Why AI Is Splitting Semiconductor Stocks From the Rest of Tech

2 hrs ago

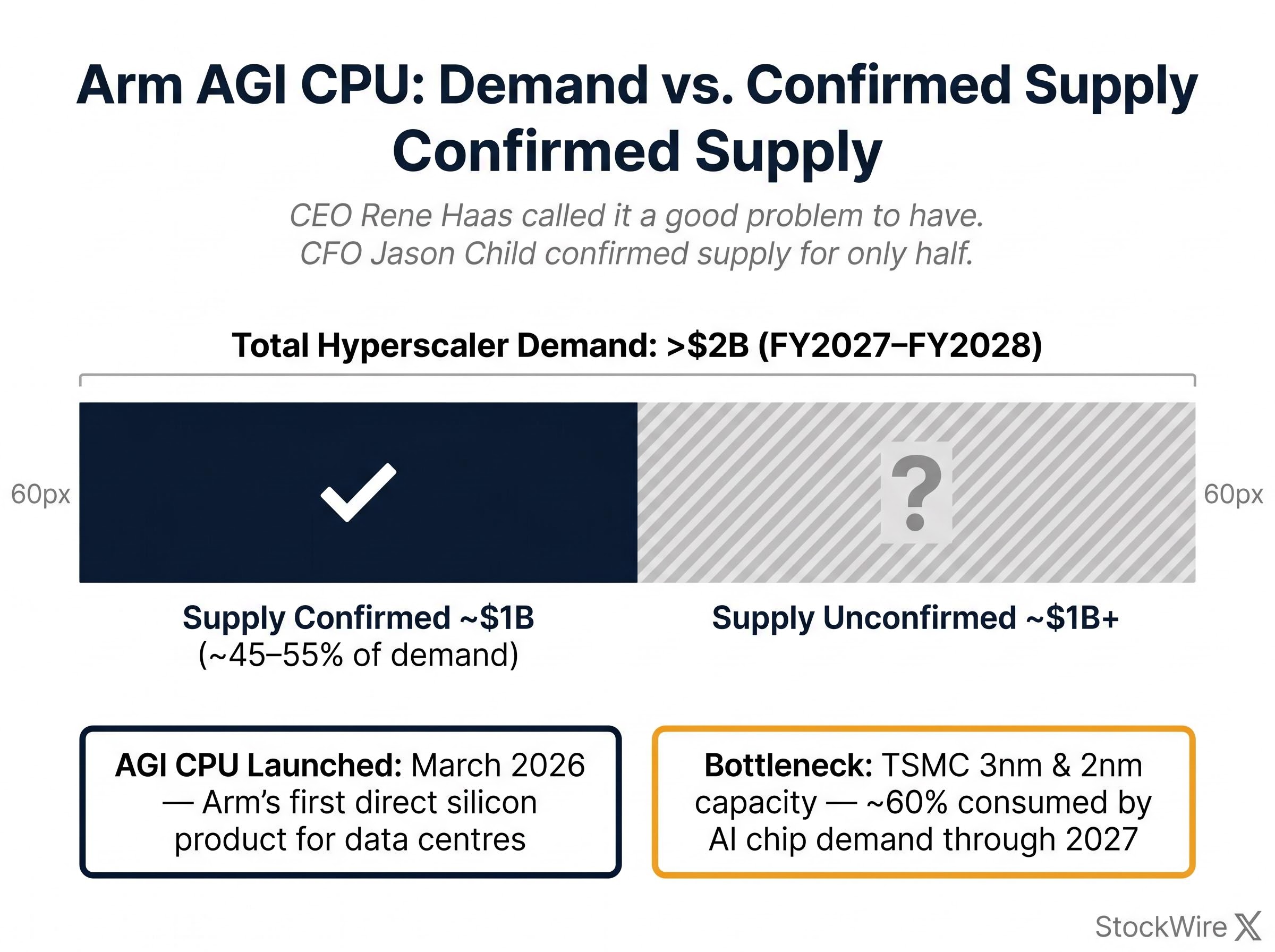

Arm Holdings delivered a beat-and-raise quarter on 6 May 2026 that, on the numbers alone, should have been a straightforward win. Revenue cleared consensus. Earnings per share came in above estimates. Forward guidance topped expectations. Then CEO Rene Haas disclosed that aggregate hyperscaler demand for Arm’s new AGI CPU product exceeds $2 billion across FY2027 and FY2028, but that supply has been confirmed for only roughly half of that figure. Within minutes, 13% of the stock’s after-hours gains evaporated. By pre-market trading on 7 May, shares sat approximately 8% below the previous close.

