Two earnings announcements landed within 24 hours of each other this week, and they produced opposite outcomes. That is not coincidence. It is a signal about where the AI boom is creating value, and where it is quietly destroying it.

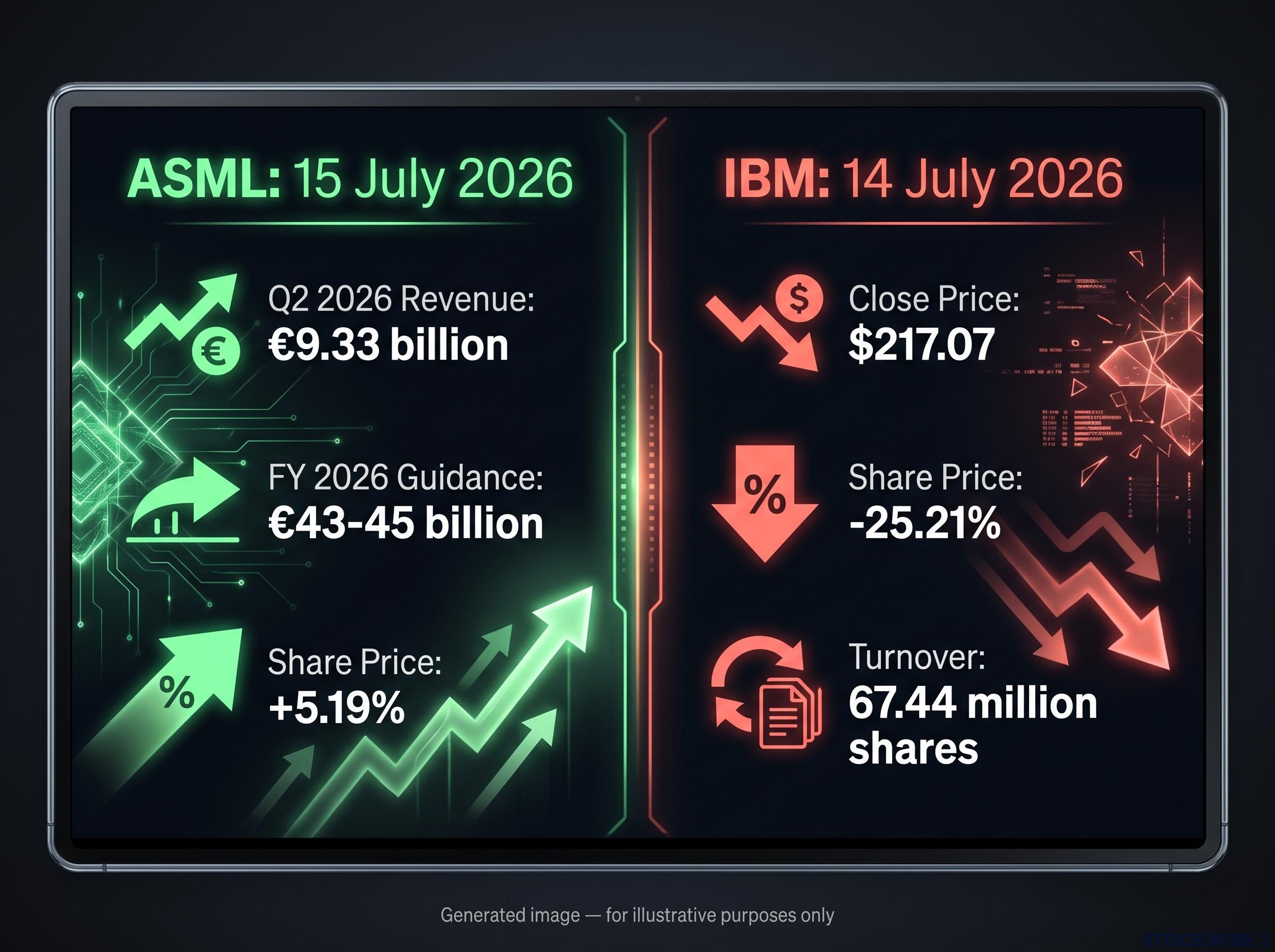

On 14-15 July 2026, ASML reported a blowout quarter with €9.33 billion in Q2 revenue and raised its full-year guidance to €43-45 billion, sending shares up more than 5%. On the same day, IBM disclosed that enterprise customers were cutting software budgets to fund AI hardware. Its shares collapsed 25.21% on turnover of 67.44 million shares traded. These are not two separate stories. They are two sides of the same structural shift in how AI capital gets allocated across the technology sector.

The AI spending shift reshaping tech portfolios is not about whether AI is growing. It is about which layer of the technology stack captures that growth and which layer funds it. Here is a framework for classifying any tech holding by its position in that food chain, and for monitoring what comes next as the reallocation continues.

