June US Inflation Report Hits as Fed Sits 9-9 on Rate Hikes

1 hr ago

Cochlear Ltd has lost roughly 62.7% of its share price value since the start of 2025, wiping billions from the market capitalisation of a company that, twelve months ago, was widely regarded as one of the ASX’s most reliable healthcare compounders. The collapse is not the result of a single bad quarter. It reflects a 35-37% FY26 profit guidance downgrade, a one-day share price fall of 32-39%, weakening surgical volumes across Europe, Middle East disruption, and a currency headwind of approximately A$25 million to A$30 million after tax in the second half of FY26 alone. Together, these have forced investors and analysts to confront a question they rarely needed to ask about Cochlear: is this a temporary disruption in a structurally sound business, or a permanent downgrade of the company’s earnings power? What follows is a detailed assessment of the financial data, the broker landscape, the valuation arithmetic, and the competing investment arguments, designed to give ASX investors a clear framework for making that judgement.

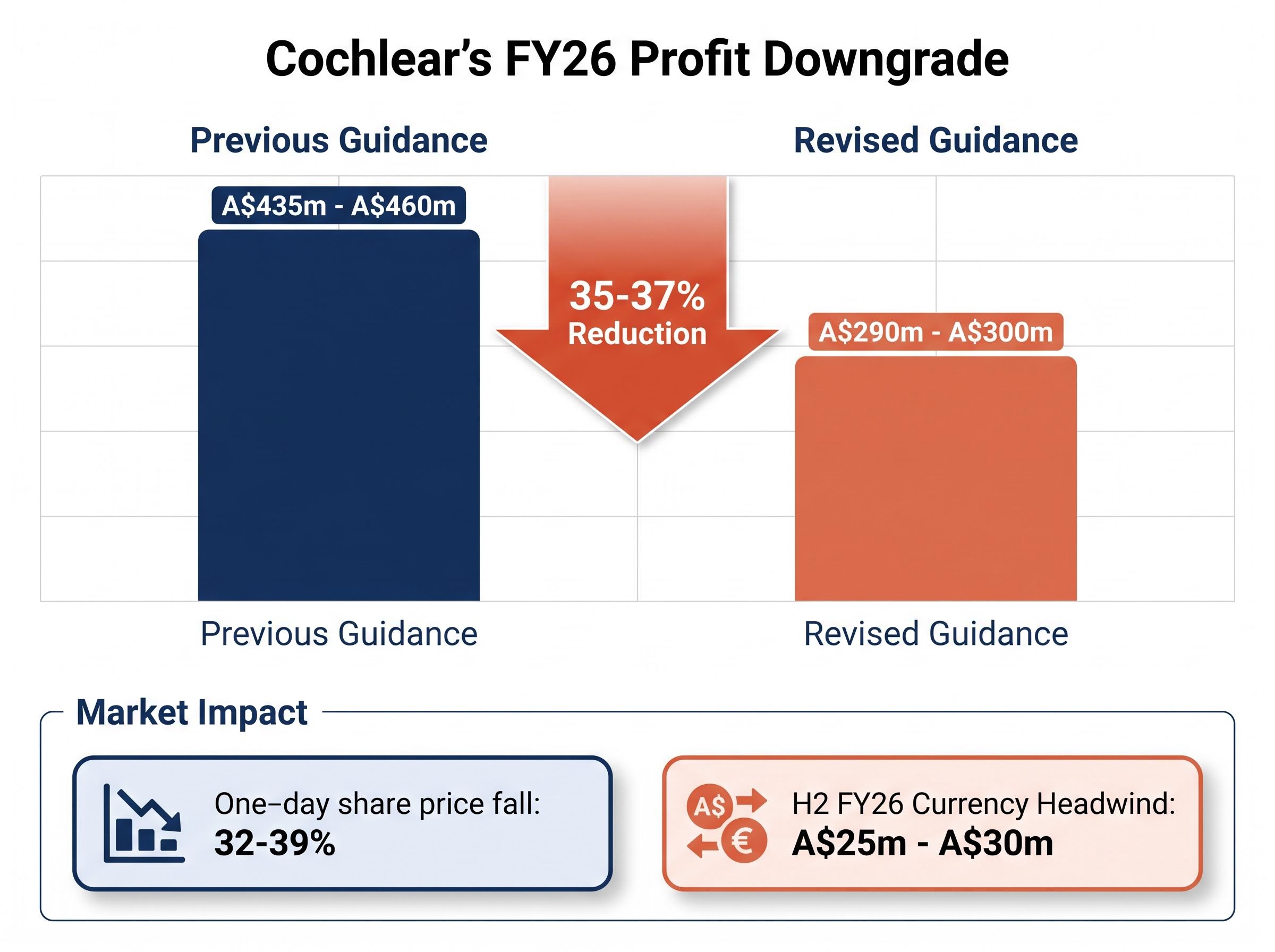

The detonator was the FY26 profit guidance revision. Cochlear cut its underlying net profit after tax (NPAT) forecast from A$435 million to A$460 million down to A$290 million to A$300 million, an implied reduction of approximately 35-37%. For a company that built its valuation premium on earnings predictability, the magnitude of the cut was severe enough to trigger an immediate re-rating.

FY26 guidance downgrade: NPAT revised from A$435m-A$460m to A$290m-A$300m, representing an approximate 35-37% reduction.

The share price fell 32-39% in a single session, depending on the intraday reference point. That one-day reaction reflected more than the earnings miss itself; it reflected the damage to management’s forecasting credibility after repeated downgrades over a compressed period.

