One of the architects of modern AI safety thinking has just filed paperwork revealing he has bet roughly $8.46 billion in notional exposure against the very chip stocks powering the AI boom he helped forecast. Leopold Aschenbrenner, a former OpenAI researcher who built his reputation on bullish AI development forecasting, disclosed through Situational Awareness LP’s Q1 2026 Form 13F (filed 18 May 2026) that his fund holds put options against ten major AI semiconductor names and ETFs. For retail and institutional investors navigating an already volatile sector, an insider turned short-seller is a signal worth decoding carefully. This analysis explains who Aschenbrenner is and why his positioning matters, breaks down what the 13F shows, teaches readers how to interpret put options as hedges versus directional bets, situates the move within broader institutional scepticism building around AI chip valuations, and frames what NVIDIA’s imminent earnings release means for the trade.

From AI bull to bearish insider: who Leopold Aschenbrenner is and why this filing matters

Leopold Aschenbrenner is still in his mid-twenties. That alone makes him an unusual figure to be managing a fund with billions of dollars in notional options exposure filed with the Securities and Exchange Commission (SEC). A former OpenAI researcher, Aschenbrenner became a recognised voice in AI forecasting circles through public writings that detailed aggressive AI development trajectories and the infrastructure buildout they would require.

Before this filing, Situational Awareness LP was characterised by bullish wagers on AI-related equities, including early identification of lesser-known AI-adjacent companies before they gained mainstream attention. The fund’s analytical framework, built on deep familiarity with the AI supply chain, produced conviction positions on the long side of the trade.

The same analytical lens that made Aschenbrenner bullish on AI infrastructure has now produced a bearish posture specifically targeted at the semiconductor supply chain that supports it.

The Q1 2026 13F, filed on 18 May 2026 and reflecting positions as of the 31 March 2026 quarter-end (SEC EDGAR filing ID: data/2045724), marks a public reversal. When a credentialed AI insider who was previously long the sector pivots to puts, it warrants scrutiny beyond the typical short-seller note.

When big ASX news breaks, our subscribers know first

What the 13F actually shows: $8.46 billion in notional put exposure across ten names

