How to Build a Global ETF Portfolio on the ASX With 3 Funds

4 hrs ago

A $1,000 fully franked dividend from a major ASX company is not actually worth $1,000 to every investor. For a self-managed super fund in pension phase, or a low-income retiree who qualifies for a full refund, that same dividend is worth $1,428.57 once the franking credit is claimed. Most Australian investors never capture the difference, either because they do not understand how the credit works or because they fail to report it correctly. Franking credits remain one of the most distinctive features of the Australian tax system, designed to prevent company profits from being taxed twice. In the 2025-2026 financial year, the system carries added relevance: the ATO introduced automatic refunds for eligible investors over 60 from 2025, and new integrity guidance (PCG 2025/3) affects how credits are claimed in certain equity-raising scenarios. What follows is a practical, step-by-step breakdown of how the franking credit system works mechanically, how to calculate entitlements on any dividend statement, what different franking levels mean in practice, and how the system plays out differently depending on an investor’s tax situation.

Before 1987, Australian shareholders faced a straightforward inequity. A company earned profits, paid corporate tax on those profits, then distributed what remained as dividends. The shareholder then paid personal income tax on the same earnings. The same dollar of profit was taxed twice: once in the company’s hands and again in the investor’s hands.

The consequences were tangible:

The 1987 introduction of dividend imputation was a structural reform to how dividend income was treated under Australian tax law. It recognised that corporate tax and personal income tax on the same profit stream were, in effect, the same obligation being charged twice.

The 1987 system had a limitation. Franking credits could reduce a shareholder’s tax bill to zero, but if the credit exceeded the tax owed, the excess was simply lost. An SMSF in pension phase paying 0% tax, or a low-income individual below the tax-free threshold, received no benefit at all.

That changed on 1 July 2000. Legislation introduced by the Howard government made franking credits fully refundable. From the 2000-01 financial year onward, investors whose credits exceeded their tax liability received the difference as a cash payment from the ATO. The credit ceased to be merely an offset. It became a direct financial entitlement.

The Australian corporate tax rate sits at 30% for large companies and 25% for eligible small businesses. When a company pays that tax before distributing profits, the credit represents tax already paid on the investor’s behalf, before the dividend ever reaches their account.

