IBM shares fell roughly 19% in pre-market trading on 14 July 2026, with preliminary Q2 figures landing well short of what Wall Street had expected. It was one of the largest single-session drops in the company’s modern history.

This is not a speculative name. IBM is one of the world’s largest enterprise technology companies, built around high-margin software, hybrid cloud infrastructure, and AI platform revenue. When a company of this scale misses by this much, the question moves beyond one quarter’s numbers. It raises something more uncomfortable: whether the way corporate IT budgets are being allocated has shifted in a way that structurally disadvantages IBM‘s strongest businesses.

Here is what actually drove the miss, why the budget dynamics behind it may not be a one-off, and what specific disclosures to watch on 22 July before drawing any conclusions. The difference between a painful but recoverable timing event and a longer-duration de-rating story comes down to what management says on that call.

A revenue miss driven by a late-quarter spending scramble

The headline numbers landed clearly below consensus. Preliminary Q2 2026 revenue for IBM reached $17.2 billion, falling short of the $17.86 billion that analysts had forecast. Adjusted earnings per share of $2.93 missed the $3.02 consensus figure, while GAAP diluted EPS of $2.27 represented a 2% decline compared with the prior year period.

| Metric | Reported | Consensus |

|---|---|---|

| Q2 2026 Revenue | $17.2B | $17.86B |

| Adjusted EPS | $2.93 | $3.02 |

| GAAP Diluted EPS | $2.27 | N/A |

Context matters here. On a year-over-year basis, total revenue edged higher by approximately 1%, and adjusted EPS rose 5%. This was a miss against expectations, not an absolute decline. But margins told a sharper story: GAAP gross margin declined 100 basis points to 57.7%, while non-GAAP operating gross margin compressed by 70 basis points to 59.4%, pointing to outsized pressure on IBM‘s highest-margin product lines.

First-half 2026 free cash flow: $4.8 billion (against full-year 2025 FCF of approximately $12.2 billion). Net cash from operations: $7.8 billion.

That free cash flow figure is the stabilising detail. $4.8 billion in the first half, measured against a full-year 2025 baseline of $12.2 billion, tells you the underlying cash generation engine has not broken. For any investor trying to calibrate whether this is structural damage or a timing shock, that distinction matters enormously.

When big ASX news breaks, our subscribers know first

Why enterprise IT budgets suddenly moved away from IBM’s strongest businesses

The miss was not caused by customers deciding IBM‘s software or mainframes were no longer worth buying. It was caused by a sudden, reactive scramble for entirely different products that ate through the same fixed quarterly budgets.

Enterprise IT spending allocations tend to be set well in advance within any quarter. When enterprise buyers surged into server, storage, and memory purchases in the final weeks of June, the money had to come from somewhere. It came from planned software renewals and mainframe upgrades, the exact categories where IBM earns its richest margins.

Hyperscaler AI capital expenditure of $725 billion projected for full-year 2026, with a $1 trillion annual run rate trajectory for 2027, is the upstream driver of the memory and server spending wave that flowed into enterprise IT budgets and ultimately displaced IBM’s software renewal pipeline in Q2.

Three dynamics converged simultaneously:

- Fixed budgets, zero-sum allocation. A late-quarter rush to secure high-bandwidth memory (HBM) and DRAM, the fast memory chips that power AI workloads, left no room for planned software renewals and mainframe upgrades.

- IBM’s highest-margin lines absorbed the deferral. Transaction Processing software and IBM Z mainframes carry some of IBM‘s best economics. When those are delayed, the hit to EPS and gross margin is disproportionately larger than the revenue shortfall alone would suggest.

- The trigger was external to IBM. Enterprise buyers were not walking away from IBM‘s offerings. Instead, they were responding to supply anxieties in the memory market, where AI workloads had taken a commanding share of global HBM and DRAM output, pushing companies to stockpile before prices rose further. Cybersecurity incidents throughout the quarter also introduced additional delays to procurement timelines.

