Why Seeing Machines Trades Below 5p Despite EU Mandate Wins

8 hrs ago

Commonwealth Bank of Australia shares closed at A$165.67 on 22 May 2026, carrying a trailing price-to-earnings ratio of 26.8x. That multiple sits nearly 59% above CBA’s own 10-year median PE of 16.88x. Every major broker that published a valuation target on the stock during 2024 and 2025 placed fair value at least 35% below where the shares trade today. Whether CBA’s price reflects genuine earnings power or a structural premium that could compress is now one of the most contested questions in Australian equities. What follows applies two valuation frameworks, the PE-based peer comparison and the Dividend Discount Model, to CBA’s own reported figures, showing what the current price is actually implying and where each method places fair value.

At A$165.67, CBA commands a trailing PE of 26.8x against reported FY25 cash earnings per share of A$6.12. The forward PE sits at approximately 24.44x, meaning even consensus estimates for the year ahead do little to close the gap with the bank’s historical norm.

The 52-week range of A$149.76 to A$192.00 places the current price in the lower half of its recent trading band, a reminder that the stock briefly touched higher ground before pulling back. Yet even after that retreat, the trailing multiple remains historically elevated.

CBA’s trailing PE of 26.8x sits nearly 59% above its own 10-year median of 16.88x.

That single number frames the question this analysis aims to answer: can either of the two most commonly used valuation frameworks close the distance between where CBA trades and where its earnings suggest it should?

The price-to-earnings ratio divides a company’s share price by its earnings per share. A higher PE means investors are paying more for each dollar of profit. At A$165.67 and FY25 cash EPS of A$6.12, CBA investors are paying roughly $27 for every dollar the bank earned last year.

Two versions of this ratio appear throughout the analysis. The trailing PE uses the most recent reported earnings. The forward PE uses consensus forecast earnings for the year ahead, which tends to produce a lower number if analysts expect profit growth. Both are useful; neither is definitive on its own.

For bank stocks specifically, peer-relative PE carries more weight than it does in sectors where business models vary widely. The four major Australian banks lend to broadly the same customer base, operate under the same regulatory framework, and report earnings on comparable accounting bases. When one bank trades at a large premium to the others, the market is making a specific judgment about the quality or growth trajectory of that franchise.

