The June consumer price index came in below expectations, and Nasdaq 100 futures had climbed 0.6% by 03:53 ET on Tuesday 15 July. For growth stocks priced on rate expectations, cooler inflation is oxygen.

Then the complication. By this morning, the U.S. military had completed a fourth straight day of operations against Iran, and crude oil holds the fate of everything the inflation number just unlocked. If oil spikes, the CPI print becomes a footnote. If oil stays contained, the print becomes a catalyst.

These are not two separate stories. The CPI only matters because it shifts Federal Reserve calculus. The Iran conflict only matters because it can re-accelerate inflation through a single channel: crude prices. One variable connects both forces, and that variable is trading in real time.

Here is what actually matters for the stock market this week, and in what order to watch it.

What the June CPI print actually unlocked for markets

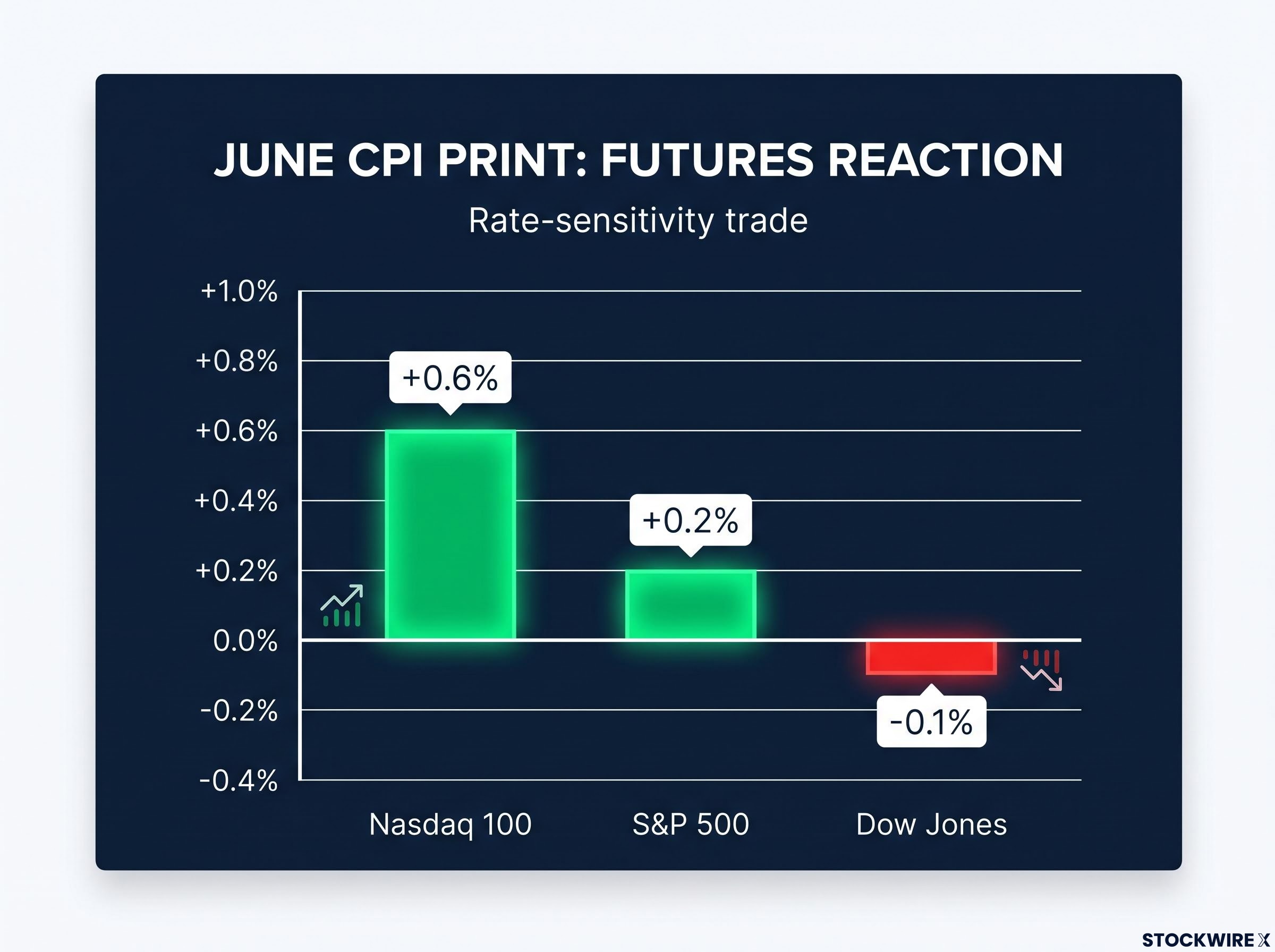

The number landed soft. June CPI cooled clearly from May, and futures moved before most investors had checked their screens. But the reaction was not uniform, and the divergence tells you exactly what kind of trade this is.