The selloff dynamics on 22 April compounded the earnings cut itself: simultaneous multiple compression, forced institutional selling triggered by index rebalancing, and a credibility collapse after management failed to flag the March deterioration until April together produced a share price reaction that materially exceeded what the guidance revision alone would have implied.

Behind the headline cut, several secondary drivers converged:

Not every revenue line deteriorated. Services revenue grew 13% in Q3 on a constant currency basis, a counterpoint that matters for the longer-term thesis. But the weight of the negative factors overwhelmed that signal, and the market priced accordingly.

Three metrics matter most when assessing a global medical device compounder: the revenue growth rate, the earnings growth trajectory, and return on equity (ROE), which measures how effectively a company generates profit from shareholder capital. Cochlear’s FY24 results provide the pre-crisis benchmark.

| Metric | FY2021 | FY24 |

|---|---|---|

| Revenue | — | A$2,236 million |

| Net Profit | A$324 million | A$357 million |

| Return on Equity | — | 19.9% |

Revenue grew at approximately 14.3% per year from 2021 to FY24, a strong rate for a mature medtech business. ROE of 19.9% clears the 15% threshold generally considered healthy for growth-oriented companies, though it is not exceptional for a stock that commanded a premium multiple. The more revealing detail sits in the gap between topline and bottom-line growth.

Net profit moved from A$324 million to A$357 million over the same period, a comparatively modest compound increase against 14.3% annual revenue growth. That divergence signals rising cost intensity, reinvestment, or both.

This is a relevant caution when projecting what a normalised earnings recovery might look like. Even in the pre-crisis period, strong revenue growth did not automatically produce proportional profit expansion. Investors modelling a recovery scenario need to account for the possibility that a return to prior revenue levels would not, on its own, restore the profit margins the market previously assumed.

