Arm Beat Every Estimate. Here’s Why the Stock Still Fell 8%

1 hr ago

Two AI hardware companies reported earnings on the same evening and collectively added tens of billions in market capitalisation the following session, while the S&P 500 simultaneously reached a fresh all-time high. That convergence is not coincidence; it is a data point about where market momentum is concentrated and what is driving it.

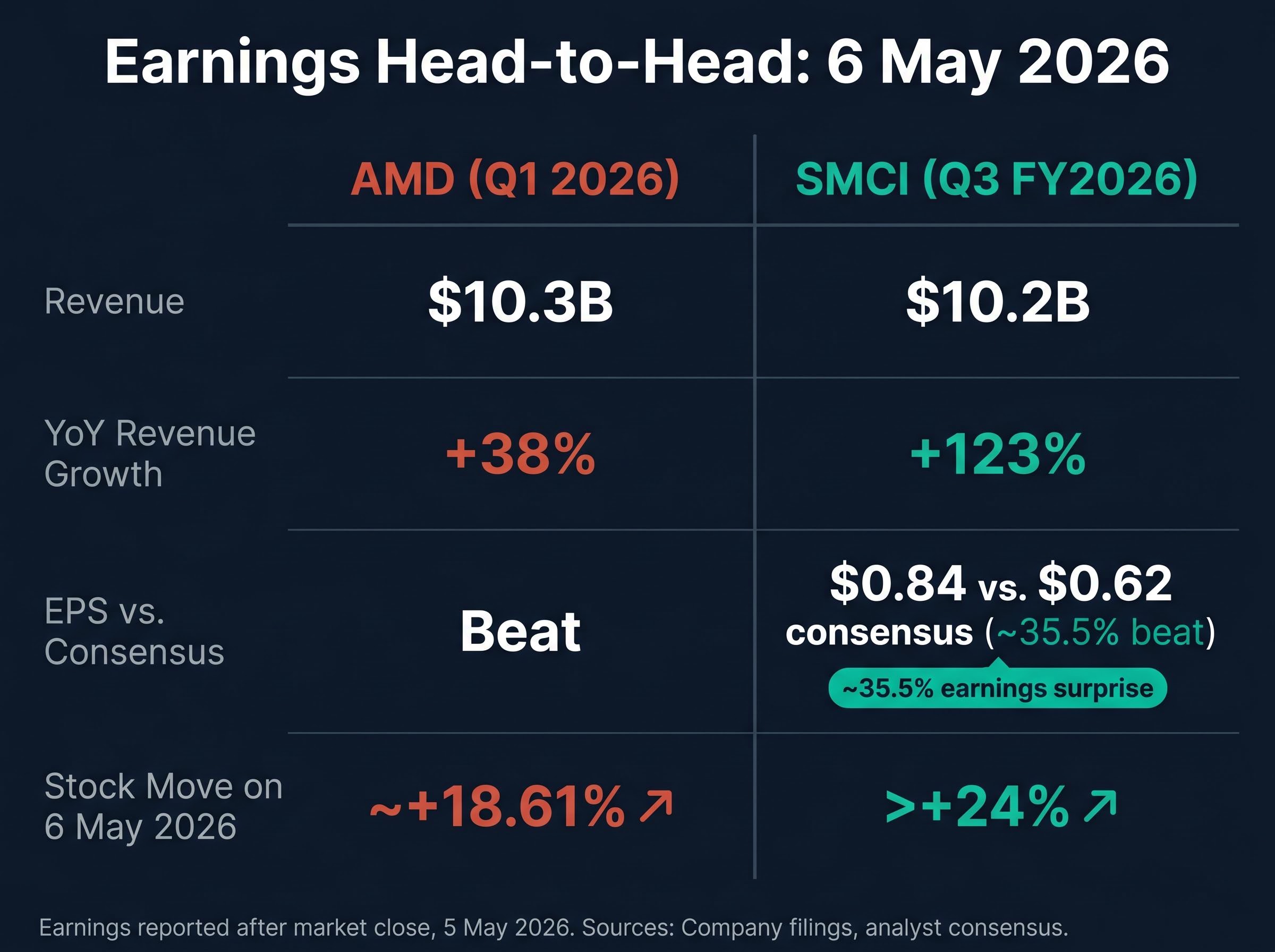

Advanced Micro Devices and Super Micro Computer reported Q1 and Q3 results respectively after market close on 5 May 2026. AMD posted $10.3 billion in revenue, up 38% year-over-year. SMCI reported $10.2 billion, up 123% year-over-year, with non-GAAP earnings per share of $0.84 beating the $0.62 analyst consensus by approximately 35%. Both stocks surged on 6 May, with the broader artificial intelligence infrastructure cohort pulling major indices to record territory.