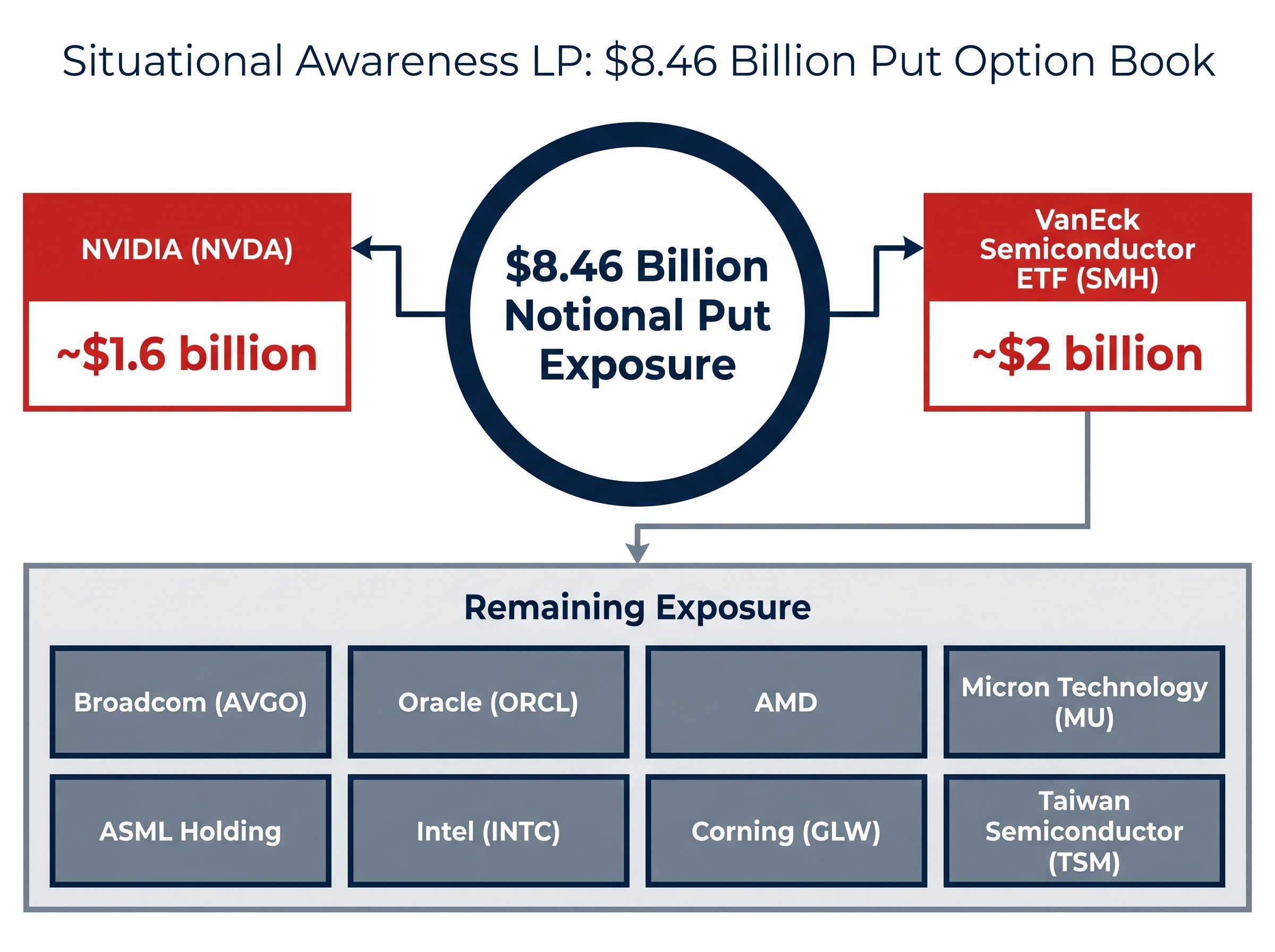

The filing discloses put positions across ten AI semiconductor and technology names, totalling approximately $8.46 billion in notional exposure. Two positions dominate the book. The remaining eight spread the bet across the broader supply chain.

A key interpretive caveat: 13F filings reflect holdings at quarter-end (31 March 2026), meaning this snapshot is approximately seven weeks old at the time of publication. Positions may have changed. All targeted stocks have appreciated considerably since Q1 end, which means any puts still held would currently carry reduced intrinsic value.

The AI hardware and software performance divergence running through 2026 provides useful context for the filing’s scope: the Morningstar Global Semiconductor Equipment index has gained 47.6% year-to-date while the Software Applications index has fallen 22.7%, a spread that partially explains why a bearish fund would concentrate put exposure in the hardware supply chain rather than the software layer.

The two headline positions: NVIDIA and the VanEck Semiconductor ETF

NVIDIA (approximately $1.6 billion notional) and the VanEck Semiconductor ETF (SMH, approximately $2 billion notional) together represent the broadest expression of the bearish thesis. NVIDIA is the single-stock flagship of the AI chip trade; SMH provides exposure to the entire AI chip supply chain in one instrument. Pairing the two allows the fund to bet against both the category leader and the sector simultaneously.

The remaining eight: where the rest of the exposure sits

The remaining positions span memory, logic, equipment, foundry, and infrastructure segments of the semiconductor ecosystem.

| Company or ETF | Ticker | Approx. Notional Exposure | Sector Role |

|---|---|---|---|

| NVIDIA | NVDA | ~$1.6 billion | AI GPU design |

| VanEck Semiconductor ETF | SMH | ~$2 billion | Sector-wide ETF |

| Broadcom | AVGO | Undisclosed breakdown | Networking and custom silicon |

| Oracle | ORCL | Undisclosed breakdown | Cloud infrastructure |

| AMD | AMD | Undisclosed breakdown | GPU and CPU design |

| Micron Technology | MU | Undisclosed breakdown | Memory (HBM and DRAM) |

| ASML Holding | ASML | Undisclosed breakdown | Lithography equipment |

| Intel | INTC | Undisclosed breakdown | Foundry and CPU design |

| Corning | GLW | Undisclosed breakdown | Fibre optic infrastructure |

| Taiwan Semiconductor | TSM | Undisclosed breakdown | Contract chip fabrication |

Corning and Oracle sit slightly adjacent to pure-play chip exposure, covering fibre optic infrastructure and cloud software respectively. The remaining six names map directly onto the AI semiconductor supply chain from design through fabrication to memory.