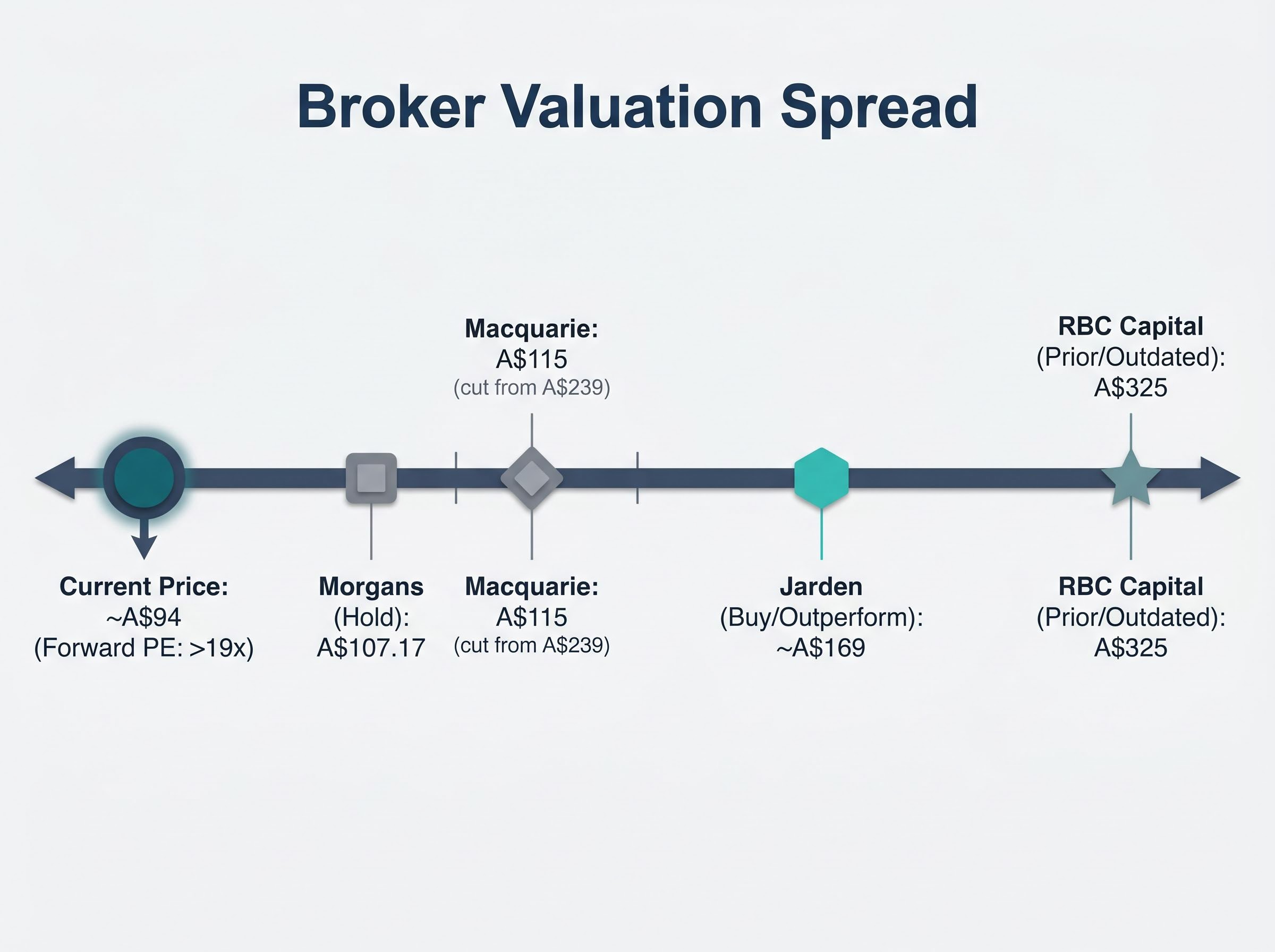

At approximately A$94, Cochlear trades at just over 19x FY26 earnings, using the midpoint of the revised guidance range.

At approximately A$94, the implied FY26 price-to-earnings ratio sits just over 19x, the lowest level in Cochlear’s recent history.

That number is simultaneously more attractive than at any point in the company’s recent past and not straightforwardly cheap. The compression reflects both a lower share price and lower earnings, not just a price-driven re-rating. Enterprise value to earnings before interest and tax (EV/EBIT) multiples have also compressed, but because the earnings denominator is falling at the same time, the de-rating is less dramatic than the raw share price decline implies.

The broker landscape captures the disagreement over what this valuation means:

| Broker | Rating | Price Target |

|---|---|---|

| Jarden | Buy / Outperform | ~A$169 |

| Macquarie | — | A$115 (cut from A$239) |

| Morgans | Hold | A$107.17 |

| RBC Capital | Outperform (prior) | A$325 (effectively outdated post-downgrade) |

The gap between Macquarie’s A$115 and Jarden’s approximately A$169 is not a rounding error. It represents a fundamentally different view of whether Cochlear’s earnings power has been temporarily impaired or permanently downgraded, and investors need to understand which scenario they are underwriting before taking a position.

The constructive argument rests on three structural pillars that the FY26 downgrade has not dismantled:

The gross margin and debt profile of the underlying business have not deteriorated alongside the share price, with gross margins remaining above 72% and a debt-to-equity ratio of approximately 13.2% as of the most recent reporting period, a distinction that matters when separating a de-rated quality compounder from a business with genuine structural impairment.

Research on global cochlear implant adoption rates underscores how large the unmet need actually is, with estimates suggesting fewer than 10% of people with severe to profound hearing loss have received an implant globally, meaning the structural demand runway extends well beyond what current surgical volume figures imply.