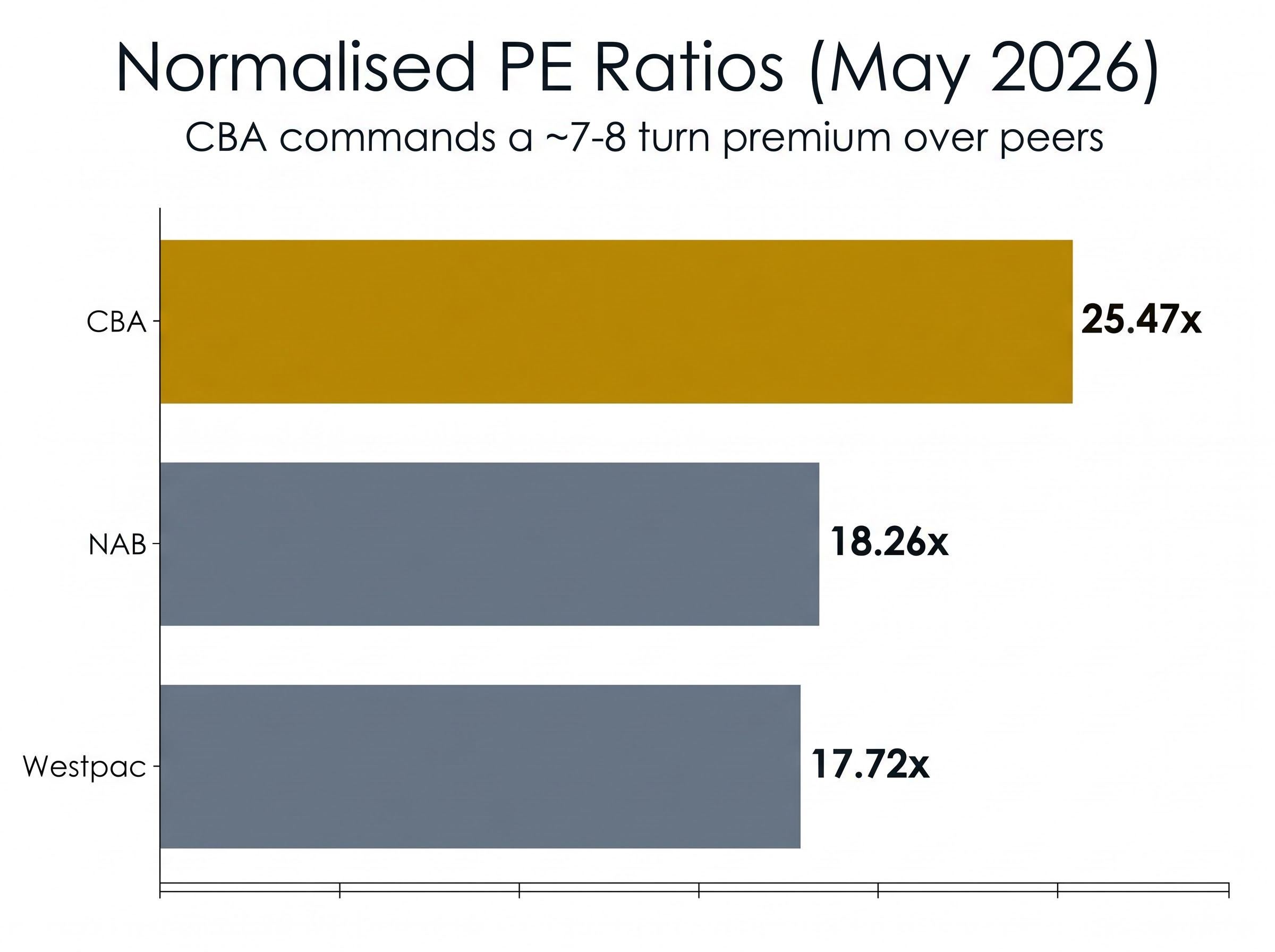

Morningstar’s normalised PE data from May 2026 quantifies the gap.

| Bank | Normalised PE (May 2026) | Premium to CBA |

|---|---|---|

| CBA | 25.47x | Baseline |

| Westpac | 17.72x | CBA trades at +7.75 turns |

| NAB | 18.26x | CBA trades at +7.21 turns |

Peer multiples have themselves drifted upward from the 12-13x forward range the Australian Financial Review cited in early 2025 to approximately 17-18x normalised by May 2026. Some of that shift reflects the difference between forward and normalised earnings bases rather than a wholesale re-rating. Regardless, CBA still commands a premium of roughly 7-8 turns over the peer average on a normalised basis, a spread that forms the starting point for the PE-based fair value estimate.

The calculation is two steps.

The results: A$6.12 x 18 = A$110.16 implied fair value on FY25 earnings. A$5.63 x 18 = A$101.34 on FY24 earnings. Some source material produces a slightly different figure of approximately A$102.67 using a marginally different sector average; the range of A$101-A$110 captures the realistic band.

PE valuation applied to NAB in FY24 produced a sector-adjusted fair value of approximately A$41.27 against a share price of A$37.37, illustrating how the same methodology that implies a 33% premium gap for CBA can point in the opposite direction for peers whose trailing multiples already sit closer to the 18x sector benchmark.

At a sector-average PE of 18x and FY25 EPS of $6.12, the implied fair value is approximately $110 per share, roughly 33% below the current price.

At A$165.67, the market is paying a premium of more than 50% over the FY25 PE-derived estimate. The model assumes CBA deserves no premium over its peers, which is a strong assumption, but it provides a clear baseline.

Broker targets from 2024 and 2025 clustered in the same territory. Morgan Stanley carried an Underweight rating with a 12-month target of approximately A$96 in March 2024. Macquarie rated the stock Underperform at approximately A$105-A$110 in August 2024. Both targets were issued when CBA was already trading above A$130, and the gap between their estimates and the share price has widened since.

The Dividend Discount Model (DDM) values a stock as the present value of all future dividends. In its simplest form, the formula divides the annual dividend by the difference between the required rate of return and the expected dividend growth rate. It is particularly suited to mature, high-payout businesses like Australian banks, where dividends represent the primary mechanism for returning capital to shareholders.

CBA declared a total FY25 dividend of A$4.85 per share, fully franked, with a payout ratio of approximately 79%. The FY26 interim dividend of A$2.35 (announced in February 2026) suggests the annualised trajectory remains stable.

Applying the DDM across a realistic range of assumptions produces a wide spread. The sensitivity table below illustrates how the implied share price shifts with different risk rate and growth rate combinations.

| Risk Rate | 2% Growth | 3% Growth | 4% Growth |

|---|---|---|---|

| 6% | $121.25 | $161.67 | $238.00 |

| 8% | $80.83 | $97.00 | $121.25 |

| 11% | $52.89 | $60.63 | $69.29 |

Using a blended mid-range set of assumptions, the DDM converges on an implied value of approximately A$98-A$100 on a cash dividend basis.

CBA’s dividends are fully franked, meaning they carry a 30% corporate tax credit that eligible Australian resident investors can use to offset personal tax liability. This effectively increases the after-tax value of each dividend dollar for qualifying holders.