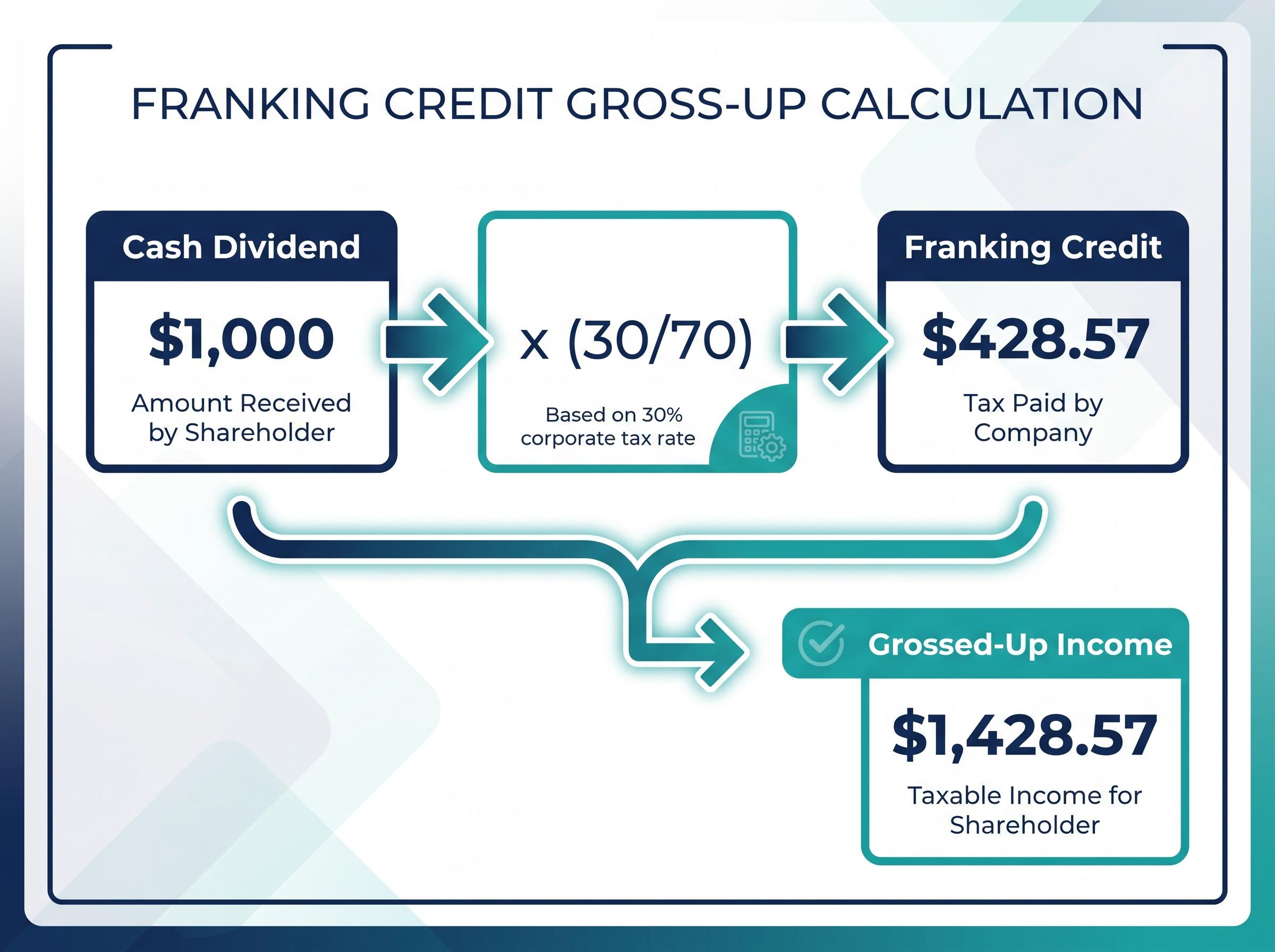

The ATO treats a franked dividend as if the investor received both the cash payment and the corporate tax already paid on their behalf. Both components are included in assessable income. This is the “grossed-up” dividend concept, and it forms the basis of every franking credit calculation.

The arithmetic follows directly from the 30% corporate tax rate. If a company pays 30% tax on its profits before distributing the remaining 70% as a dividend, the credit that attaches to any cash dividend is the tax already paid on the original 100%.

Franking credit = (Cash dividend x 30) / 70

Applying this to any dividend statement involves three steps:

Two real ASX examples from the 2024-2025 period illustrate how this works in practice.

| Company | Cash Dividend Per Share | Franking Credit Per Share | Grossed-Up Income Per Share | Corporate Tax Rate |

|---|---|---|---|---|

| CBA (interim, Dec 2024) | $2.35 | $1.007 | $3.357 | 30% |

| BHP (final, Jun 2025) | US$0.60 (fully franked) | US$0.257 | US$0.857 | 30% |

For a round number: a $1,000 fully franked cash dividend generates a franking credit of $1,000 x (30/70) = $428.57. The grossed-up income reported to the ATO is $1,428.57. If the investor’s total tax liability on that income is zero, the full $428.57 is refundable as cash.

The ability to perform this calculation from any dividend statement is the foundational skill for assessing the true after-tax value of Australian dividend income.

Constructing a well-structured ASX dividend income portfolio requires more than selecting high-yielding stocks; payout ratio sustainability, ex-dividend date timing, and the compounding mechanics of dividend reinvestment plans all determine whether a portfolio delivers reliable income or exposes investors to dividend traps that erode capital over time.

A fully franked dividend carries the maximum credit. 100% of the dividend has Australian corporate tax attached, meaning the full 30/70 formula applies to the entire cash amount. For an Australian resident investor, this is the most tax-efficient form of dividend income.

