3 ASX Tech ETFs That Target What the ASX 200 Misses

1 hr ago

A company with no dividends, a triple-digit price-to-earnings ratio, and no guarantee of future profit can still command a multi-trillion-dollar market valuation. The question is why any rational investor would buy it. Millions of investors hold growth stocks without fully understanding the mechanics, risk profile, or trade-offs embedded in the investment. The gap between buying a growth stock and understanding one is wide, and expensive to ignore. What follows is a complete explanation of what growth stocks are, why their valuations work the way they do, what structural risks they carry, and how real companies like Amazon and Nvidia illustrate those dynamics in practice.

Most investors associate growth stocks with technology companies or fast-rising share prices. That intuition is partially correct, but it misses the structural mechanics that distinguish a growth stock from any other equity category.

Growth stocks are shares in companies projected to expand revenue and earnings at rates meaningfully exceeding broader market averages. The returns on these investments arrive exclusively through capital appreciation, not income. That distinction matters because it shapes the investor’s only path to profit: selling shares at a higher price than they were purchased.

Growth companies reinvest accumulated earnings back into the business, funding research, product development, and market expansion, rather than distributing profits to shareholders as dividends. The reinvestment decision is deliberate. It reflects management’s belief that every dollar returned to shareholders is a dollar not compounding within the business.

These companies appear across all sectors and exchange sizes, though they cluster most visibly in innovation-intensive industries where proprietary technology, patents, or platform advantages create durable competitive positioning. Both small-cap explorers and multi-trillion-dollar mega-caps can qualify.

Four structural characteristics define a growth stock:

