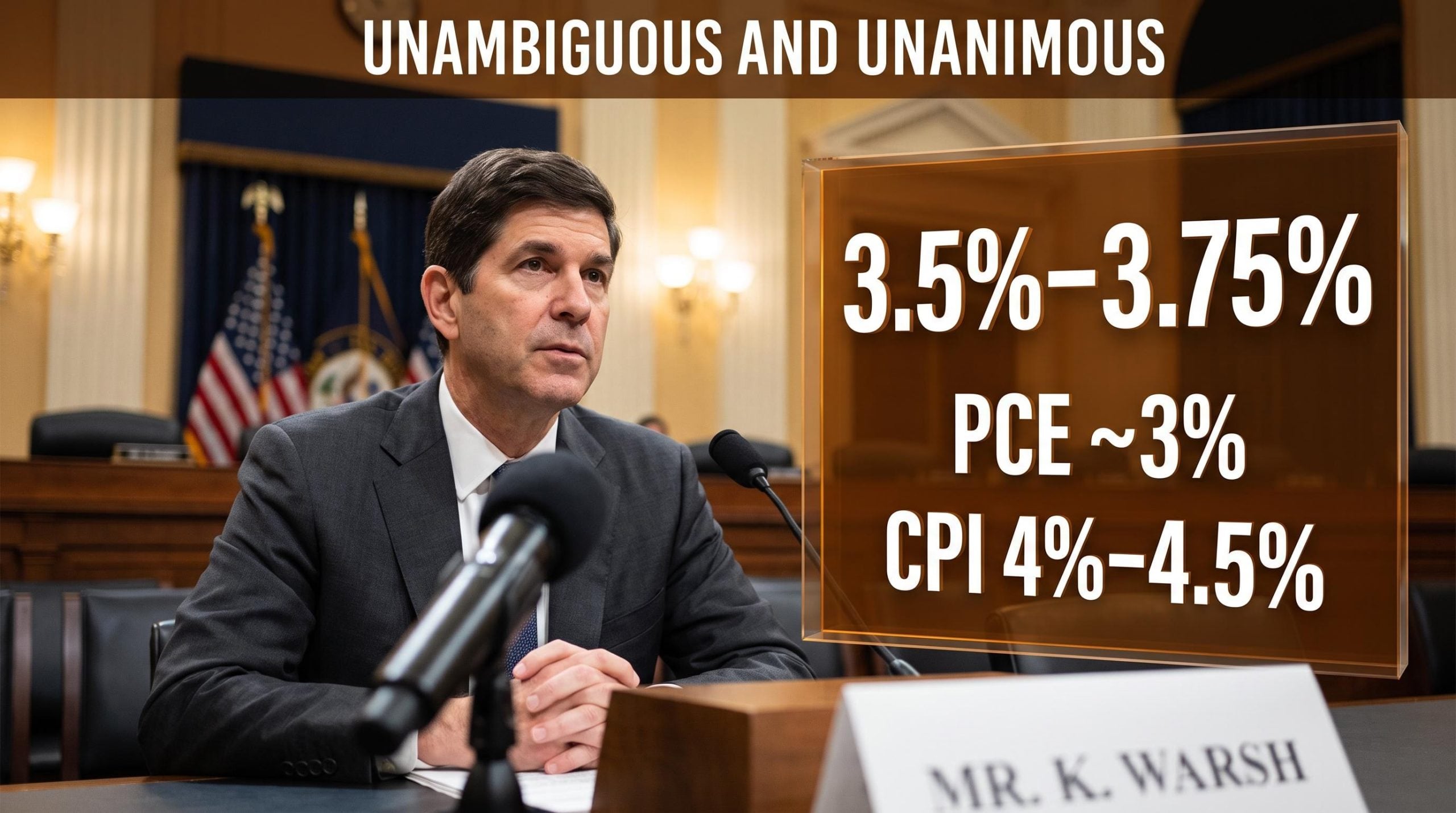

Fed Chairman Kevin Warsh told Congress today that the central bank will not accept inflation above 2%, and that the June rate hold at 3.5%-3.75% is not a prelude to easing. The message was direct, specific, and left almost no room for interpretation.