Partially franked dividends carry credits on only a portion of the payment. The franked portion generates a credit calculated at 30/70; the unfranked portion carries none. This structure typically arises when a company earns part of its profits offshore (where Australian corporate tax was not paid), when its franking account balance is insufficient to fully frank the distribution, or when a company operating under the 25% small business rate distributes dividends exceeding its franked profits.

ANZ’s May 2026 interim payment is a live example of a partially franked dividend in practice: at 75% franking, the grossed-up value per share is calculated only on the franked portion, producing a different credit amount than if the full 83 cents were franked at 100%, and investors comparing it against fully franked alternatives need to account for that gap in their after-tax yield assessment.

An unfranked dividend carries zero tax credit. The investor pays full personal income tax on the cash received, with no offset for corporate tax already paid.

| Dividend Type | Tax Credit Available | Who Benefits Most | Example Scenario |

|---|---|---|---|

| Fully franked | Full 30/70 credit on entire dividend | All Australian residents; greatest value for low-tax investors | CBA interim dividend: $2.35 + $1.007 credit |

| Partially franked | Credit on franked portion only | Australian residents, though benefit is proportionally reduced | Company with 60% Australian earnings franks only 60% of dividend |

| Unfranked | None | No franking benefit; same tax treatment as interest income | Offshore-sourced distribution with no Australian tax paid |

The practical implication is material when comparing ASX dividend stocks side by side.

A fully franked 3.5% yield may deliver better after-tax returns than an unfranked 4% yield for Australian resident investors, depending on their marginal tax rate.

Non-resident shareholders are generally not entitled to claim franking credits, which means the franking label is primarily relevant to Australian residents assessing after-tax income.