Two ways to use a put: interpreting institutional options positions in a 13F filing

Before drawing conclusions about what the Situational Awareness LP filing signals, readers need a framework for interpreting what a put option actually does inside an institutional portfolio.

A put option gives its holder the right to sell an asset at a specified price before a set date. It gains value if the underlying asset falls in price. Institutions use puts in two fundamentally different ways:

- Portfolio hedging: The fund holds long positions in the same or related stocks and buys puts as insurance against a decline. In this scenario, the puts are a cost of protection, not a bet on collapse. Distinguishing features include puts paired with disclosed long holdings, relatively modest notional size relative to the long book, and expiry dates aligned with known risk events.

- Directional short bet: The fund buys puts without corresponding long positions, wagering that prices will fall. Distinguishing features include large notional exposure without offsetting longs, concentration in a single sector or theme, and strike prices set meaningfully below current trading levels.

13F filings do not disclose strike prices, expiry dates, or the fund’s long book. The filing is a partial picture only. Without knowing whether Situational Awareness LP holds offsetting long positions, the puts could represent either insurance or conviction.

This distinction matters. A $8.46 billion notional put book reads very differently as a hedge on a $15 billion long portfolio than it does as a standalone directional wager.

The interpretive gap matters especially for retail investors, because the short selling risks for retail investors who attempt to replicate institutional put strategies include borrow fees, margin requirements, and timing drag that erode returns even when the directional thesis proves correct.

Aschenbrenner is not alone: the institutional scepticism building around AI semiconductor valuations

The Situational Awareness LP filing does not exist in isolation. A pattern of institutional caution has been building around AI chip valuations through multiple channels.

At the Sohn Investment Conference on 14 May 2026, two fund managers drew explicit historical parallels. Joyce Meng of Fact Capital and Soren Aandahl of Blue Orca Capital compared current AI chip valuations to prior technology manias, including the railroad boom, the internet bubble, and the French Mississippi Bubble of the 1720s. According to CNBC reporting, AI chip valuations by at least one concentration metric now rival that 18th-century speculative episode and exceed Nasdaq valuations at the dot-com peak.