Why IBM’s margin mix made the damage worse than the headline suggests

IBM has deliberately shifted its business toward software and services over recent years because those lines carry structurally higher margins than hardware. That strategy has been working: gross margins expanded in 2025 as software grew faster than the rest of the portfolio.

The Q2 spending shift effectively reversed that trend in a single quarter. The parts of IBM that were deferred, Transaction Processing and IBM Z, are not peripheral businesses. They are the engine of IBM‘s margin expansion thesis. When those are the lines that slip, the damage to profitability is outsized relative to the revenue lost.

The most important distinction for investors: this was supply-chain fear in the memory market, not a verdict on IBM‘s software or mainframe competitiveness. That shifts the question from “is IBM losing?” to “how long does this external pressure last?”

Where IBM actually performed well in Q2 2026

The miss dominated the headline, but not every part of IBM struggled. Several segments delivered results that suggest the growth thesis is partially intact even in a difficult quarter.

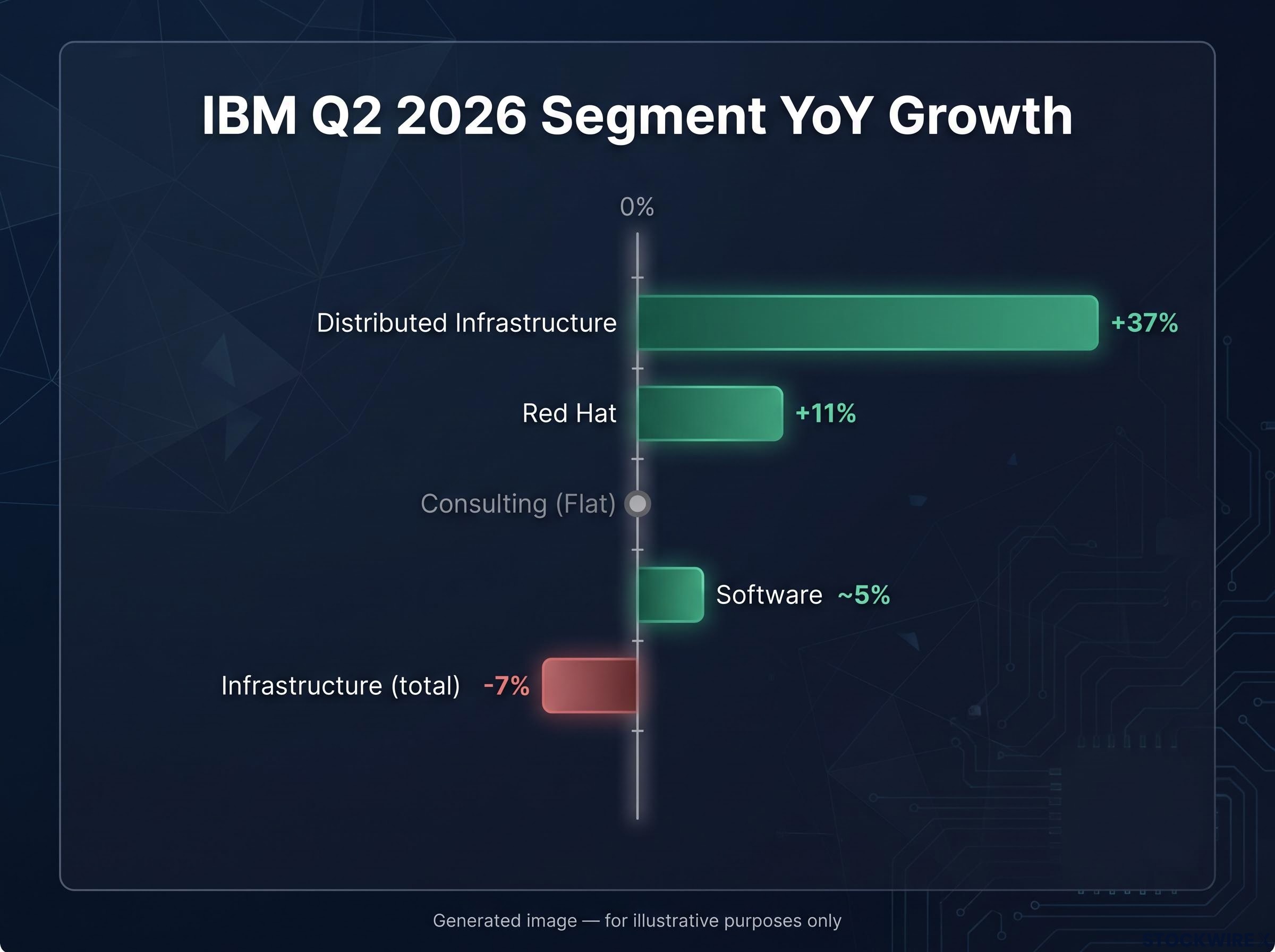

Red Hat posted accelerating revenue growth of 11% year over year. The broader Software segment recorded a gain of approximately 5%. Both figures indicate that hybrid cloud and AI platform adoption continues to produce results.

Distributed Infrastructure delivered what was arguably the quarter’s sharpest contrast, recording a 37% year-over-year gain that represented the segment’s best result in its reported history. IBM‘s own infrastructure business benefited from the same hardware spending wave that hurt its software lines.

AI infrastructure spending winners in the same quarter include Lenovo, whose Infrastructure Solutions Group grew revenue 37% year-on-year and crossed into sustainable profitability, illustrating that the hardware spending wave IBM’s software lines lost budget share to produced concrete earnings results elsewhere in the enterprise technology stack.

| Segment | Q2 2026 YoY Growth |

|---|---|

| Software | ~5% |

| Red Hat | +11% |

| Consulting | Flat |

| Infrastructure (total) | -7% |

| Distributed Infrastructure | +37% |