The reversal was not about what Arm earned. It was about what Arm may not be able to deliver. What follows is a framework for understanding how a clean financial quarter produced a sharp sell-off, how Arm’s supply gap compares to the constraints facing AMD and Intel, and what specific indicators will determine whether the situation resolves or compounds.

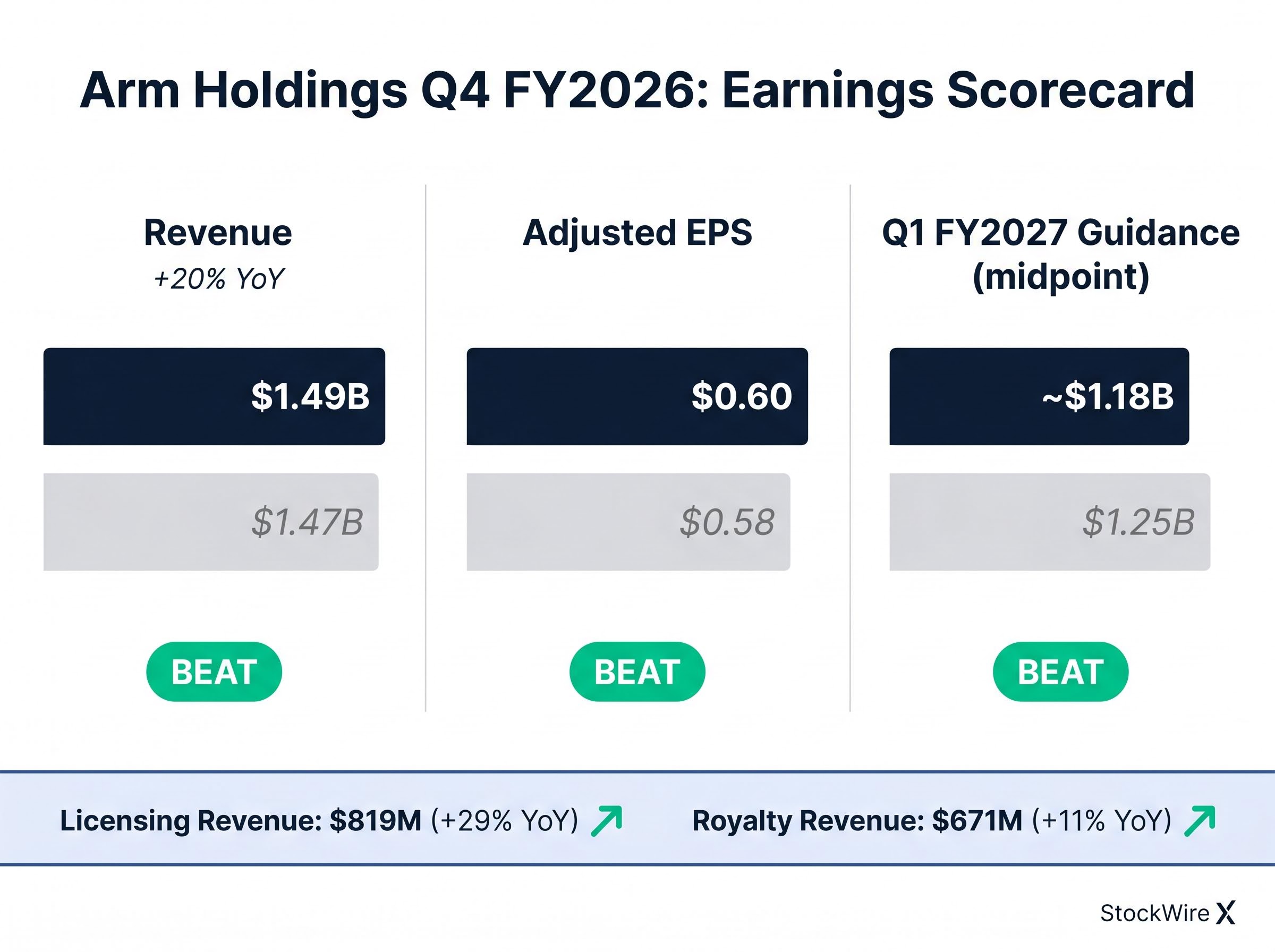

Q4 FY2026 revenue came in at $1.49 billion, up 20% year-over-year, beating the $1.47 billion consensus. Adjusted earnings per share landed at $0.60, clearing the $0.58 estimate. Both revenue streams contributed:

Q1 FY2027 guidance of approximately $1.18 billion at the midpoint (plus or minus $50 million) also cleared the $1.25 billion consensus, completing a quarter where every headline number exceeded expectations.

| Metric | Q4 FY2026 Actual | Consensus Estimate | Result |

|---|---|---|---|

| Revenue | $1.49 billion | $1.47 billion | Beat |

| Adjusted EPS | $0.60 | $0.58 | Beat |

| Q1 FY2027 Guidance (midpoint) | approximately $1.18 billion | $1.25 billion | Beat |

The stock did not decline because the quarter was weak. Investors who conflate the share price drop with a disappointing result are reading the wrong line of the earnings call.