- S&P 500 futures: +0.2%

- Nasdaq 100 futures: +0.6%

- Dow Jones futures: –0.1%

The Nasdaq tripled the S&P 500‘s gain while the Dow slipped into the red. That split is not noise. Growth and technology stocks carry longer duration, meaning their valuations are more sensitive to where interest rates are heading. When inflation cools, the probability of further Fed tightening drops, and the present value of future earnings for high-growth names rises disproportionately. The Dow, weighted toward shorter-duration industrials and financials, does not benefit the same way.

Growth stock valuations are mechanically sensitive to discount rate changes because the bulk of their intrinsic value sits in earnings projected years out; a one-percentage-point rise in the rate used to discount those future cash flows compresses present value meaningfully even when underlying business performance remains unchanged.

The CPI data reduced near-term fears the Fed might resume tightening. That is what moved futures, not the inflation number itself.

This is a rate-sensitivity trade, not a broad market rally. Tech and AI names are the primary beneficiaries, and the reader holding a diversified portfolio should recognise that today’s headline gains may be concentrated in one corner of the market rather than spread across it.

When big ASX news breaks, our subscribers know first

The Iran conflict on day four: what “market desensitisation” actually means

What is happening

On 15 July 2026, the U.S. military wrapped up a fourth day of consecutive strikes on Iranian soil. Speaking to Fox News, President Trump indicated that operations would press on until Tehran came to the table, though he acknowledged that Iranian representatives had signalled openness to negotiations. Separately, the administration pulled back a previously announced plan to levy fees on vessels navigating the Strait of Hormuz, removing one immediate pressure point for international shipping operators and energy cost expectations.

Why market calm is not market safety

Here is the counterintuitive part. Markets have largely stopped flinching at each new strike headline. Day one moved crude. Day four barely registered. That pattern has a name: desensitisation. Repeated exposure to similar headlines reduces the per-headline price impact. But desensitisation does not reduce the underlying risk of a supply disruption; it reduces the market’s preparedness for one.

A disruption to oil moving through the Strait of Hormuz could swiftly revive inflation concerns and undo the equity gains the CPI data helped create.

The fact that markets are treating day-four strikes as routine extension rather than fresh shock means the next genuine escalation, a confirmed disruption to tanker flows or damage to loading infrastructure, would hit a market that is structurally under-hedged for that scenario. That asymmetry is the real risk to price in right now.

The Hormuz oil risk premium built into crude prices reflects more than headline military exchanges; the near-total withdrawal of commercial war-risk insurance has effectively constrained tanker traffic even during periods when physical passage was technically open, creating a structural tightness that persists independently of day-to-day diplomatic signals.