On a programme-to-programme comparison with the z16, the z17 mainframe was tracking at close to 130% of the predecessor cycle’s adoption pace at an equivalent stage. If customers are adopting the new generation faster than the previous one, the underlying demand signal is intact. The Q2 deferral looks more like timing than defection.

The central debate: one bad quarter or a new budget reality?

Both sides of this argument have specific evidence behind them, and the honest answer is that the verdict cannot be reached today.

The bull case centres on deferral, not cancellation. The z17 is being adopted at 130% of the z16 pace. First-half free cash flow of $4.8 billion shows the model’s resilience. Panic memory buying normalises once supply fears ease, and the revenue and margin profile reverts. If management confirms this on 22 July, a sentiment-driven 19% selloff in a Dow component could look like an overreaction.

The bear case is that AI infrastructure, GPUs, servers, networking, HBM, DRAM, permanently claims a larger share of enterprise capital budgets. If CIOs treat software renewals and mainframe refreshes as flexible line items that can be deferred repeatedly, IBM‘s highest-margin franchises face a structural growth ceiling, not a timing dip. Cybersecurity-related procurement delays add a second compounding source of uncertainty, increasing the probability that “deferred” deals get downsized or re-scoped rather than closed at full value.

IBM’s technology roadmap has produced genuine breakthroughs in recent months, including the 0.7nm nanostack chip demonstrated at VLSI 2026, though analysts have consistently noted these milestones represent late-decade revenue events rather than catalysts for the 2026-2028 earnings window.

| Bull Case Signal | Bear Case Signal |

|---|---|

| z17 adoption at 130% of z16 pace | Memory market pressure described as multi-quarter |

| $4.8B first-half free cash flow | Risk that deferred deals get downsized or re-scoped |

| Red Hat accelerating to 11% growth | AI hardware could permanently claim a larger budget share |

Anyone claiming certainty in either direction today is extrapolating from incomplete data. IBM‘s prior full-year guidance called for mid-single-digit constant-currency revenue growth and strong free cash flow. The size and character of any revision on 22 July is where the structural-versus-cyclical question begins to get answered.

