 2026 broker updates, dividend yield trajectory, and whether current FX spot rates differ materially from the USD0.66 and EUR0.61 assumptions embedded in guidance all require resolution.

The discount is real. The quality is real. But the earnings trajectory and execution risk mean this is a research starting point, not a conclusion.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.