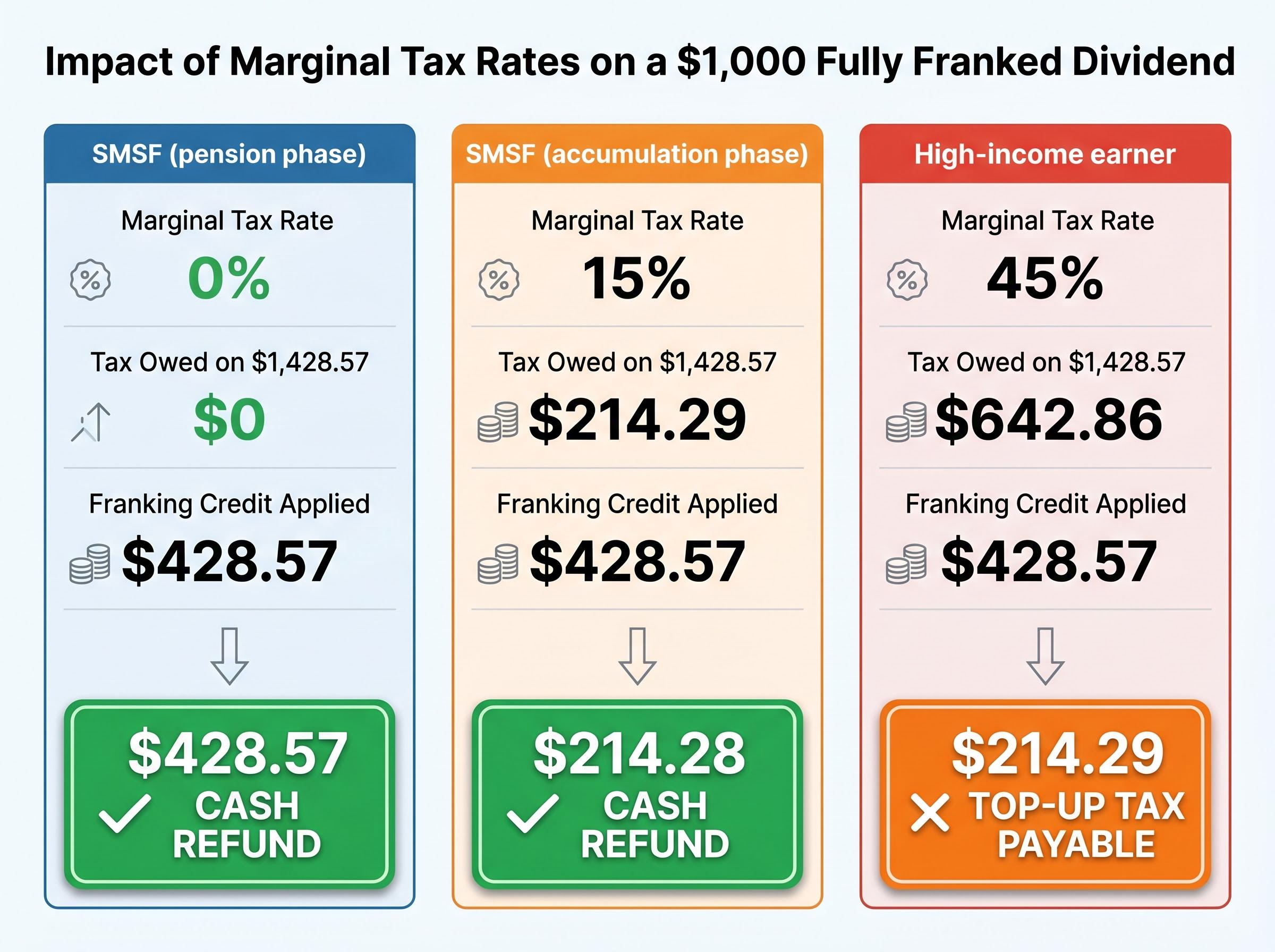

The value of a franking credit is not fixed. It depends entirely on the gap between the 30% corporate tax rate already paid and the investor’s personal marginal tax rate. Three investor profiles illustrate how the same $1,000 fully franked dividend produces three very different outcomes.

| Investor Type | Marginal Tax Rate | Tax Owed on $1,428.57 | Franking Credit Applied | Net Outcome |

|---|---|---|---|---|

| SMSF (pension phase) | 0% | $0 | $428.57 | $428.57 cash refund |

| SMSF (accumulation phase) | 15% | $214.29 | $428.57 | $214.28 cash refund |

| High-income earner | 45% | $642.86 | $428.57 | $214.29 top-up tax payable |

An SMSF in pension phase pays 0% tax. The entire $428.57 credit is refunded as cash, making the effective dividend worth $1,428.57. This is the highest-value scenario in the imputation system and a cornerstone of retirement income planning for many Australian self-managed funds.

CBA’s franking credit returns illustrate this dynamic in concrete terms: pension-phase superannuation investors in CBA received the full 30% franking credit as a cash refund from the ATO across four consecutive fully franked dividend payments, lifting the effective after-tax yield to approximately 1.4 times the face value of each dividend, a gap that is invisible when reading the headline yield figure alone.

At the 15% accumulation phase rate, the tax owed on the grossed-up income is $214.29. The $428.57 credit more than covers this, leaving a $214.28 refund.

A high-income earner at the 45% marginal rate owes $642.86 on the grossed-up income. The $428.57 credit reduces this to a $214.29 top-up payment. The credit does not eliminate the tax bill entirely, but the investor is still materially better off than if the dividend had been unfranked, where the full $642.86 would apply to the $1,428.57 with no offset.

From 2025, the ATO introduced automatic franking credit refunds for eligible individuals. The eligibility criteria are:

No application is required for this cohort. Previously, eligible individuals needed to submit form NAT 4105 manually. The automatic process removes that administrative step for qualifying retirees.

The ATO franking credit refund eligibility criteria specify the residency, age, and compliance conditions that determine whether an investor receives a cash refund rather than a simple tax offset, with pension-phase SMSFs and low-income retirees standing to benefit most from meeting those conditions.

The most common compliance trap for retail investors is the 45-day holding period rule. To claim a franking credit, shares must be held “at risk” for at least 45 days around the ex-dividend date. Selling too early, even by a single day, can void the credit entitlement entirely.