What follows is an examination of what those results reveal about enterprise AI demand, how they fit the Q1 2026 earnings cycle, and what the concentration of AI-related names in major indices means for investors assessing whether this momentum has fundamental support or is running ahead of it.

AMD gained approximately 18.61% on 6 May 2026. SMCI surged more than 24%. Both reactions were tied directly to earnings beats reported the prior evening, and the scale of the moves warrants examination before any interpretation is offered.

AMD’s 38% year-over-year revenue growth and SMCI’s 123% year-over-year revenue growth are not in the same category as a typical large-cap beat. At $10.2 billion in quarterly revenue, SMCI delivered non-GAAP EPS of $0.84 against a $0.62 consensus, a 35.5% upside surprise that is structurally unusual at this scale.

SMCI’s non-GAAP EPS of $0.84 beat the $0.62 analyst consensus by approximately 35.5%, one of the largest earnings surprises in the AI infrastructure cohort this quarter.

| Metric | AMD (Q1 2026) | SMCI (Q3 FY2026) |

|---|---|---|

| Revenue | $10.3 billion | $10.2 billion |

| YoY Revenue Growth | 38% | 123% |

| EPS vs. Consensus | Beat (specific figure unverified) | $0.84 vs. $0.62 (~35.5% beat) |

| Single-Session Stock Move (6 May) | ~18.61% | >24% |

These are not incremental updates. The magnitude of both the earnings beats and the stock reactions sets the foundation for every layer of analysis that follows.

AMD’s headline revenue figure was not built on consumer or gaming divisions. The data centre segment was the primary driver of both revenue and earnings growth, positioning the company’s results as a direct signal of enterprise AI demand rather than a diversified-business beat.

AMD data centre revenue reached $5.8 billion in Q1 2026, up 57% year-over-year and now accounting for more than half of the company’s total quarterly revenue, with record free cash flow of $2.6 billion confirming that AI infrastructure has crossed from capital-consumption to cash-generation for the company.

SMCI’s 123% revenue growth carries a similar concentration. As a server platform builder dependent on GPU-intensive AI workloads, its results function as a downstream indicator of hyperscaler spending behaviour. When SMCI management referenced hyperscaler capital expenditure commitments as supporting forward visibility, the implication was direct: the company’s order book tracks upstream spending decisions by the largest cloud infrastructure buyers.

The four largest hyperscalers, Alphabet, Amazon, Microsoft, and Meta, are projected to spend a combined $700-$725 billion in capital expenditure during 2026, according to multiple analyst and industry reports:

Morgan Stanley raised its own hyperscaler capex forecast to $805 billion, above the consensus range. SMCI’s raised guidance for Q4 FY2026 and full-year FY2026 was explicitly linked to deferred AI shipments and hyperscaler demand, providing a structural rather than speculative basis for the forward numbers.

Morgan Stanley’s revised hyperscaler capex forecast of $805 billion places the consensus range of $700-$725 billion as a floor rather than a ceiling, reinforcing the structural basis for the forward guidance that both SMCI and AMD management cited on their earnings calls.

Both companies’ results are not independent stories. They are two measurements of the same underlying variable: enterprise AI infrastructure demand funded by the same upstream spending pool.