At just over 19x forward earnings, the stock is trading well below its own historical premium. Jarden’s target of approximately A$169 remains the most constructive credible broker position, implying substantial upside if operating conditions normalise.

While implant sales are under pressure, the services segment (sound processor upgrades, accessories, connectivity software) is growing and provides a recurring revenue base that pure implant volume numbers obscure. A revenue mix shift toward services changes the risk profile of the business over time, even if it reduces the headline growth rate that once justified the premium valuation.

The swing factor is cost restructuring. If management can build a lower cost-to-serve base during the current volume downturn, the earnings recovery from normalised volumes could prove more powerful than current consensus implies. That remains an “if,” not a certainty.

Repeated guidance downgrades over a short period represent the most uncomfortable data point in the bear argument. The pattern raises a pointed question: does management lack adequate visibility into its own business, or are underlying conditions changing faster than the company’s forecasting model can track? Either answer is a problem for investors who depended on earnings predictability.

Guidance cut magnitude: FY26 NPAT revised from A$435m-A$460m to A$290m-A$300m, a reduction of approximately 35-37%.

The structural re-rating risk demands direct acknowledgment. If the market permanently reprices Cochlear from a quality compounder multiple to an ordinary medtech multiple, the appropriate price-to-earnings ratio may be materially lower than 19x even on recovered earnings. The four core bear case risk factors are:

FDA regulatory uncertainty has added a persistent risk premium to the device-maker category that sits above and beyond the currency and rate-cycle headwinds most commentary focuses on, with policy instability under the current administration raising the discount rate investors apply to pre-approval pipeline assets and compressing valuations across the medical device sector regardless of individual company fundamentals.

Macquarie’s post-downgrade target of A$115 anchors the cautious institutional view. Morgans’ Hold at A$107.17 corroborates limited near-term upside at current levels.

The investment question at today’s price comes down to three variables the individual investor controls:

Short interest in COH has tracked between 4% and 5.7% of shares on issue through mid-2026, a range that signals active professional scepticism about a near-term recovery without reaching the elevated levels typically associated with crowded short positions or a genuine short squeeze setup.

Investors watching for signs of stabilisation should look for three things: confirmation that the A$290 million to A$300 million guidance range is not cut again; any commentary on FY27 volume recovery expectations in Europe and the Middle East; and management’s update on cost restructuring progress. A clean result in line with the downgraded guidance, with no further reduction and any forward commentary suggesting stabilisation, would likely be the minimum required to shift sentiment from cautious to constructive.

The 62.7% decline does not mean Cochlear has become a poor business. It means the market has repriced a quality business that has lost earnings predictability. The long-term structural case (demographics, market leadership, services growth) remains intact, but the near-term earnings case is materially weaker than the market believed twelve months ago.

The stock may ultimately prove to be a buying opportunity. The evidence does not yet clearly support that conclusion. ASX investors considering a position should be explicit about the assumptions they are making, particularly around earnings recovery timing, the persistence of European volume constraints, and the risk of further guidance revisions, before acting.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Cochlear's share price has fallen approximately 62.7% since the start of 2025, driven by a 35-37% FY26 profit guidance downgrade, weak surgical volumes in Western Europe, Middle East disruption, and a currency headwind of approximately A$25 million to A$30 million after tax in the second half of FY26.

Cochlear revised its FY26 underlying NPAT guidance from A$435 million to A$460 million down to A$290 million to A$300 million, representing a reduction of approximately 35-37% and triggering a single-session share price fall of 32-39%.

Broker targets vary significantly: Jarden holds the most constructive view at approximately A$169, Macquarie cut its target to A$115 from A$239, and Morgans rates the stock Hold with a target of A$107.17, reflecting deep disagreement over whether the earnings impairment is temporary or permanent.

A recovery would likely require confirmation that the A$290 million to A$300 million FY26 guidance range is not cut again, evidence of normalising surgical volumes in Europe and the Middle East, and progress on management's cost restructuring efforts.

The long-term case rests on Cochlear's global market leadership with over 750,000 implantable devices distributed historically, demographic tailwinds from ageing populations, and a services segment that grew 13% in Q3 on a constant currency basis, with fewer than 10% of people with severe hearing loss globally having received an implant.