Warsh’s 14 July 2026 appearance before the House Financial Services Committee was his first testimony before that body. It confirmed what his June press conference suggested: this is a Federal Reserve defined by inflation intolerance, not market accommodation. The “higher for longer” framework is no longer a hedge. It is the base case.

Warsh’s confirmation into a 3.8% CPI environment shaped the inflation-intolerance mandate that today’s testimony codified; a Fed chair who inherited that specific inflation inheritance has little institutional latitude to frame a hold as anything resembling patience.

Here is what that posture means for your portfolio right now, across equities, fixed income, and real assets, with a clear map of the data points that would need to shift before anything changes.

What Warsh told Congress, and why his phrasing matters

Delivering his first congressional testimony as Fed chairman to the House Financial Services Committee, Warsh confirmed that the Federal Open Market Committee (FOMC), the Fed’s rate-setting body, kept the federal funds rate within a target band of 3.5%-3.75% at its 17 June 2026 meeting. The decision was unanimous.

What matters more than the hold itself is the language Warsh chose to describe it.

The committee is “unambiguous and unanimous” in its commitment to delivering price stability.

That phrasing is not standard central banker hedging. “Unambiguous” closes the interpretive gap. “Unanimous” removes any suggestion of internal dissent. Warsh also stated explicitly that the Fed will not be comfortable with an inflation objective above 2%, and pushed back directly on political pressure for rate cuts, framing the Fed’s independence as non-negotiable.

The precision here is deliberate. The words a Fed chair uses in congressional testimony carry forward into market pricing for months. By narrowing the interpretive space this aggressively, Warsh is telling rate markets that the hold is not a soft pivot and should not be modelled as one. If you have been positioning for near-term cuts, today’s testimony is the clearest signal yet to update that assumption.

When big ASX news breaks, our subscribers know first

Where the U.S. economy actually stands right now

In Warsh’s telling, the economy is progressing at a solid clip, and examining each major sector in turn explains why the Fed feels no compulsion to ease policy.

Consumer spending is growing at a measured pace. Industrial production has been climbing steadily across 2026. Employment conditions are holding up well, with hiring broadly matching the pace of workforce expansion and the jobless rate showing little meaningful movement. No clear recession signal is present.

Residential real estate is the outlier, continuing to underperform relative to every other major sector, weighed down by the same elevated rate environment that the Fed shows no inclination to relieve.

| Sector | Current trajectory | Rate sensitivity | Warsh commentary signal |

|---|---|---|---|

| Consumer spending | Growing at a measured pace | Moderate | Supports hold rationale |

| Manufacturing | Trending upward in 2026 | Moderate | Bright spot cited |

| Labour market | Balanced; steady unemployment | Low (currently) | No recession signal |