In March 2026, Arm launched its AGI CPU product, a direct silicon play that marked a meaningful strategic departure from its traditional intellectual property licensing model. Rather than selling chip blueprints, Arm began selling finished data centre processors, a shift that placed the company in direct competition for hyperscaler server contracts.

On the earnings call, Haas framed the demand picture in terms that initially sent shares higher.

The scale of Arm’s disclosed demand becomes clearer when placed against the broader hyperscaler capex cycle: combined AI infrastructure spending across Meta, Microsoft, Alphabet, and Amazon is projected at $600 billion to $750 billion for 2026, a permanent reallocation that has shifted semiconductor supplier dynamics from demand uncertainty to supply constraint as the binding variable.

CEO Rene Haas described aggregate hyperscaler demand for AGI CPUs as exceeding $2 billion across FY2027 and FY2028, more than double the figure announced at launch, characterising the situation as “a good problem to have.”

The optimism lasted until CFO Jason Child spoke.

Child disclosed that supply has been confirmed for only the first $1 billion tranche, representing roughly 45-55% of total booked demand. Delivery in H2 FY2027 is expected to be “lumpy” due to foundry constraints.

The bottleneck sits at TSMC’s 3nm and 2nm capacity, where AI chip demand (including Arm Neoverse designs) is consuming approximately 60% of 3nm capacity through 2027. Arm’s allocations are capped not because of engineering issues but because of hyperscaler priority queuing at the foundry level. Samsung and GlobalFoundries have been cited in supply chain reporting as alternative ramp options, though TSMC retains approximately 70% share of these designs.

The pressure on Arm’s foundry allocations sits inside a broader TSMC capacity competition playing out across the entire advanced-node semiconductor industry, with Apple simultaneously exploring Samsung Foundry and Intel Foundry Services as potential US-based manufacturing alternatives in response to the same 3nm and 2nm scarcity that is capping Arm’s AGI CPU shipments.

The gap is structural, not operational. Arm has a product hyperscalers want to buy. It cannot yet secure enough foundry capacity to fill the orders.

The intraday arc on 6 May traced the market processing two distinct pieces of information in sequence:

The first move priced the beat. The second move repriced the execution risk embedded in the supply gap disclosure.

At approximately 121x forward P/E (based on the FY2027 non-GAAP EPS consensus of approximately $1.95), Arm’s valuation already embeds a strong execution assumption, leaving little margin for any new uncertainty about delivery timing.

At an EV/Revenue multiple of approximately 18x, the stock is priced for a company that converts its pipeline into recognised revenue on schedule. The supply gap disclosure introduced the first concrete evidence that conversion may be slower than the market assumed. In a valuation regime where execution is already priced as a given, even a partial disruption to the delivery timeline compresses the premium.

For investors holding Arm at 121x forward P/E, the supply gap is not the only risk to model: hardware spending sustainability across the hyperscaler cohort has attracted scrutiny from analysts who argue that $635 billion to $700 billion in FY2026 infrastructure commitments depend on generative AI application revenue catching up to deployment costs, a catch-up that has not yet materialised at scale.

Arm is not the only data centre chip supplier contending with demand that outstrips supply. Both AMD and Intel reported similar dynamics in their most recent quarters.

AMD reported Q1 2026 data centre revenue of $5.8 billion on 5 May, up 57% year-over-year, with server demand described as outpacing supply through CY2026 and a backlog exceeding $5 billion. Intel reported Q1 2026 data centre and AI revenue of $5.1 billion on 23 April, with CEO Lip-Bu Tan citing AI accelerator demand alongside x86 CPU shipment constraints related to 18A process delays and a backlog of approximately $4 billion.