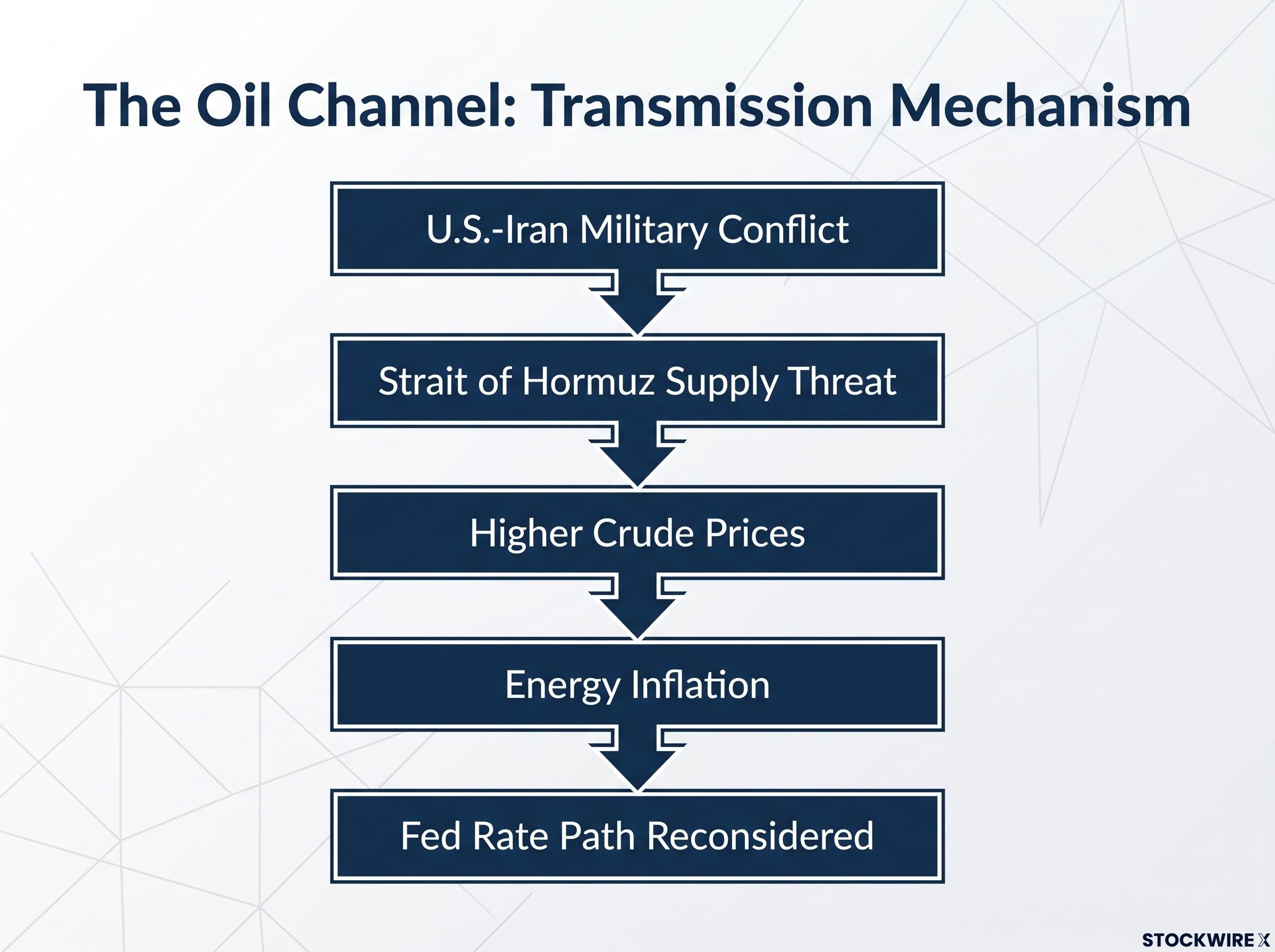

The oil channel: how geopolitical escalation connects directly to the CPI story

The transmission mechanism is specific: Middle East escalation threatens oil supply, a supply disruption drives crude prices higher, higher crude feeds directly into energy inflation, and energy inflation forces the Fed to reconsider its rate path regardless of what the June CPI just showed. The two lead stories of the day are not independent. They are linked through a single variable, and crude prices are therefore the most important indicator to monitor this week.

How inflation data and geopolitical risk interact, and why crude prices are the arbiter

The June CPI print is only as durable as crude prices allow it to be. That is the conditional logic that frames this entire week.

If oil stays contained, the inflation data supports the case for the Fed holding rates steady, growth stocks continue to benefit, and earnings season plays out against a constructive macro backdrop. If geopolitical escalation drives crude materially higher, the inflation relief evaporates, the Fed’s ability to hold steady is compromised, and the equity gains built on the CPI print unwind.

| Factor | Category | Market implication |

|---|---|---|

| Cooler June CPI | Supportive | Reduces probability of further Fed tightening; favours growth equities |

| Tech and AI earnings momentum | Supportive | Reinforces sector leadership and near-term index support |

| Strong initial bank results (JPM, BAC, MS, BNY) | Supportive | Confirms financial sector resilience under current rate environment |

| U.S.-Iran military conflict (day 4) | Risk | Any Strait of Hormuz disruption could reignite inflation fears rapidly |

| Cautious corporate guidance potential | Risk | Weak forward outlook from consumer-exposed sectors may trigger multiple compression |

Watch the VIX, breakeven inflation rates (the market’s real-time inflation expectation gauge), and Fed funds futures (which price in the probability of future rate moves). These are the instruments that tell you whether the market’s current read is shifting. The week’s question is not whether the CPI was good. It is whether crude prices allow the CPI signal to hold, and that is a geopolitical question as much as an economic one.