What ASML’s numbers are actually telling the market

ASML is not just a semiconductor equipment company. Its order book functions as a thermometer for multi-year AI infrastructure confidence. Chipmakers only commit to purchasing lithography systems, the machines that print circuit patterns onto silicon wafers, when they have high-conviction visibility on demand stretching years into the future. A guidance upgrade from ASML is not a routine beat-and-raise. It is a statement about where the largest technology companies on earth are placing irreversible capital bets.

The Q2 2026 reading on that thermometer came in hot:

- Q2 2026 revenue: €9.33 billion, beating analyst consensus

- Full-year 2026 guidance raised: €43-45 billion, materially above prior projections

- Share price: up 5.19% on 15 July 2026

- Management attribution: upgrade driven by AI-related demand for advanced logic and memory chips

The full-year guidance raise is the number that matters most. When hyperscalers and leading chipmakers are placing orders years in advance, they are betting real capital on sustained AI workload growth. That forward commitment is what the guidance raise reflects, and it tells you this infrastructure cycle has legs beyond the current quarter.

The individual quarterly beat matters less than the raised trajectory. ASML’s customers are not ordering more lithography tools because of one strong quarter in AI chip sales. They are ordering because their own internal demand forecasts, built on committed hyperscaler contracts, justify multi-year capacity expansion. That distinction separates a cyclical uptick from a structural commitment.

The Futurum Group AI capex forecasts for 2025-2026 place aggregate spending commitments from the five largest US cloud and AI infrastructure providers approaching $700 billion, a scale that contextualises why chipmakers and equipment suppliers are treating this cycle as a multi-year structural commitment rather than a single-year demand spike.

When big ASX news breaks, our subscribers know first

IBM’s 25% collapse and the fixed-budget problem

The mechanism that crushed IBM’s share price is more important than the share price move itself. Understanding it changes how you evaluate every software holding in a technology portfolio.

Enterprise IT budgets are not expanding to accommodate AI. They are being reallocated within roughly fixed envelopes. Money that previously went to software licences, consulting engagements, and cloud platform subscriptions is being redirected toward AI servers, accelerators, and the infrastructure required to run large-scale AI workloads. IBM disclosed this directly: its customers told it, in effect, that the software line item was where the cuts were coming from.

The current AI investment cycle has already surpassed every prior technology spending peak as a share of US GDP, with combined hyperscaler capex commitments for 2026 sitting in the $600-$805 billion range, a scale of commitment that makes the fixed-budget reallocation pressure IBM described structurally inevitable rather than anecdotal.

AI spending is not being layered on top of what enterprises already commit to technology. The existing envelope is simply being carved up differently.

That disclosure landed hard. On 14 July 2026, IBM stock closed at $217.07, down 25.21%, with 67.44 million shares changing hands. The volume figure is the detail worth pausing on. That level of turnover is not retail panic. It is institutional holders exiting in size, repricing IBM based on a structural reassessment of where its revenue sits in the spending hierarchy.

Why IBM’s business model sits at the wrong end of the reallocation

IBM has spent years repositioning around higher-margin hybrid cloud and software revenue. That strategy made sense in a world where enterprise software budgets were stable or growing. It becomes a vulnerability when those budgets are precisely the pool that enterprise CFOs treat as cuttable to fund urgent AI capex.

The budget vulnerability IBM exposed runs deepest in vendors still dependent on per-seat pricing models, where AI-native competitors are entering enterprise markets at 80-90% lower cost points, converting the pricing structure itself into a structural liability rather than a stable revenue floor.

This is not an IBM-specific execution failure. The disclosure weighed on other enterprise software peers, confirming that the budget reallocation dynamic extends across the category. The pattern is also consistent with history. Early-cycle technology transitions, from mainframes to client-server to private cloud, have consistently crowded out other IT line items before total budgets eventually expand. The first phase rewards the infrastructure layer. The software layer absorbs the cost.

Understanding the AI stack: where spending flows and where it stalls

The ASML and IBM results map neatly onto a framework that every technology investor now needs. The AI stack, meaning the layers of technology required to build and deploy AI systems, is not receiving capital evenly. Understanding which layer a company occupies determines whether the current spending environment is a tailwind or a headwind.