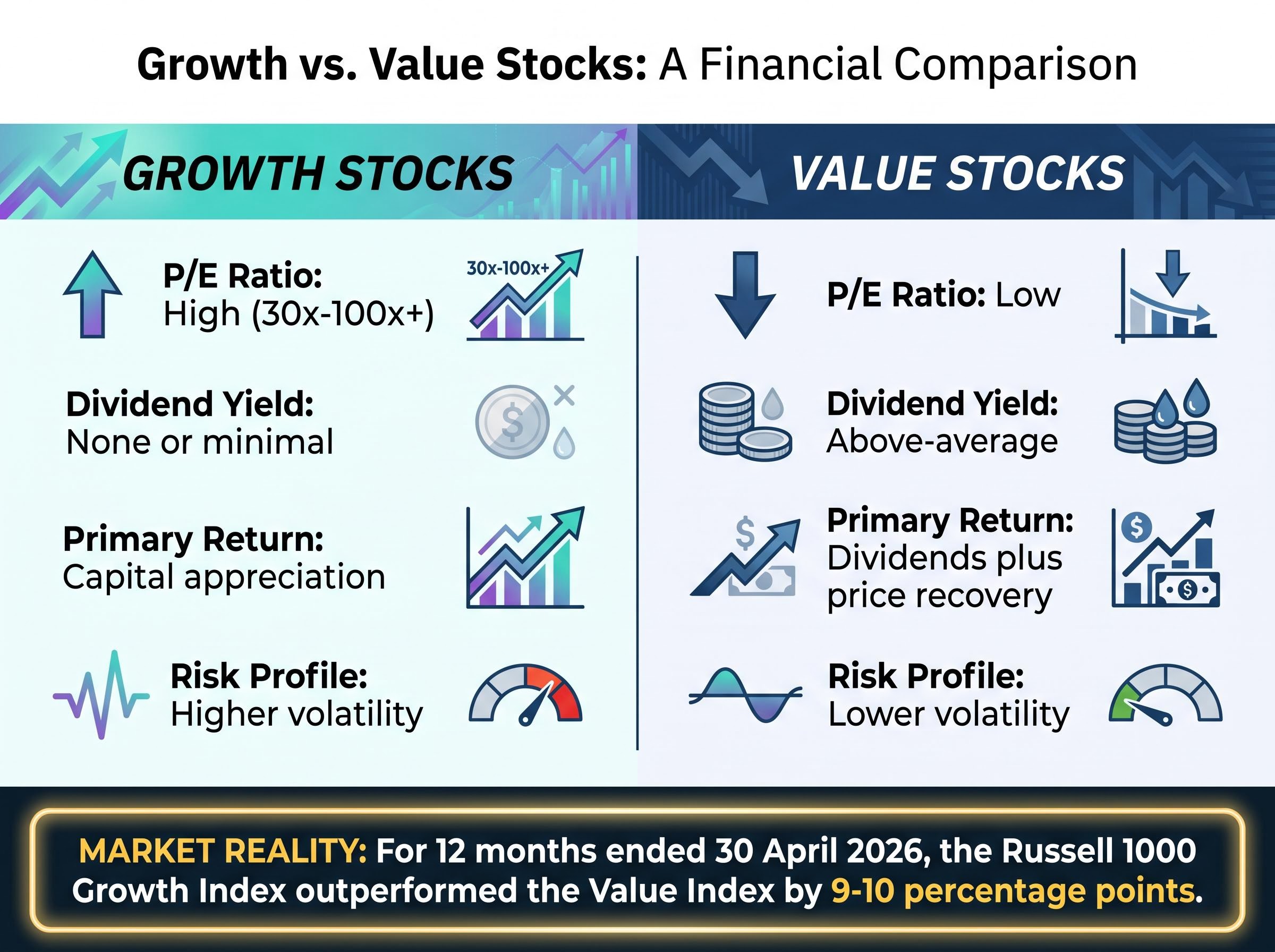

High P/E ratios on growth stocks are not irrational. They reflect the market pricing in anticipated future earnings rather than current earnings.

A company reporting minimal profits today can carry a high P/E legitimately if investors believe its earnings trajectory will catch up to, and eventually exceed, the premium paid. The valuation is forward-looking by construction. Investors are not paying for what the company earns now; they are paying for what they believe it will earn over the next five, ten, or twenty years.

Growth and value investing represent genuinely contrasting worldviews about where investment value resides. One camp pays a premium for future earnings expansion. The other looks for companies the market has underpriced relative to their current fundamentals.

Growth investors accept elevated P/E ratios because they believe the company’s expansion rate will justify the premium over time. Value investors seek low P/E and low price-to-book (P/B) ratios, targeting companies whose current assets or earnings power exceed what the share price implies. The metrics each camp uses to evaluate the same stock can produce opposite conclusions.

Dividends serve as a structural differentiator. Value stocks generally offer above-average dividend yields, providing investors with income during the holding period. Growth stocks characteristically pay nothing until the investor sells. That difference changes the risk calculus: a value investor receives partial compensation for waiting, while a growth investor receives none.

Neither approach is universally superior across all market cycles. Many investors hold both simultaneously for diversification purposes, blending forward-looking appreciation potential with current-income stability.

The value investing framework uses precisely these metrics in reverse: a P/E below 15, a price-to-book ratio below 1.5, and a free cash flow yield above 5% are the screening thresholds that value investors apply where growth investors would walk away, which is why the two camps can look at the same stock and reach opposite conclusions about whether it is attractively priced.

For the 12 months ended 30 April 2026, the Russell 1000 Growth Index outperformed the Russell 1000 Value Index by approximately 9-10 percentage points, per FTSE Russell index data. Morningstar’s style-box data for the same period shows directionally consistent but slightly different figures, reflecting methodology differences across providers.

| Characteristic | Growth stocks | Value stocks |

|---|---|---|

| Typical P/E ratio | High (often 30x-100x+) | Low (often below market average) |

| Dividend yield | None or minimal | Above-average |

| Basis of valuation | Projected future earnings growth | Current fundamentals and assets |

| Primary return mechanism | Capital appreciation (selling at higher price) | Dividends plus price recovery |

| Risk profile | Higher volatility; no income cushion | Lower volatility; dividend income as buffer |