| Residential real estate | Underperforming | High | Acknowledged drag |

Inflation remains the defining constraint

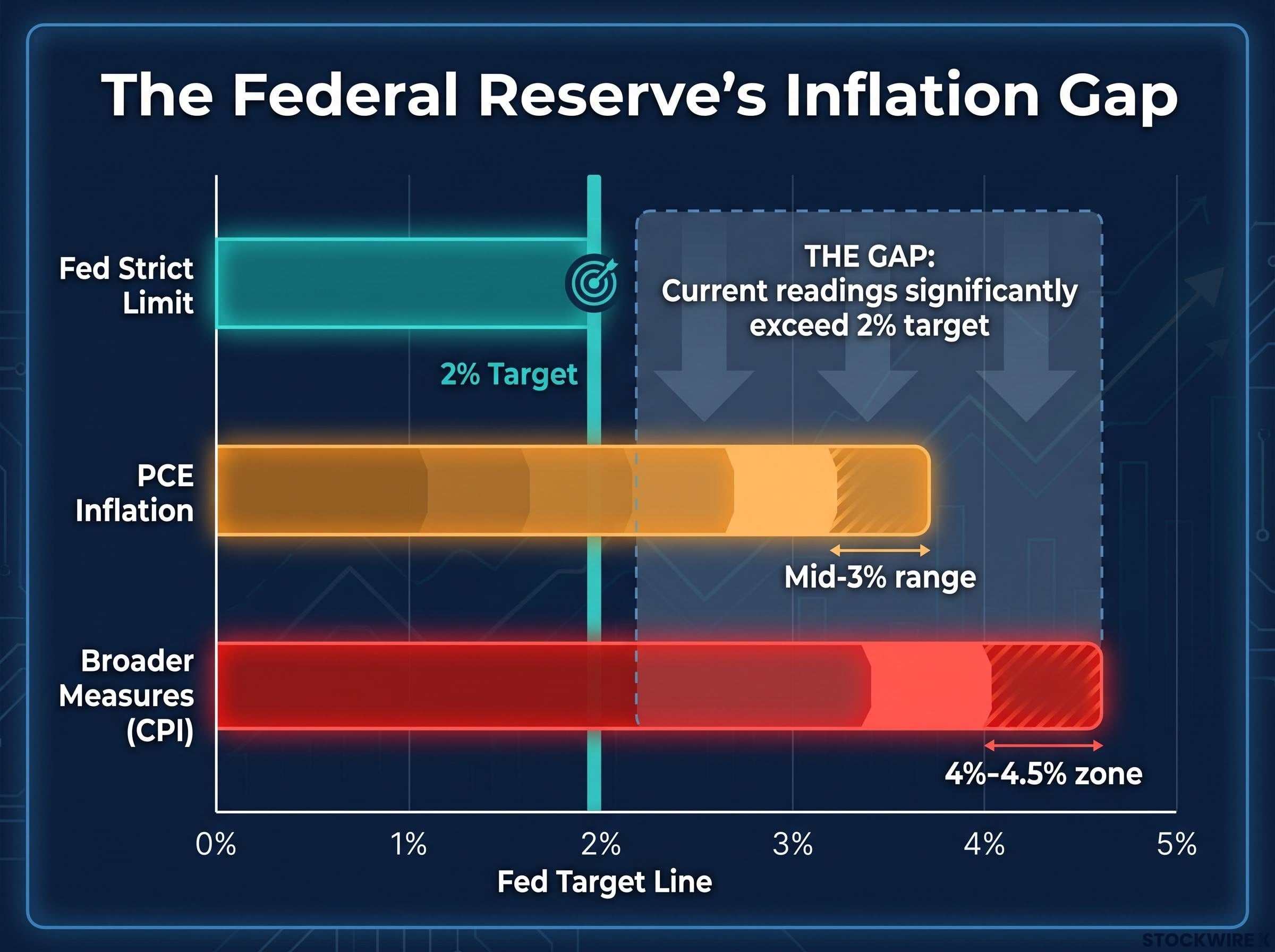

Some inflation measures have cooled modestly, but the operative fact has not changed. Personal Consumption Expenditures (PCE) inflation, the Fed’s preferred gauge, is running around the mid-3% range according to research estimates, with broader measures sitting in the 4%-4.5% zone. Both remain materially above the 2% target.

Core PCE readings through May 2026 held at 3.4% year-over-year, sitting 140 basis points above the Fed’s target and providing the precise data backdrop that made Warsh’s zero-tolerance language at today’s hearing structurally unavoidable rather than rhetorical.

A labour market that is not breaking and inflation that is not breaking toward 2% is exactly the combination that gives the Fed no reason to ease. That dynamic is the structural reason this hold was inevitable, and it tells you which sectors carry macro tailwinds (cyclicals, industrials) and which carry the full weight of the rate environment (housing, mortgage-exposed financials).

What “higher for longer” means across asset classes

The rate hold reshapes risk and return across every major asset class. Here is the map.