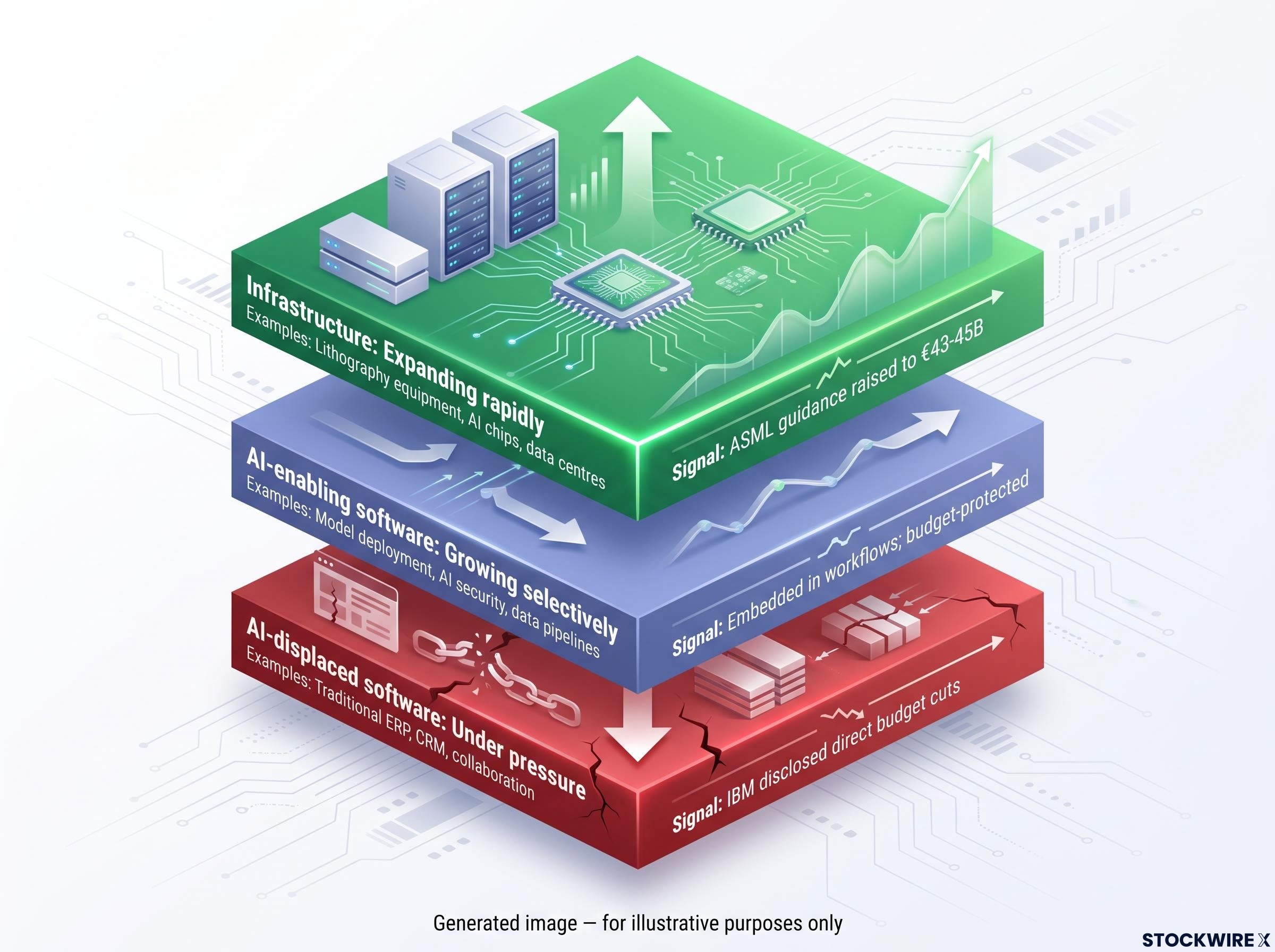

The stack breaks into three categories:

- Infrastructure layer: semiconductor equipment makers, advanced fabs and foundries, AI accelerators and custom silicon, data centre build-out (networking, power, cooling). This is where capital is flowing most aggressively.

- AI-enabling software: model deployment platforms, AI security tools, data engineering pipelines. Software that is necessary to make AI infrastructure productive. These are budget winners, not donors.

- AI-displaced software: traditional enterprise software (ERP, CRM, collaboration tools) and IT services not explicitly tied to AI workflows. These are the budget line items being cannibalised.

The infrastructure layer’s advantage is not simply that it sits upstream in the supply chain; it is that companies resolving binding constraints on AI deployment, whether power availability, cooling density, or grid interconnection timelines, occupy positions that are structurally difficult to commoditise in the way that software licences are not.

| Stack layer | Budget trend | Example type | Current demand signal |

|---|---|---|---|

| Infrastructure | Expanding rapidly | Lithography equipment, AI chips, data centres | ASML guidance raised to €43-45B |

| AI-enabling software | Growing selectively | Model deployment, AI security, data pipelines | Embedded in AI workflows; budget-protected |

| AI-displaced software | Under pressure | Traditional ERP, CRM, collaboration | IBM disclosed direct budget cuts from customers |

This classification is not academic. It determines whether an investor holding a broad tech ETF is net long or net short the current phase of the AI cycle, even if that ETF carries both infrastructure and software names. Most technology funds mix these exposures without distinguishing between them. The hidden bet inside those holdings is now visible, and it runs in opposite directions depending on where the weight sits.