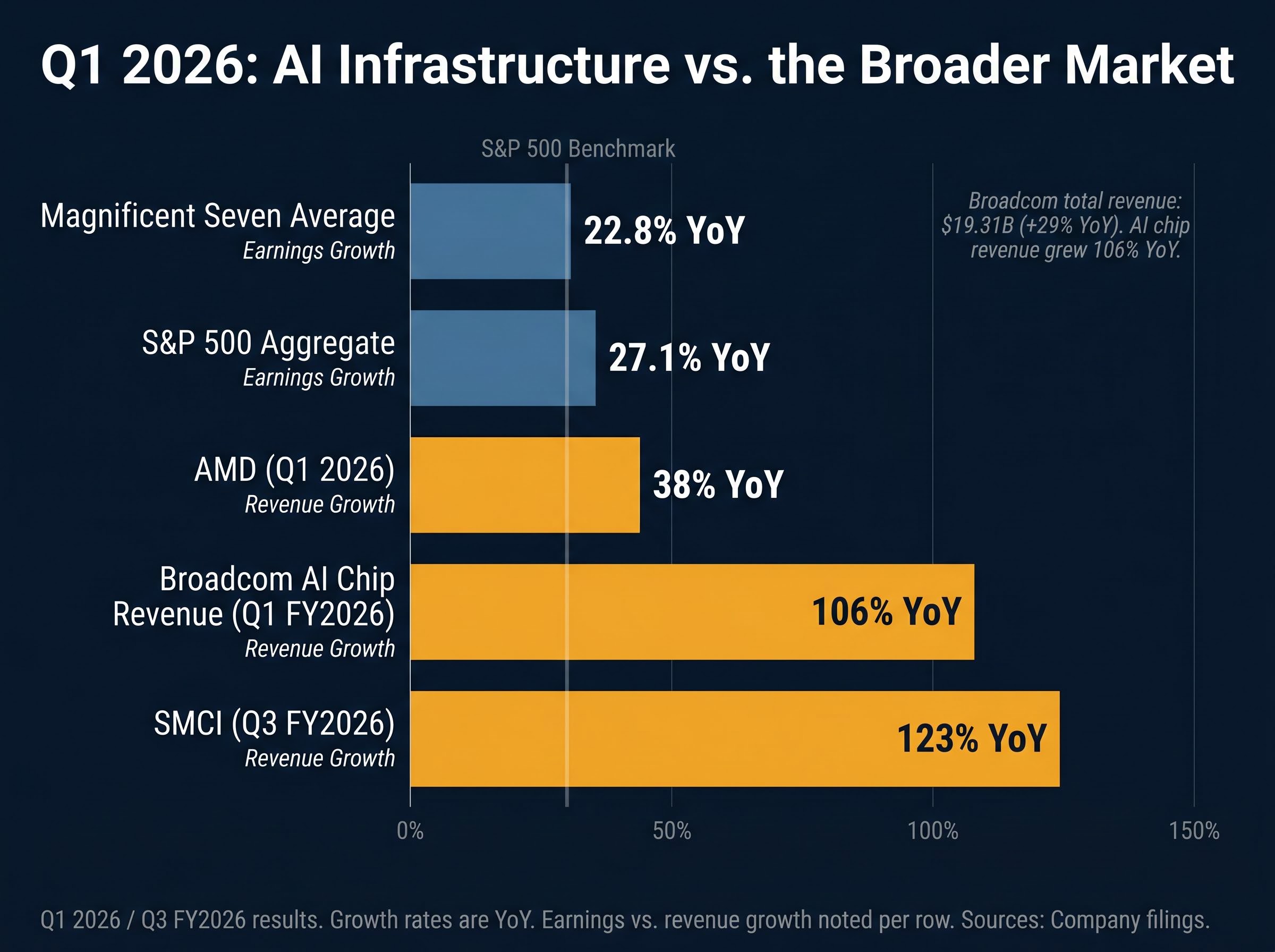

S&P 500 Q1 2026 aggregate earnings growth is tracking at approximately 27.1%. The Magnificent Seven’s estimated earnings growth for the same period sits at approximately 22.8% year-over-year. Both figures represent strong performance by historical standards.

AMD at 38% and SMCI at 123% sit well above even the Magnificent Seven average, placing them in a different growth stratum entirely within an already-outperforming cohort.

The pattern extends beyond two companies. Broadcom reported Q1 FY2026 revenue of $19.31 billion, up 29% year-over-year, with AI chip revenue growing 106% year-over-year. That result reinforces the same signal: AI infrastructure names are generating earnings growth rates that are multiples of the broader market average.

Broadcom’s AI chip revenue grew 106% year-over-year in Q1 FY2026, confirming the pattern is not an AMD-and-SMCI-specific phenomenon but a consistent dynamic across the AI infrastructure layer.

| Cohort / Company | Q1 2026 Earnings Growth (YoY) |

|---|---|

| S&P 500 Aggregate | ~27.1% |

| Magnificent Seven Average | ~22.8% |

| AMD | 38% (revenue growth) |

| Broadcom (AI chip revenue) | 106% |

| SMCI | 123% (revenue growth) |

The earnings cycle remains incomplete. Nvidia has not yet reported as of 7 May 2026, with its earnings call scheduled for 20 May 2026. Until the dominant GPU supplier to the hyperscalers that fund this entire spending cycle delivers its own results, the Q1 picture for AI infrastructure is still missing its largest data point.