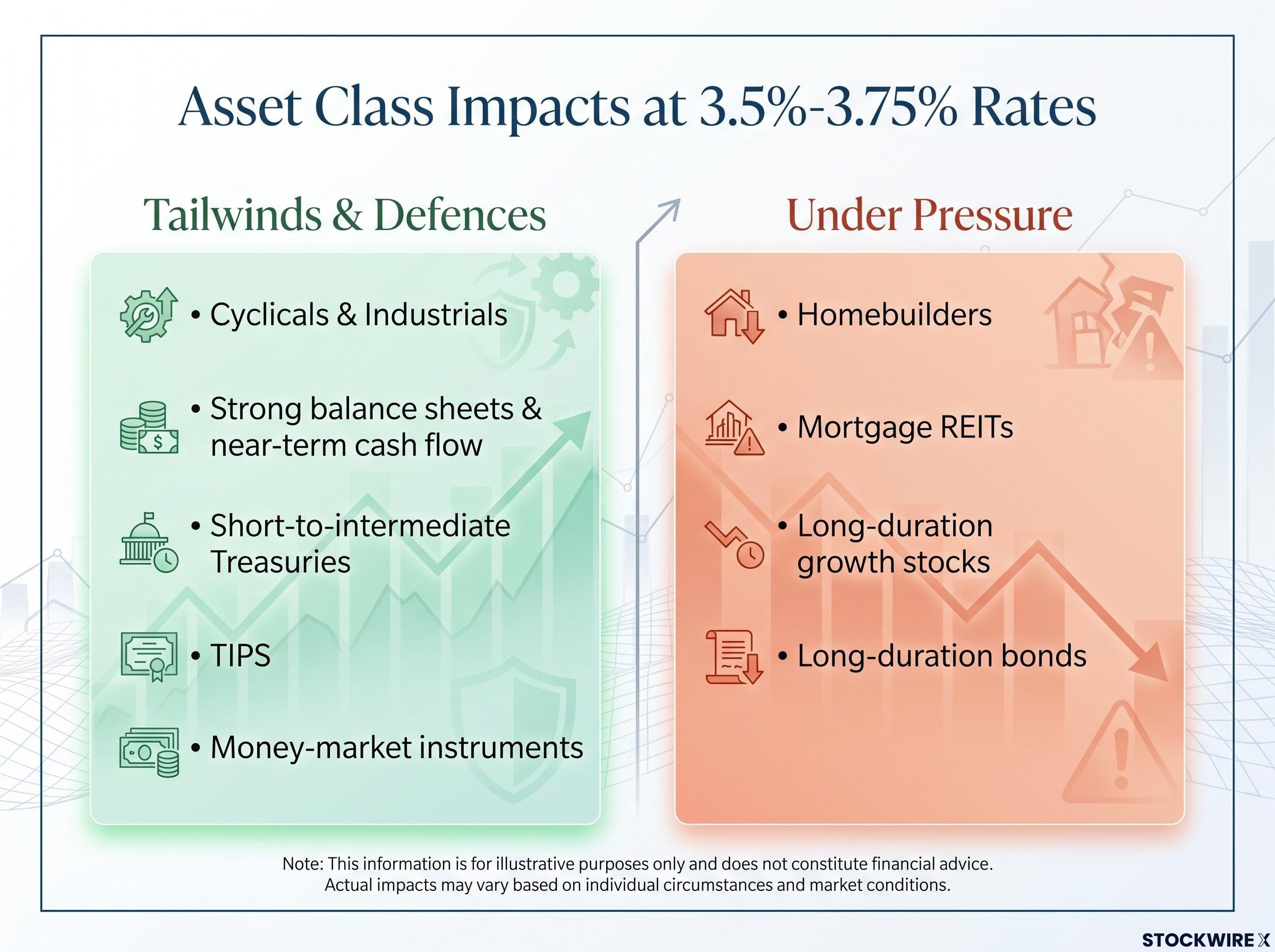

Equities: quality and cyclicals over rate-sensitive names

A still-growing economy with no recession signal supports earnings for broad cyclicals and industrials. The pressure falls on the other side of the ledger:

- Sectors with relative tailwinds: cyclicals, industrials, and companies with strong balance sheets and near-term cash flow generation.

- Sectors under pressure: homebuilders, mortgage REITs (real estate investment trusts that hold mortgage-backed assets), and richly valued long-duration growth stocks whose cash flows sit years in the future.

The 3.5%-3.75% policy rate sustains financing costs that directly compress margins for rate-sensitive businesses. Favour balance-sheet strength and cash flow generation over speculative growth.

Fixed income and real assets: shorten duration, keep inflation hedges

A meaningful share of FOMC members expect at least one rate hike by year-end 2026, according to the latest dot plot projections.