What enterprise IT budget reallocation means beyond IBM

IBM‘s Q2 experience is an early, high-visibility example of a tension that is likely to surface at other enterprise software and services companies: when hardware and memory capital expenditure surges, something else in the IT budget gets deferred.

AI infrastructure investment is not purely additive to enterprise IT budgets. It competes directly with existing software renewal cycles, mainframe refreshes, and professional services engagements. Within fixed quarterly budgets, it introduces a genuine zero-sum dynamic.

The budget scramble that hurt IBM in Q2 2026 sits inside a broader pattern: enterprise AI spending governance has not kept pace with AI adoption speed, and companies ranging from Uber to unnamed hyperscaler clients have burned through entire quarterly budgets on AI infrastructure before measurable product outcomes materialised.

The categories most exposed to this reallocation include:

- Software renewals and upgrade cycles

- Mainframe refresh programmes

- Professional services and consulting engagements

The categories that benefited:

- Server and storage infrastructure

- High-bandwidth memory and DRAM procurement

- AI-adjacent networking equipment

Conditions in the memory and hardware markets have been characterised by some observers as potentially lasting several quarters, meaning Q3 2026 earnings season across enterprise technology broadly could surface similar dynamics.

For investors with exposure to enterprise software or IT services companies beyond IBM, this is a sector-level signal worth monitoring, not just an IBM-specific event to file away.

The next major ASX story will hit our subscribers first

Five things to watch when IBM reports on July 22

IBM Q2 2026 Earnings Call: 22 July 2026, 5:00 p.m. ET

The preliminary numbers set the stage. The 22 July call is where the structural question either gets addressed or deepens. Here are the five disclosures that matter most, ranked by signal value:

- Revised full-year revenue and free cash flow guidance. This is the single highest-signal disclosure. IBM‘s prior guidance targeted mid-single-digit constant-currency revenue growth and strong free cash flow. A modest trim with confident language suggests a recoverable timing event. A deep cut or language indicating poor visibility suggests the 19% drop may not fully price the risk.

- Software renewal pipeline and backlog for deferred Transaction Processing deals. Concrete numbers on deferred renewals and expected closure dates will distinguish genuine timing issues from lost business.

- IBM Z order book and refresh cycle penetration. Commentary on whether enterprises are waiting or rethinking mainframe investment altogether will validate or undermine the z17 adoption thesis.

- Management’s characterisation of how long elevated hardware and memory spending will persist. If the read is multi-quarter or longer, the bear case strengthens materially.

- Red Hat growth trajectory. Whether double-digit expansion continues, and what is driving it, will show whether IBM‘s highest-growth platform business is resilient to the broader budget pressure.

That guidance revision will do more to determine IBM stock’s direction over the following 30 days than anything else on the call. Investors who have these five checkpoints ready can evaluate the disclosures as they arrive, rather than waiting 24-48 hours for analyst consensus to form.

What the July 22 call must answer before the verdict on IBM stock is in

The 19% drop reflects genuine uncertainty, and that uncertainty is rational. The data contains real grounds for both recovery and concern, and the question of whether this budget reallocation is cyclical or structural will not be resolved by today’s preliminary numbers.

First-half free cash flow of $4.8 billion says the underlying model is functional. The z17 at 130% of z16 adoption pace says mainframe demand is delayed, not destroyed. But neither data point answers the more difficult question: whether AI hardware permanently claims a larger share of the enterprise IT wallet.

The 22 July call is the actual decision point. If management delivers stable backlog data, guidance maintained or modestly trimmed, and continued Red Hat acceleration, the selloff begins to look like a recoverable overreaction. If the revision is deep and visibility is described as poor, the structural concern gains real evidence behind it. Until then, the most useful investor posture is to hold the data that matters, watch for the specific disclosures that resolve the question, and resist drawing a premature verdict from price action alone.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.