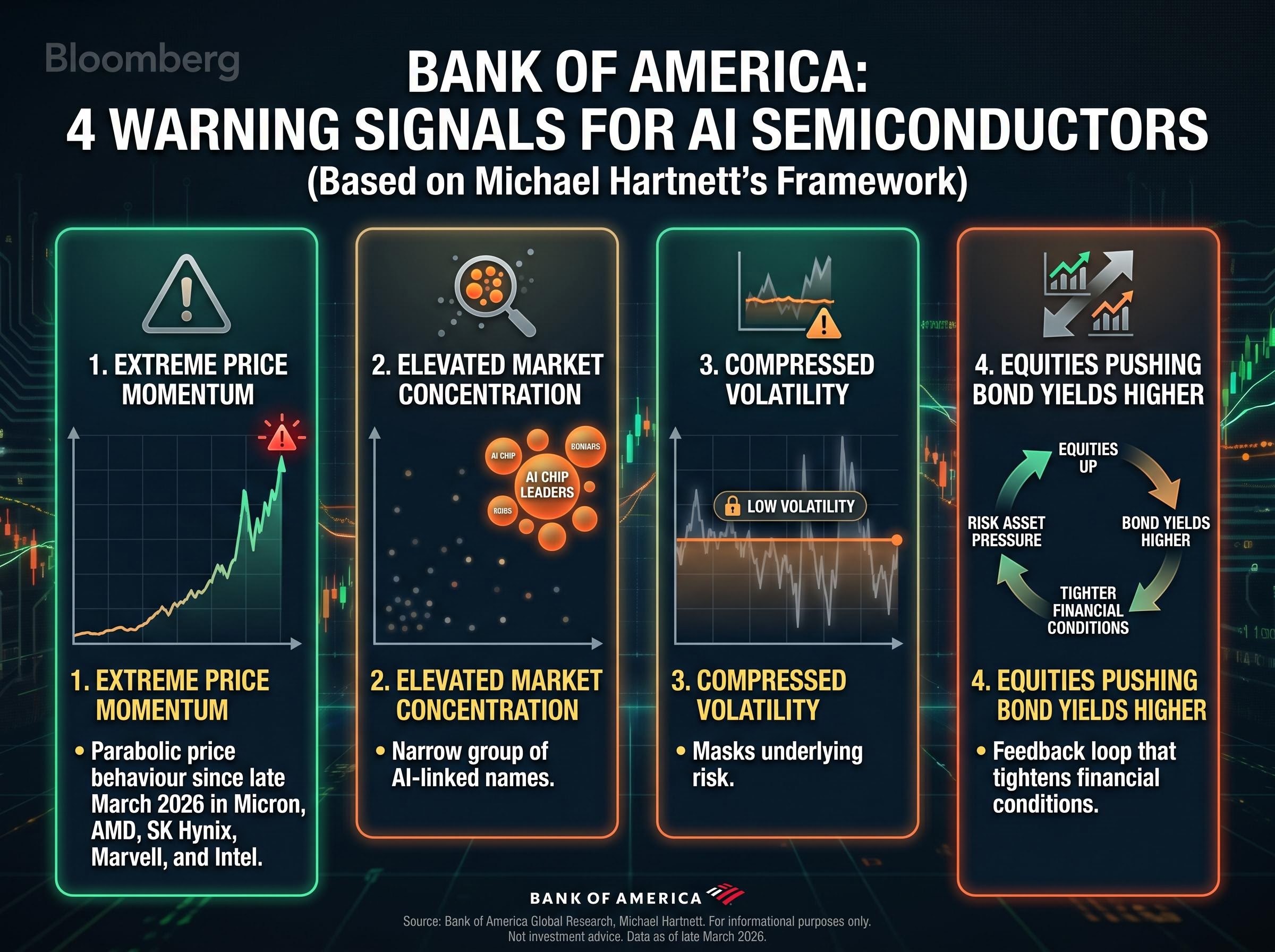

Bank of America strategist Michael Hartnett has identified four warning signals in the current market environment:

- Extreme price momentum across the semiconductor complex

- Elevated market concentration in a narrow group of AI-linked names

- Compressed volatility that masks underlying risk

- Equities pushing bond yields higher, a feedback loop that tightens financial conditions

Parabolic price behaviour since late March 2026 has been documented in Micron, AMD, SK Hynix, Marvell, and Intel.

Historical analogies and what they do (and do not) tell us

The railroad and internet parallels carry a consistent lesson: in each case, the underlying technology succeeded while many early equity participants failed. The infrastructure was real. The valuations were not.

That said, historical analogies are illustrative, not predictive. AI infrastructure spending remains robust by most near-term metrics, and a Bloomberg survey found that roughly 80% of the 32 investment managers polled across the US, Asia, and Europe remain bullish on equities overall. Scepticism is a minority institutional view, not a consensus call. Goldman Sachs economist Dominic Wilson has noted the current market environment is growing more complex, with risk that overly aggressive expectations create a valuation overhang even as AI infrastructure spending continues to support chip revenues.

The structural foundation of the bearish thesis rests on a capex-to-revenue lag that Morningstar analyst Dennis Li estimates at 18-24 months, meaning the $725 billion in 2026 hyperscaler commitments may not translate into semiconductor revenue at the pace implied by current valuations.