That asymmetry matters. Long-duration bonds face outsized risk if inflation surprises to the upside; short-to-intermediate Treasuries and high-quality credit offer more attractive risk-adjusted carry with less sensitivity to hawkish surprises.

TIPS (Treasury Inflation-Protected Securities, bonds whose principal adjusts with inflation) and select commodities retain a role as portfolio ballast while inflation remains elevated. Meanwhile, money-market instruments yielding meaningfully above zero at the current policy rate make cash a productive position, not idle insurance.

The dot plot’s tilt toward potential hikes rather than cuts means that if you have been holding long-duration equity or bond positions on the assumption the Fed will blink, you are carrying a risk the market has not fully priced.

The Fed independence signal and why investors should treat it as structural

Warsh’s explicit pushback on political pressure for rate cuts is not a political aside. It is a durable investment signal about how the Fed’s policy reaction function will behave under stress.

The message is straightforward: the policy path will be driven by inflation and labour data, not by market discomfort or political demands. The Fed will remain independent.

Why the “Fed put” repricing changes the risk calculus

The “Fed put” is the historical investor assumption that the Fed will step in and ease aggressively if markets fall hard enough, effectively putting a floor under asset prices.

Under Warsh, that put is much further out of the money, a characterisation that emerged in market commentary after his debut. In practical terms, this means higher required equity risk premiums, reduced justification for aggressive leverage, and the need to stress-test portfolios against a scenario where the Fed simply does not intervene during a meaningful sell-off.

The Fed put repricing Warsh has engineered operates alongside a parallel dynamic in fiscal policy, where the Trump put faces the same self-suppression paradox: market confidence in a backstop suppresses the very fear signals that would need to materialise before any policy reversal occurs.

If you have implicitly built a Fed rescue assumption into your risk models, Warsh has materially shifted the terms. The downside scenario in a market correction is now wider than it was under previous chairs, and portfolios calibrated to a more accommodative backstop need to account for that.

The next major ASX story will hit our subscribers first

What the data will need to show before anything changes

The policy path from here is entirely data-dependent. Two conditions would need to shift before the Fed’s posture plausibly moves:

- PCE inflation: Must move convincingly toward 2%. The mid-3% readings still in place leave no room for the Fed to declare progress sufficient. Each monthly release is the single most important data point for rate expectations.

- CPI (Consumer Price Index): Broader price measures in the 4%-4.5% range reinforce the Fed’s caution. A sustained decline across multiple CPI prints would be required to shift the narrative.

- Non-farm payrolls: A material deterioration in job creation, moving beyond the current balanced state, would be the second trigger. As long as employment holds, the Fed has cover to stay restrictive.

The dot plot signals hikes are more likely than cuts at present. The asymmetric risk is to the upside on rates, not the downside. Each monthly inflation or jobs print between now and the next FOMC meeting is effectively a referendum on whether Warsh’s hold becomes a hike, and positioning ahead of those releases should reflect that asymmetry.

Mapping Warsh’s Fed: the framework investors carry forward from 14 July

Warsh’s inaugural testimony crystallised three durable takeaways: the inflation zero-tolerance posture is institutional, not personal; the rate hold is not a pivot signal; and the “Fed put” has been repriced to a more distant strike.

The portfolio construction principles that follow from those takeaways are specific:

- Equities: favour quality, balance-sheet strength, and cash flow generation over rate-sensitive and long-duration growth names.

- Fixed income: shorten duration; emphasise high-quality credit and inflation-protected securities.

- Cash and real assets: treat money-market yields as a genuine return source and maintain inflation hedges as structural holdings, not tactical trades.

The next PCE and jobs reports are the first tests of whether the hold extends through the next FOMC cycle or escalates into a hike. Those releases are where the market’s conversation with Warsh’s Fed continues, and they deserve the same attention you gave today’s testimony.

For investors ready to translate Warsh’s hold into specific allocation decisions, our dedicated guide to portfolio positioning in high-rate environments covers the five-step framework for staying invested across equities, bonds, and property without depending on a rate pivot that may not arrive.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.