The gross dividend calculation: A$4.85 cash dividend divided by (1 minus 0.30) equals approximately A$6.93 gross dividend. Applying the DDM to this grossed-up figure lifts the implied valuation to approximately A$143.80, materially higher than the cash dividend estimate but still below the current share price of A$165.67.

The franking credit calculation the article applies here, dividing the cash dividend by 0.70, follows the standard 30/70 formula; for eligible investors, this means a A$4.85 fully franked dividend carries an attached credit of approximately A$2.08, making the total economic value of each distribution A$6.93 before any personal tax offset is applied.

The gross dividend DDM is most relevant for Australian investors with taxable income who can fully utilise the franking credits. For institutional investors, superannuation funds with different tax positions, or non-resident shareholders, the cash dividend version provides the more applicable reference point.

Well-resourced analysts disagree on whether the premium is earned or excessive. That disagreement itself is informative.

The case for a structural premium:

Structural demand from passive funds, compulsory superannuation inflows, and SMSF familiarity bias creates persistent mechanical buying pressure on CBA that operates largely independently of any earnings-based valuation signal, which is one reason the premium documented in this analysis has remained durable through multiple periods of analyst-flagged overvaluation.

The case against paying this price:

CBA was described as “trading on about 20 times forward earnings versus 12-13 times for ANZ, NAB, and Westpac” in early 2024 AFR reporting. Since then, the price has risen from approximately A$130 to A$165, and the spread has widened further.

Citi offered perhaps the most measured view, rating the stock Neutral at approximately A$115 in October 2024 and describing it as “fairly valued to slightly overvalued,” acknowledging the quality franchise while noting that “upside appears limited unless we see a positive surprise on revenue growth or further capital management.”

The two valuation approaches produce different numbers but point in the same direction.

| Method | Key Input | Implied Fair Value | Gap to Current Price |

|---|---|---|---|

| PE peer comparison | 18x sector PE, FY25 EPS $6.12 | ~A$110 | ~33% below |

| DDM (cash dividend) | $4.85 dividend, blended assumptions | ~A$98-$100 | ~40% below |

| DDM (gross dividend) | $6.93 grossed-up dividend | ~A$144 | ~13% below |

None of the three estimates reaches A$165. The gross dividend DDM comes closest, and that version applies only to Australian tax-resident investors who can fully utilise franking credits.

At A$165.67 and a trailing PE of 26.8x, the market is pricing CBA for earnings growth and multiple expansion that the FY25 result, with its approximately 4% NPAT growth, does not yet reflect. The 79% payout ratio also constrains how quickly dividends can grow without either a material lift in earnings or an increase in the proportion of profits distributed.

The models provide a framework. They do not provide a buy or sell signal. Three steps can sharpen the picture further:

At A$165.67, both models agree: the market is pricing CBA as though the best-case scenario is the base case.

The premium could persist. Passive fund flows, CBA’s index weight, and the bank’s reputation as a defensive compounder may continue to support a multiple well above the sector average. That outcome is possible, but it is a bet on sentiment and structural demand rather than on the reported numbers. CBA delivered approximately 4% NPAT growth in FY25. The trailing PE of 26.8x implies far more than that. The gap between those two facts is where the investment decision lives.

For investors wanting to build their own valuation model from scratch using the same two methods applied here, our dedicated guide to PE and DDM convergence for ASX banks walks through the step-by-step calculations with a CBA worked example, explains why convergence between the two methods carries more analytical weight than any single model output, and provides a downloadable sensitivity table framework.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The Dividend Discount Model values a stock as the present value of all future dividends by dividing the annual dividend by the difference between the required return and expected growth rate. Applied to CBA's FY25 cash dividend of A$4.85, the model produces an implied fair value of approximately A$98-A$100 under blended mid-range assumptions.

As of May 2026, CBA trades at a normalised PE of approximately 25.47x, compared to Westpac at 17.72x and NAB at 18.26x, meaning CBA commands a premium of roughly 7-8 PE turns above the peer average on a normalised basis.

Because CBA's dividends are fully franked, eligible Australian tax-resident investors can gross up the A$4.85 cash dividend to approximately A$6.93, and applying the DDM to this higher figure lifts the implied valuation to around A$143.80, still below the current share price of A$165.67.

Broker targets from 2024 and 2025 clustered well below the current price: Morgan Stanley set a target of approximately A$96, Macquarie approximately A$105-A$110, UBS approximately A$110, Citi approximately A$115, and Morningstar placed fair value at approximately A$92 in August 2024.

CBA's premium is often attributed to its above-sector return on equity of 13.5%, heavy weighting in the ASX 200 driving structural demand from passive index funds, lower perceived earnings volatility, and persistent buying from self-managed super funds and superannuation inflows.