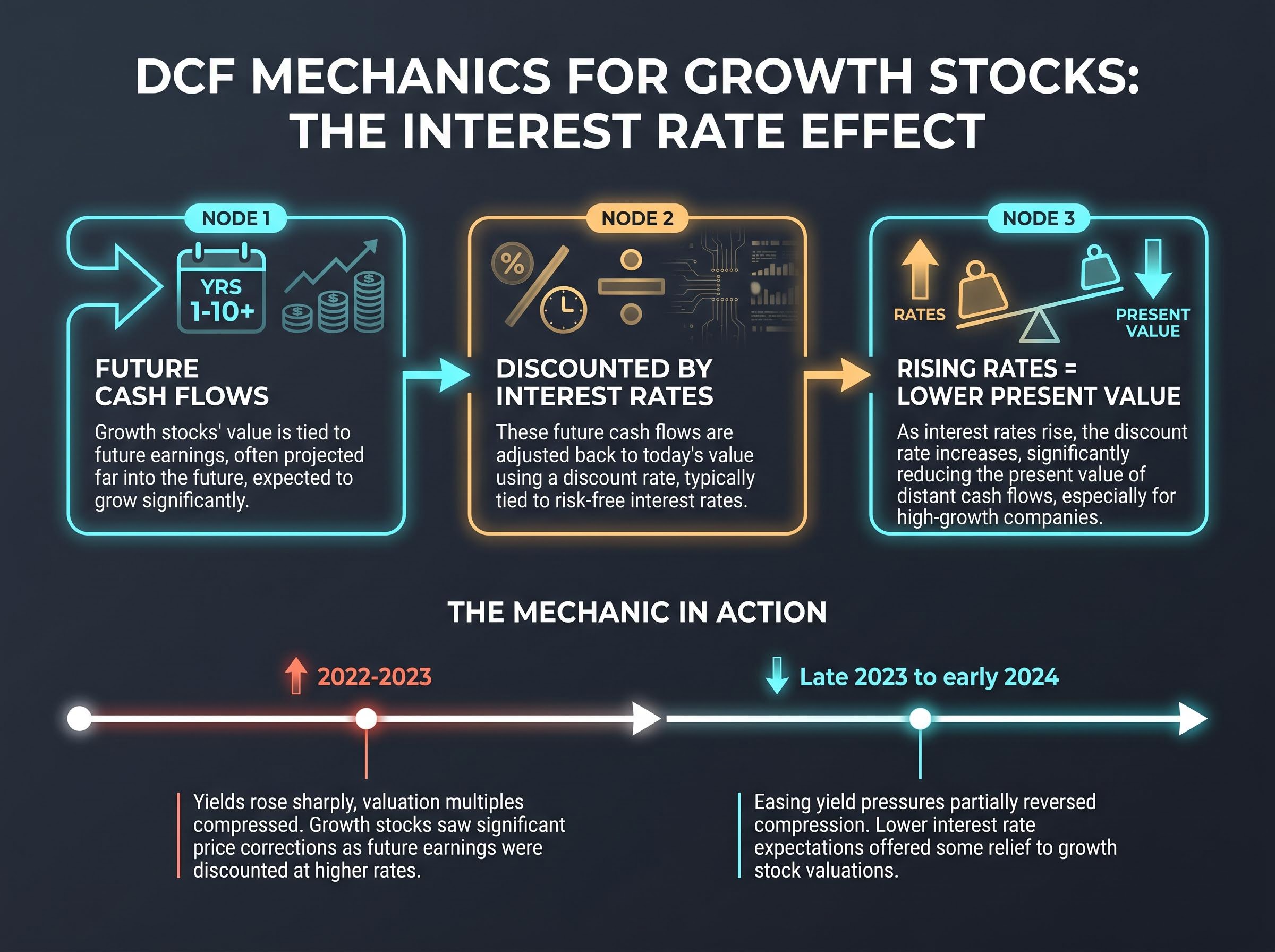

The premium investors pay for a growth stock is not arbitrary. It follows a specific financial logic called discounted cash flow (DCF), a method of estimating what a company’s future earnings are worth in today’s terms.

The mechanic works in three steps:

The peer-reviewed DCF research on interest rate sensitivity published by Killins, Johnk, and Egly formalises the mechanism informally described by market commentators: as discount rates rise, the present value of cash flows expected far in the future falls disproportionately relative to near-term cash flows, making long-duration equities structurally more exposed than shorter-duration assets.

This means a growth stock’s share price can fall without any deterioration in the underlying business. A rate increase compresses the present value of the future earnings the market had already priced in.

As Bloomberg reported in January 2024, high-multiple growth stocks are “highly sensitive to changes in the discount rate because much of their cash flow lies far in the future.” Reuters, in March 2024, explicitly linked lower yields to higher valuations for growth names through discounted-cash-flow mechanics, noting growth stocks remain vulnerable if yields reverse course.

According to Morningstar (June 2024), growth equities trade at a premium relative to long-term fair value estimates, with the premium most pronounced in technology and communication services, and “higher real yields continue to pose a key risk for growth valuations.”