Rising rates, stretched multiples, and why AI chip stocks face a difficult macro backdrop

The who-is-betting-against question leads naturally to a why-it-might-work question. The macro environment provides the intellectual foundation for the bearish thesis.

AI semiconductor stocks are long-duration assets. Their valuations depend heavily on earnings expected years into the future. When interest rates rise, the present value of those distant earnings compresses, because the risk-free rate used to discount them increases. This is not theoretical. The Bloomberg survey of 32 investment managers in mid-May 2026 identified elevated bond yields as the primary recognised risk to equity markets.

NBER duration-based stock valuation research establishes that long-duration growth equities are disproportionately sensitive to discount rate movements, with even modest increases in the risk-free rate compressing present values sharply when earnings are weighted toward the distant future.

The structural pressure points facing the AI chip complex include:

- Rising Treasury yields compressing discounted cash flow valuations for long-duration growth names

- Elevated market concentration, where the most expensive names carry the longest implied payback periods

- Long-duration earnings dependence that amplifies sensitivity to rate movements

- Compressed volatility that may understate the probability of a sharp repricing event

Hartnett’s specific warning that equities are exerting upward pressure on bond yields describes a feedback loop: strong equity performance draws capital from bonds, pushing yields higher, which in turn pressures the very growth stocks driving the rally.

Goldman Sachs’s Dominic Wilson has offered a counterpoint. AI infrastructure capital expenditure commitments from hyperscalers remain a genuine near-term revenue tailwind for chip makers. The tension between macro headwinds and micro demand support is where the real analytical debate sits. Retail investors who understand this yield-duration relationship are better positioned to assess when the macro environment becomes more or less supportive of the AI equity trade.

What NVIDIA’s earnings Wednesday will tell investors about whether the bears are early or right

NVIDIA reports earnings on Wednesday, 21 May 2026, two days from publication. The report functions as the most proximate test of whether AI semiconductor demand fundamentals can sustain current valuation multiples.

Two data points will matter most: data-centre revenue performance against consensus expectations, and forward guidance language on hyperscaler demand. The outcomes split into two distinct scenarios for the bearish thesis.

| Scenario | Implication for Bearish Thesis |

|---|---|

| Strong beat with bullish guidance | Compresses the puts’ value further, reinforces the bull case, and extends the timeline before any valuation reckoning |

| Miss or cautious forward guidance | Validates the bearish positioning and could accelerate sector-wide repricing as momentum names lose their earnings anchor |

The 13F timing gap complicates interpretation further. Positions were as of 31 March 2026, meaning Situational Awareness LP’s current exposure is unknown and may have already been adjusted ahead of this earnings event.

One earnings print does not resolve a structural valuation debate. Even if NVIDIA beats, the questions raised by Aschenbrenner’s filing, the Sohn presenters, and Hartnett’s warning signals do not disappear after a single quarter’s results.

One filing, one data point, and a sector at an inflection point

Aschenbrenner’s $8.46 billion notional put book is the most concrete signal yet that credentialed AI insiders are no longer uniformly bullish on the semiconductor supply chain. The filing aligns with a wider pattern of institutional caution expressed through conference presentations, strategy notes, and historical valuation comparisons.

The interpretive limits established earlier bear repeating. The 13F is a partial snapshot. The puts may be hedges rather than pure directional bets. The fund’s current posture is unknown. Retail investors monitoring this theme should watch two forward-looking signals: NVIDIA’s 21 May earnings data-centre revenue print and any further 13F disclosures in subsequent quarters from Situational Awareness LP.

The discipline here is reading institutional positioning as one input among several, not as a trading signal to replicate directly. The structural questions about AI chip valuations, rate sensitivity, and concentration risk are real. Whether the bears are early, right, or both remains an open question that no single filing or earnings report will close.

Investors who want to stress-test the bearish thesis against the strongest available bull case should read our deep-dive into hyperscaler AI capital expenditure commitments, which documents how Amazon, Microsoft, Alphabet, and Meta spent $130 billion in Q1 2026 alone and tracks the revenue metrics that would need to disappoint to validate a structural repricing of semiconductor names.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.