The S&P 500 and Nasdaq reached fresh all-time highs on 5 May 2026, and that advance was materially assisted by AI-related stock momentum. When AI-related names represent approximately 30% of S&P 500 market capitalisation, a passive index investor is already making a concentrated AI bet whether they intend to or not.

Index concentration risk is not an abstract concern for passive investors: six technology firms now comprise over 30% of S&P 500 weighting, meaning that standard diversified portfolio construction through a single US index fund produces a materially different risk profile today than it did five years ago.

That concentration carries three structural implications:

Analysts have flagged price-to-earnings ratios above 50x for several AI infrastructure names. That metric is one variable in a multi-factor assessment, not a binary warning signal. Elevated valuations in high-growth names are not inherently disqualifying, but they require the underlying growth rates to be sustained.

The hyperscaler capex commitments outlined earlier provide one basis for sustained demand. Whether those commitments extend into 2027 and beyond at the same rate is a separate question, and one the current data does not definitively answer.

Hardware valuation risk is amplified by two factors the earnings beats alone do not resolve: physical supply chain bottlenecks including memory shortages and grid power constraints that restrict rapid deployment of approved capex budgets, and a derivatives market that some analysts flag as potentially underpricing the volatility implications of any future spending slowdown from the four major hyperscalers.

AMD, SMCI, and Broadcom have each delivered results that confirm strong AI infrastructure demand. The pattern across multiple companies and multiple quarters is now consistent. It is also incomplete.

Nvidia’s Q1 FY2027 earnings call is scheduled for 20 May 2026, the single most closely watched remaining event in the AI earnings cycle.

Nvidia remains the dominant GPU supplier to the hyperscalers whose capex figures underpin the forward guidance from companies like SMCI and AMD. Its results will either validate or complicate the pattern established so far. Two data points merit particular attention:

Analyst commentary has also flagged potential slowdowns in AI infrastructure growth post-2026, a legitimate counterweight to the current earnings optimism.

For investors wanting to translate the infrastructure demand picture into specific stock allocation decisions, our dedicated guide to Nvidia versus Broadcom as AI chip investments examines the GPU flywheel model against the custom ASIC contract model, including Broadcom’s locked-in multi-year agreements with Google and Meta, Nvidia’s valuation compression from prior peak multiples, and the structural risk from Amazon’s Trainium in-housing programme.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

The results from AMD, SMCI, and Broadcom are not sentiment-driven anomalies. They reflect a verifiable pattern of enterprise AI infrastructure demand that has now appeared consistently across multiple companies in the Q1 2026 earnings cycle, supported by hyperscaler capex commitments projected at $700-$805 billion for the year.

For index investors, the concentration of AI-related names at approximately 30% of S&P 500 market capitalisation means that both the current highs and any future volatility in the AI cohort will show up in supposedly diversified portfolios. That structural reality does not change whether the earnings news is good or bad.

The most consequential data point in this cycle arrives on 20 May 2026, when Nvidia reports. Until then, the momentum is real, the fundamentals are supporting it, and the picture is explicitly incomplete.

AI stocks are shares in companies that design, manufacture, or supply hardware and software for artificial intelligence workloads. In 2026, they are moving markets because hyperscalers like Alphabet, Amazon, Microsoft, and Meta are projected to spend a combined $700-$805 billion on AI infrastructure, driving outsized revenue and earnings growth for companies like AMD, SMCI, and Broadcom.

AMD reported Q1 2026 revenue of $10.3 billion, up 38% year-over-year, while Super Micro Computer reported Q3 FY2026 revenue of $10.2 billion, up 123% year-over-year, with non-GAAP EPS of $0.84 beating the $0.62 analyst consensus by approximately 35.5%.

AI-related names now represent approximately 30% of S&P 500 market capitalisation, meaning investors holding a standard S&P 500 index fund have significant effective exposure to the AI theme, a concentration level that may not match their intended risk profile and amplifies both gains and potential losses tied to AI sector performance.

Nvidia is scheduled to report its Q1 FY2027 earnings on 20 May 2026, and its results are considered the most consequential remaining data point in the AI earnings cycle because it is the dominant GPU supplier to the hyperscalers whose capex commitments underpin the forward guidance of companies like AMD and SMCI.

Key risks include price-to-earnings ratios above 50x for several AI infrastructure names requiring sustained growth to justify, physical supply chain bottlenecks such as memory shortages and grid power constraints, potential analyst-flagged slowdowns in AI infrastructure growth post-2026, and the amplified index-level impact if hyperscaler capex decelerates given the sector's heavy weighting in major indices.