The mechanic played out in real time across 2022-2024. When yields rose sharply in 2022-2023, valuation multiples on growth stocks compressed across the board. The Wall Street Journal (April 2024) described how growth stocks with the richest valuations sold off on days when 10-year Treasury yields spiked, with many investors viewing leading growth franchises as “priced for perfection.”

Easing yield pressures in late 2023 to early 2024 partially reversed that compression, demonstrating the mechanic working in both directions.

Equity duration and yield sensitivity vary significantly across sectors: the IMF has estimated that a 100 basis point rise in global long-term real rates lowers the equilibrium price-to-earnings ratio of advanced-economy indices by 10-15% with earnings held constant, which explains why the 2022-2023 yield spike compressed growth multiples so sharply even as many of the underlying businesses continued growing.

The OECD Economic Outlook (May 2024) warned that persistent uncertainty about the path of policy rates creates ongoing valuation risk for long-duration assets such as growth equities, a risk that remains relevant regardless of which direction rates move next.

The most immediate risk is the simplest one. If the anticipated growth does not materialise, investors who paid a premium have no dividend income to cushion the loss and no recovery mechanism except waiting for a turnaround that may never come.

Consider a biotech company pursuing an unproven drug candidate. If regulatory approval is denied or the treatment proves ineffective, years of research and development expenditure may yield no return. The stock may never reach its projected value. The outcome is binary for the company and for the shareholder.

That company-specific risk is only the first layer. A second, less visible risk is valuation stretch: the possibility that a growth stock’s price can decline even while its earnings hold steady, simply because the market decides the multiple it assigned was too generous. According to Barron’s (August 2024), “the margin of safety is thin because valuations already discount optimistic growth and benign rate scenarios” for mega-cap growth stocks. The Financial Times (October 2024) noted that earnings revisions had been positive for leading growth stocks, yet price gains outpaced fundamentals, raising concerns about valuation mean reversion.

The third layer is the macro-level interest-rate sensitivity detailed in the previous section, where rising rates compress present value regardless of company performance.

Three distinct risk layers apply to any growth stock position:

Sophisticated institutional investors disagree on how stretched current valuations are. Jeremy Grantham of GMO, as summarised by the Financial Times (January 2024), described mega-cap growth as a “superbubble” with poor prospective long-term returns even for fundamentally strong companies. Rob Arnott of Research Affiliates argued in Barron’s (June 2024) that growth stocks are priced at extreme premiums to value, reminiscent of past episodes that preceded years of value outperformance.

Goldman Sachs, in its “US Equity Outlook 2025”, described growth valuations as “full but not universally in bubble territory,” recommending a focus on profitable, cash-generating growth companies rather than unprofitable high-multiple names.

The disagreement itself is informative. Even the most constructive institutional views carry conditions.

Current growth stock valuations have swung from one extreme to the other: Morningstar data from March 2026 placed growth equities at a 21% discount to fair value, a level recorded less than 5% of the time since 2011, driven by technology sector losses in names including Nvidia, Meta, and Microsoft, illustrating how quickly the same multiple expansion that creates paper gains can reverse.

The abstract mechanics become concrete when applied to companies investors actually own.

Amazon has carried the structural characteristics of a growth stock for over two decades: persistently elevated P/E ratios, no dividends, and market capitalisation growth driven entirely by investor belief in future earnings expansion. From September 2021 through December 2023, Amazon’s P/E ratio ranged between approximately 51x and 245x, according to Macrotrends data. As of mid-May 2026, its trailing P/E sits at approximately 50x (Morningstar reports low-50s; Yahoo Finance reports high-40s, reflecting methodology differences). Its market capitalisation exceeds US$2 trillion, ranking it approximately 4th-5th among U.S.-listed companies.

Analyst growth estimates for Amazon in 2024 exceeded 33%, per Yahoo Finance historical estimates. Investors who bought at high multiples years ago were betting on exactly this kind of sustained expansion.

Nvidia represents the current cycle’s most prominent growth stock. The Financial Times (February 2024) called Nvidia “the poster child of the current growth and AI trade,” citing explosive revenue growth from AI chips, high reinvestment in research and development, and valuation multiples reflecting future demand assumptions rather than current earnings alone.