A small shareholder exemption applies. If an investor’s total franking credits for the entire financial year are under $5,000, the holding period rule does not apply. The threshold is assessed across all franking credits received in the year, not on a per-parcel or per-dividend basis.

Four compliance steps apply to all investor types:

For investors who do not qualify for the automatic refund process, form NAT 4105 remains available for manual applications.

From 2025, the ATO introduced Practical Compliance Guideline PCG 2025/3, a formal risk assessment framework targeting situations where a company raises equity (issues new shares) and uses the proceeds to fund a franked distribution. The guideline does not alter the general entitlement for investors holding ordinary shares for income purposes.

PCG 2025/3 is primarily relevant for sophisticated investors, wholesale funds, and SMSF trustees involved in capital raisings or complex distribution structures. Investors participating in such transactions should consider seeking specific tax advice regarding their entitlement under the new framework.

Understanding how franking credits work is one step. Acting on that understanding each financial year is what converts knowledge into actual tax savings or cash refunds. The following annual checklist provides a repeatable process:

The ATO’s myTax system expects dividend amounts and franking credits to be reported exactly as they appear on the company’s dividend statement. Discrepancies between reported figures and statement amounts are a common trigger for processing delays.

One detail frequently overlooked: when dividends are reinvested through a dividend reinvestment plan (DRP) rather than received as cash, the franking credit still attaches to the grossed-up dividend. The reinvested amount must still be declared as income in the investor’s tax return. The credit is not forfeited simply because no cash was received.

The 2025-2026 financial year follows the same fundamental imputation framework established in 2000. No proposed changes to the refundability of franking credits were reported as of mid-2025. The recent ATO updates, including automatic refunds for over-60s and the PCG 2025/3 integrity guideline, refine administration and compliance rather than alter the underlying entitlement.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The core mechanism is straightforward: a franking credit transforms a cash dividend into a grossed-up entitlement worth materially more than the face amount, with the greatest benefit flowing to low-tax investors and SMSFs in pension phase. The framework has been structurally unchanged since 2000, and the 2025 updates reinforce administration rather than alter the underlying system.

Australian investors who want to maximise after-tax returns from ASX dividend income should calculate the grossed-up yield on fully franked stocks as standard practice, not as an afterthought. The formula introduced in this guide applies to every dividend statement received from every ASX-listed company paying franked distributions.

For further reading, consider exploring SMSF dividend strategies, how to interpret ASX dividend announcements, and how to compare dividend yields on a grossed-up, after-tax basis across different franking levels.

For investors wanting to take the grossed-up yield analysis further into formal stock valuation, our dedicated guide to applying the dividend discount model to ASX stocks covers how franking credits alter the effective yield inputs required by the Gordon Growth Model, with sector-by-sector application across Australian banks, listed infrastructure, and consumer staples.

Franking credits are tax offsets attached to dividends paid by Australian companies that have already paid 30% corporate tax on their profits. When you receive a franked dividend, you include both the cash amount and the credit in your taxable income, then use the credit to reduce or eliminate the tax you owe, with any excess refunded as cash if your tax rate is lower than 30%.

To calculate the franking credit on a fully franked dividend, multiply the cash dividend amount by 30 and divide by 70. For example, a $1,000 cash dividend generates a franking credit of $428.57, giving a grossed-up income of $1,428.57 that you report to the ATO.

Investors whose franking credits exceed their total income tax liability receive the difference as a cash refund from the ATO. This most commonly benefits SMSFs in pension phase (taxed at 0%), SMSFs in accumulation phase (taxed at 15%), and low-income retirees below the tax-free threshold.

To claim a franking credit, you must hold your shares at risk for at least 45 days around the ex-dividend date. If you sell too early, even by one day, your entitlement to the credit can be voided. A small shareholder exemption applies if your total franking credits for the financial year are under $5,000.

From 2025, the ATO introduced automatic franking credit refunds for eligible individuals aged over 60 who meet residency and compliance conditions, removing the need to manually lodge form NAT 4105. The ATO also released PCG 2025/3, an integrity guideline affecting how credits are claimed in equity-raising scenarios.