AMD’s Q1 2026 beat was powered by the same structural shift: agentic AI workload demand is driving CPU procurement alongside GPU infrastructure, with AMD raising its server CPU total addressable market growth forecast from 18% to 35% annually and data centre revenue hitting $5.78 billion, a figure that contextualises exactly how large the hyperscaler appetite for non-GPU silicon has become.

| Company | Q1 2026 DC Revenue | Backlog | Supply Status |

|---|---|---|---|

| AMD | $5.8 billion | > $5 billion | Demand outpacing supply through CY2026 |

| Intel | $5.1 billion | ~$4 billion | 18A process delays constraining shipments |

| Arm | AGI CPU (new product) | > $2 billion demand | ~45-55% of demand supply-confirmed |

Piper Sandler’s 7 May note highlighted that Arm’s Neoverse architecture retains a structural edge for custom AI CPU workloads versus AMD and Intel’s general-purpose x86 designs. Barclays noted on 6 May that the hyperscaler AGI pull signals an architecture shift, but cautioned that the thesis depends on supply catching up. The difference is proportional exposure: Arm’s supply gap is larger relative to its disclosed demand, and its valuation premium leaves less room for slippage than AMD’s approximately 35x forward P/E or Intel’s lower multiple.

Arm’s traditional business model operates on two revenue streams. The first is technology licensing: upfront fees collected when chip designers adopt Arm’s architecture. The second is per-unit royalties: smaller payments collected each time a device using an Arm design ships. Both streams grew in Q4 FY2026 (licensing up 29%, royalties up 11%), and neither depends on Arm physically manufacturing anything.

The March 2026 AGI CPU launch changed this structure. By entering direct silicon manufacturing for data centre chips, Arm moved from selling blueprints to selling finished processors. Revenue from this product line is contingent on physical supply, meaning foundry constraints now directly cap how much revenue Arm can recognise.

The data centre segment’s long-term projection of $15 billion (referenced at Arm’s Everywhere event) depends on this new model scaling. The supply gap matters more for Arm than it would for a pure-play IP licensor precisely because the business model shift has tied revenue to physical delivery.

ARK Invest stated publicly on 6 May that the supply gap represents an execution risk rather than a demand risk, indicating an intention to add to its position on the dip. KeyBanc Capital Markets characterised the disclosure as a reality check on AGI hype, trimming FY2027 EPS estimates by 5% while maintaining its Overweight rating. Piper Sandler’s 7 May note acknowledged that the supply gap exposes higher execution risk than AMD’s fuller demand visibility, but concluded that the Neoverse architecture advantage remains intact.

Three forward-looking indicators will determine whether the supply gap resolves or widens:

Analyst price targets reflect the range of outcomes the street is pricing:

The spread between $125 and $255 is itself a measure of how uncertain the execution path remains.

Q4 FY2026 was a genuine beat-and-raise quarter. The licensing business grew 29%. Royalties expanded 11%. Guidance cleared consensus. On the financials alone, there was nothing to sell.

The after-hours reversal was not irrational. At 121x forward P/E, Arm’s share price has always been a bet on execution, and the 6 May disclosure introduced the first concrete evidence that execution on the AGI CPU may be slower than the valuation assumed. ARK Invest sees an execution delay worth buying through. KeyBanc sees a reason to trim estimates while holding conviction. Both readings are internally consistent; the difference lies in how much tolerance each investor assigns to a supply gap of this scale at this multiple.

The quarter answered the demand question. The supply question remains open.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Arm reported Q4 FY2026 revenue of $1.49 billion, up 20% year-over-year, beating the $1.47 billion consensus, with adjusted EPS of $0.60 against a $0.58 estimate. Q1 FY2027 guidance of approximately $1.18 billion at the midpoint also cleared consensus expectations.

The sell-off followed CFO Jason Child's disclosure that supply has been confirmed for only roughly half of the $2 billion in aggregate hyperscaler demand for Arm's new AGI CPU product, introducing execution risk into a stock already trading at approximately 121x forward P/E.

The AGI CPU, launched in March 2026, is a finished data centre processor that Arm sells directly to hyperscalers, departing from its traditional IP licensing model. Unlike royalty and licensing revenue, this product line ties Arm's revenue recognition directly to physical supply, meaning foundry constraints now cap how much revenue the company can deliver.

The bottleneck sits at TSMC's 3nm and 2nm capacity, where AI chip demand is consuming approximately 60% of 3nm capacity through 2027, and Arm's foundry allocations are capped by hyperscaler priority queuing rather than any engineering failure. Delivery in H2 FY2027 is expected to be lumpy as a result.

All three companies face demand exceeding supply: AMD reported a backlog above $5 billion with server demand outpacing supply through CY2026, and Intel cited a roughly $4 billion backlog alongside 18A process delays. Arm's gap is proportionally larger relative to its disclosed demand, and its approximately 121x forward P/E leaves less tolerance for slippage than AMD's roughly 35x multiple.