Q2 earnings season: what the first bank results reveal about market selectivity

The initial wave of bank earnings arrived, and identical macro conditions produced dramatically different stock reactions.

| Company | Q2 earnings reaction | Signal for investors |

|---|---|---|

| JPMorgan Chase | +2.50% | Execution rewarded in a supportive macro backdrop |

| Bank of America | +1.88% | Solid beat met with measured optimism |

| Morgan Stanley | +2.98% | Strongest bank rally; capital markets activity rewarded |

| BNY | +2.14% | Custody and servicing revenue held up |

| Citigroup | -5.29% | Sharp punishment despite broadly supportive conditions |

| Wells Fargo | -2.71% | Disappointing results met with immediate selling |

Citigroup’s 5.29% single-day drop in a macro environment that should have been supportive tells you the market is not in a mood to overlook execution risk. When the backdrop is constructive and individual names still get punished this severely, valuations are stretched enough that investors are demanding delivery, not giving benefit of the doubt.

The earnings expectations gap explains why Citigroup fell 5.29% in a macro environment that should have been supportive: markets price the difference between reported results and prior forecasts, not results in absolute terms, so any company trading at a stretched valuation faces disproportionate punishment when delivery falls short of what was already priced in.

Why guidance matters more than results this earnings season

Today’s scheduled reporters add distinct information beyond their individual stock impact. BNY and BlackRock offer a window into how institutional capital is being deployed, where fund flows are heading, and how portfolio allocations are shifting. Morgan Stanley extends the capital markets read. United Airlines offers a real-time consumer and business demand read through bookings and revenue per available seat mile (a metric that measures how much an airline earns for each seat flown one mile).

Backward-looking results confirm the past. Guidance language on demand, margins, geopolitical disruptions, and borrowing costs tells investors what Q3 and Q4 hold. Any language from financial or consumer-exposed companies that signals hesitation about the back half of 2026 is where the earnings risk concentrates. If you hold rate-sensitive or consumer-exposed positions, today’s guidance from BlackRock and United Airlines is a direct signal for your own portfolio exposure.

The next major ASX story will hit our subscribers first

What investors should actually watch this week, ranked by market impact

The logic established across this piece points to a clear priority order. Not all news carries equal weight this week.

- Crude oil prices and any Strait of Hormuz developments. A confirmed disruption to oil flows overrides everything else instantly. Watch Brent and WTI for any move above recent ranges; that is the signal that the geopolitical risk is no longer being absorbed.

- Earnings reactions, specifically guidance from BlackRock, United Airlines, and forward-looking commentary from financials. A single cautious guidance line from United Airlines is a data point, not a market event, but a pattern of cautious guidance across consumer-exposed names shifts the entire earnings narrative.

- Fed rhetoric distinguishing the inflation trend from a geopolitical one-off. Any language from Fed officials suggesting oil-related price pressures could feed through to core inflation would change the rate calculus rapidly.

- Whether sector leadership broadens beyond tech and AI or remains narrow. A rally carried by a handful of growth names is structurally more fragile than one with broad participation.

- Treasury yields and Fed funds futures as real-time rate expectation trackers. If implied rate cut timing shifts materially, equity valuations will follow.

The macro and geopolitical stories can flip direction within hours of each other. Crude prices sit at the top of this list regardless of how other variables move.

Whether this week resolves the tension or deepens it

The week ahead is a test with a specific outcome structure. If oil stays contained, earnings guidance holds, and Fed commentary validates the CPI signal, equities have a credible path toward new highs. If any of the three fails, year-to-date gains face meaningful compression risk.

A market that finishes the week with both geopolitical risk elevated and earnings guidance weakened simultaneously would represent a qualitatively different risk environment than the one that opened Monday. The rally has been narrowly led by growth and AI names, which makes it structurally more fragile than broad-participation rallies historically.

Narrow market leadership concentrated in megacap technology and AI names has characterised the 2026 rally from its earliest stages, with gains of approximately 10% year-to-date masking the degree to which broader participation has lagged, a structural feature that amplifies the downside when the leading sector faces a concurrent macro and earnings headwind.

The week’s question is not whether the CPI was good, but whether crude prices allow the signal to hold.

The honest answer is that this week’s outcome is genuinely uncertain, and positioning accordingly is more useful than a directional prediction. Today’s CPI optimism and the fourth day of Iran strikes represent a tension that will either resolve or break by Friday. The reader’s job is not to predict the outcome but to know in advance what resolution and what a break each look like, so the response is driven by data rather than headlines.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements are speculative and subject to change based on market developments and company performance.