The Wall Street Journal (May 2024) described Nvidia as “a quintessential growth stock whose valuation hinges on future AI demand.”

| Metric | Amazon (AMZN) | Nvidia (NVDA) |

|---|---|---|

| Approximate trailing P/E (mid-2026) | ~50x | High (varies by quarter) |

| Dividend policy | No dividend | Minimal dividend |

| Primary growth driver | Cloud (AWS), advertising, e-commerce scale | AI chip demand, data centre expansion |

| Key valuation risk | Cloud growth deceleration; margin pressure | AI capex cycle slowing; customer concentration |

Neither case proves growth investing works in general. Both illustrate the upside case, which is precisely what makes them instructive about the category’s structure rather than its guaranteed outcomes.

For investors who want to move beyond the category-level analysis above into specific AI stock decisions, our dedicated guide to AI stock selection breaks down a three-tier framework spanning hardware, cloud, and software, examines how J.P. Morgan, BlackRock, Goldman Sachs, and Morgan Stanley each allocate across those tiers, and explains why NVIDIA, Microsoft, and Palantir carry structurally different risk profiles despite all being classified as growth stocks.

The question an investor needs to answer before buying a growth stock is not “is this a good company?” It is: “is the growth already priced in, and what happens to my investment if that growth is delayed or lower than expected?”

Four questions provide a practical evaluation framework:

Selectivity matters. T. Rowe Price, in its January 2024 growth-equity outlook, stated that attractive opportunities remain in select secular growers, especially in cloud, AI, and healthcare innovation, but warned that overall growth valuations are above long-term averages, requiring “more selectivity and a stronger focus on earnings durability.”

Fidelity Investments’ strategists said in their 2024 equity outlook that “the easy money in the growth trade may be behind us” after sharp multiple expansion in 2023, recommending diversified exposure rather than concentrated bets in the most expensive names.

Cathie Wood of ARK Invest, speaking to Bloomberg in February 2024, argued that innovation-focused growth stocks remain compelling over a 5-year horizon for investors willing to tolerate large drawdowns and hold through cycles.

Combining growth and value stocks within a portfolio addresses the income gap that growth-only positions leave and reduces sensitivity to any single interest-rate environment. Value holdings provide dividend income during periods when growth names are compressing, while growth holdings deliver appreciation potential that stable, mature companies typically cannot match.

The appropriate growth allocation varies by time horizon. Long-horizon investors can absorb greater drawdowns and wait for compounding to work. Shorter-horizon investors face more timing risk with high-multiple positions, where a rate shock or earnings miss in the wrong quarter can erase years of accumulated gains.

Growth stocks reward investors who understand the bet they are making. The investment is a forward-looking wager: that a company’s future earnings expansion will justify the premium paid today, and that the interest-rate environment will not compress the valuation before those earnings arrive.

Whether that bet pays off depends on the company’s execution, the rate backdrop, and the price the investor paid at entry. Applying the evaluative framework above, asking what growth rate the P/E implies, how rate-sensitive the valuation is, and whether the company generates cash today, converts a narrative-driven purchase into a structured thesis.

That thesis requires ongoing reassessment. Rates shift. Earnings revisions change. Multiples expand and compress. A growth stock position is never a settled conclusion; it is a forward-looking view that demands updating as conditions move.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Growth stocks are shares in companies expected to expand revenue and earnings at rates well above market averages, returning value solely through capital appreciation rather than dividends. Value stocks, by contrast, trade at low price-to-earnings ratios relative to current fundamentals and typically offer above-average dividend yields as an income buffer while investors wait for price recovery.

Growth stock P/E ratios are high because investors are paying for projected future earnings rather than current profits; the valuation is forward-looking by design, reflecting the belief that the company's earnings trajectory will catch up to and justify the premium paid over a five, ten, or twenty year horizon.

Rising interest rates increase the discount rate used in discounted cash flow models, which reduces the present value of cash flows expected far in the future; because growth stocks derive most of their value from those distant earnings, their share prices can fall significantly even when the underlying business continues to perform well.

Three distinct risk layers apply: company-specific growth disappointment where the projected expansion simply does not arrive; valuation stretch risk where multiples compress even with stable or growing earnings; and macro-level interest-rate sensitivity that compresses the present value of future cash flows regardless of company performance.

Investors should identify what specific growth rate the current P/E implies and whether that rate is realistic, assess how sensitive the valuation is to a 1-2 percentage point rise in interest rates, determine whether the company is currently profitable, and consider what happens to the investment if growth arrives later or lower than the market has priced in.