How to audit a tech portfolio for AI spending exposure

The framework above becomes useful only when applied to actual holdings. The process takes three steps:

- Classify the stack position. For each technology holding, determine whether it primarily sells infrastructure inputs to AI (equipment, chips, data centres), sells software that is necessary for AI deployment and orchestration, or depends on enterprise software budgets that are under reallocation pressure.

- Assess the budget direction. Ask whether the company’s revenue line is receiving reallocated AI capital or donating it. IBM’s disclosure is the specific prompt to scrutinise software holdings for implicit assumptions about budget stability.

- Evaluate whether the current valuation reflects that reality. If a software holding’s valuation still prices in growth rates that assume stable or expanding enterprise software budgets, the IBM result is a direct challenge to that assumption. The investor needs to decide whether the company has a credible AI-enabler narrative or not.

On the infrastructure side, the case is strong but not without risk. ASML’s raised multi-year guidance validates the overweight thesis, but semiconductor capital equipment is historically among the most volatile sectors when capacity overshoots demand. Positioning for the infrastructure cycle requires sizing positions with the expectation of sharp pullbacks, even within a structurally favourable trend.

Hyperscaler capex as an early-warning system: Track quarterly capital expenditure guidance from AWS, Azure, Google Cloud, and Meta. Sustained or rising AI-related capex supports the infrastructure trade and increases the odds that budget pressure on software persists. A pronounced capex slowdown would be the first signal to reassess exposure on both sides.

On the software side, the right response is not wholesale exit. It is triage. Prioritise names embedded in AI workflows or genuinely mission-critical regardless of AI spending trends. Scrutinise those whose growth assumptions were built in a pre-AI budget environment.

The next major ASX story will hit our subscribers first

Three scenarios that could change this picture

The bifurcation thesis is supported by this week’s evidence. It is not guaranteed to persist. Three scenarios could reverse or soften it.

Budget expansion. If AI deployments begin generating clearly measurable productivity gains, enterprises may increase total IT budgets rather than simply reallocating within them. Historical precedent supports this possibility: prior technology transitions saw initial crowding-out followed by later budget expansion as productivity gains materialised. If that pattern repeats, the pressure on software names eases.

Infrastructure overbuild. If AI capacity is over-provisioned relative to realised workloads, equipment and chip orders could slow sharply, reversing the infrastructure trade even as the long-term AI trend remains intact. ASML management has flagged tariffs and export controls as macro constraints on converting demand into revenue, adding a layer of policy risk to the capacity expansion thesis.

Software repositioning. Some enterprise software vendors will integrate AI in ways that make them central to AI value capture, converting from budget donors into budget winners. At that point, stock-level analysis becomes more important than category-level analysis.

What to monitor between now and the next earnings cycle

The bifurcation thesis is confirmed or challenged by recurring data, not a single week’s events. Three indicators form the monitoring framework:

- Earnings call commentary: management language from both infrastructure and software companies on budget dynamics, order visibility, and customer AI adoption

- Valuation multiple movements: shifts in multiples for high-growth software names as the market digests the reallocation theme

- Hyperscaler capex guidance: quarterly capital expenditure disclosures from the major cloud platforms as the upstream signal for both sides

The next major hyperscaler capex disclosures, ASML’s next order book update, and the next wave of enterprise software earnings are the data points that will either reinforce or complicate this framework. The cadence of monitoring matters as much as the current signal.

Positioned for the phase you are actually in, not the one you assumed

Being “in tech” is no longer a sufficient description of a portfolio’s AI exposure. ASML’s raised guidance to €43-45 billion and IBM’s institutional selloff on 67.44 million shares at a 25.21% decline are not two separate stories. They are the same story told from two positions in the supply chain. The portfolio implication runs in the same direction from both ends: the infrastructure layer is capturing the capital, and the traditional software layer is funding it.

Both signals are forward-looking. The raised guidance reflects professional capital being committed to AI infrastructure years in advance. The institutional-scale selloff reflects professional capital exiting a structural position it no longer believes in. Together, they represent one of the clearest single-week illustrations of the AI spending reallocation dynamic visible in public market data.

The investor posture this warrants is granular, stack-aware analysis applied now, monitored against the three leading indicators outlined above, and held with the understanding that this is a phase of the AI cycle, not its permanent state. The framework, the audit process, and the monitoring indicators give you a repeatable process for staying positioned through the current phase while watching for the transition signals that will define the next one.

For investors wanting to translate the stack classification framework into an actual allocation, our dedicated guide to AI ETF portfolio construction covers a four-layer approach spanning US large-cap platforms, international tech, mid-cap innovators, and infrastructure enablers, with overlap management guidance for existing holdings.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and forward-looking statements are subject to market conditions and various risk factors.